Why Won’t The Fed Tell Congress the Truth About Our Debt?

By Warren Mosler

Category Archives: Fed

The Fed’s operation tweet vs twist

Seems to me the force keeping yields down on the short end can be called operation tweet, as the Fed is simply announcing its forecasts for lower rates, which are subject to immediate change, data dependent.

But with operation twist, the Fed actually buys the longer term securities vs just talking about them, as it also lightens up on the shorter term securities.

So after the current knee jerk reaction to tweet I’m looking at the ramifications of twist to dominate.

The Fed Is Misleading Congress About Europe – US Business News Blog – CNBC

The Fed is Starving Economy of Interest Income – US Business News Blog – CNBC

The Fed is Starving Economy of Interest Income

By Warren Mosler

He left out the part about needing a fiscal adjustment to compensate but this is part one of a three part presentation of something I wrote.

from a primary dealer

Preface. I generally subscribe to the view that in free currencies, deficits are mostly self-funding, and ‘enormous’ deficits needn’t be accompanied by higher yields. Government builds a bridge, pays the bridgebuilder, who pays the grocer, who eventually either buys the Treasury or deposits in a bank whose reserves are fungible vs T-bills via the intermediating Fed. Government dissavings and private sector savings are equal and offsetting, as long as the Central Bank has a working spreadsheet and an interest rate target. Yields are just a function of duration needs of savers vs borrowers, but the AMOUNTS always match up. Likewise, I don’t believe that the creation of bank reserves is inflationary or hyper-inflationary; bank lending is capital – not reserve – constrained. Loan officers don’t check the vaults. There is always enough. I continue to marvel at the armies of deficit vigilantes who take aim at Treasuries and JGBs, armed with Gold Standard thinking or even the latest Reinhart/Rogoff, only to retreat 2-3 year later. It didn’t work shorting US Treasuries in 2009-2010 for the ‘money supply’ or ‘deficit spike,’ and that roadside is stacked with corpses. Even the Home Run deficit vigilante hitters who nailed Europe this year (and Europe is, for now, operating as a quasi-Gold standard and an entirely different set of risks) offset those gains with losses betting the other way on the US, UK, and Japan. It’s evident in the returns.

Central Banks ‘Printing Money Like Gangbusters’: Gross

Can’t argue with success:

Central Banks ‘Printing Money Like Gangbusters’: Gross

By Margo D. Beller

Jan 11 (CNBC) — The world’s central banks are “printing money like gangbusters,” which could revive the threat of inflation , Pimco founder Bill Gross told CNBC Wednesday.

By putting “hundreds of billions” in currency in circulation, the central banks “can produce reflation—that’s why we’re seeing the pop in oil, gold” and other commodities, he said in a live interview.

At the same time, “there’s the potential for deflation if the private credit markets can’t produce some sort of confidence and solvency going forward,” Gross said. “So we’re at great risk here, not only in the U.S. but on a global basis.”

Gross has previously predicted a “paranormal” market in 2012 characterized by “credit and zero-bound interest rate risk” and fewer incentives for lenders to extend credit.

He said stock and bond investors must lower their expectations when it comes to returns, with 2 percent to 5 percent as good as they get this year.

He also told CNBC he expects the Federal Reserve will keep interest rates “exactly where it is at 25 basis points for the next three to four years.”

Gross’s Total Return Fund, the world’s largest bond fund, had over $10 billion in outflows in 2011, but Gross stressed the fund “started 2011 at $240 billion and ended it at $244 billion.”

He said he will run the Pimco Total Return Fund ETF , which starts March 1, the same way he runs the bond Total Return Fund, adding, “They’re twins.”

Federal Reserve p/l

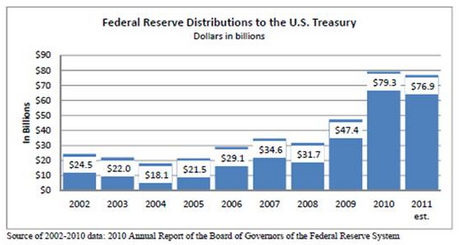

Federal Reserve to Return $76.9 Billion to US Treasury From What Central Bank Earned in 2011

Yes, income the economy would have earned without QE…

How about rotating the BOJ governors with the FOMC? ;)

.

Proposal update, including the JG

My proposals remain:

1. A full FICA suspension:

The suspension of FICA paid by employees restores spending which supports output and employment.

The suspension of FICA paid by business helps keep costs down which in a competitive environment lowers prices for consumers.

2. $150 billion one time distribution by the federal govt to the states on a per capita basis to get them over the hump.

3. An $8/hr federally funded transition job for anyone willing and able to work to assist in the transition from unemployment to private sector employment.

Call me an inflation hawk if you want. But when the fiscal drag is removed with the FICA suspension and funds for the states I see risk of what will be seen as ‘unwelcome inflation’ causing Congress to put on the brakes long before unemployment gets below 5% without the $8/hr transition job in place, even with the help of the FICA suspension in lowering costs for business.

It’s my take that in an expansion the ’employed labor buffer stock’ created by the $8/hr job offer will prove a superior price anchor to the current practice of using the current unemployment based buffer stock as our price anchor.

The federal government caused this mess for allowing changing credit conditions to cause its resulting over taxation to unemploy a lot more people than the government wanted to employ. So now the corrective policy is to suspend the FICA taxes, give the states the one time assistance they need to get over the hump the federal government policy created, and provide the transition job to help get those people that federal policy is causing to be unemployed back into private sector employment in a more orderly, more ‘non inflationary’ manner.

I’ve noticed the criticism the $8/hr proposal- aka the ‘Job Guarantee’- has been getting in the blogosphere, and it continues to be the case that none of it seems logically consistent to me, as seen from an MMT perspective. It seems the critics haven’t fully grasped the ramifications of the recognition of the currency as a (simple) public monopoly as outlined in Full Employment AND Price Stability and the other mandatory readings.

So yes, we can simply restore aggregate demand with the FICA suspension and funds for the states, but if I were running things I’d include the $8 transition job to improve the odds of both higher levels of real output and lower ‘inflation pressures’.

Also, this is not to say that I don’t support the funding of public infrastructure (broadly defined) for public purpose. In fact, I see that as THE reason for government in the first place, and it should be determined and fully funded as needed. I call that the ‘right size’ government, and, in general, it’s not the place for cyclical adjustments.

4. An energy policy to help keep energy consumption down as we expand GDP, particularly with regard to crude oil products.

Here my presumption is there’s more to life than burning our way to prosperity, with ‘whoever burns the most fuel wins.’

Perhaps more important than what happens if these proposals are followed is what happens if they are not, which is more likely going to be the case.

First, given current credit conditions, world demand, and the 0 rate policy and QE, it looks to me like the current federal deficit isn’t going to be large enough to allow anything better than muddling through we’ve seen over the last few years.

Second, potential volatility is as high as it’s ever been. Europe could muddle through with the ECB doing what it takes at the last minute to prevent a collapse, or doing what it takes proactively, or it could miss a beat and let it all unravel. Oil prices could double near term if Iran cuts production faster than the Saudis can replace it, or prices could collapse in time as production comes online from Iraq, the US, and other places forcing the Saudis to cut to levels where they can’t cut any more, and lose control of prices on the downside.

In other words, the risk of disruption and the range of outcomes remains elevated.