{kind=link}

US May Final Consumer Confidence TABLE

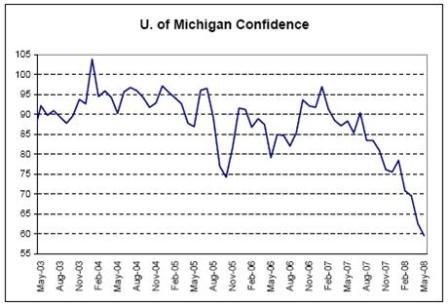

Interesting how current conditions improved while expectations fell, probably due to expected higher prices.

It’s all about inflation now.

[top]

Interesting how current conditions improved while expectations fell, probably due to expected higher prices.

It’s all about inflation now.

[top]

(an interoffice email)

On Thu, May 29, 2008 at 11:58 PM, Deep wrote:

>   The attached charts shows the change in 3M Forwards for the USD curve from its

>   lowest yield point this year (17Mar08) to today.

>  ÂÂÂ

>   In Chart 1, the changes are compared to two other periods where we had strong

>   selloffs Jun03->Sep03 and Apr07->Jun07.

>  ÂÂÂ

>   As the chart shows, in the current selloff, the front end has moved approx 180bp

>   (similar in magnitude to the 2003 selloff). However, in contrast to both 2003 and 2007,

>   the forwards beyond 8y have barely moved. In 2003 and 2007, the 10Y3M rate sold off

>   approx 55% as much as the front end. Both of these periods were characterized by

>   mortgage convexity paying.

>  ÂÂÂ

>   The lack of movement of the back end in the current selloff is leading to an extreme

>   flattening of the yieldcurve compared to prior selloffs.

>  ÂÂÂ

Hi Deep,

I’m thinking the forwards are anticipating future Fed moves. They see a relatively quick ‘take back’ of the cuts as market functioning returns and we are left with a ‘normal ‘ slowdown.

With cpi looking to move past 5% over the next few months, passthroughs to core increasing, gdp muddling through with strong exports, the Fed will have to decide what the appropriate ‘real rate’ is for what they feel is an appropriate output gap.

The markets will likely believe/discount the Fed will be successful, which means a eurodollar curve that rises sharply with the inflation attack and then tails off after it’s success.

Warren

>  ÂÂÂ

>   A possible reason for the unusual nature of the current selloff maybe that

>   two offsetting flows characterize it –

>  ÂÂÂ

>   a) unwind of yieldcurve steepeners by Fixed income, Credit and Equity Funds

>   as part of their delevering out of steepeners – this leads dealers to hedge by

>   paying the front end (less than 5Y) and receive the back end (beyond 10Y).

>  ÂÂÂ

>   b) paying of 10Y by mortgage convexity hedgers

>  ÂÂÂ

>   The offsetting flows in the 10Y sector may result in the lack of movement in the

>   forwards beyond 8Y.

>

>    A low-risk way to position against the extreme flattening selloff is through

>   the Midcurve steepener. The trade is to

>   ÂÂÂ

>    Buy 3160mm Z8expiryZ9 97.00 Call

>   Sell 100mm 12Dec08->10Y 4.25% receiver

>    execute at zero cost

>

>  ÂÂÂ

[top]

Highlights

| European Inflation Accelerates More Than Forecast as Oil Surges |

Note the concern over inflation expectations in the text below.

That’s what has turned the Fed as well.

| German Retail Sales Unexpectedly Dropped on Inflation |

| Weber Rules Out Changing ECB’s Current Inflation Goal |

While the US economic memory from the depression is unemployment lines, the German memory is wheelbarrows full of money.

Eurozone unemployment is down to about 7% which frightens the inflation hawks, as per the below reports.

| Trichet Says Pushing Down Inflation Is ECB’s Biggest Challenge |

Articles

European Inflation Accelerates More Than Forecast as Oil Surges

(Bloomberg) European inflation accelerated faster than economists forecast this month as oil prices jumped to a record, adding to what European Central Bank President Jean-Claude Trichet has called policy makers’ “biggest challenge.”

The inflation rate in the euro area rose to 3.6 percent, matching a 16-year high, from 3.3 percent in April, the European Union statistics office in Luxembourg said in a statement today.

Economists had forecast a 3.5 percent rate, according to the median of 36 estimates in a Bloomberg survey.

The ECB, which aims to keep consumer-price growth below 2 percent, said yesterday there are signs inflation expectations “have been trending up recently” and it’s imperative that they remain contained. The Frankfurt-based bank celebrates its 10th anniversary this weekend, having failed to meet its target for the last eight years.

“There has been a sharp deterioration in the inflation picture,” said Simon Barry, an economist at Ulster Bank in Dublin. “Our base case is the ECB is on hold for now, but the inflation risk has increased and there’s no room for complacency.”

Separate figures published by the statistics office today show that unemployment in the euro area remained at a record low 7.1 percent in April.

Crude Oil

Crude oil prices have doubled in the last 12 months and reached a record $135.09 May 22. Food commodities have also surged in the last year, boosting how much consumers are paying for staples such as bread and milk. Wheat has gained 45 percent in the past year and corn has surged 51 percent.

Soaring prices have led to protests in Europe and companies and consumers expect prices to continue to rise. A European Commission index of manufacturers’ selling price expectations increased this month, while consumers’ outlook for their personal finances deteriorated. Greencore Group Plc, the world’s biggest maker of prepared sandwiches, this week said it’s been passing on cost increases to customers by raising its prices.

In France, fishermen have blockaded ports in the past week to protest against the increase in oil prices, while a group representing bus companies in Ireland said it may have to stop school runs because of the cost of gasoline.

Key Rate

The ECB has kept its key rate at a six-year high of 4 percent to counter inflation even as the economy of the 15 euro nations cools. The central bank is concerned that wages will increase to compensate for the higher cost of living, threatening a wage-price spiral.

“We’re looking at below trend growth” in the euro area, said Barry, the Ulster Bank economist. “But for the ECB to consider cutting, that would require a pretty sharp weakening in the economy and nothing so far is heading that way.”

(snip)

Some companies are raising salaries. German wages increased the most in 12 years in January, the statistics office said last month. Germany’s Ver.di union in March negotiated a settlement for as many as 2.1 million public-sector staff that is worth 8.9 percent over two years.

Weber Rules Out Changing ECB’s Current Inflation Goal

(Bloomberg) European Central Bank council member Axel Weber said revising the ECB’s definition of price stability would jeopardize the bank’s credibility at a time when fighting inflation is “of the essence.”

“I see no compelling reason why a temporary, albeit protracted, rise in energy and food prices should give rise to a discretionary change in the eurosystem’s stability norm,” Weber said at a conference in Frankfurt today. “It would risk unanchoring inflation expectations at a point in time where their solid anchoring is of the essence.”

The ECB defines price stability as keeping inflation just below 2 percent “over the medium term” and has struggled to meet that goal since taking charge of monetary policy in 1999. While economists including Joachim Fels of Morgan Stanley say the ECB should be open to changing its target, President Jean-Claude Trichet said May 8 he won’t consider it “for one second.”

“The present price hikes are a timely reminder that, when it comes to inflation, complacency is out of place,” said Weber, who is also head of Germany’s Bundesbank. “We cannot rest on our laurels where credibility is concerned.”

`Prepared to Act’

The ECB’s 21-member governing council is scheduled to hold its next assessment on interest rates on June 5.

“Over the past decade, the Eurosystem has shown that — if necessary — it is prepared to act in a firm and timely manner,” Weber said. “We will continue to do so over the next decades in order to maintain price stability.”

Surging energy costs pushed inflation to 3.6 percent in May, the most since 1992, from 3.3 percent in the previous month, the European Union’s statistics office in Luxembourg said today.

Economists forecast a 3.5 percent rate, according to the median of 36 estimates in a Bloomberg survey.

Surging food and oil prices “represent the latest, and arguably the most worrying, disturbance in a series of substantial upside price shocks,” Weber said.

Inflation expectations, as measured by French inflation-indexed bonds, rose to an all-time high of 2.46 percent on May 28 from around 2.1 percent two months ago.

A surge in inflation expectations close to 3 percent for this year “is hardly surprising,” Weber said. “Market participants and the general public are likely to readjust their short-term inflation expectations as soon as they observe inflation returning to a lower level.”

Trichet Says Pushing Down Inflation Is ECB’s Biggest Challenge

(Bloomberg) European Central Bank President Jean-Claude Trichet said the central bank’s “biggest challenge” is to push inflation just below 2 percent in the medium term, according to an interview with Bild newspaper.

“We have to be careful that current price shocks of food and oil don’t translate into price increases of other goods and exaggerated wage agreements, thus triggering a general inflation and wage wave,” Trichet told the newspaper in the interview published today. Bild translated his remarks into German.

Price stability “is and will always be the most important aim of the ECB,” Trichet told the newspaper. Regarding the global financial turbulence, the ECB continues to be “very alert and ready to act” if needed, he said.

Germany is the only large member of the euro zone where the measure of economic sentiment remains above its long-term average of 100.0. It rose slightly to 103.0 in May from 102.8 in April.

French economic sentiment in May fell below the 100.0 long-term average for the first time in more than a year, declining to 99.8 from 103.1 a month earlier. Sentiment remains well below average in Italy, Spain and Greece.

[top]

| Survey | n/a |

| Actual | 172.2 |

| Prior | 175.9 |

| Revised | 176.0 |

Still moving lower. The sample is the 20 largest metro areas which were the regions hit hardest by the speculative bulge.

Broader measures don’t show this kind of depreciation.

| Survey | -14.2% |

| Actual | -14.4% |

| Prior | -12.7% |

| Revised | n/a |

Same as above.

| Survey | n/a |

| Actual | 159.2 |

| Prior | 170.6 |

| Revised | 170.6 |

Same as above.

| Survey | n/a |

| Actual | -14.1% |

| Prior | -8.9% |

| Revised | n/a |

Same as above.

| Survey | 520K |

| Actual | 526K |

| Prior | 526K |

| Revised | 509K |

April up and higher than expected, March revised down some.

| Survey | -1.1% |

| Actual | 3.3% |

| Prior | -8.5% |

| Revised | -11.0% |

| Survey | 60.0 |

| Actual | 57.2 |

| Prior | 62.3 |

| Revised | 62.8 |

This is what an export economy looks like.

| Survey | 1 |

| Actual | -3 |

| Prior | 0 |

| Revised | n/a |

[comments]

| Survey | -49 |

| Actual | -51 |

| Prior | -49 |

| Revised | n/a |

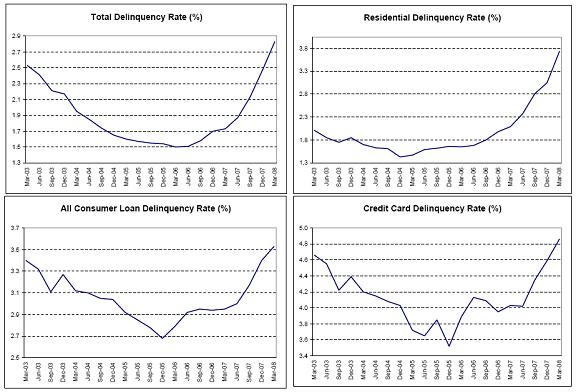

As above. Consumers are getting squeezed by inflation, while exports boom.

[top]

thanks, a few quips below:

Karim writes:

Labor conditions, plans to buy home and plans to buy auto all fall to new cycle lows

Tough living in an export economy.

Inflation rips as non-residents outbid us for your output, as all our funds are spent on food and fuel.

Narrow index of 20 metro regions, with 4 or 5 biggest spec boom/bust regions doing most of the damage.

Coming back from unsustainably low levels give the US population and income growth.

Actual homes in inventory fell to the lowest levels since July.

Tough first quarter with record low consumer sediment :) behind us.

Right, this was also suggested in a prior email- the political response towards a food shortage would be cash distributions.

Assuming there actually is a world food shortage and the prices are indicative of a world market allocating by price, this doesn´t create any new food but simply adds upward pressure on prices, triggering an international inflation.

Politically, there is no other choice but to add to inflation like this to at least be seen to be doing something.

Mexico’s poor get food cash boost

The Mexican government is to give its poorest citizens a monthly cash payment of 120 pesos ($11.55; £5.85) to help them cope with rising food prices.

The news came a day after the country said it would cut tariffs on imported crops such as corn, wheat and rice.

In a further sign of the impact of rising food and fuel costs, inflation in Vietnam jumped to 25% in May, the highest rate for 10 years.

Average food costs have risen by 42.4% in a year, the Statistics Office said.

Growing demand

In Mexico, official figures show consumer prices rose by 4.55% – the fastest rate for three years – in the 12 months to 30 April, led by increases in the cost of tomatoes, chicken and cooking oil.

Growing demand from fast-expanding countries such as India and China has been blamed for spiralling food prices, along with record fuel costs and the use of grain to produce bio-fuels.

Governments around the world are under pressure to intervene to help the poorest cope with the sharp food price rises.

There have been public demonstrations about food prices in a number of countries including Egypt and South Africa.

Mexico’s monthly cash payment, which will go to 26 million people in the Latin American country, equates to just over twice the national daily minimum wage of 50 pesos.

The government faced street protests last year when the price of tortillas doubled.

Rice restrictions

Vietnam has seen the price of rice, its staple food, jump 67.8% in the last 12 months, according to government figures.

One of Vietnam’s most important sources of imported rice, Cambodia, stopped exporting the grain in March.

It is one of a number of rice-producing countries, including India, Egypt and Indonesia, to have either banned or restricted exports in recent months to secure supply for domestic customers.

On Tuesday, Cambodia was set to resume exports of rice after its two-month ban ended.

Prime Minister Hun Sen said only rice that was not needed for domestic consumption could be sold for overseas consumption until the new harvesting season began in December.

Last year, that amounted to 1.6 million tons of milled rice.

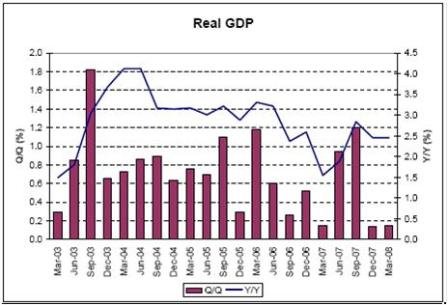

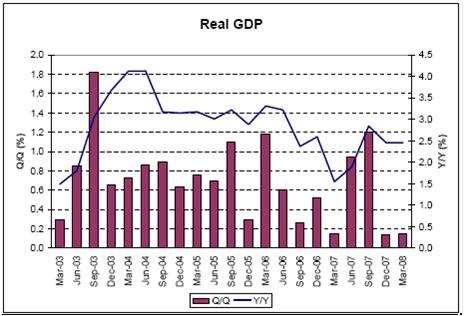

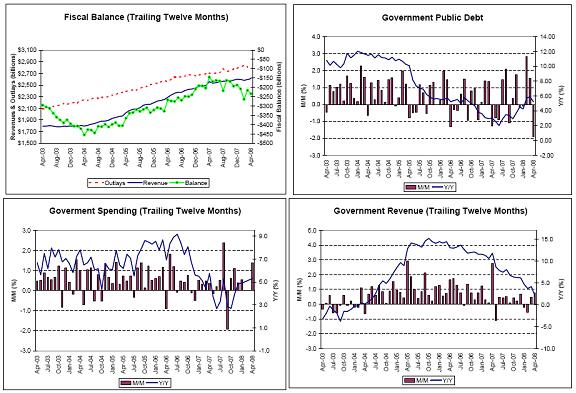

Hard to see any recession here, and the consensus is for Q1 to be revised up to 0.9%, bringing year over year up to 2.8%.

I also think the estimates of the effects of the fiscal package are on the low side.

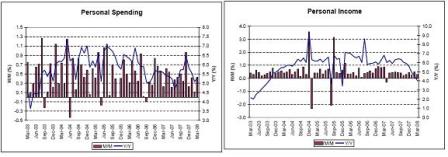

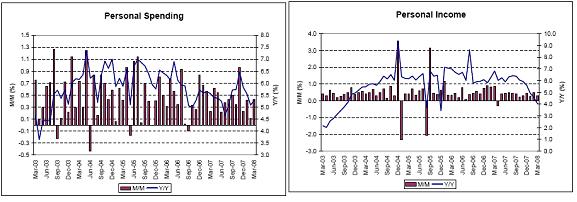

Income and spending continue to chug along, ahead of core but not headline ‘inflation’.

Still moving higher.

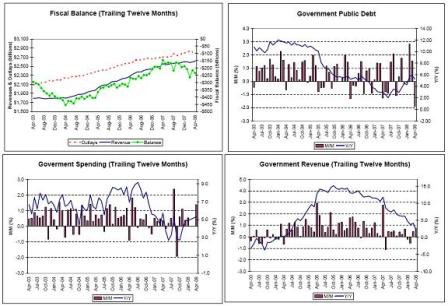

Fiscal rebates now kicking, with other government spending on the rise as well – should be a decent Q2 and better Q3.

And revenues seems to be holding up also indicating no recession yet.

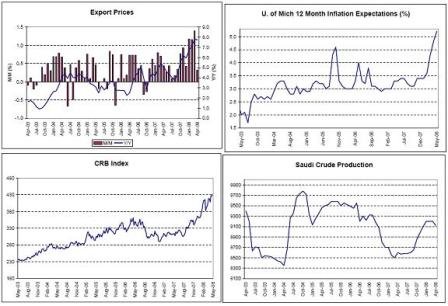

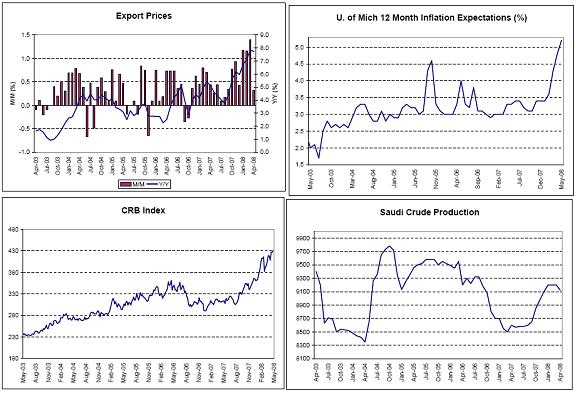

While headline CPI took a slight breather due to seasonal factors, the drivers of the current bout of inflation continue without let up, as crude oil touches $135 and the USD fall resumes.

Saudi crude output remains above 9 million bpd, indicating world demand is holding at the higher prices.

Booming exports and export prices work in tandem.

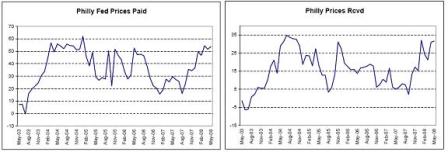

Inflation expectations have alarmed the FOMC with recent speeches indicating there will probably be no more rate cuts if inflation continues to escalate .

The Fed watches this carefully in regard to inflation expectations, along with surveys and professional forecasts which have gone up considerably.

The 5 year tips 5 years forward dipped a couple of months ago on the generally commodity sell off, then fell again for short term technical reasons- the first five years went up with crude and the 10 year stayed about the same, so the forwards went down as a matter of arithmetic and little volume – and now this is all sorting itself out along the curve, with the forwards moving up as shown.

Just saw Fed Gov Warsh on TV saying the same thing Vice Chair Kohn said (and was also in the Fed minutes) they have to be careful about perceptions that the Fed’s inflation tolerance have gone up feeding into inflation expectations.

And concern has been further supported by pronouncements that even if the economy weakens some there’s no room for rate cuts.

[top]

I cut quite a bit, but still a lot worth a quick read:

In view of continuing strains in interbank and other financial markets, the Committee took up proposals to expand several of the liquidity arrangements that had been put in place in recent months. Chairman Bernanke indicated his intention to increase the overall size of the Term Auction Facility under delegated authority from the Board of Governors, and he proposed increases in the swap lines with the European Central Bank and Swiss National Bank to help address pressures in short-term dollar funding markets.

Still problems with USD funding in the eurozone.

By unanimous votes, the Committee approved the following three resolutions:

The Federal Open Market Committee directs the Federal Reserve Bank of New York to increase the amount available from the System Open Market Account under the existing reciprocal currency arrangement (“swap” arrangement) with the European Central Bank to an amount not to exceed $50 billion. Within that aggregate limit, draws of up to $25 billion are hereby authorized. The current swap arrangement shall be extended until January 30, 2009, unless further extended by the Federal Open Market Committee.

The Federal Open Market Committee directs the Federal Reserve Bank of New York to increase the amount available from the System Open Market Account under the existing reciprocal currency arrangement (“swap” arrangement) with the Swiss National Bank to an amount not to exceed $12 billion. Within that aggregate limit, draws of up to $6 billion are hereby authorized. The current swap arrangement shall be extended until January 30, 2009, unless further extended by the Federal Open Market Committee.

The information reviewed at the April meeting, which included the advance data on the national income and product accounts for the first quarter, indicated that economic growth had remained weak so far this year. Labor market conditions had deteriorated further, and manufacturing activity was soft. Housing activity had continued its sharp descent, and business spending on both structures and equipment had turned down. Consumer spending had grown very slowly, and household sentiment had tumbled further. Core consumer price inflation had slowed in recent months, but overall inflation remained elevated.

The stronger than expected April numbers hadn’t been released yet, including the drop in the unemployment rate to 5.0%.

Although industrial production rose in March, production over the first quarter as a whole was soft, having declined, on average, in January and February. Gains in manufacturing output of consumer and high-tech goods in March were partially offset by a sharp drop in production of motor vehicles and parts and by ongoing weakness in the output of construction-related industries. The output of utilities rebounded in March following a weather-related drop in February, and mining output moved up after exhibiting weakness earlier in the year. The factory utilization rate edged up in March but stayed well below its recent high in the third quarter of 2007.

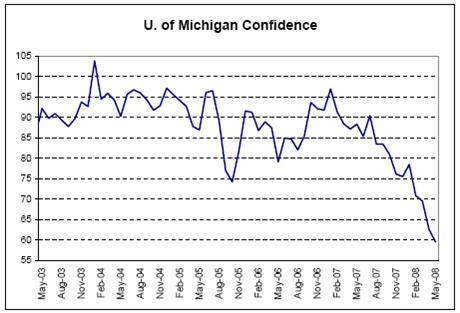

Real consumer spending expanded slowly in the first quarter. Real outlays on durable goods, including automobiles, were estimated to have declined in March, but expenditures on nondurable goods were thought to have edged up, boosted by a sizable increase in real outlays for gasoline. For the quarter as a whole, however, real expenditures on both durable and nondurable goods declined. Real disposable personal income also grew slowly in the first quarter, restrained by rapidly rising prices for energy and food. The ratio of household wealth to disposable income appeared to have moved down again in the first quarter, damped by the appreciable net decline in broad equity prices over that period and by further reductions in house prices. Measures of consumer sentiment fell sharply in March and April; the April reading of consumer sentiment published in the Reuters/University of Michigan Survey of Consumers was near the low levels posted in the early 1990s.

That’s how it goes in an export driven economy. They haven’t recognized that yet:

Residential construction continued its rapid contraction in the first quarter. Single-family housing starts maintained their steep downward trajectory in March, and starts of multifamily homes declined to the lower portion of their recent range. Sales of new single-family homes declined in February to a very low rate and dropped further in March. Even though production cuts by homebuilders helped to reduce the level of inventories at the end of February, the slow pace of sales caused the ratio of unsold new homes to sales to increase further. Sales of existing homes remained weak, on average, in February and March, and the index of pending sales agreements in February suggested continued sluggish activity in coming months. The recent softening in residential housing demand was consistent with reports of tighter credit conditions for both prime and nonprime borrowers.

Recent signs of housing stabilizing haven’t materialized yet.

The U.S. international trade deficit widened in February. Imports rose sharply, more than offsetting continued robust growth of exports. Most major categories of non-oil imports increased in February, and imports of natural gas, automobiles, and consumer goods surged. Imports of services continued to rise at a robust pace. By contrast, oil imports moved down. Increases in exports in February were concentrated in agricultural goods, automobiles, and industrial supplies, particularly fuels. Exports of capital goods declined for the second consecutive month, with weakness evident across a wide range of products.

The March numbers weren’t out yet, and they bounced back strongly, resulting in upward revisions to Q1 GDP.

Real economic growth in the major advanced foreign economies was estimated to have slowed further in the first quarter and consumer and business sentiment was generally down. In Japan, business sentiment fell significantly and indicators of investment remained weak. In the euro area, growth was estimated to have remained subdued in the first quarter, with Germany and France faring better than Italy and Spain. Growth in the United Kingdom slowed in the first quarter, as credit conditions tightened. Available data for Canada indicated a continued substantial drag from exports in the first quarter, although domestic demand appeared relatively robust. In emerging market economies, economic growth slowed some in the fourth quarter and was estimated to have held about steady in the first quarter. In emerging Asia, real economic growth was estimated to have picked up in the first quarter from a robust pace in the fourth quarter, led by brisk expansions in China and Singapore. Growth in other emerging Asian economies generally remained subdued. The pace of expansion in Latin America likely declined some in the first quarter, largely because the Mexican economy slowed in the wake of softer growth in the United States.

Headline inflation in the United States was elevated in March. Although the increase in food prices slowed in March relative to earlier in the year, energy prices rose sharply. Excluding these categories, core inflation rose at a relatively subdued rate again in March. The core personal consumption expenditures (PCE) price index increased at a somewhat more moderate rate in the first quarter than in the fourth quarter of 2007. Survey measures of households’ expectations for year-ahead inflation rose further in early April, but survey measures of longer-term inflation expectations moved relatively little. Average hourly earnings increased in March at a somewhat slower pace than in January and February. This wage measure rose significantly less over the 12 months that ended in March than in the previous 12 months. The employment cost index for hourly compensation continued to rise at a moderate rate in the first quarter.

Food and energy have since gone up further than forecast at the meeting.

At its March 18 meeting, the Federal Open Market Committee (FOMC) lowered its target for the federal funds rate 75 basis points, to 2-1/4 percent. In addition, the Board of Governors approved a decrease of 75 basis points in the discount rate, to 2-1/2 percent. The Committee’s statement noted that recent information indicated that the outlook for economic activity had weakened further; growth in consumer spending had slowed, and labor markets had softened. It also indicated that financial markets remained under considerable stress, and that the tightening of credit conditions and the deepening of the housing contraction were likely to weigh on economic growth over the next few quarters. Inflation had been elevated, and some indicators of inflation expectations had risen, but the Committee expected inflation to moderate in coming quarters, reflecting a projected leveling-out of energy and other commodity prices and an easing of pressures on resource utilization.

Which didn’t happen.

Still, the Committee noted that uncertainty about the inflation outlook had increased, and that it would be necessary to continue to monitor inflation developments carefully. The Committee said that its action, combined with those taken earlier, including measures to foster market liquidity, should help to promote moderate growth over time and to mitigate the risks to economic activity. The Committee noted, however, that downside risks to growth remained, and indicated that it would act in a timely manner as needed to promote sustainable economic growth and price stability.

Conditions in U.S. financial markets improved somewhat, on balance, over the intermeeting period, but strains in some short-term funding markets increased. Pressures on bank balance sheets and capital positions appeared to mount further, reflecting additional losses on asset-backed securities and on business and household loans. Against this backdrop, term spreads in interbank funding markets and spreads on commercial paper issued by financial institutions widened significantly. Financial institutions continued to tap the Federal Reserve’s credit programs. Primary credit borrowing picked up noticeably after March 16, when the Federal Reserve reduced the spread between the primary credit rate and the target federal funds rate to 25 basis points. Demand for funds from the Term Auction Facility stayed high over the period. In addition, the Primary Dealer Credit Facility drew substantial demand through late March, although the amount outstanding subsequently declined somewhat. Early in the period, historically low interest rates on Treasury bills and on general-collateral Treasury repurchase agreements indicated a considerable demand for safe-haven assets. However, Federal Reserve actions that increased the availability of Treasury securities to the public apparently helped to improve conditions in those markets. In five weekly auctions beginning on March 27, the Term Securities Lending Facility provided a substantial volume of Treasury securities in exchange for less-liquid assets. Yields on short-term Treasury securities and Treasury repurchase agreements moved higher, on balance, following these auctions; nonetheless, “haircuts” applied by lenders on non-Treasury collateral remained elevated, and in some cases increased somewhat, toward the end of the period.

In longer-term credit markets, yields on investment-grade corporate bonds rose, but their spreads relative to Treasury securities decreased a bit from recent multiyear highs. In contrast, yields on speculative-grade issues dropped, and their spreads relative to Treasury yields narrowed significantly. Gross bond issuance by nonfinancial firms was robust in March and the first half of April and included a small amount of issuance by speculative-grade firms. Supported by increases in business and residential real estate loans, commercial bank credit expanded briskly in March despite the report of tighter lending conditions in the Senior Loan Officer Opinion Survey on Bank Lending Practices conducted in April. Part of the strength in commercial and industrial loans was apparently due to increased utilization of existing credit lines, the pricing of which reflects changes in lending policies only with a lag.

Also, though standards were ‘tightened’, that doesn’t mean most borrowers can’t meet those standards.

Some banks surveyed in April reported that they had started to take actions to limit their exposure to home equity lines of credit, draws on which had grown rapidly in recent months. After having tightened considerably in March, conditions in the conforming segment of the residential mortgage market recovered somewhat. Spreads of rates on conforming residential mortgages over those on comparable-maturity Treasury securities decreased, and credit default swap premiums for the government-sponsored enterprises declined substantially. Broad stock price indexes increased markedly over the intermeeting period, mainly in response to earnings reports and announcements of recapitalizations from major financial institutions that evidently lessened investors’ concerns about the possibility of severe difficulties materializing at those firms.

Conditions in the money markets of major foreign economies remained strained, particularly in the United Kingdom and the euro area. Term interbank funding spreads rose in these areas, despite steps taken by their central banks to help ease liquidity pressures. Yields on sovereign debt in the advanced foreign economies moved up in a range that was about in line with the increases in comparable Treasury yields in the United States. The trade-weighted foreign exchange value of the dollar against major currencies rose.

The dollar is back down now.

M2 expanded briskly again in March, as households continued to seek the relative liquidity and safety of liquid deposits and retail money market mutual funds. The increases in these components were also supported by declines in opportunity costs stemming from monetary policy easing.

Over the intermeeting period, the expected path of monetary policy over the next year as measured by money market futures rates moved up significantly on net, apparently because economic data releases and announcements by large financial firms imparted greater confidence among investors about the prospects for the economy’s performance in coming quarters. Futures rates also moved up in response to both the Committee’s decision to lower the target for the federal funds rate by 75 basis points at the March 18 meeting, which was a somewhat smaller reduction than market participants had expected, and the Committee’s accompanying statement, which reportedly conveyed more concern about inflation than had been anticipated.

Yes.

The subsequent release of the minutes of the March FOMC meeting elicited limited reaction. Consistent with the higher expected path for policy and easing of safe-haven demands, yields on nominal Treasury coupon securities rose substantially over the period, and the Treasury yield curve flattened. Measures of inflation compensation for the next five years derived from yields on inflation-indexed Treasury securities were quite volatile around the time of the March FOMC meeting and on balance increased somewhat over the intermeeting period, although they remained in the lower portion of their range over the past several months. Measures of longer-term inflation compensation declined, returning to around the middle of their recent elevated range.

They seem to continue to give these quite a bit of weight.

In the forecast prepared for this meeting, the staff made little change to its projection for the growth of real gross domestic product (GDP) in 2008 and 2009. The available indicators of recent economic activity had come in close to the staff’s expectations and had continued to suggest that a substantial softening in economic activity was under way. The staff projection pointed to a contraction of real GDP in the first half of 2008 followed by a modest rise in the second half of this year, aided in part by the fiscal stimulus package.

Doesn’t look like there will be a contraction; so, GDP is likely to be higher than staff forecasts.

Here’s where the subsequent talk of headline measures passing into core was discussed.

The forecast of headline PCE inflation in 2008 was revised up in light of the further run-up in energy prices and somewhat higher food price inflation; headline PCE inflation was expected to exceed core PCE price inflation by a considerable margin this year. In view of the projected slack in resource utilization in 2009 and flattening out of oil and other commodity prices, both core and headline PCE price inflation were projected to drop back from their 2008 levels, in line with the staff’s previous forecasts.

They are relying on slack in 2009 to bring down this year’s inflation.

In conjunction with the FOMC meeting in April, all meeting participants (Federal Reserve Board members and Reserve Bank presidents) provided annual projections for economic growth, the unemployment rate, and inflation for the period 2008 through 2010. The projections are described in the Summary of Economic Projections, which is attached as an addendum to these minutes.

These were all before subsequent ‘better than expected’ releases, higher crude prices, and a falling USD.

In their discussion of the economic situation and outlook, FOMC participants noted that the data received since the March FOMC meeting, while pointing to continued weakness in economic activity, had been broadly consistent with their expectations. Conditions across a number of financial markets were judged to have improved over the intermeeting period, but financial markets remained fragile and strains in some markets had intensified. Although participants anticipated that further improvement in market conditions would occur only slowly and that some backsliding was possible, the generally better state of financial markets had caused participants to mark down the odds that economic activity could be severely disrupted by a further substantial deterioration in the financial environment.

Their concern of systematic tail risk has gone down substantially.

Economic activity was anticipated to be weakest over the next few months, with many participants judging that real GDP was likely to contract slightly in the first half of 2008. GDP growth was expected to begin to recover in the second half of this year, supported by accommodative monetary policy and fiscal stimulus, and to increase further in 2009 and 2010. Views varied about the likely pace and vigor of the recovery through 2009, although all participants projected GDP growth to be at or above trend in 2010. Incoming information on the inflation outlook since the March FOMC meeting had been mixed. Readings on core inflation had improved somewhat, but some of this improvement was thought likely to reflect transitory factors, and energy and other commodity prices had increased further since March. Total PCE inflation was projected to moderate from its current elevated level to between 1-1/2 percent and 2 percent in 2010, although participants stressed that this expected moderation was dependent on food and energy prices flattening out and critically on inflation expectations remaining reasonably well anchored.

As per Kohn’s latest speech, they have seen these inflation expectations begin to elevate.

Conditions across a number of financial markets had improved since the previous FOMC meeting. Equity prices and yields on Treasury securities had increased, volatility in both equity and debt markets had ebbed somewhat, and a range of credit risk premiums had moved down. Participants noted that the better tone of financial markets had been helped by the apparent willingness and ability of financial institutions to raise new capital. Investors’ confidence had probably also been buoyed by corporate earnings reports for the first quarter, which suggested that profit growth outside of the financial sector remained solid,

Yes, they have noted that outside the financial sector and housing the economy looks pretty good.

and also by the resolution of the difficulties of a major broker-dealer in mid-March.

Probably Bear Stearns.

NOTE: They didn’t refer to it by name.

Moreover, the various liquidity facilities introduced by the Federal Reserve in recent months were thought to have bolstered market liquidity and aided a return to more orderly market functioning. But participants emphasized that financial markets remained under considerable stress, noted that the functioning of many markets remained impaired, and expressed concern that some of the recent recovery in markets could prove fragile. Strains in short-term funding markets had intensified over the intermeeting period, in part reflecting continuing pressures on the liquidity positions of financial institutions. Despite a narrowing of spreads on corporate bonds, credit conditions were seen as remaining tight. The Senior Loan Officer Opinion Survey on Bank Lending Practices conducted in April indicated that banks had tightened lending standards and pricing terms on loans to both businesses and households. Participants stressed that it could take some time for the financial system to return to a more normal footing, and a number of participants were of the view that financial headwinds would probably continue to restrain economic activity through much of next year. Even so, the likelihood that the functioning of the financial system would deteriorate substantially further with significant adverse implications for the economic outlook was judged by participants to have receded somewhat since the March FOMC meeting.

The housing market had continued to weaken since the previous meeting, and participants saw little indication of a bottoming out in either housing activity or prices. Housing starts and the demand for new homes had declined further, house prices in many parts of the country were falling faster than they had towards the end of 2007, and inventories of unsold homes remained quite elevated. A small number of participants reported tentative signs that housing activity in a few areas of the country might be beginning to pick up, and a narrowing of credit risk spreads on AAA indexes of sub-prime mortgages in recent weeks was also noted. Nonetheless, the outlook for the housing market remained bleak, with housing demand likely to be affected by restrictive conditions in mortgage markets, fears that house prices would fall further, and weakening labor markets. The possibility that house prices could decline by more than anticipated, and that the effects of such a decline could be amplified through their impact on financial institutions and financial markets, remained a key source of downside risk to participants’ projections for economic growth.

There have been subsequent glimmers of hope that housing has stabilized and may be turning.

Growth in consumer spending appeared to have slowed to a crawl in recent months and consumer sentiment had fallen sharply. The pressure on households’ real incomes from higher energy prices and the erosion of wealth resulting from continuing declines in house prices likely contributed to the deceleration in consumer outlays. Reports from contacts in the banking and financial services sectors indicated that the availability of both consumer credit and home equity lines had tightened considerably further in recent months and that delinquency rates on household credit had continued to drift upwards. Consumer sentiment and spending had also been held down by the softening in labor markets–nonfarm payroll employment had fallen for the third consecutive month in March and the unemployment rate had moved up. The restraint on spending emanating from weakness in labor markets was expected to increase over coming quarters, with participants projecting the unemployment rate to pick up further this year and to remain elevated in 2009.

Subsequently, the unemployment rate fell.

Consumption spending was likely to be supported in the near term by the fiscal stimulus package, which was expected to boost spending temporarily in the middle of this year. Some participants suggested that the weak economic environment could increase the propensity of households to use their tax rebates to pay down existing debt and so might diminish the impact of the package. However, it was also noted that the tightening in credit availability might mean a significant number of households may be credit constrained and this might increase the proportion of the rebates that is spent. The timing and magnitude of the impact of the stimulus package on GDP was also seen as depending on the extent to which the boost to consumption spending is absorbed by a temporary run-down in firms’ inventories or by an increase in imports rather than by an expansion in domestic output.

The jurry is still out on this. My guess is the rebates will add more to GDP than forecasted.

The outlook for business spending remained decidedly downbeat. Indicators of business sentiment were low, and reports from business contacts suggested that firms were scaling back their capital spending plans. Several participants reported that uncertainty about the economic outlook was leading firms to defer spending projects until prospects for economic activity became clearer. The tightening in the supply of business credit was also seen as holding back investment, with some firms apparently reluctant to reduce their liquidity positions in the current environment. Spending on nonresidential construction projects continued to slow, although the extent of that slowing varied across the country. A few participants reported that the commercial real estate market in some areas remained relatively firm, supported by low vacancy rates.

Yes.

The strength of U.S. exports remained a notable bright spot. Growth in exports, which had been supported by solid advances in foreign economies and by declines in the foreign exchange value of the dollar, had partially insulated the output and profits of U.S. companies, especially those in the manufacturing sector, from the effects of weakening domestic demand. Several participants voiced concern, however, that the pace of activity in the rest of the world could slow in coming quarters, suggesting that the impetus provided from net exports might well diminish.

The March numbers subsequently released showed further acceleration of exports.

The information received on the inflation outlook since the March FOMC meeting had been mixed. Recent readings on core inflation had improved somewhat, although participants noted that some of that improvement probably reflected transitory factors. Moreover, the increase in crude oil prices to record levels, together with rapid increases in food and import prices in recent months, was likely to put upward pressure on inflation over the next few quarters. Prices embedded in futures contracts continued to point to a leveling-off of energy and commodity prices.

Still misreading the info implied from futures prices:

Although these futures contracts probably remained the best basis for projecting movements in commodity prices, participants emphasized the considerable uncertainty attending the likely path of commodity prices and cautioned that commodity prices in recent years had often advanced more quickly than had been implied by futures contracts. Several participants reported that business contacts had expressed growing concerns about the increase in their input costs and that there were signs that an increasing number of firms were seeking to pass on these higher costs to their customers in the form of higher prices. Other participants noted, however, that the extent of the pass-through of higher energy and food prices to core retail prices appeared relatively limited to date, and that profit margins in the nonfinancial sector remained reasonably high, suggesting that there was some scope for firms to absorb cost increases without raising prices. Available data and anecdotal reports indicated that gains in labor compensation remained moderate, and some participants suggested that wage growth was unlikely to pick up sharply in coming quarters if, as anticipated, labor markets remained relatively soft. However, several participants were of the view that wage inflation tended to lag increases in prices and so may not provide a useful guide to emerging price pressures.

Agreed!

On balance, participants expected the recent increases in oil and food prices to continue to boost overall consumer price inflation in the near term; thereafter, total inflation was projected to moderate, with all participants expecting total PCE inflation of between 1-1/2 percent and 2 percent by 2010. Participants stressed that the expected moderation in inflation was dependent on the continued stability of inflation expectations.

One can’t overstate the weight they all put on inflation expections, which are now seen as elevating.

A number of participants voiced concern that long-term inflation expectations could drift upwards if headline inflation remained elevated for a protracted period or if the recent substantial policy easing was misinterpreted by the public as suggesting that Committee members had a greater tolerance for inflation than previously thought.

This was again expressed recently by Vice Chair Kohn in his speech.

The possibility that inflation expectations could increase was viewed as a key upside risk to the inflation outlook. However, participants emphasized that appropriate monetary policy, combined with effective communication of the Committee’s commitment to price stability, would mitigate this risk.

‘Appropriate monetary policy’ opens the door for rate hikes.

Participants stressed the difficulty of gauging the appropriate stance of policy in current circumstances. Some participants noted that the level of the federal funds target, especially when compared with the current rate of inflation, was relatively low by historical standards. Even taking account of current financial headwinds, such a low rate could suggest that policy was reasonably accommodative. However, other participants observed that the pronounced strains in banking and financial markets imparted much greater uncertainty to such assessments and meant that measures of the stance of policy based on the real federal funds rate were not likely to provide a reliable guide in the current environment. Several participants expressed the view that the easing in monetary policy since last fall had not as yet led to a loosening in overall financial conditions, but rather had prevented financial conditions from tightening as much as they otherwise would have in response to escalating strains in financial markets. This view suggested that the stimulus from past monetary policy easing would be felt mainly as conditions in financial markets improved.

Seems there are three ‘camps’ on this point.

In the Committee’s discussion of monetary policy for the intermeeeting period, most members judged that policy should be eased by 25 basis points at this meeting. Although prospects for economic activity had not deteriorated significantly since the March meeting, the outlook for growth and employment remained weak and slack in resource utilization was likely to increase. An additional easing in policy would help to foster moderate growth over time without impeding a moderation in inflation.

There hasn’t been any forward looking sign of moderation since that meeting.

Moreover, although the likelihood that economic activity would be severely disrupted by a sharp deterioration in financial markets had apparently receded, most members thought that the risks to economic growth were still skewed to the downside. A reduction in interest rates would help to mitigate those risks. However, most members viewed the decision to reduce interest rates at this meeting as a close call.

Interesting statement!

The substantial easing of monetary policy since last September, the ongoing steps taken by the Federal Reserve to provide liquidity and support market functioning, and the imminent fiscal stimulus would help to support economic activity. Moreover, although downside risks to growth remained, members were also concerned about the upside risks to the inflation outlook, given the continued increases in oil and commodity prices and the fact that some indicators suggested that inflation expectations had risen in recent months. Nonetheless, most members agreed that a further, modest easing in the stance of policy was appropriate to balance better the risks to achieving the Committee’s dual objectives of maximum employment and price stability over the medium run.

The Committee agreed that that the statement to be released after the meeting should take note of the substantial policy easing to date and the ongoing measures to foster market liquidity. In light of these significant policy actions, the risks to growth were now thought to be more closely balanced by the risks to inflation. Accordingly, the Committee felt that it was no longer appropriate for the statement to emphasize the downside risks to growth. Given these circumstances, future policy adjustments would depend on the extent to which economic and financial developments affected the medium-term outlook for growth and inflation. In that regard, several members noted that it was unlikely to be appropriate to ease policy in response to information suggesting that the economy was slowing further or even contracting slightly in the near term, unless economic and financial developments indicated a significant weakening of the economic outlook.

In other words, no thought of more rate cuts without that change in outlook.

Votes for this action: Messrs. Bernanke, Geithner, Kohn, Kroszner, and Mishkin, Ms. Pianalto, Messrs. Stern and Warsh.

Votes against this action: Messrs. Fisher and Plosser.

Messrs. Fisher and Plosser dissented because they preferred no change in the target federal funds rate at this meeting. Although the economy had been weak, it had evolved roughly as expected since the previous meeting. Stresses in financial markets also had continued, but the Federal Reserve’s liquidity facilities were helpful in that regard and the more worrisome development in their view was the outlook for inflation. Rising prices for food, energy, and other commodities; signs of higher inflation expectations; and a negative real federal funds rate raised substantial concerns about the prospects for inflation. Mr. Plosser cited the recent rapid growth of monetary aggregates as additional evidence that the economy had ample liquidity after the aggressive easing of policy to date. Mr. Fisher was concerned that an adverse feedback loop was developing by which lowering the funds rate had been pushing down the exchange value of the dollar, contributing to higher commodity and import prices, cutting real spending by businesses and households, and therefore ultimately impairing economic activity. To help prevent inflation expectations from becoming unhinged, both Messrs. Fisher and Plosser felt the Committee should put additional emphasis on its price stability goal at this point, and they believed that another reduction in the funds rate at this meeting could prove costly over the longer run.

By notation vote completed on April 7, 2008, the Committee unanimously approved the minutes of the FOMC meeting held on March 18, 2008.

[top]

Recent comment by Fed Vice Chair Donald Kohn:

If longer-term inflation expectations were to become unmoored–whether because of a protracted period of elevated headline inflation or because the public misinterpreted the recent substantial policy easing as suggesting that monetary policy makers had a greater tolerance for inflation than previously thought–then I believe that we would be facing a more serious situation.

This could be telling. It hasn’t been said before by any FOMC member, and it was voluntary, in that no one asked the question.

It is something he is trying to communicate.

The FOMC sees inflation expectations showing signs of elevating, and is wondering whether it is at least partially responsible.

Their ‘theory’ had told them there was an inflation price to pay for cutting into a triple negative supply shock if it went so far as to allow inflation expectations to accelerate.

Credit spreads are in substantially from the wides, GDP isn’t collapsing and forecasts are for modest improvements.

Fiscal rebates are kicking in, being spent, and supporting prices.

Inflation is ripping, and now has the full attention of the FOMC.

Oil 130+

Dollar down

Stocks down a touch

Interest rates up a touch

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}