First, I’ve been pretty quiet on the mideast goings ons.

I’ve been watching intently from the time Egypt made headlines,

and have yet to see anything of particular consequence to us, beyond oil prices.

I’ve yet to come up with any channel to world aggregate demand, inflation, etc. apart from oil prices.

Seems all moves in stocks and bonds have been linked directly or indirectly only to actual and potential changes in crude oil and product prices.

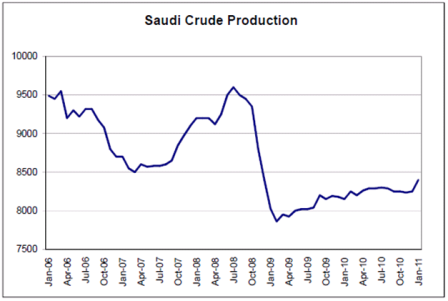

And the mainstream has yet to realize that ultimately the Saudis- the only producer with excess capacity, continues as price setter, at least until their excess capacity is gone.

So the price of crude oil remains set by decree, and not market forces.

And markets don’t yet seem to know that.

Credit the Saudis for outsmarting the world on that score.

They say they don’t set prices, but let the market set price, as they only set spreads to benchmark market prices they post for their refiners.

The world completely misses the simple difference between the Saudi’s reaction function as a price setter, and prices set competitively in the market place.

That’s like the Fed saying they don’t set $US interest rates, because they have a reaction function that guides them.

So what does that mean?

It means the price of crude will come down only if the Saudis want it to come down (assuming they do have excess capacity).

And my best guess is that their survival strategy includes a lower price of oil.

They will play the maestro with grand gesture and international ‘faux diplomacy’ with ‘high level’ behind the scenes goings ons with pledges to come to the rescue with promises of production increases to replace any lost output due to the crisis, making it clear that they are going the extra mile and taking extraordinary measures to ensure the western economies both won’t see any supply disruptions and prices will be contained. Making it clear that we owe them for their selfless, gargantuan, efforts and expenditures of political capital on our behalf.

It’s all a big show to ingratiate themselves to the West in the hopes of getting the western support needed to sustain their position of power.

And the west will never realize that prices went up only because the Saudis raised their posted prices under cover of their reaction function that the west mistakes for ‘market forces,’ and that prices will go down only as the Saudis simply lower their posted prices, as they continue to play us for complete fools.

Much like China does to us because we think we need to sell our Tsy secs to fund our federal spending.

And with lower crude prices we go ‘risk off’ and much of the recent moves in other markets reverse.

The other possibility is that the Saudis don’t cut price, maybe because they decide they want the increased revenues to sustain control domestically with increased distributions to their population.

One way or another, it’s all their political decision, and we don’t even understand how it works, which reduces the odds that whatever influence we might have will be used to our ultimate benefit.

Before the early 1970’s the price of oil was set by the Texas Railroad Commission, who kept it relatively low and stable, fueling growth with reasonable price stability, while govt policy fostered relatively high levels of employment and low output gaps.

Since the hand off to the Saudis in the early 1970’s, when circumstances allowed them to take over as swing producer/price setter, prices have increased dramatically with very high levels of volatility, disrupting the world order and fostering today’s very high levels of unemployment and massive output gaps, as govts struggle with fears of inflation and seemingly no understanding of the process that’s got us into that mess.

And now with the world turmoil perhaps largely a function of mass unemployment, and govts with no idea how to keep that from happening, the pendulum is shifting from order to chaos.