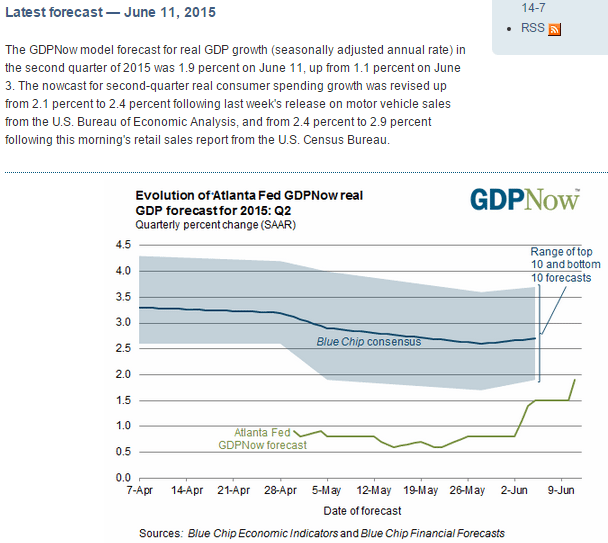

At the beginning of 2013 the US let the FICA tax reduction and some of the Bush tax cuts expire and then in April the sequesters kicked totally some $250 billion of proactive deficit reduction. This cut 2013 growth from what might have been 4% to just over half that, peaking in Q3 and then declining to negative growth in Q1, due to the extremely cold winter. Forecasts were for higher growth in 2014 as the ‘fiscal headwinds’ subsided. GDP did resume after the weather improved, though not enough for 2014 to look much different from 2013. And with the fall in the price of oil in Q4 2014, forecasts for Q1 2015 were raised to about 4% based on the ‘boost to consumers’ from the lower oil prices. Instead, Q1 GDP was -.7%. The winter was on the cold side and the consumer had been saving instead of spending the savings from lower gas prices. And the forecasts for Q2 were for about 4% growth based on a bounce back and consumers now spending their gas savings. Most recently Q2 forecasts have been reduced with the release of Q2 data.

My narrative is that we learned the extent of capex chasing $90 in Q4 after the price fell in half. It seemed to me then that it had been that capex that kept 2013 growth as high as it was and was responsible for the bounce from Q1 2014 as well as the continued positive growth during 2014 up to the time the price of oil dropped and the high priced oil related capex came to a sudden end.

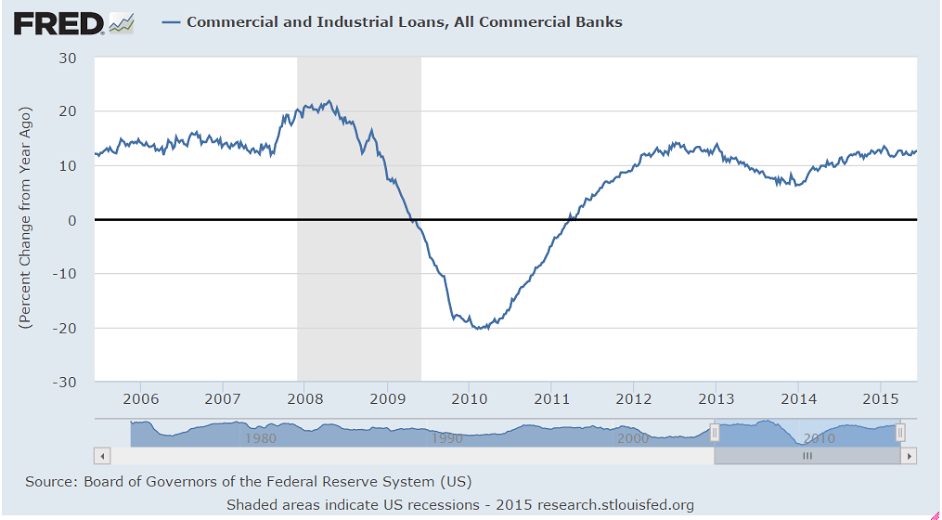

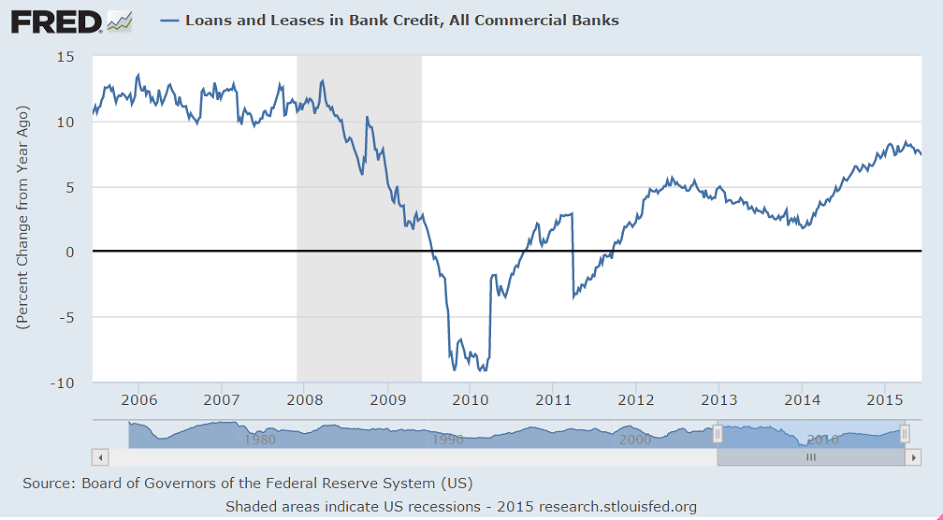

By identity if any agent spend less than his income another must have spent more than his income or the output would not have been sold. So for 2012 the output was sold with govt deficit spending where it had been, and when it was cut by some $250 billion in 2013 some other agent had to increase it’s ‘deficit spending’ (which can be via new debt or via depleting savings) or the output would have been reduced by that amount. Turns out the increase in oil capex was maybe $150 billion for 2013 and again in 2014, best I can tell, and this was sufficient to keep the modest growth going while it lasted. And when it ended in Q4 that spending (plus multipliers) ended as well, as evidenced by the sudden decline in GDP growth. And so far the Q2 numbers don’t look like they’ve increased much, if any, since Q1. And to do so will take an increase in ‘borrowing to spend’ that I can’t detect. Of course, I missed the surge in oil capex last year, so there could be something this year I’m missing as well.

When oil prices dropped I pointed out three things-

1. Income saved by buyers of oil equaled income lost by sellers, so the benefit to total spending was likely to be small and could be negative, depending on propensities to save and to spend on imports. And yes, some of the sellers of oil were ‘non residents’, but that was likely to reduce US exports, and cuts in global capex could reduce US exports as well.

2. Lost capex was a direct loss of GDP, plus multipliers, both domestically and globally.

3. Deflation in general is highly problematic for lenders, and tends to reduce private sector credit expansion in general.

To me this meant the drop in oil prices was an unambiguous negative. And in the face of universal expectations (including the Fed) that it was a positive, which can be further problematic.

Euro Zone

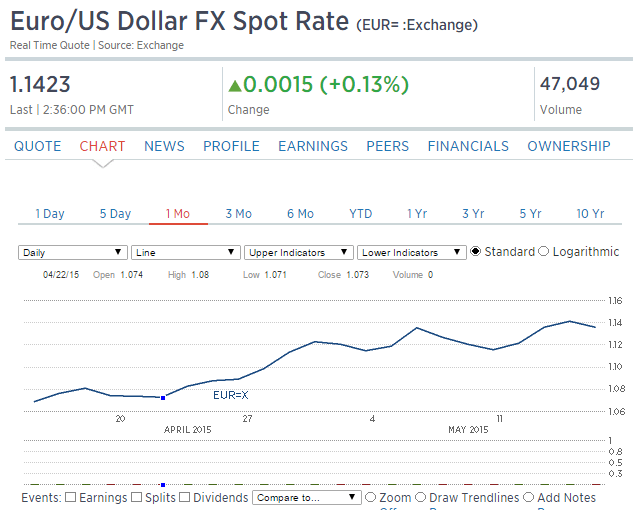

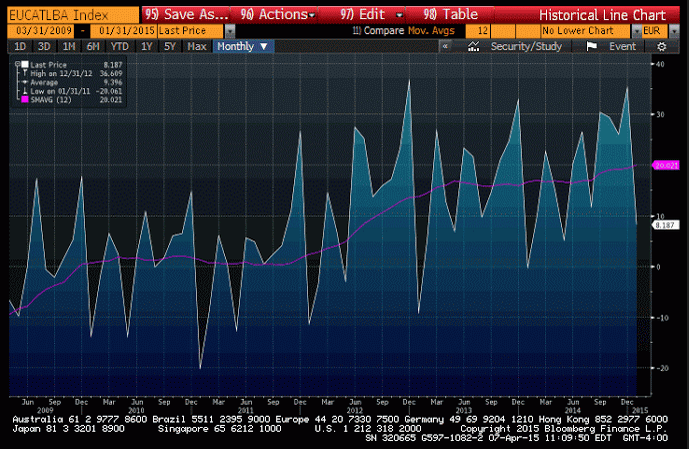

Forecasts are for modestly improving growth largely due to the weak euro driving exports. However, the euro is down from massive foreign CB selling, probably due to fears of ECB policy and the Greek saga. This technical selling drove the euro down and the euro area 19 member current account surplus up, absorbing the euro the portfolios were selling. Once the portfolio selling subsides- which it will as euro reserves are depleted and short positions reach maximums- the trade flows continue, which then drives the euro up until those trade flows reverse. In other words, the euro appreciates until net exports decline and the anticipated GDP growth fades. And there is nothing the ECB can do to stop it, as rate cuts and QE works only to the extent it frightens portfolio managers into selling, etc.

Also, ironically, a Greek default would fundamentally strengthen the euro as Greek bonds are nothing more than euro balances in the ECB system, and a default is a de facto ‘tax’ that reduces the holdings of euro net financial assets in the economy, making euro that much ‘harder to get’ etc.