Edward talks to Warren Mosler, chairman of Consulier Engineering on why the EU’s approach to the Greek debt crisis has failed to lift the Greek …

So for decades the BOJ has tried to create inflation and failed, for 7 years the Fed has tried and failed, the ECB has tried and failed, etc. etc. etc. Maybe it’s not so easy for a CB to create inflation? Or impossible…;)

Feb 16 (Reuters) — Abe hopes BOJ keeps stimulus to meet inflation goal, upbeat on economy (Reuters) Japanese Prime Minister Shinzo Abe said on Monday praised the BOJ’s aggressive stimulus program for helping revive the economy and wipe out the public’s “sticky deflationary mindset.” “I hope the BOJ continues to steadily proceed with bold monetary easing to achieve 2 percent inflation,”

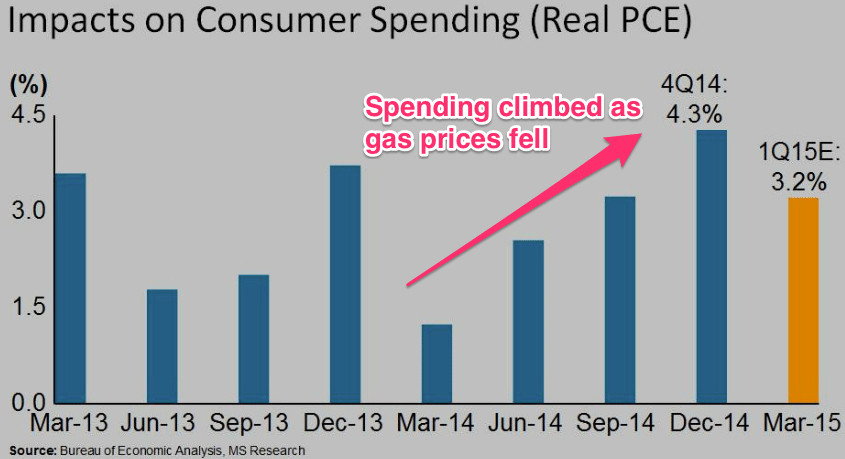

No consideration that the lower prices in the first instance only shift income from sellers of oil to buyers of oil:

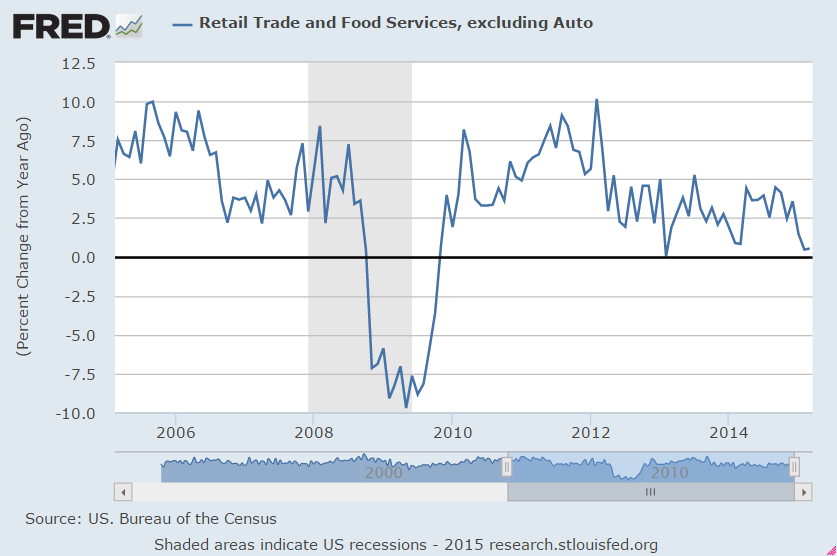

Even excluding gas, retail spending was flat last month after ticking down 0.2% in December. The retail restraint is somewhat surprising given that the average household is expected to save hundreds of dollars this year on gas that averaged $2.23 a gallonon Thursday, down from $3.32 a year ago, according to the AAA.

Greece demands a credible growth package:

“No more loans — not until we have a credible plan for growing the economy in order to repay those loans, help the middle class get back on its feet and address the hideous humanitarian crisis.” YV

Italy : Merchandise Trade

Highlights

The seasonally adjusted trade balance returned a sizeable E5.1 billion surplus in December following a slightly larger revised E3.8 billion excess in November.

December’s sharp improvement was mainly attributable to a 2.6 percent monthly bounce in exports, their fourth increase in the last five months, which easily more than reversed a 1.1 percent mid-quarter drop. Outside of durable consumer goods all of the major sectors saw solid monthly gains and total exports were up 6.3 percent from their level in December 2013.

However, weak domestic demand and lower oil costs were also once again a factor in the expansion of the black ink. Hence, imports were down 1.6 percent versus December (minus 0.5 percent ex-energy), their third straight month of decline. Compared with a year ago, purchases from overseas were off 1.3 percent.

Having hit a low of E-4.1 billion in March 2011 the turnaround in the Italian trade balance has been sharp and quite steady. Net exports probably provided a useful boost to economic growth last quarter and look likely to play a key role in any sustained upswing in 2015.