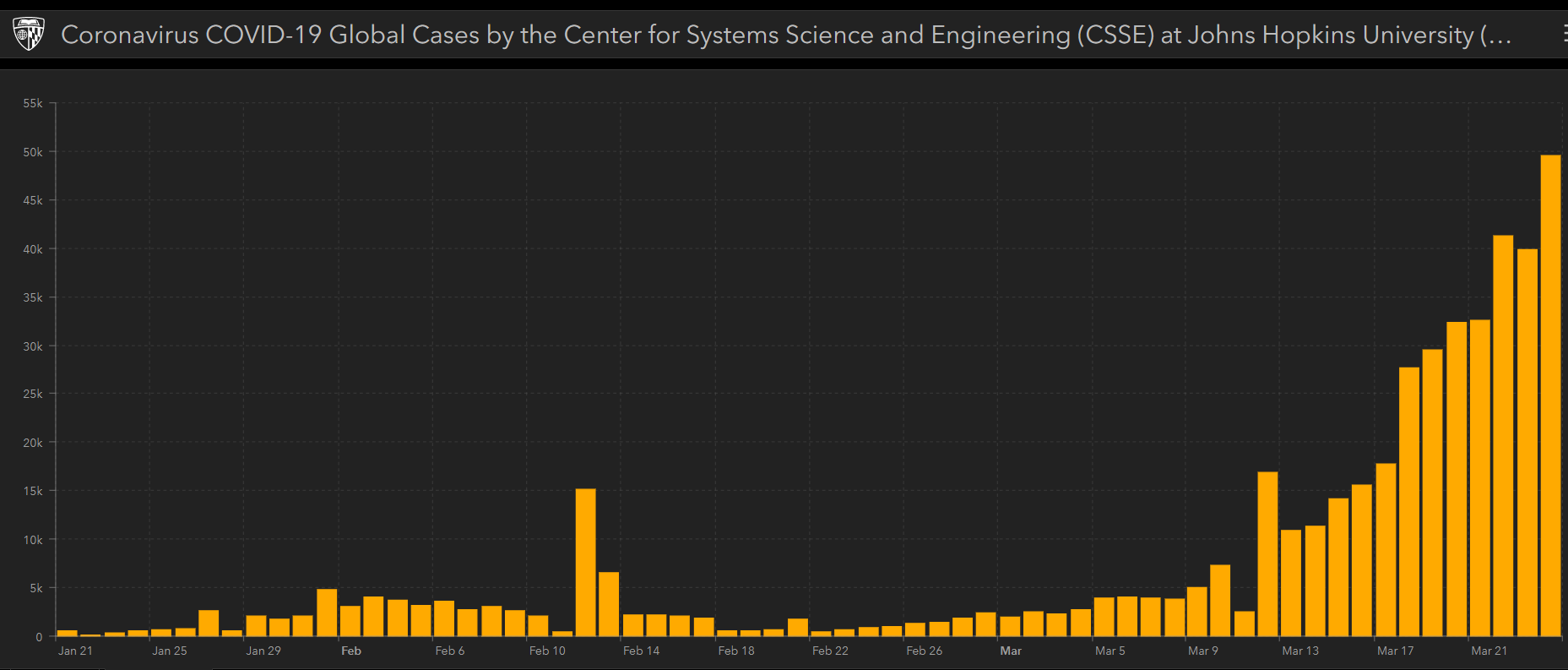

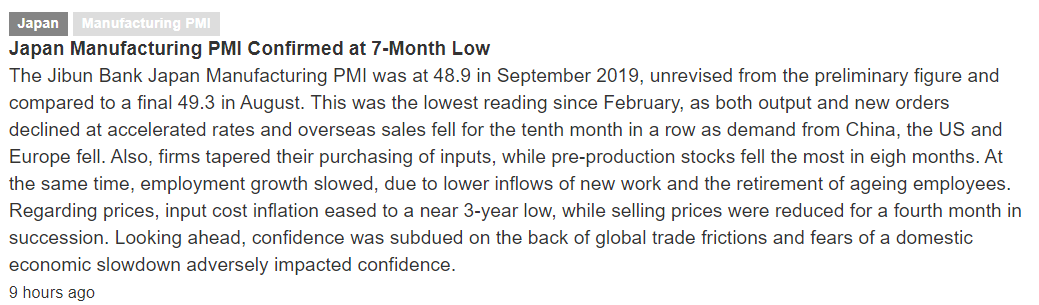

Big spike up:

New daily global confirmed cases growing:

US cases growing rapidly and soon to surpass Italy and China to take the lead globally:

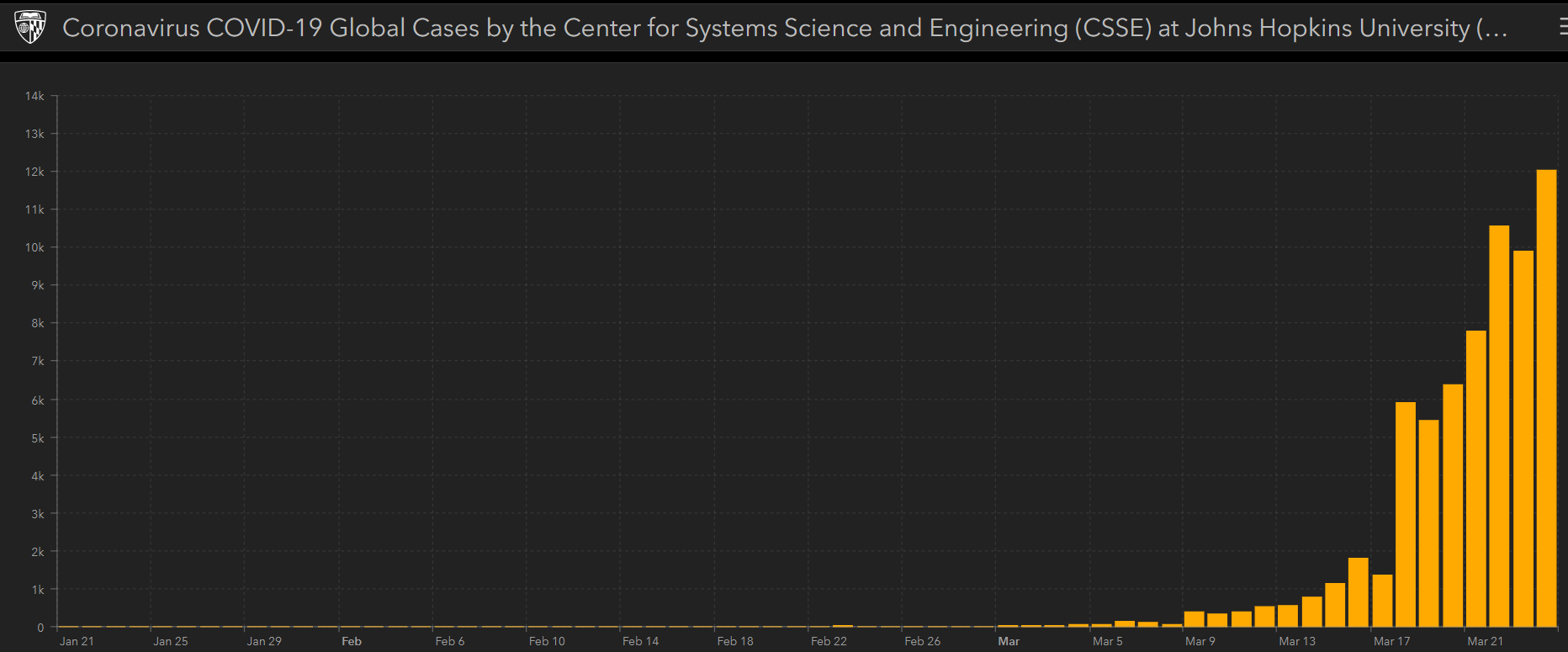

Big spike up:

New daily global confirmed cases growing:

US cases growing rapidly and soon to surpass Italy and China to take the lead globally:

Just a partial recap of today’s releases as the tariff induced global trade collapse continues:

Lots of headlines pointing to corporate weakness:

Amazon sales outlook falls short after record holiday quarter

(Reuters) Fast and free shipping helped the world’s largest online retailer boost revenue by 20 percent. Net income jumped 63 percent to $3 billion for the fourth quarter. Its international operating loss shrunk to $642 million in the quarter from $919 million a year earlier. The company forecast net sales of between $56 billion and $60 billion for the first quarter. Overall, net sales for the fourth quarter were $72.38 billion and beat analysts’ average estimate of $71.87 billion on the back of a strong holiday season, which includes the major U.S. shopping event Black Friday.

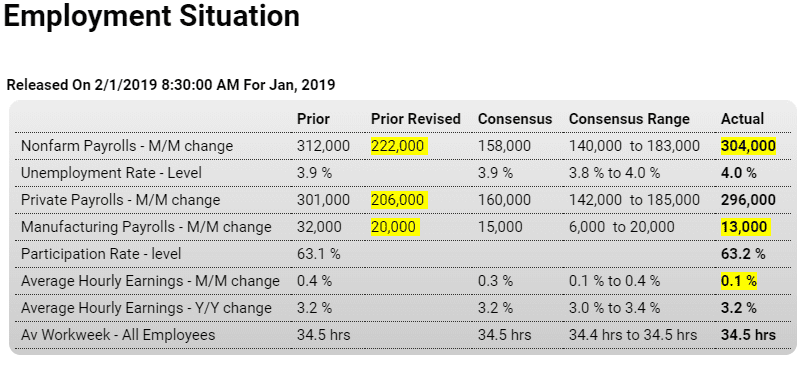

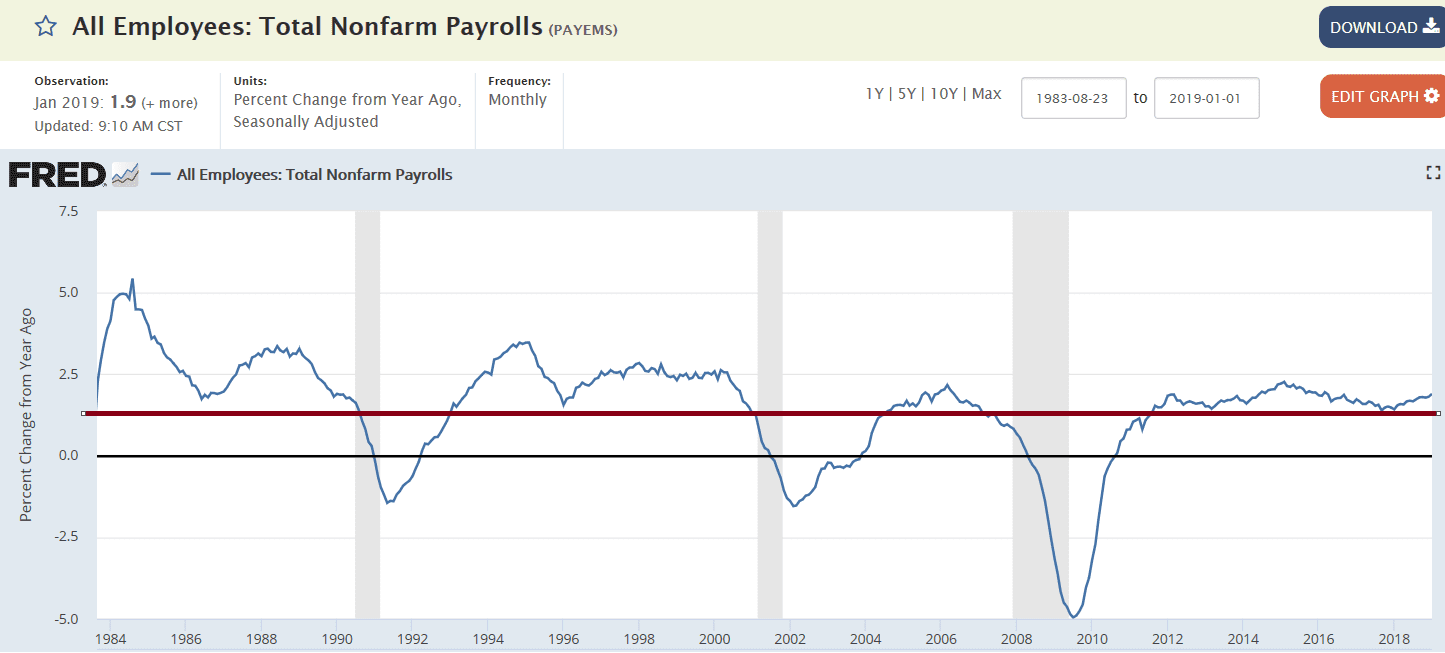

Seems to be holding up as the rest of the global economy is fading fast. The revisions are interesting, best not to judge a number until it’s at least a month old:

Seems to be nudging back up since the tax cuts, or maybe it all gets revised down next month to make it look more like the other indicators?

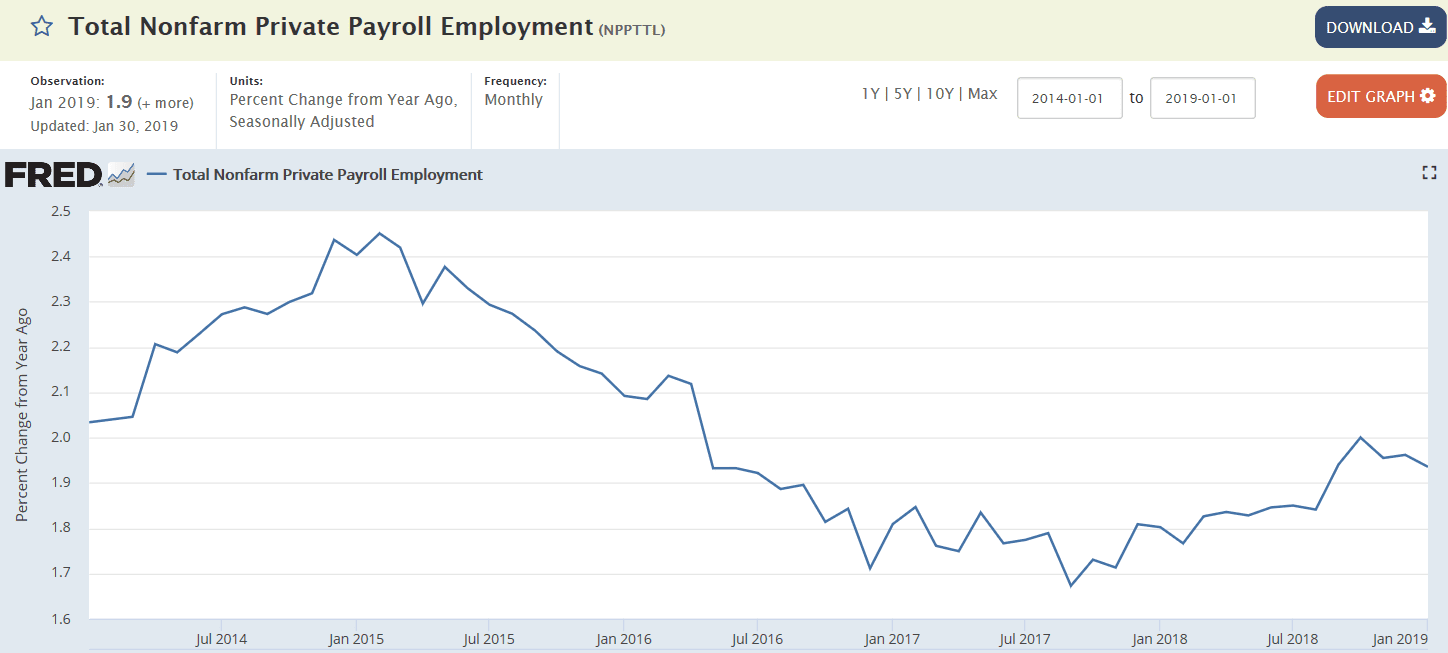

Private payrolls alone tell a somewhat different story:

Looks like no repeal and replace pending:

I think Paul Ryan is trying to pull a fast one on repealing Obamacare

On the surface, it looked like a GOP news conference touting a possible compromise with conservatives to help get the health-care reform bill passed. But House Speaker Paul Ryan and his fellow Republicans really just tipped their hand and admitted their top concern isn’t really repealing and replacing Obamacare, it’s keeping what’s left of the Obamacare exchanges up and running.

Don’t take my word for it. House Energy and Commerce Committee Chairman Greg Walden said it himself when he cheered on the compromise:

“So this is another step in the right direction and I know we’ll keep working forward in this process in the next couple of weeks as we work to refine our product, improve our product, and get to the goal of saving Americans on their premiums, making sure that the Affordable Care Act exchanges don’t fully collapse, we see examples again of more insurers contemplating pulling out of the market, and our job is to try and reform this process in a timely manner.”

Sometimes public purpose demands regulation, regardless of ideology.

One classic example is a football game, where if any one person stands he can see better, but if everyone stands no one can see better and no one can see at all if they are seated. The answer is collective action, where you might have a policy of no one being allowed to stand for more than a few seconds, or something like that.

Likewise, if there are no federal pollution laws, states then compete with each other where whoever allows companies to pollute has the highest inflow of new companies and the lowest personal tax rates. Again, public purpose is served by having national minimums.

That is, there is public purpose in preventing what otherwise would be what’s called a ‘race to the bottom.’

So when dismantling regulation, public purpose is best served by not reinstituting any such races to the bottom, which I have yet to here even discussed.

Somewhat related are moral hazard issues.

For example, since bank deposits are federally insured, which has been shown beyond dispute over time to itself serve public purpose, there is no ‘market discipline’ on the liability side of banking, and therefore the asset side begs full regulation and supervision as the savings and loan debacle of the 1980’s and other periods of lax supervision have repeatedly demonstrated.

Unilaterally announcing we are now the new ‘global police’ raises a few questions?

Seems to me there are at least dozens of serious infractions daily?

‘Holding to account’ and ‘crimes against the innocents’ etc. begs further definition?

Is launching a few missiles to announce displeasure the President’s precedent?

Does this policy require legislative initiative?

And many more.

Looks to me like drawing a line in the sand with your head in the sand?

“The U.S. will stand up against anyone who commits crimes against humanity, Secretary of State Rex Tillerson said on Monday, less than a week after Washington launched missile strikes in response to an alleged Syrian chemical attack.

“We rededicate ourselves to holding to account any and all who commit crimes against the innocents anywhere in the world,” Tillerson told reporters while commemorating a German Nazi massacre committed in Italy in 1944.”

What Does Modern Money Theory Tell us About Demonetisation?

Dec 5 (The Wire) — Warren Mosler, a founder of MMT, explains the idea of “taxes drive money” using a simple example. He pulls out his visiting card in a classroom and …

Continuous flow of this stuff:

Donald Trump insults China with Taiwan phone call and tweets on trade, South China Sea

PR No. 298 PM TELEPHONES PRESIDENT-ELECT USA Islamabad: November 30, 2016

Prime Minister Muhammad Nawaz Sharif called President-elect USA Donald Trump and felicitated him on his victory. President Trump said Prime Minister Nawaz Sharif you have a very good reputation. You are a terrific guy. You are doing amazing work which is visible in every way. I am looking forward to see you soon. As I am talking to you Prime Minister, I feel I am talking to a person I have known for long. Your country is amazing with tremendous opportunities. Pakistanis are one of the most intelligent people. I am ready and willing to play any role that you want me to play to address and find solutions to the outstanding problems. It will be an honor and I will personally do it. Feel free to call me any time even before 20th January that is before I assume my office.

On being invited to visit Pakistan by the Prime Minister, Mr. Trump said that he would love to come to a fantastic country, fantastic place of fantastic people. Please convey to the Pakistani people that they are amazing and all Pakistanis I have known are exceptional people, said Mr. Donald Trump.

Here’s what he said a year or so ago:

Just an FYI, Italy’s 5 Star party, which may take control in the next election, wants to ‘renegotiate terms’ within the EU, including relaxation of fiscal limits, but its ‘Plan A’ is not to leave the euro or the EU.

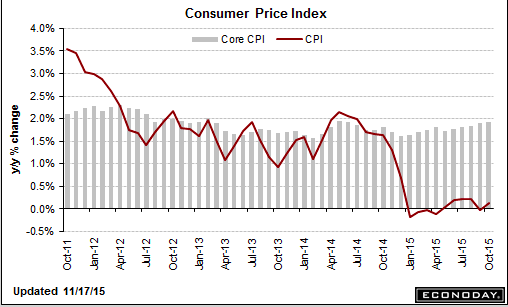

Nothing here to get the Fed concerned about inflation:

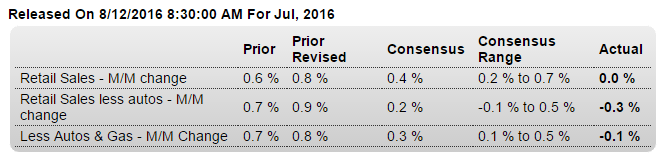

Not good, less then expected and excluding autos, a ‘core reading’ even worse. Seems to me that perhaps the higher gas prices that caused the increases over the last couple of month’s have taken their toll on other spending. And at the macro level, without an increase in either private or public deficit spending top line growth won’t be there:

Highlights

Consumers spent their money on vehicles in July but not on much else as retail sales came in unchanged. When excluding autos, retail sales slipped 0.3 percent for the first decline in this reading since March. When excluding both autos and gasoline, the latter falling on lower prices, retail sales improve slightly but are still down 0.1 percent for the first decline since January. This core reading is telling and will likely define total consumer spending (which includes services) for the month of July.The big plus that saves the report is the 1.1 percent monthly surge in motor vehicle sales, one that follows a 0.5 percent gain in June. Spending elsewhere may be weak, but spending on vehicles is a signal of consumer confidence and strength. Elsewhere, positives are hard to find.

Supermarket sales fell in the month as did building materials. Sporting goods were especially weak as were restaurant sales, the latter a discretionary category that speaks to the month’s lack of non-vehicle punch. On the plus side once again are sales at nonstore retailers which, driven by ecommerce, jumped a sizable 1.3 percent for a second straight month and follows even larger gains in prior months. Sales at gasoline stations, reflecting lower prices, swung 2.7 percent lower following a 2.2 percent gain in the prior month.

The consumer is the driver of the economy and July’s weakness for retail sales makes for a slow start to the third quarter and will ease talk for now of a September FOMC rate hike. Upward revisions are footnotes in the report with June now at plus 0.8 percent, up 2 tenths from the initial reading which will pull GDP revision estimates for the second quarter higher.

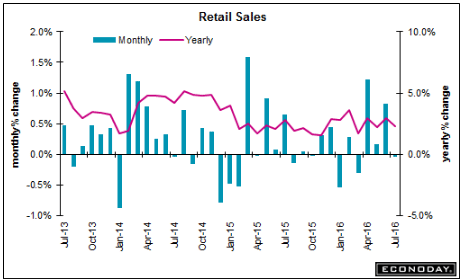

You can see how retail sales growth peaked when oil capex collapsed at the end of 2014,

and that spending has yet to be ‘replaced’:

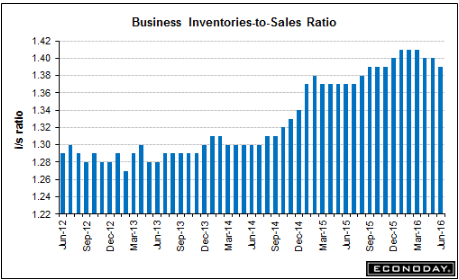

Business inventories corrected some due to what I think was a one time jump in auto sales (which remain down year over year). However inventories still look way too high to me and so the liquidation is likely to continue into q3. And note that the inventory growth began when oil capex collapsed:

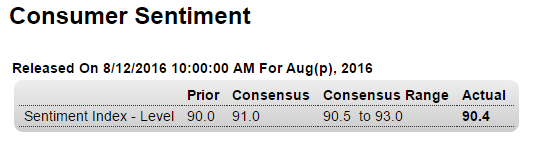

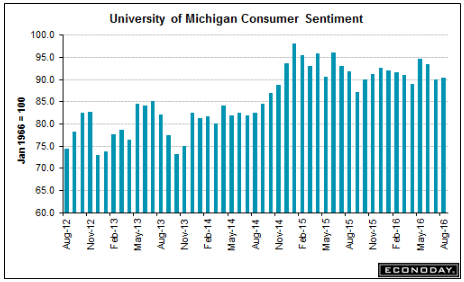

This was also below expectations and doesn’t look to be recovering to prior levels:

Highlights

Consumer sentiment is flat, at 90.4 for the August flash for only a 4 tenths gain. Components are mixed with expectations higher, at 80.3 for a 3.5 point gain, but current conditions lower, down 2.9 points to 106.1. The gain in expectations points to rising confidence in the jobs outlook but the decline in current conditions hints at a second month of slowing for consumer spending.

This too peaked when oil capex collapsed:

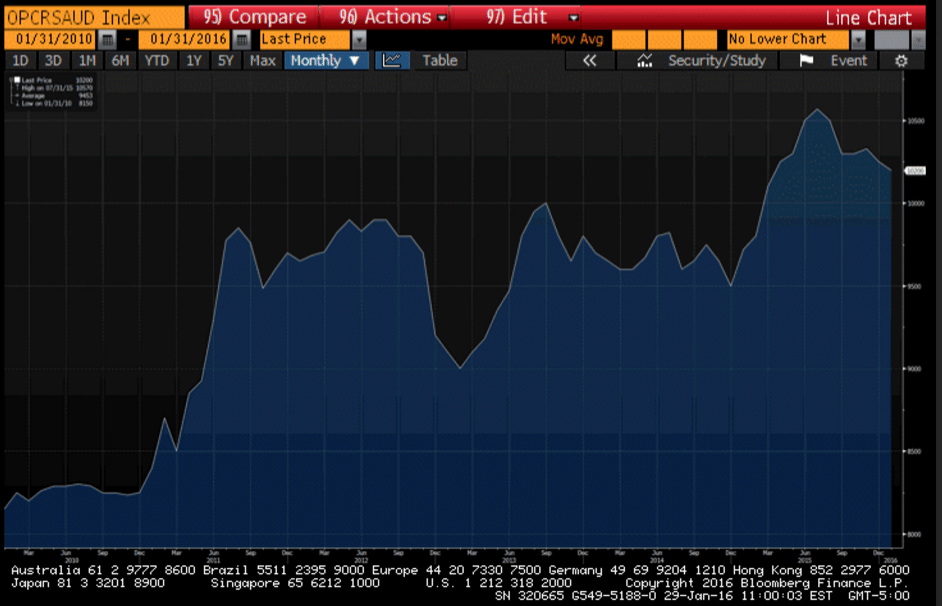

Saudi oil sales have moved up a bit but are still far below their presumed output availability of 12 million bpd. So it’s still a matter of setting price, in this case via their posted discounts to benchmarks:

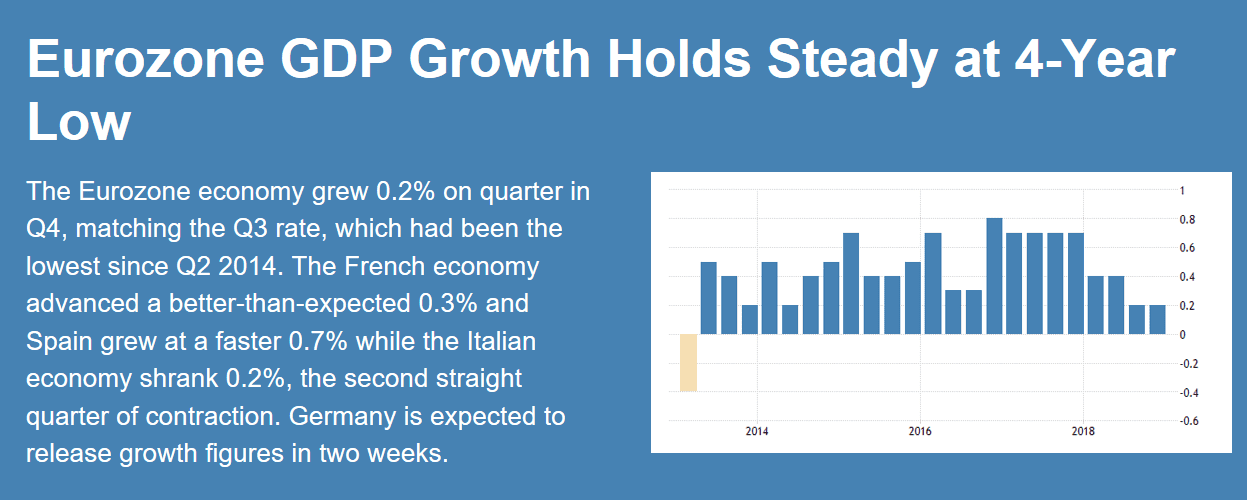

German GDP grows much faster than expected

By Todd Buell

Aug 12 (MarketWatch) — Germany’s economy grew at a much faster pace than expected in the second quarter. In quarterly adjusted terms, Europe’s largest economy and economic powerhouse grew by 0.4%. The statistics office said that growth came primarily from foreign trade. Quarterly growth in the first quarter was 0.7%.

Euro Area GDP Growth Rate

The Eurozone’s economy expanded 0.3 percent on quarter in the three months to June 2016 slowing from a 0.6 percent growth in the previous period and matching preliminary reading, second estimate showed. Among the largest economies of the Euro Area, GDP growth slowed in Germany and Spain; while growth in France and Italy was flat.

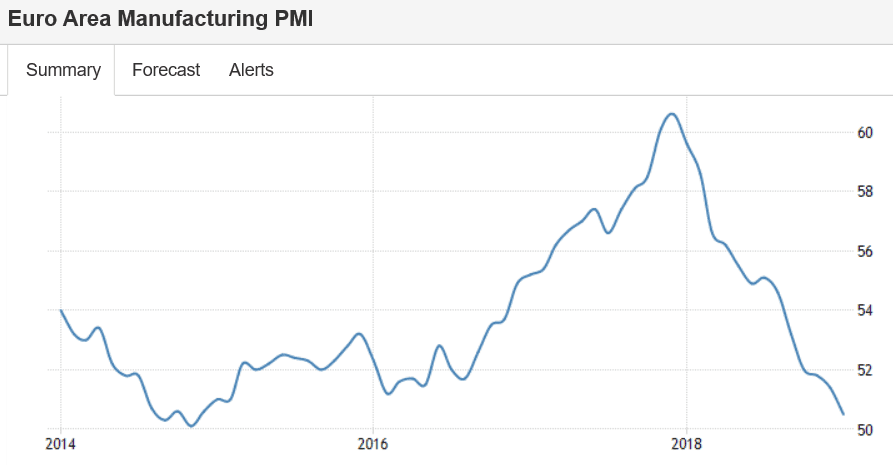

The euro area trade surplus in general seems to be continuing, even as global trade weakens. Fundamentally this removes net euro financial assets from global markets that were sold by portfolio managers. Those managers include central bankers proactively selling their euro reserves over the last two years or so to buy US dollars, which has in turn kept the euro low enough to drive the surplus:

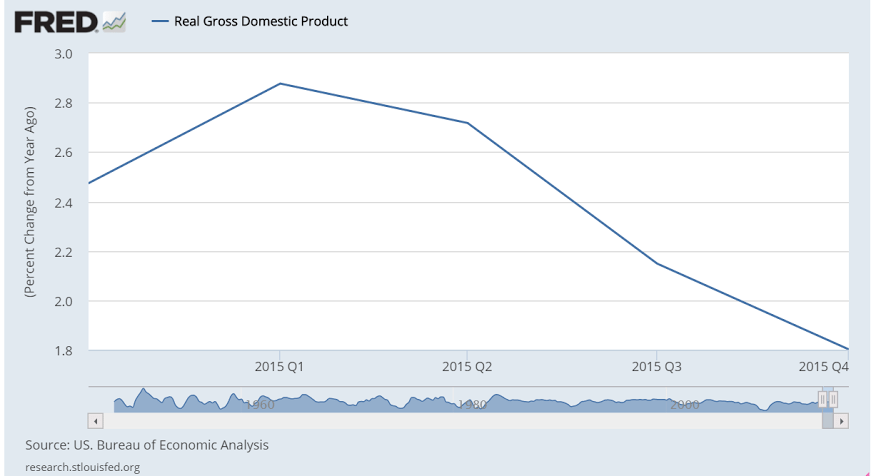

As expected, the deceleration continues, and over the next couple of years it wouldn’t surprise me if the entire year gets revised down substantially:

GDP

Highlights

Consumer spending is the central driver of the economy but is slowing, at least it was during the fourth quarter when GDP rose only at a 0.7 percent annualized rate. Final demand rose 1.2 percent, which is the weakest since first quarter last year but is still 5 tenths above GDP.

Spending on services, adding 0.9 percentage points, was a leading contributor to the quarter as was spending on goods, at plus 0.5. Residential investment, another measure of consumer health, rose very solidly once again, contributing 0.3 percentage points. Government purchases added modestly to growth.

The negatives are on the business side especially those facing foreign markets. Net exports pulled down GDP by 0.5 percentage points. Non-residential investment pulled down GDP by more than 0.2 percentage points. Reduction in inventory investment, which the FOMC warned about on Wednesday, pulled the quarter down by 0.5 percentage points.

Price data are not accelerating, at plus 0.8 percent for the GDP price index which is the lowest reading since plus 0.1 in the first quarter last year. The core price reading is only slightly higher, at plus 1.1 percent which is also the weakest reading in a year.

There are definitely points of concern in this report, especially the weakness in exports and business investment, but it’s the resilience in the consumer, despite a soft holiday season, that headlines this report and should help confirm faith in the domestic strength of the economy.

And this from JPM:

Consumer spending slowed to a 2.2% pace of advance, while business fixed investment spending contracted at a 1.8% rate, the first decline since 2012. A slowing in inventory investment subtracted 0.5%-point from growth last quarter. Even so, the pace of stockbuilding—a $69 billion annual rate—is still faster than is sustainable and poses an ongoing headwind to producers early in 2016. As such, after today’s report we see some more downside risk to our 2.0% projection for Q1 GDP growth.

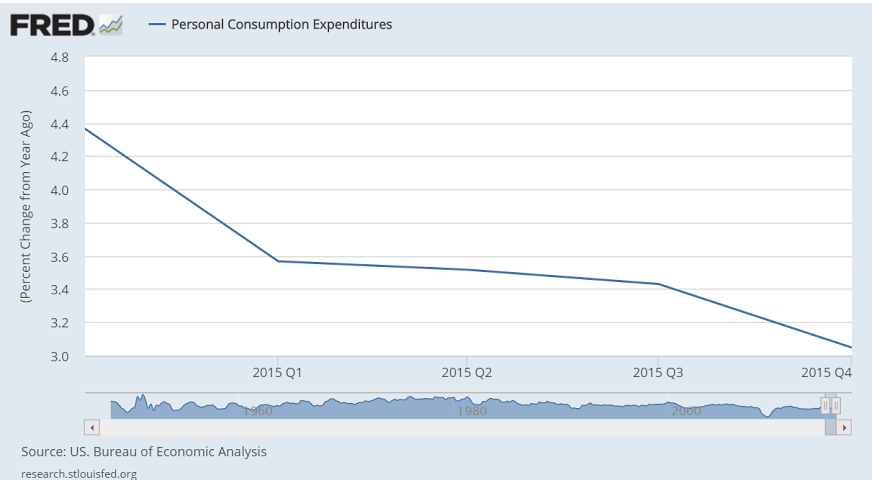

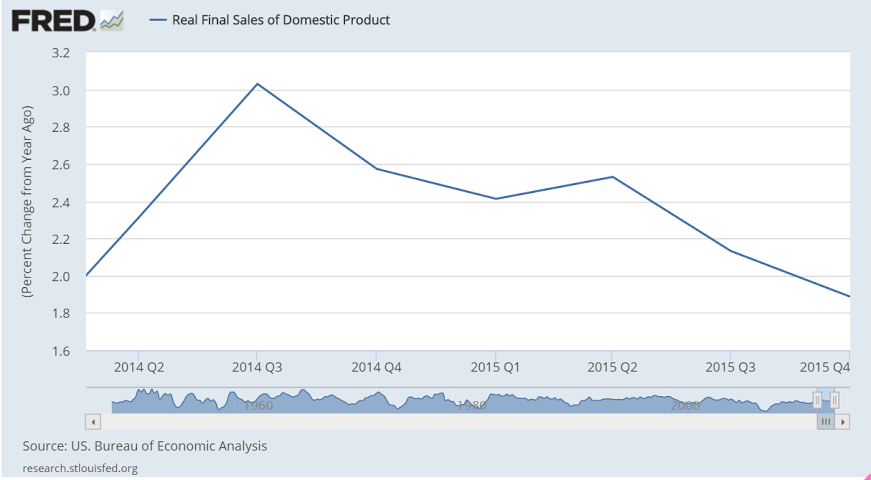

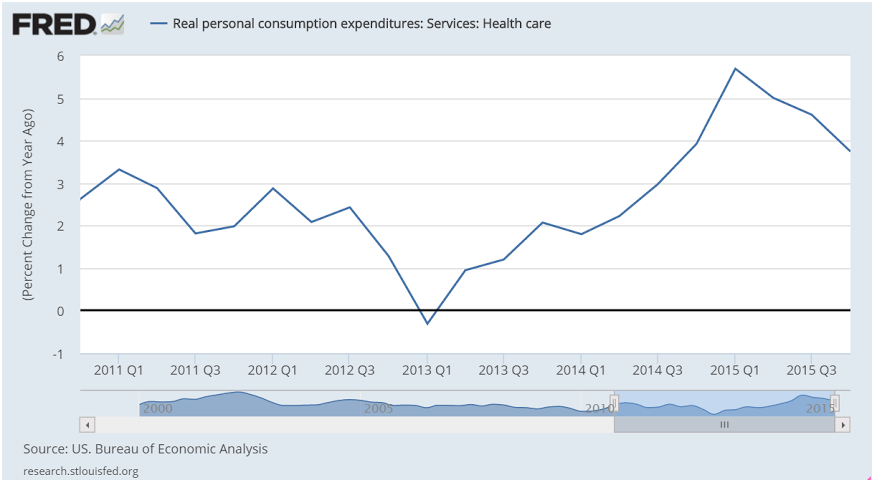

The consumer looks to be going down hill to me, and this includes increases in total health care premiums due to the newly insured under Obamacare. This chart is not adjusted for inflation, which shows the growth of nominal spending has slowed dramatically. Fortunately the ‘deflator’ indicates that with prices down real purchases have been sustained. But consumers on average tend to spend most all of their incomes, which means fortunately for them prices didn’t rise as fast or they would have bought fewer real goods and services.

Here’s the last year of GDP year over year growth, after oil capex collapsed:

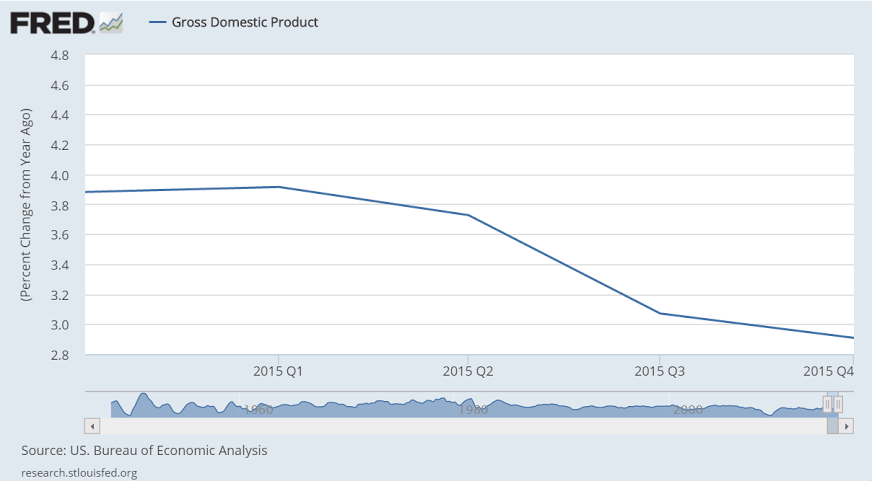

This is nominal GDP, not adjusted for inflation:

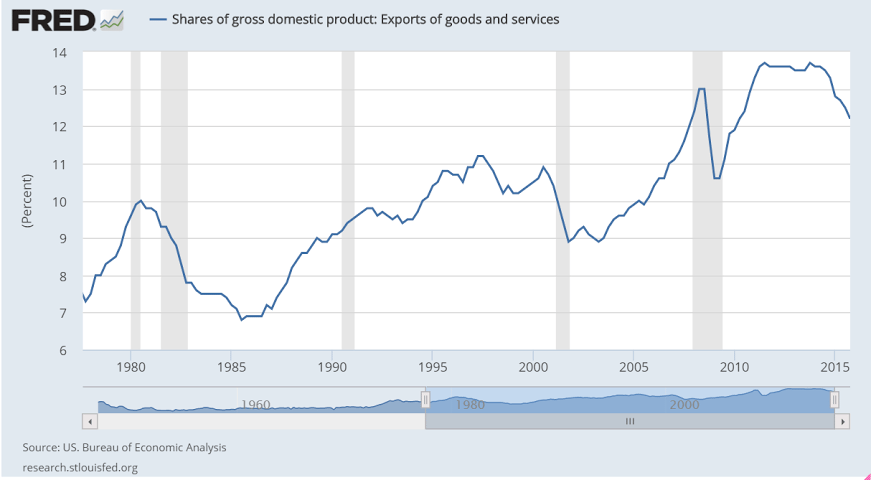

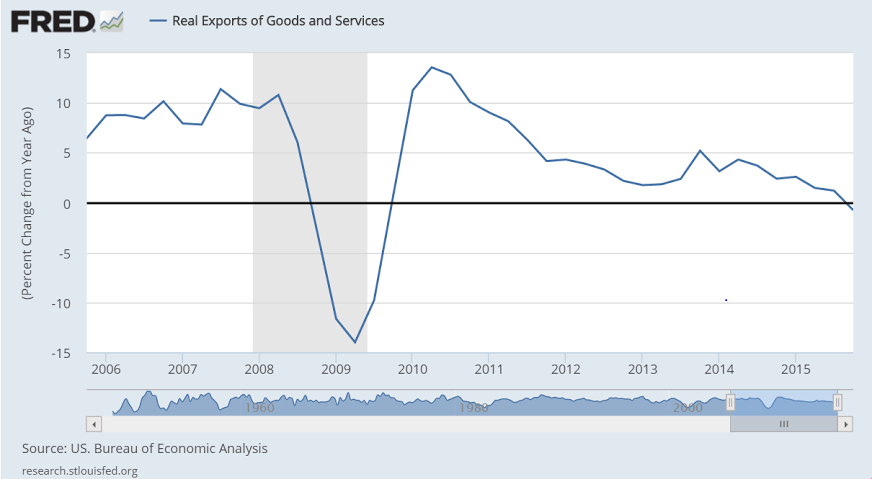

Note the relation between export collapses and recessions:

The increase in premium expenditures for the newly insured is a ‘one time’ event that offered support last year and won’t be repeated this year.

Interesting how even at the dramatically lowered prices due to increased discounts the Saudis appear to be selling less oil. Patiently waiting for March pricing to be released:

Yet another bad one:

Kansas City Fed Manufacturing Index

Highlights

Kansas City manufacturing, along with that of Dallas, are suffering the worst of any regions in the nation’s factory contraction. Kansas City came in at minus 9 for the ninth contraction in 10 months.

Minus signs sweep nearly all readings including new orders and backlogs which are in extremely deep contraction, at minus 27 and minus 36 respectively. Production is at minus 8 with shipments at minus 7. Employment is at minus 7 with price readings moving deeper into contraction, at minus 14 for raw materials and, ominously for inflation expectations, at minus 15 for finished products.

One of the few pluses in the report, ironically, is the index for new export orders which came in at a very modest plus 1. But it’s not only exports that have been pulling down the factory sector but also energy equipment, the latter which is especially sinking the nation’s energy patch.

Chicago PMI: Jan Chicago Business Barometer Jumps 12.7 Points to 55.6

The Chicago Business Barometer bounced back sharply in January, increasing 12.7 points to 55.6 from 42.9 in December, the highest pace of growth in a year.

Chief Economist of MNI Indicators Philip Uglow said, “While the surge in activity in January marks a positive start to the year, it follows significant weakness in the previous two months, with the latest rise not sufficient to offset the previous falls in output and orders. Previously, surges of such magnitude have not been maintained so we would expect to see some easing in February. Still, even if activity does moderate somewhat next month, the latest increase supports the view that GDP will bounce back in Q1 following the expected slowdown in Q4.”

“At current prices U.S. shale producers are losing more than $2 billion a week, according to consulting firm AlixPartners LLP.”

” Italian gross domestic product per capita has hardly changed in 20 years.”

And all they needed was a fiscal adjustment sufficient to get aggregate demand to appropriate levels:

Amari’s fall leaves Abenomics in lurch

Jan 29 (Nikkei) — “I bear responsibility for appointing him,” a visibly pained Abe told reporters Thursday following the resignation of Akira Amari, who also served as his right-hand man in the Trans-Pacific Partnership trade negotiations. Amari devised the basis for Abenomics. He helped alter LDP economic policy’s traditional bias toward public works, shifting the emphasis to a pro-growth strategy of making Japanese companies more competitive and innovative. After Abe led the LDP back to power in 2012, he put Amari in charge of the government’s new industrial competitiveness council and the reconstituted Council on Economic and Fiscal Policy.

Nor will this work, negative rates are just another tax:

BOJ adopts negative interest rates

Jan 29 (Nikkei) — The Bank of Japan decided to adopt negative interest rates at its policy meeting on Friday, voting 5-4 to apply an interest rate of -0.1 percent on current accounts that financial institutions hold at the central bank. At the same time, the BOJ revised its inflation forecast for fiscal 2016 down to 0.8% from a previous level of 1.4%. In a statement, the BOJ said it adopted the negative interest rate policy in order to achieve its price stability target of 2% at the earliest possible time, and signalled that it will “cut the interest rate further into negative territory if judged necessary.”

This might have had something to do with their decision:

Japan’s industrial output falls 1.4% in December, down for 2nd month

Jan 29 (Kyodo) — Japan’s industrial output in December fell a seasonally adjusted 1.4 percent from the previous month, in sharp contrast with a rise of 0.9 percent the government had projected based on hearings with manufacturers last month. The government said the trend of output is fluctuating without clear direction, maintaining its basic assessment of production from the previous month. For 2015, the industrial output index fell 0.8 percent from the previous year. The production index increased 2.1 percent in 2014. Polled manufacturers said they expect output to rise 7.6 percent in January and then fall by 4.1 percent in February.

Part of the Fed’s mandate is to hit it’s 2% inflation target:

Still at recession type levels:

This is also what recession looks like:

The anointed ‘driver of the economy’ continues to falter as previously discussed:

Housing Market Index

Highlights

The housing market index from the nation’s home builders shows weakness, at 62 for November and missing the Econoday consensus by 2 points. And compared to a revised October, the index is down 3 points. Yet readings in the report, though slowing, remain solid and one important detail is favorable.

Of the report’s three components, future sales are down a sizable 5 points but the level is still in the seventies, exactly at 70. Present sales, which is the most heavily weighted component, fell 3 points to 67, also still a strong level.

The positive in the report is a 1 point rise in traffic, a component which, at 48 in the latest report, has been lagging badly but is getting closer to the breakeven 50 mark. Weakness in this reading has been reflecting lack of first-time buyers in the market.

Turning to regional data, the highest composite score goes to the West, at an enormously strong 77, followed by the South, at 62. Two less watched regions for new homes, the Midwest and North, trail at 59 and 52.

There are positives in this report but the decline in both future and present sales is a reminder that both starts and permits for single-family homes have been slowing. Despite the rise in traffic, this report probably pulls back the housing outlook by a degree.

October 2015 Sea Container Counts Continue to Show Trade Recession Continues

By Steven Hansen

The data for this series continues to be in contraction. The year-to-date volumes are contracting for both exports and imports. The trade sector remains in a recession.

Federal agencies don’t need ‘capital’ to function.

This is simply unspent income that reduces aggregate demand:

FHA Meets Minimum Reserve Requirement for First Time Since 2009

(WSJ) — The Federal Housing Administration, which backs low-down-payment mortgages popular with first-time home buyers, said its insurance fund’s net worth at the end of September was $23.8 billion, up from a year-earlier level of $4.8 billion. Its capital reserve ratio, which by law is required to stay above 2%, rose to 2.07%, the first time it met the threshold since the start of the agency’s 2009 fiscal year. With the private subprime-mortgage market largely gone, the agency offers some of the easiest terms available, letting borrowers with a credit score as low as 580 make a down payment of as little as 3.5%.

Passenger car registrations: +8.2% over ten months; +2.9% in October

(ACEA) — In October 2015, the EU passenger car market continued its upward trend, despite a slower rate of increase (+2.9%), marking the 26th consecutive month of growth. Demand for new passenger cars saw momentum slowing down in all major markets. Registrations in Italy (+8.6%), Spain (+5.2%), Germany (+1.1%) and France (+1.0%) kept growing, even though less strong than in past months, while the UK market declined in October (-1.1%). Across the region, new passenger car registrations totalled 1,104,868 units, also supported by growth in the EU’s new member states (EU-12).

Can’t admit fiscal works and monetary doesn’t:

Abe to call for supplementary budget topping 3tn yen

(Nikkei) — Prime Minister Shinzo Abe will direct the Japanese government to put together a supplementary budget totaling more than 3 trillion yen ($24.2 billion) next week to help shore up a flagging economy. The government is set to compile measures to cope with the Trans-Pacific Partnership trade pact on Nov. 25 and steps for promoting active civic engagement on Nov. 26, with both to be incorporated into the extra budget for fiscal 2015. The prime minister declined to characterize the supplementary budget as a stimulus measure, since doing so could be seen as admitting defeat on Abenomics.

Capital spending delays took toll on July-September GDP

(Nikkei) —Weak capital investment led Japan’s economy to shrink by an annualized 0.8% in the three months ended September. A 1.3% drop in capital investment was the main cause of the decline. Corporations had planned to invest a good deal this fiscal year, though the follow-through has been lacking. Machinery orders, which typically lead capital investment by three to six months, slipped 10% for the July-September quarter. But if the outlook for economic growth overseas remains hazy, more companies could put investment on hold.

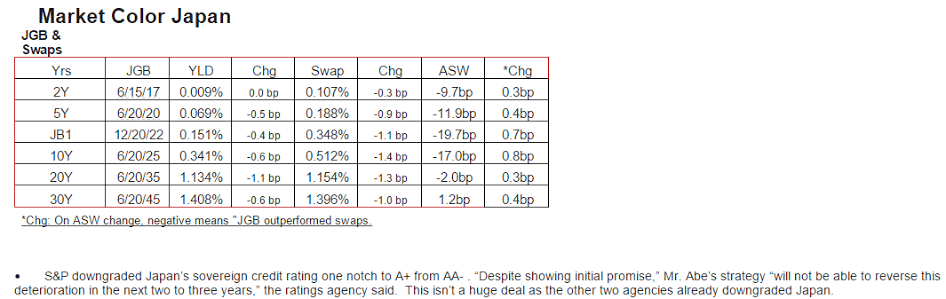

Yields on JGB’s fall a bit with S&P downgrade. I’ve spoken to S&P. They know better. They are intellectually dishonest.

I included these as they give some indication of the macro outlook:

FedEx Trims Outlook on Weak Freight Demand

Sept 16 (WSJ) — FedEx said it expects adjusted earnings of $10.40 to $10.90 a share for the year ending May 31, down from its previous guidance of $10.60 to $11.10 a share. Average daily volume for Ground’s package business grew 4% in the quarter, which was about in line with the company’s expectations. Ground’s operating income slipped 1% to $537 million, while revenue shot up 29% to $3.83 billion in part from the addition of GENCO. For the first quarter ended Aug. 31, FedEx posted a profit of $692 million, or $2.42 a share, up from $653 million, or $2.26 a share, a year earlier. Revenue increased 5% to $12.3 billion.

Oracle Reports Decline in Profits

Sept 16 (WSJ) — Oracle said net income fell 20% in the period ended Aug. 31, but was off only 8% excluding currency effects. Total revenue, off 2%, was up 7% on a constant-currency basis, Oracle said. Oracle said new licenses declined 16% in dollars, or 9% in constant currency. Overall, Oracle reported a profit of $1.75 billion, or 40 cents a share, down from $2.18 billion, or 48 cents a share, a year earlier. Excluding stock-based compensation and other items, profit would have been 53 cents a share, compared with 62 cents a year earlier. Total revenue declined to $8.45 billion from $8.6 billion a year earlier.

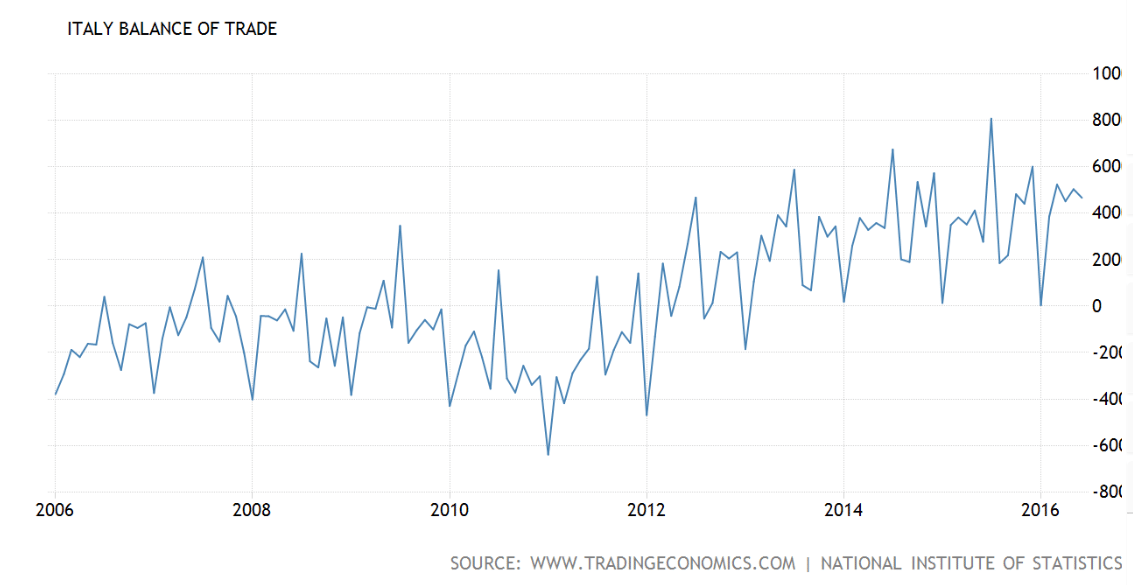

Euro friendly:

Italy : Merchandise Trade

Highlights

The seasonally adjusted trade balance was in a E3.7 billion surplus in July, up from an unrevised E2.6 billion excess in June.

However, the headline improvement masked contractions in both sides of the balance sheet. Hence, exports fell 0.4 percent on the month, their third decline since March but only due to weakness in energy (ex-energy exports grew 0.4 percent). Imports were off a steeper 3.7 percent (minus 4.0 percent ex-energy). Compared with a year ago, exports were up 6.3 percent after a 9.4 percent rise in June and imports 4.2 percent higher following a 12.2 percent gain last time.

The July black ink was more than 6 percent above its average level in the second quarter. This suggests that net exports could provide a boost to real GDP this quarter having been a drag in the previous period.

They talk about the ‘portfolio balance channel’ meaning investors shifting to ‘riskier assets’ due to QE, etc. But at the macro level, it’s about the total ‘risky assets’ available, and it looks like the growth rate is declining:

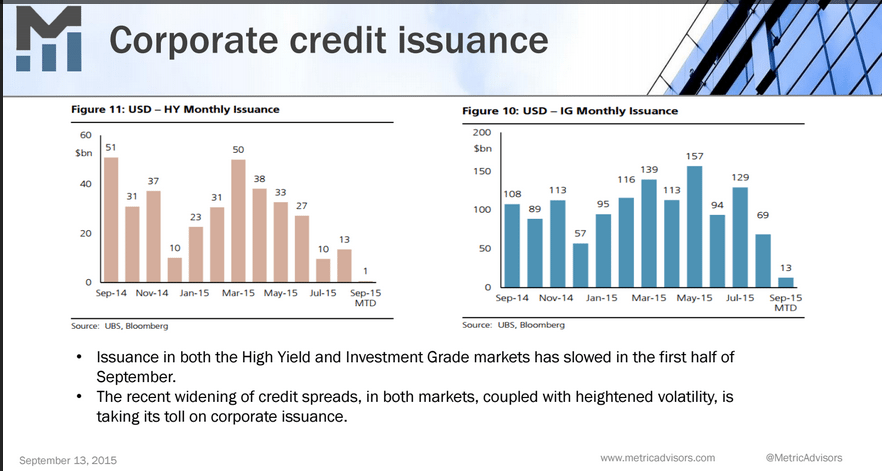

No sign of a burst in issuance here:

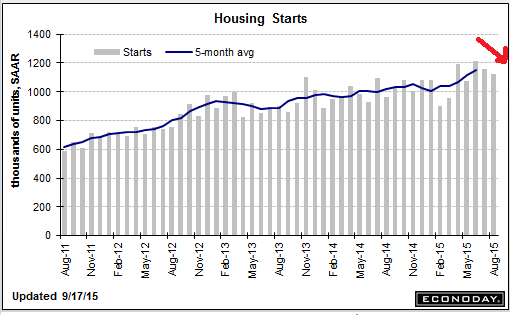

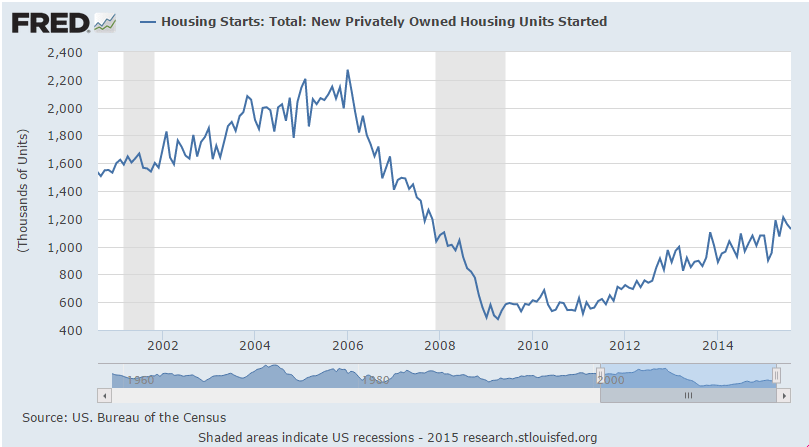

Housing Starts

Highlights

Housing starts fell back in August but not permits which gained and point to strength for starts ahead. Starts fell 3.0 percent in the month to a lower-than-expected 1.126 million annual pace while permits rose 3.5 percent to a higher-than-expected 1.170 million. Starts for single-family homes, like the headline for starts, also fell 3.0 percent in August but follow a 10.9 percent surge in July. Permits for single-family homes rose 2.8 percent in the latest month to 699,000 which is the highest since 2008.

Housing under construction is also at a 2008 high, at 920,000 vs 908,000 in July. But completions were down in the month, from July’s 966,000 pace to a still healthy 935,000.

By region, starts data show increasing strength for the South which is by far the largest region, up 7.1 percent in the month. Permits in the South rose 2.4 percent for a 10 percent year-on-year gain. Permits in the West are the strongest of any region, up 9.6 percent in the month for a year-on-year rate surge of 36 percent.

Revisions to July were mixed with starts revised lower but permits higher. On net, this report is another positive for housing which is proving to be a key sector for the 2015 economy.

Steady progress but still depressed and still well below the lows of the 2001 recession:

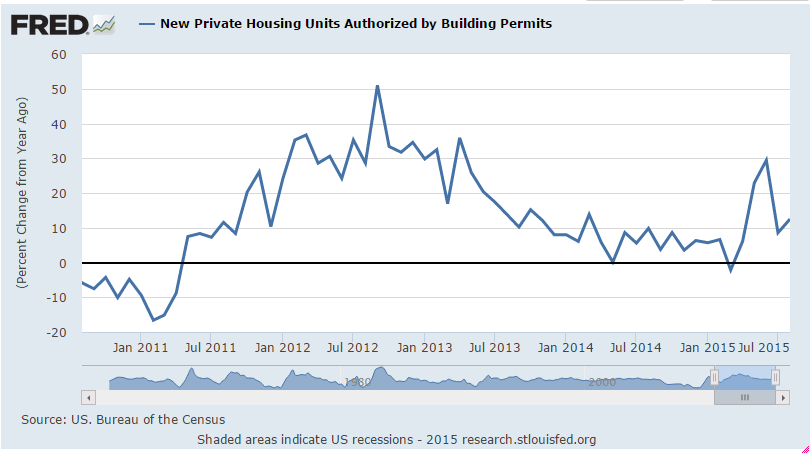

Too soon to tell if the prior spike will be followed by a more serious collapse:

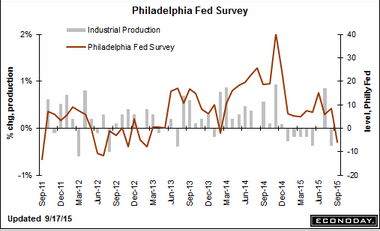

Philadelphia Fed Business Outlook Survey

Highlights

There may very well be something wrong with the manufacturing sector, at least in the Northeast where the Empire State index has been in deep negative ground for the last two months followed now by a minus 6.0 headline for the Philly Fed index. This is the first negative reading since February 2014.

But the headlines for both of these reports, which are not composite scores of separate components, are sentiment scores of sorts, rough month-to-month assessments of general conditions. A key positive in today’s is continued strength in new orders which rose 3.6 points to 9.4. Unfilled orders, nevertheless, have been trending into contraction, at minus 6.6 for the third straight negative reading.

But some details are very strong with shipments at plus 14.8 and employment at plus 10.2 for a 5-month high. In a negative signal also seen in the Empire State report, prices received, that is prices for final goods, is in contraction at minus 5.0.

The Fed is wondering whether global volatility and stock market losses are affecting consumer confidence. Early data this month from regional Feds suggest the effects may also be extending to business sentiment.

Rail Week Ending 12 September 2015: Tremendous Unimprovement After Previous Week’s Improvement

Sept 17 (Econintersect) — Week 36 of 2015 shows same week total rail traffic (from same week one year ago) collapsed according to the Association of American Railroads (AAR) traffic data. Intermodal traffic significantly declined year-over-year, which accounts for approximately half of movements. and weekly railcar counts continued in contraction. It could be that the data last week was screwed up – and the data this week was an adjustment.

And so how good can the US economy be if the Fed thinks the appropriate fed funds rate is still near 0%?

;)