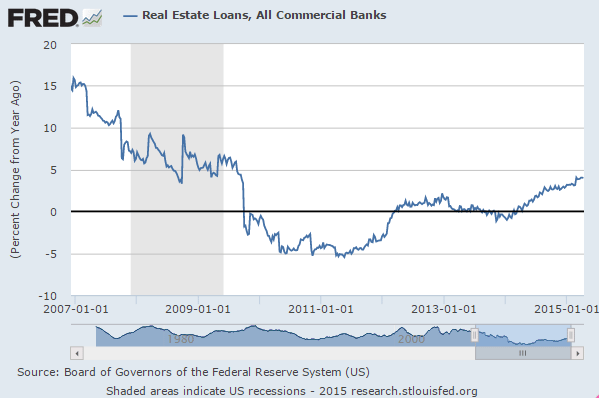

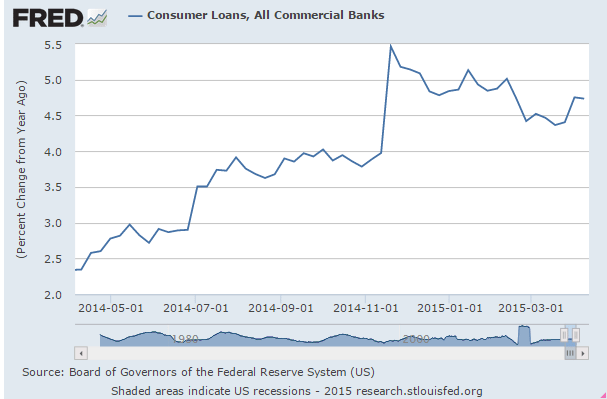

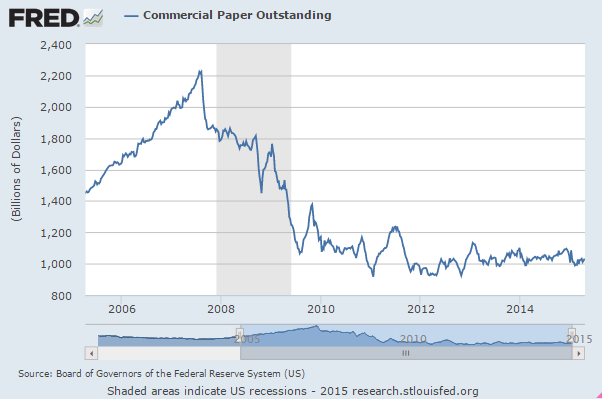

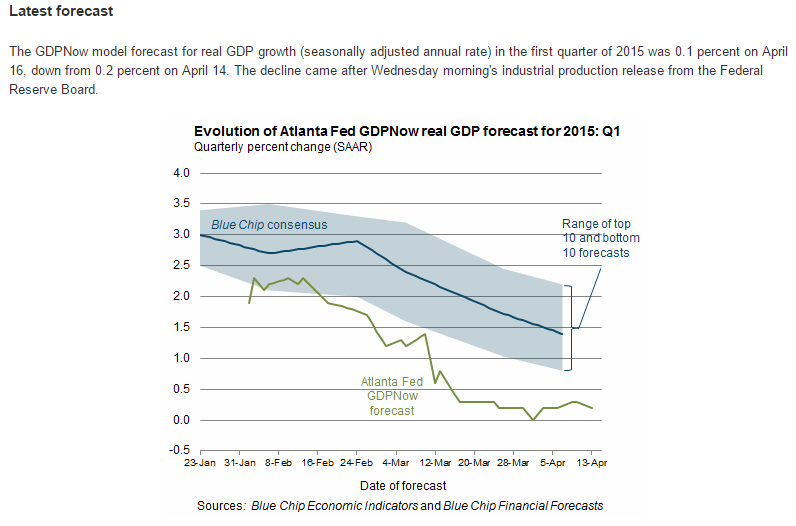

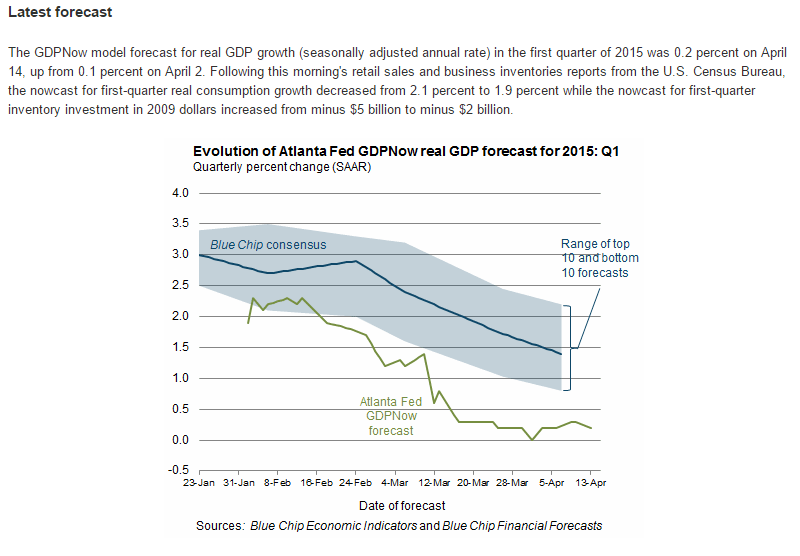

About this time last year I was looking to find signs of the credit expansion needed to ‘replace’ the cuts in Federal deficit spending and couldn’t find anything. Turns out it was the expanded investment chasing high priced oil that supported GDP growth of a bit over 2%. With that now behind us, and most every indicator in decline and with many GDP estimates now below 1%, I’m again looking for signs of a credit expansion capable of supporting positive growth, and so far, if anything, it looks to be going the other way.

And the latest from the Atlanta Fed isn’t encouraging

Author Archives: WARREN MOSLER

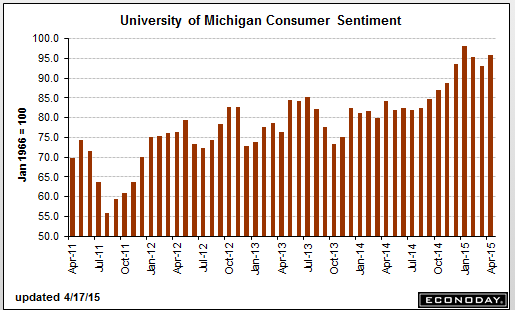

Michigan Consumer sentiment, CPI, Texas employment, rail traffic, apartment market

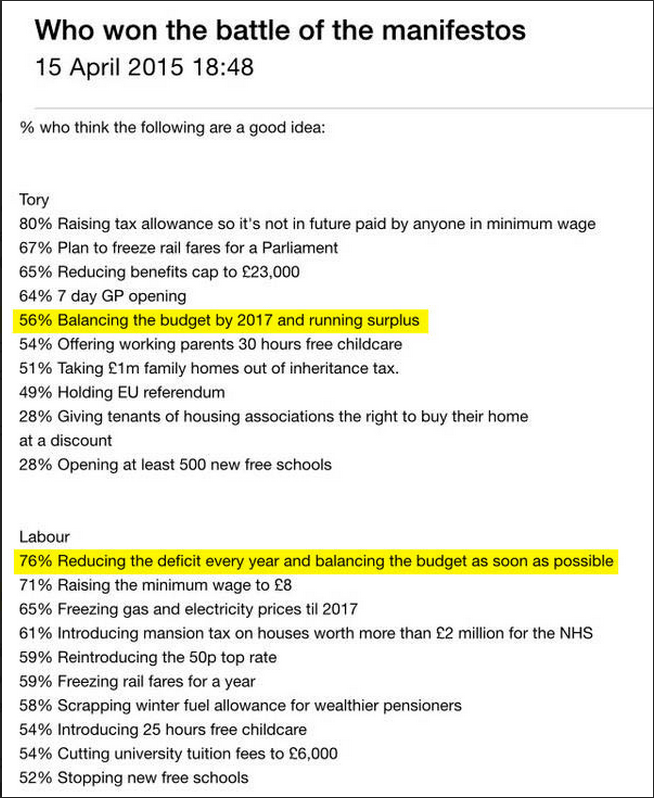

Again, this is one man one vote, not one dollar one vote:

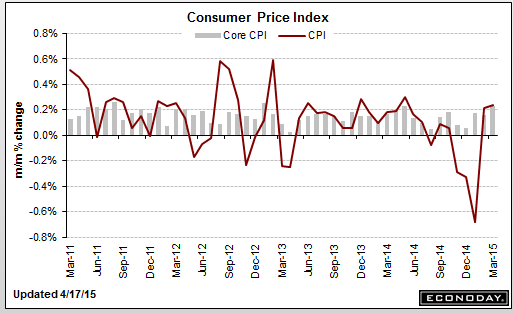

Consumer Price Index

Highlights

Higher energy prices coming up from low levels boosted the CPI. But the trend is still soft. Overall consumer price inflation rose 0.2 percent after rebounding 0.2 percent in February. The March figure equaled analysts’ forecast for a 0.2 percent gain. Energy increased 1.1 percent after gaining 1.0 percent in February. Gasoline prices increased 3.9 percent after rebounding 2.4 percent in February after plummeting 18.7 percent in January, Food slipped 0.2 percent after rising 0.2 percent in February. Excluding food and energy, consumer price inflation posted at a 0.2 percent increase, following a 0.2 percent rise for February. Analysts forecast a 0.1 percent gain.

Within the core, along with the shelter index, a broad array of indexes rose in March, including medical care, used cars and trucks, apparel, new vehicles, household furnishings and operations, and recreation. The index for airline fares, in contrast, declined for the fourth time in the last 5 months.

On a seasonally adjusted basis, the headline CPI was essentially unchanged after being down 0.1 percent in February on a year-ago basis. Excluding food and energy, the year-ago rate was 1.8 percent versus 1.7 percent February. Essentially, the trend in inflation is still sluggish and will allow the Fed to not hurry rate increases.

The Texas Workforce Commission reported that non-farm payroll employment in the Lone Star State declined by 25,400 (or -0.22%) on a seasonally adjust basis in March, the first monthly decline since September 2009 and the largest monthly decline since August 2009. Declines were broad-based from an industry perspective, with mining and logging, construction, manufacturing, and the service-producing sectors all experiencing a monthly dip in employment.

Rail Week Ending 11 April 2015: Continued Weakness In Rail Data

(Econintersect) — Week 14 of 2015 shows same week total rail traffic (from same week one year ago) again declined according to the Association of American Railroads (AAR) traffic data. Intermodal traffic, which accounts for half of movements, is growing year-over-year – but weekly railcar counts remain in contraction. Rail traffic remains surprisingly weak.

This still looks reasonably loose to me:

Buy signal?

Mr. Draghi said at the time that “there is no going back to the lira or the drachma or to any other currency. It is pointless to bet against the euro. It is pointless to go short on the euro.”

Housing starts, Italy Merchandise Trade, UK opinion chart, ECB euro policy musings

Moving up some but still relatively low, but as previously discussed,

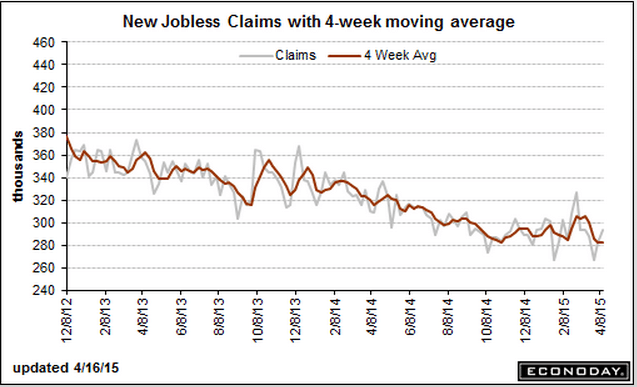

this is about people losing jobs, not new hires:

Jobless Claims

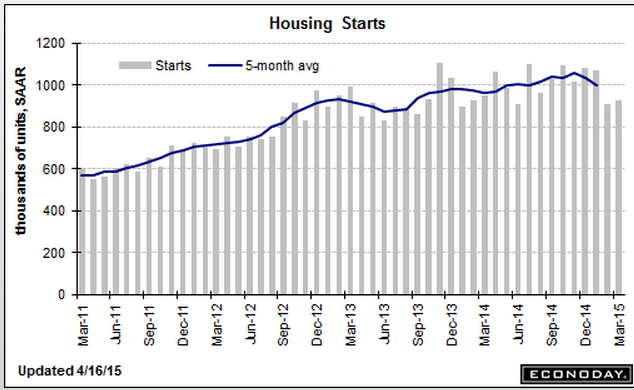

And yet another lower than expected release:

Housing Starts

Just anecdotal evidence of what happens as the euro is pushed down by CB portfolio selling to ‘equate supply and demand’ etc.

Italy : Merchandise Trade

Highlights

The seasonally adjusted merchandise trade balance was in a sizeable E4.6 billion surplus in February, up from an unrevised E3.9 billion excess in January.

The headline gain was attributable to a tidy bounce in exports which, up 2.5 percent on the month, essentially reversed their January decline. Capital goods saw a 7.6 percent rise while consumer goods were up 0.2 percent and energy 2.7 percent. Intermediates fell 0.5 percent. Overall exports were 3.7 percent higher than in February 2014, a marked acceleration versus their minus 4.2 percent January rate.

Low odds of the UK going for fiscal expansion:

Not to forget every Fed member recognizes their role in ‘managing expectations’ as they all believe that the economic performance has a large psychological component. That is, if people were led to believe things were getting worse that would cause a downturn.

Beige Book: U.S. Economy Powers Through Headwinds

By Jefferey Sparshott

April 15 (WSJ) — The U.S. economy continued to expand across most of the country in February and March, though a strong dollar, falling oil prices and harsh winter weather slowed activity in some sectors, according to the Federal Reserve’s latest survey of regional economic conditions. The Fed found modest or moderate growth in eight of its 12 districts. Elsewhere, the pace of economic activity was described as steady, slight or continuing to expand. Minutes of the March meeting showed “several” officials thought June would be the right time, though others said it would be better to wait.

Possible narrative?:

China told Draghi that if the ECB not to go to negative rates and QE or they would retaliate by selling their euro reserves. So Draghi did exactly that to induce a ‘devaluation’ to support EU net exports. The ploy worked, for as long as it lasts. When the CB reserve liquidation fades, the euro will appreciate until the current account surplus turns to a deficit, reversing prior gains in output and employment, and dashing any hoped of growth and employment:

ECB’s Mario Draghi Says Stimulus Is Working

By Brian Blackstone and Todd Buell

April 15 (WSJ) — ECB President Mario Draghi said there is “clear evidence the monetary policy measures we put in place have been effective.” Mr. Draghi said, “The euro area economy has gained further momentum since the end of 2014. We expect the economic recovery to broaden and strengthen substantially.”

German GDP forecasts hiked on weak euro

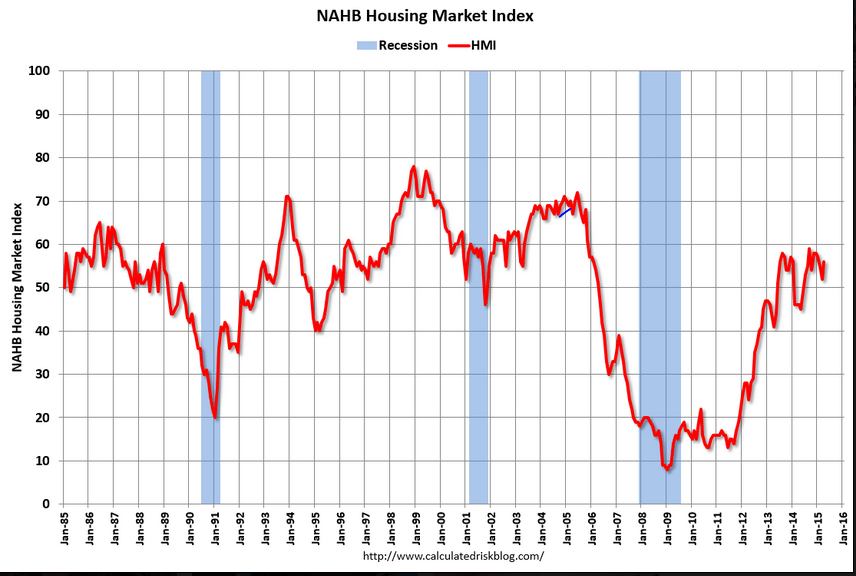

mtg purchase apps, NY manuf survey, industrial production, home builders index

Turned south again, unfortunately. Remains seriously depressed.

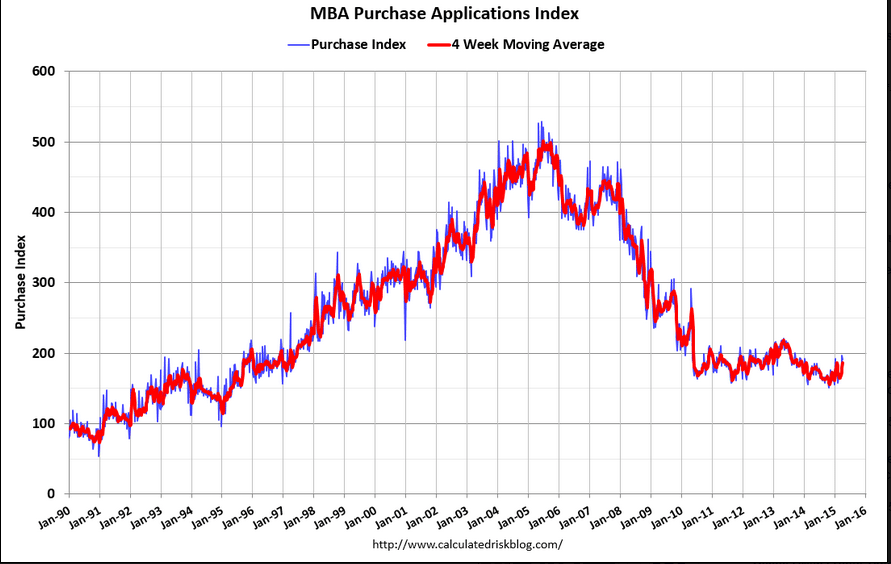

MBA Mortgage Applications

Highlights

After three straight weeks of impressive gains, the purchase index slipped back 3.0 percent in the April 10 week. Year-on-year, the index is still up a solid 7.0 percent in a reading that points to strength for the spring housing market.

More bad news:

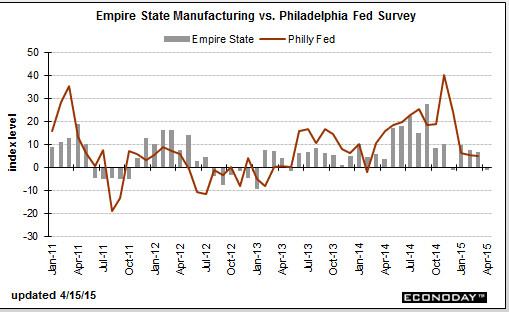

Empire State Mfg Survey

Highlights

There’s no evidence yet that the manufacturing sector is building up steam early into the spring quarter. The Empire State index points to month-to-month contraction for April, at minus 1.19 for only the second negative reading in the last 23 months. The other negative reading was in December which was just about the beginning of this indicator’s slowdown.

New orders are contracting noticeably, at minus 6.00 for the second straight contraction. Weakness in exports, tied to the strong dollar and soft global demand, is a major factor behind the dip in orders. Unfilled orders, at minus 11.70, are in sharp contraction for a second straight month.

But the drop in orders has yet to pull down shipments which, at least for now, are still in the plus column and well into the plus column, at 15.23. Employment is also well into the plus column at 9.57 on top of March’s standout strength of 18.56.

Still, shipments and employment are certain to turn lower if orders don’t pick up. But, in an optimistic note, that’s exactly what the sample sees as a sizable 52 percent expect general conditions to improve in the next six months.

All in all, today’s report is soft reflecting weakness in global demand, weakness underscored by yesterday’s data out of China where GDP is at a 6-year low. Watch for the US industrial production and the latest hard data on manufacturing at 9:15 a.m. ET.

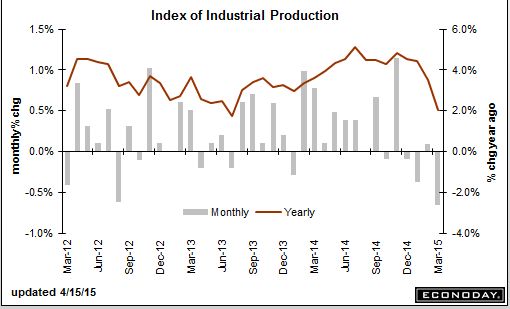

Another bad one:

Industrial Production

Highlights

The manufacturing sector remains sluggish. Industrial production for March fell 0.6 percent after a February rise of 0.1 percent. The March drop was largely due to utilities although manufacturing was soft. Market expectations were for a 0.3 percent fall for overall production in March.

Manufacturing edged up 0.1 percent in March after dipping 0.2 percent the month before. Analysts projected a 0.2 percent increase.

Mining dropped 0.7 percent in March after a 1.6 percent decrease the prior month. Utilities plunged 5.9 percent after surging 5.7 percent in February.

The production of durable goods moved up 0.2 percent, on the strength of a rebound in the production of motor vehicles and parts. The output of primary metals declined 3.2 percent to register the largest loss among durable goods industries. The production of nondurable goods moved up 0.1 percent; decreases in the indexes for paper, for chemicals, and for plastics and rubber products mostly offset gains by the other major nondurables industries. The production of other manufacturing industries (publishing and logging) fell 0.4 percent. The decrease of 0.7 percent for mining reflected a drop of 17 1/2 percent in the index for oil and gas well drilling and servicing that was partly offset by gains in crude oil and natural gas extraction and by a bounce back in coal mining.

Overall capacity utilization declined to 78.4 percent from 79.0 percent in February.

Not terrible but still low historically:

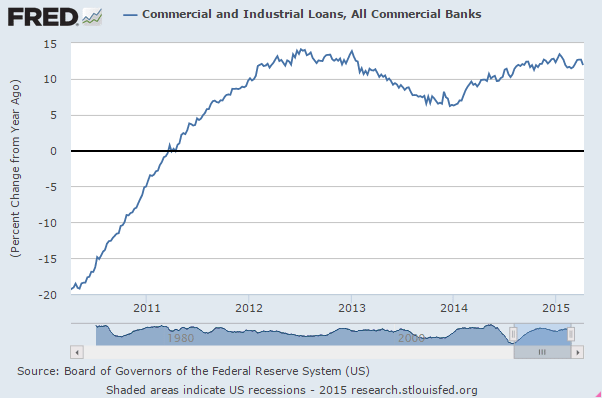

Atlanta Fed, Retail Sales, Redbook retail sales, small business optimism index, business inventories

Another string of lower than expected releases

And 2nd quarter nowcasts are showing about the same as Q1 no bounce yet.

Auto sales have a high import component. Note that reports of domestic wholesale auto output and sales have been lower than expected. And note year over year growth decline, though some of that is lower fuel prices. But of course the lower fuel prices were presumed to translate into higher sales elsewhere…

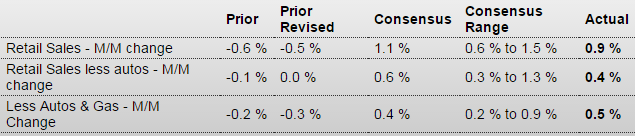

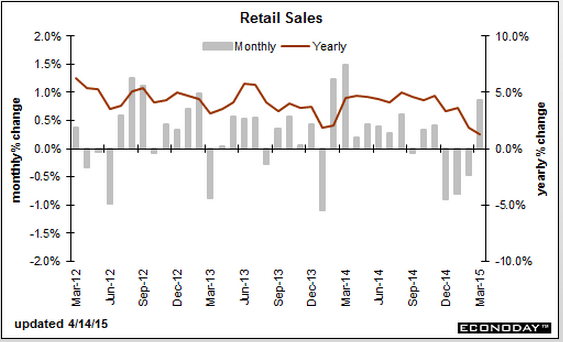

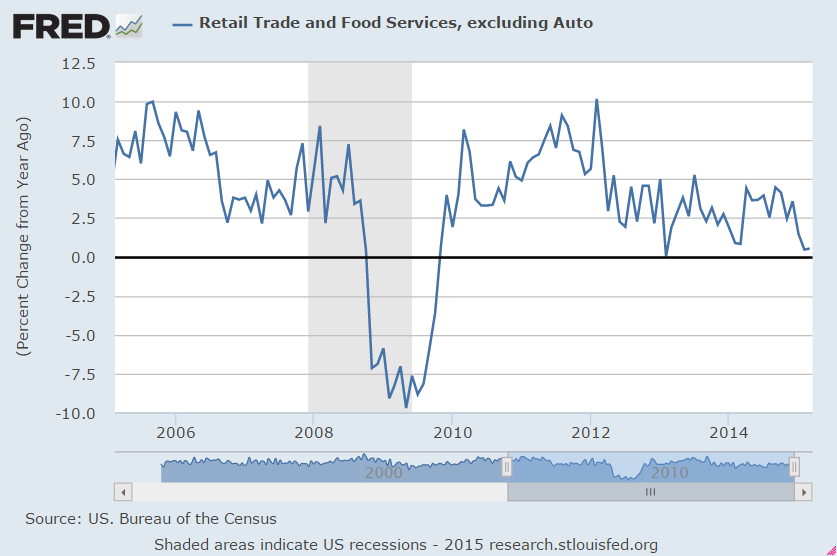

Retail Sales

Highlights

Weather effects may be fading with healthy sales numbers in March. Retail sales in March rebounded 0.9 percent after dropping 0.5 percent in February. The market consensus for March was for a 1.1 percent boost. Excluding autos, sales gained 0.4 percent, following no change in February. Expectations were for a 0.6 percent increase. Gasoline sales dipped 0.6 percent after 2.3 percent increase in February. Excluding both autos and gasoline sales rebounded 0.5 percent after declining 0.3 percent in February. Expectations were for a 0.4 percent increase.

By components, strength was seen in motor vehicles (up 2.7 percent), furniture, clothing, department stores, and miscellaneous store retailers.

On a year-ago basis, retail trade and food service were up 1.3 percent in March, compared to 1.9 percent in February.

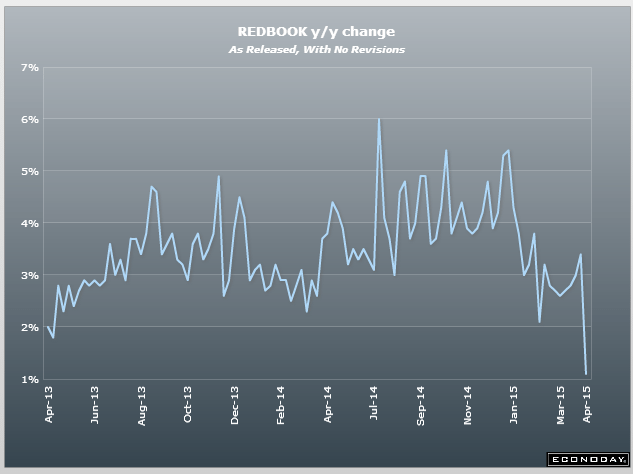

Redbook retail sales chart speaks for itself:

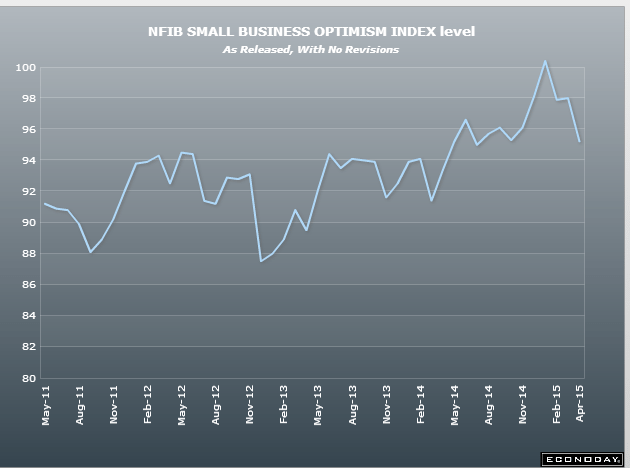

Another series in decline:

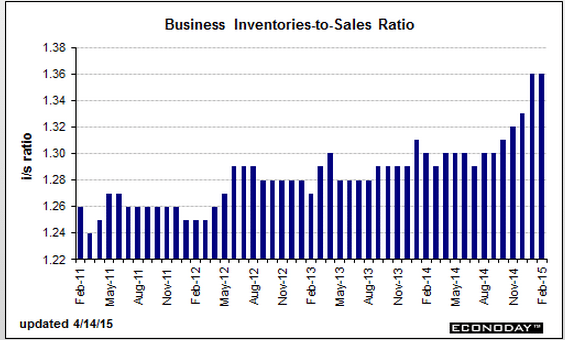

Business inventories remain way high:

Udine presentation

These are the slides of one of my presentations here in Italy.

One of the main points is that the deficit limit functions to limit the euro denominated net ‘savings’ of the economy, with the unemployment the evidence that 3% currently falls short of the ‘demand for savings’.

(Note that when I present it I make the point that ‘savings’ can be held by residents or non residents.)

Udine Presentation

Euro update and anecdotal econ news

This gives you a pretty good idea of the magnitude of euro selling by central banks. The question is when are they finished, and perhaps, when foreign exporters again pressure their cb’s to increase holdings to target the euro zone for exports, which is the reason the cb’s originally bought the euro.

And note that the current account surpluses indicate the EU may be through the ‘j curve’ as net exports continue to move higher with the foreign cb induced currency depreciation.

Of course QE and negative rates continue to work to strengthen the euro, as the does the current account surplus, so it’s just a matter of time before the fundamentals overtake CB selling. The problem is timing… ;)

Euro’s Reserve Status Jeopardized as Central Banks Dump Holdings

By Kevin Buckland David Goodman

April 10 (Bloomberg) — Quantitative easing may be helping Europe achieve its economic targets, but it’s also undermining the long-term viability of the euro by tarnishing its allure as a global reserve currency.

Central banks cut their euro holdings by the most on record last year in anticipation of losses tied to unprecedented stimulus. The euro now accounts for just 22 percent of worldwide reserves, down from 28 percent before the region’s debt crisis five years ago, while dollar and yen holdings have both climbed, the latest data from the International Monetary Fund show.

“As a reserve currency, the euro is falling apart,” said Daniel Fermon, a strategist at Societe Generale SA in Paris. “As long as you have full quantitative easing, there’s no need to invest. The problem for the moment is we don’t see a floor for the currency. Money’s flowing out.”

European Central Bank President Mario Draghi has in the past welcomed the drop-off in reserve managers’ holdings because a weaker exchange rate makes the continent more competitive. Yet firms including Mizuho Bank Ltd. warn the currency’s waning popularity reflects a more lasting loss of confidence in an economy that shrank in two of the past three years.

Sinking Economically

The decline in euro reserves suggests other central banks consider the ECB’s 1.1 trillion euros ($1.2 trillion) of QE bond purchases, which started a month ago, to be the biggest threat to the currency’s global status since its 1999 debut.

Greece’s debt woes aren’t helping, either. The ECB ramped up the emergency funding available to Greek banks Thursday to alleviate the country’s worsening liquidity issues amid drawn-out negotiations over its bailout.

Outright Sales

National Australia Bank Ltd. estimates reserve managers sold at least $100 billion-worth of euros in the fourth quarter of 2014.

“Most of the fall in the euro share represented outright selling of euros” rather than simply reflecting declines in the exchange rate, said Ray Attrill, the bank’s global co-head of currency strategy in Sydney.

Of the $6.1 trillion of reserves for which central banks specify a currency, the proportion of euros fell in every quarter of 2014, IMF data show. Last year was also the first time euro holdings fell in cash terms.

Euro Weakening

Yen holdings increased in three of the four quarters and make up 4 percent of the total, up from as low as 2.8 percent in early 2009. Dollars account for the biggest proportion at 63 percent after reserve managers increased their holdings in the final six months of last year. That’s down from as much as 73 percent in 2001.

The changes came as the yen and euro each sank 12 percent versus the greenback last year. The euro has tumbled about the same amount since then, which should further shrink its presence in central banks’ war chests.

The euro’s also falling against its broader peers, dropping more than 7 percent this year among a basket of its Group of 10 nations tracked by Bloomberg Correlation-Weighted Indexes, the biggest decline in the group. The dollar climbed almost 7 percent on the prospect of higher U.S. interest rates, beating a gain of about 6 percent in the yen.

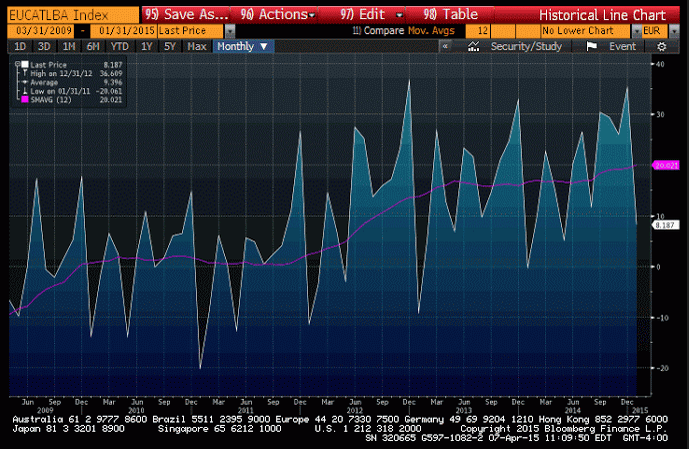

EU current account:

NACM’s Credit Managers Index Drops Even Further in March

The March report of the Credit Managers’ Index (CMI) from the National Association of Credit Management (NACM) fell further this month indicating that some serious financial stress is manifesting in the data.

“We now know that the readings of last month were not a fluke or some temporary aberration that could be marked off as something related to the weather,” said NACM Economist Chris Kuehl. “These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage.”

The combined score of 51.2 is moving dangerously close to contraction zone. The index of favorable factors dropped to 55.4 while the unfavorable factors drastically fell to 48.5–a place this index has not seen since after the end of the recession. “The signal this sends is that many companies are not nearly as healthy as it has been assumed and that there is considerably less resilience in the business sector than assumed,” said Kuehl.

Most categories showed decreases this month, but the real damage occurred in the unfavorable changes categories. According to Kuehl, the most disturbing drop happened in the rejection of credit applications category, which fell from 48.1 to an even weaker 42.9. The accounts placed for collection fell to 49.8, disputes improved slightly to 49, dollar amount beyond terms fell to 45.5, and dollar amount of customer deductions dropped to 48.7.

Rail Week Ending 04 April 2015: Weakness Continues

(Econintersect) — Week 13 of 2015 shows same week total rail traffic (from same week one year ago) again declined according to the Association of American Railroads (AAR) traffic data. Intermodal traffic, which accounts for half of movements, is growing year-over-year – but weekly railcar counts remain in contraction. Rail traffic remains surprisingly weak.

Baltic Dry Index is Now Below the Great Recession Low

By: John O’Donnell

April 11 (Econintersect) — The Baltic Dry Index is considered a coincident and leading indicator for global economic growth. It tracks the cost of shipping bulk commodities around the world. The BDI is now below the level reached during the Great Recession.

from Prof. Terzi

Presentation from Professor Andrea Terzi:

The Eurozone crisis: A debt shortage as the final cause

wholesale trade

Not that it matters but another bad release:

Wholesale Trade

Highlights

Inventories relative to sales in the wholesale sector remained bloated for a 2nd straight month in February, up 0.3 percent vs a decline of 0.2 decline in wholesale sales. The mismatch keeps the stock-to-sales ratio unchanged at 1.29, which is the highest reading since the recession period of June 2009.

Revisions to January are even more unfavorable with the inventory build revised 1 tenth higher to plus 0.4 percent and sales revised even lower to minus 3.6 percent from an initial minus 3.1 percent. January, reflecting a huge price-related downswing in petroleum products, was the worst month for wholesale sales since March 2009.

But it’s more than any one sector as sales declines in the 2 months are spread out broadly through components. Pulling February down the most were electrical goods, machinery, and metals, all pointing to weakness in the industrial economy, weakness perhaps related to declining exports. Wholesale sales of autos were also weak. All these components show bloated gains in their stock-to-sales ratios.

The wholesale sector is the intermediary between manufacturing and retailing, and the signals it is sending tell of weakening demand on the retail side and point to slowing production on the manufacturing side. These of course are negative signals for future employment growth. Watch for the business inventories report on Tuesday which will include an inventory update out of retailing.