State of the Hedge Fund IndustrySeptember 14, 2010, 1pm-5pm followed by cocktail reception

New York City

Join us as distinguished experts from the hedge fund industry speak candidly about the biggest issues affecting managers today. Speakers will discuss challenges and opportunities in a post-financial crisis world, including the new—more difficult—capital raising environment; what smaller firms can do to ‘institutionalize’ themselves; and how seeding firms are playing a important role as the fund of funds model wavers. Other topics include regulatory reform and what it means for hedge funds, and a discussion about where alpha can be found going forward.

Co-hosted by FINalternatives

Agenda

1:00 – 1:30 Registration

1:30 – 2:00 State of the Industry, State of the Markets

2:10 – 3:00 Panel One: Growing Your Assets

JOHN SEIGENTHALER, CEO-NY, Seigenthaler Public Relations (former NBC News Anchor) – Moderator

ALAN GLATT, Managing Partner, Protocol Capital Management

ANTHONY SCARAMUCCI, Managing Partner, SkyBridge Capital

DANIEL SOLOMON, President and COO, Lyford Group International

3:00 – 3:30 Coffee Break

3:30 – 4:20 Panel Two: Post-Crisis: Challenges And Opportunities

SIMON FLUDGATE, Partner, Aksia

Additional Speakers to be announced

4:30 – 5:00 Keynote Speaker

WARREN MOSLER, Founder and Principal, III Offshore Advisors

5:00 – 6:30 Cocktail Reception

Non-Mfg ISM

With modest GDP growth and a 1.4 trillion deficit downside to equities can only come from an external shock.

High unemployment keeps the Fed on hold and the 0 rate policy keeps costs of production down and keeps personal income gains modest.

At least for now, the combo of 0 rates and an 8%+ budget deficit continues to be supportive of only modest aggregate demand growth and only very modest employment growth.

Again, good for stocks, where a bit of top line growth and productivity gains keep earnings growth positive.

Karim writes:

- Strong service sector report with particular strength in key components (orders and employment)

- Employment index crosses 50 and at highest since 2008

- Service sector picking up growth mantle from manufacturing

- ADP gain plus upward revision to prior month suggest about 125-150k in private sector job growth

| July | June | |

| Composite | 54.3 | 53.8 |

| Activity | 57.4 | 58.1 |

| Prices Paid | 52.7 | 53.8 |

| New Orders | 56.7 | 54.4 |

| Employment | 50.9 | 49.7 |

| Export orders | 52.0 | 48.0 |

| Imports | 48.0 | 48.0 |

CH News | Australia Has Record Trade Surplus on China Coal, Iron Demand

It’s good to be China’s coal mine.

Though it does make Australia one of the world’s largest contributors to the increasingly unpopular emissions issues.

Australia Has Record Trade Surplus on China Coal, Iron Demand

Australia Has Record Trade Surplus on China Coal, Iron DemandBy Jacob Greber

Aug. 4 (Bloomberg) — Australia’s trade surplus unexpectedly

reached a record in June as Chinese demand spurred exports of

coal and iron ore, while imports stagnated amid a slowdown in

domestic spending.

The excess of exports over imports reached A$3.54 billion

($3.2 billion), almost double the median forecast in a Bloomberg

News survey, a Bureau of Statistics report showed in Sydney

today. A separate report showed house-price gains decelerated in

the second quarter, underscoring the impact of the central

bank’s six interest-rate increases since early October.

Hanke on Greece

Hate to criticize someone proposing a payroll tax holiday- darn that Lerner’s law!

A Big Bang for GreeceThere is a way out of the debt trap for Athens.

By Stece H. Hanke

June 30 (WSJ) — How did Greece get into the death spiral that it’s in? Unfunded entitlements. In other words, promise somebody something, don’t come up with the financing for it, and pretty soon you find yourself in a fiscal/debt crisis.

Yes, happens to those who are not the issuer of their currency all the time, including those with fixed fx arrangements. EU members, US States, corporations, households, Russia when fixed to the dollar, Mexico when fixed to the dollar, etc.

But never with issuers of the currency. They can always make payments as desired.

This is where Greece ended up, and in February, the Greek government called in some outside advisers (Joseph Stiglitz for one), and the blame game began. Prime Minister Papandreou, who is also president of Socialist International, started blaming everyone. First, it was the speculators. Then he went on a tear against his own colleagues in the European Union. The Germans really got whacked according to Mr. Papandreou, they were a big cause of Greece’s troubles.

Never would have happened under the drachma. Just would have been the usual inflation and currency depreciation.

But Greece is a user of the euro, not the issuer like the ECB is.

Ironically, after blaming outsiders for all their problems, the Greeks have called in the foreign doctors. In this case it isn’t just the IMF, but also the EU politicians and bureaucrats who are involved. But this may ultimately be a case in which the doctors kill the patient.

The problem ended for Greece and the entire eu in general only after the ECB agreed to ‘write the check’ and started buying greek bonds.

There was no other way.

To address the moral hazard issue that comes with ECB support, the ECB insisted on the ‘terms and conditions’ to contain inflation possibilities

They haven’t started with what they should be doing, but with a standard IMF-type austerity program. The government has promised to cut public expenditures. It has also raised taxes. Unlike neighboring Bulgaria, which did exactly the right thing by refusing to increase its VAT, Greece has increased its VAT twice since the crisis.

What should Greece have done? It should have started with a Big Bang, doing a number of things simultaneously a la New Zealand. In 1984, New Zealand elected a Labor government after Robert Muldoon’s National Party governments had made a complete mess of the economy. The Muldoon governments introduced, over the course of almost a decade, a socialist-style system in New Zealand. Labor, under finance minister Roger Douglas, introduced structural reforms centered on deregulation and competitiveness. As a consequence, New Zealand had a massive economic revolution after the ’84 election. Greece should adopt a New Zealand-type Big Bang.

The NZ gov was the issuer of its own currency and therefore didn’t face the solvency problem Greece did. otherwise it would have been an entirely different story.

As part of its Big Bang, Greece should have begun by rescheduling its debt. But it also should have implemented a supply-side fiscal consolidation. That means cutting government expenditures, but also changing the tax regime.

Without the ECB writing the check, that would have resulted in a systemic collapse of the euro member national govts and the payments system in general.

With the ECB writing the check there are other options.

Right now, Greece has very onerous payroll taxes that are paid by employers and, ultimately, labor. As part of a Big Bang, Greece should eliminate the employer contribution to payroll taxes, which is currently 28% of wages (employees pay a further 16% rate directly).

With funding entirely dependent on the good will of the ECB, those decisions are up to the ECB, not Greece. If they cross the ECB they get cut off and again face default.

At the same time, Greece should make its VAT rates uniform. Right now, there are three VAT rates in Greece. This is typical in Europe. You have the regular VAT, a VAT that is reduced by 50% for other categories, and, finally, a super-reduced VAT. I would eliminate the reduced and super-reduced rates, and just have one, uniform rate for the VAT one set below the current top VAT rate of 23%.

If Greece did those two things, it would end up generating more revenue than it is generating right now. Even when based on a static, simple-minded analysis, that would put Greece ahead of the revenue game.

At the macro level for the EU it’s about the right fiscal balance needed to sustain growth and employment, which is probably a deficit higher than the growth rate. But at the micro level it’s about credit worthiness which means a deficit lower than the growth rate. So the members need to be tighter than the union needs to be. This requires a central govt/ECB that runs the needed deficits to make it all work efficiently. Much like the US states balance and the fed govt runs the deficits.

But more importantly, it would also substantially reduce its economy’s labor costs overnight. Employers’ social security contributions are about 7.8% of GDP. Eliminating the employer contribution would yield about a 22% reduction in the overall Greek wage bill as a percentage of GDP. This would make the Greek economy more competitive without the currency devaluation that some commentators claim is necessary. These changes would also, obviously, reduce consumption, increase savings, and reduce the level of debt in the country.

Allow me to make a comment about devaluation. There are some people who are wringing their hands and saying, “Well, the problem with Greece is that it put itself into a euro straitjacket and it can’t devalue the drachma anymore. So, Greece is in a trap. There’s nothing it can do!”

Yes, but note devaluing was never a policy tool. It was the consequence of policy. Today the consequence of the same policy is default rather than currency depreciation.

But there is something the Greeks can do. They can reduce the economy’s total labor cost by 22%, simply by eliminating the employer contribution to payroll taxes. To see what the size of a devaluation would have to be to generate a positive competitiveness shock of this magnitude, let’s assume that 50% of a devaluation would be passed through to the economy in the form of increased inflation reasonable assumption about a small, open economy like Greece’s.

In this case, Greece would have to have a 44% devaluation to be equivalent, in terms of competitiveness, to the positive shock that would accompany the elimination of the employer contribution to payroll taxes.

So, with the elimination of the employer contribution to the payroll tax, Greece would enhance its competitiveness. The enhancement would be equal to roughly a 44% devaluation. Moreover, the supply-side generated competitiveness would not be accompanied by the inflation and widespread private-sector bankruptcy that a devaluation would provoke.

Needless to say, neither Greece nor its international partners are contemplating a voluntary debt restructuring,

That would also require a restructuring of the banking system as the loss of capital would require some kind of adjustment as well.

let alone a supply-side Big Bang, which makes it more likely that Greece will remain stuck in a trap. But don’t let anyone tell you there’s nothing Greece could do. It’s not too late to change course. What’s more, other countries in Europe that are facing down a possible debt crisis could likewise try a similar approachreschedule debt, cut taxes on labor to improve competitiveness and spur job creation, while raising some consumption taxes to keep the revenue coming in. There is a way out of the Greek trap.

Mr. Hanke is a professor of applied economics at the Johns Hopkins University in Baltimore and a senior fellow at the Cato Institute in Washington, D.C. This article is adapted from remarks made at the Cato Institute’s Policy Forum, “Europe’s Economic Crisis and the Future of the Euro,” on May 11, 2010, Washington, D.C.

ISM/Bernanke

I tend to agree with Karim and Fed Chairman Bernanke.

Modestly improving GDP growth with unemployment coming down very gradually until a consumer credit expansion takes hold.

Good for stocks, not so good for most of the people still struggling to survive, as the Obama administration continues to preside over what might be the largest transfer of wealth from bottom to top in the history of the world.

And no credible energy policy. We are completely at the mercy of the Saudis who can unilaterally hike prices any time they feel like it.

Karim writes:

- ISM shows lift from inventories likely has run its course as inventory component crossed back above 50

- But customer inventories remain low and employment index rises to second highest level since 2004

- Going forward, private demand, not inventory rebuilding will drive manufacturing

- Bernanke addressed this today (below) and seems to maintain his above consensus growth forecast

| July | June | |

| Index | 55.5 | 56.2 |

| Prices paid | 57.5 | 57.0 |

| Production | 57.0 | 61.4 |

| New Orders | 53.5 | 58.5 |

| Inventories | 50.2 | 45.8 |

| Customer inventories | 39.0 | 38.0 |

| Employment | 58.6 | 57.8 |

| New export orders | 56.5 | 56.0 |

| Imports | 52.5 | 56.5 |

- “Business in July was strong, the best month since October 2008.” (Fabricated Metal Products)

- “Slow economy has killed sales for new equipment orders.” (Machinery)

- “Quoting activity and sales are slow, and backlog is dropping.” (Computer & Electronic Products)

- “Business continues to be sluggish and has fallen slightly as the economic ills continue.” (Nonmetallic Mineral Products)

- “Retailers are still unwilling to gamble on inventory.” (Printing & Related Support Activities)

Bernanke

While the support to economic activity from stimulative fiscal policies and firms’ restocking of their inventories will diminish over time, rising demand from households and businesses should help sustain growth. In particular, in the household sector, growth in real consumer spending seems likely to pick up in coming quarters from its recent modest pace, supported by gains in income and improving credit conditions. In the business sector, investment in equipment and software has been increasing rapidly, in part as a result of the deferral of capital outlays during the downturn and the need of many businesses to replace aging equipment. At the same time, rising U.S. exports, reflecting the expansion of the global economy and the recovery of world trade, have helped foster growth in the U.S. manufacturing sector.

To be sure, notable restraints on the recovery persist. The housing market has remained weak, with the overhang of vacant or foreclosed houses weighing on home prices and new construction. Similarly, poor economic fundamentals and tight credit are holding back investment in nonresidential structures, such as office buildings, hotels, and shopping malls.

Video of the Senatorial Forum at Trinity College

Fed Bullard

It’s not just him, the all say ‘quantitative easing’ will ‘work’ when they should now have enough evidence and theory to know all it does is lower interest rates which are already plenty low with regards encouraging lending.

Might just be managing expectations but more likely they still actually believe it.

*DJ Fed’s Bullard: Worried About Possible Deflationary Outcome For US(DJ)

*DJ Bullard: Says More Quantitative Easing Will Work(DJ)

*DJ Bullard: Says Deflation Not Most Likely Economic Scenario(DJ)

*DJ Fed’s Bullard: Most Likely Scenario Is That Recovery Will Continue(DJ)

*DJ Bullard: Acknowledges Weaker US Data Over Last Two Months(DJ)

*DJ Bullard: Euro Zone Has Done Reasonable Job Containing Crisis(DJ)

Bullard/Fed

Karim writes:

Bullard

- Definitely out there on his own. FRB would certainly not communicate policy shift through him

- Also, everyone has different reasons why QE works. Most of the Fed leadership thinks just via interest rate channel and announcement effect. Bullard thinks through monetary channel, which makes him a minority.

GDP Data: Something for everyone; capex recovery intact; consumer spending sluggish; net exports a large drag; inventories an offset

- Annualized gwth at 2.4%; Q1 revised from 2.7% to 3.7%; Prior data revised lower

- Private consumption 1.6% vs 1.9% in Q1; Investment up 28.8% vs 29.1% in Q1

- Business capex (equipment and software spending) up 21.9% vs 20.4% in Q1

- Residential fixed investment (housing) up 21.9% (aided by expiring tax credit)

- Exports and imports both up in double digits, but net exports a drag on growth of -2.78%

- Inventories contribute 1.05%

EU Daily | Europe Economic Confidence Rises as Exports Improve

It’s off to the races for a while in the euro zone as the adjustment that began when the ECB started buying member nation debt continues, and the still large budget deficits support incomes and growth while the still low euro supports exports.

Fears of solvency risks for govts and the banking system are fading fast.

The euro meanwhile will continue to adjust/appreciate with a small lag in response to rising net exports and ultimately keep a lid on them.

If US jobless claims are up it’s good for US stocks, as unemployment is perceived to keep labor costs and interest rates down.

If claims are down it’s good for stocks as it’s evidence of a bit more top line growth, which trumps any fears of damage from interest rate hikes.

China weakness serves to keep a lid on resource costs which is good for stocks.

Earnings season has confirmed that business has figured out how to make money in the current environment, supported by 8%+ federal deficits that is also supporting 4% personal income growth as well as nominal and real GDP growth.

Unemployment working its way lower in tiny increments unfortunately causes politicians and mainstream economists to think their measures are ‘working,’ including revised down deficit projections from the automatic stabilizers, and that it all just need lots of time due to the severity of the downturn.

This is very good for stocks which further supports the political desire to prove themselves right. And it is very bad for people forced to wait years before their lives can begin to recover, as with modest improvement in GDP a fiscal adjustment that could drastically accelerate the move back to full employment is highly unlikely.

At age 60, it’s not looking like I’ll get to experience how good this economy could be for everyone if we understood monetary operations and reserve accounting.

EU Headlines

Europe Economic Confidence Rises as Exports Improve

ECB Puts Bigger Discounts on Low-Quality Collateral

German Unemployment Fell for 13th as Exports Boom

Lagarde Predicts Significant Pickup in World Growth

Berlusconi Survives Confidence Vote to Pass Deficit Reductions

Italian Business Confidence Rises to Two-Year High on Exports

Inflation in Spain at highest point in 18 months

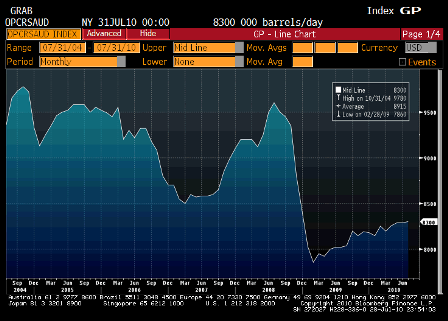

Saudi oil production

Looks like net demand is slowly using up Saudi excess capacity.

But there’s a long way to go.

No telling when they might alter prices- it’s a political decision on their part.