Will Greece Resolution Spark a Bigger Crisis?

By John Carney

Mar 8 (CNBC) — Markets around the world were buoyed on hopes that Greece’s long and winding journey to debt restructuring may at last be its final port of call.

But some are warning that this may actually be the beginning of a new and more dangerous crisis.

The private sector is being asked to write off more than 70 percent of the face value of their Greek government bonds in return for new debt. This will help Greece meet its debt obligations and enable it to tap into bailout funds from the EU and IMF.

It seems likely that other nations burdened by heavy debt loads and high interest rates may seek to follow Greece’s path to debt relief. If Greece doesn’t have to pay what it owes, they might argue, why should we? Call it Haircut Contagion.

European officials insist that Greece is a one-time deal, not meant to set a precedent for other nations. But it is easy to see that minority parties in debt-burdened European nations could find a demand for relief an attractive platform. Imposing a “tax” on bondholders rather asking citizens to pay higher taxes while public services are cut might prove popular with voters.

Demands for debt relief could take many forms. Greece has been able to encourage bond holders to participate in the debt swap by enacting laws that incorporated “collective action clauses” into the 86 percent of bonds governed by Greek law. These clauses allow super-majorities of bond holders to force hold-outs to participate in swaps. Other countries in the euro zone could replicate this strategy.

“Effectively, this is a large gift from the Greeks to the parts of the euro zone that face debt crises. By conducting its debt exchange in the way it did, Greece has in effect resurrected the plausibility of purely voluntary debt-reduction operations in Europe,” Moody’s has explained.

Such demands would put new strains on the global financial system. While Europe’s banks and insurance companies can withstand losses on Greek debt, a series of similar haircuts might destabilize the system and render some institutions insolvent.

Warren Mosler, a trader based in the Virgin Islands who is credited with creating the euro-swap futures contract, fears that all it would take to set off a panic would be serious political discussion of widespread haircuts.

“The idea of Greek default transformed from being a Greek punishment to a gift, with the pending question: ‘If Greece doesn’t have to pay, why do I?’ — threatening a far more disruptive outcome that is yet to be fully discounted,” Mosler writes on his website, Mosler Economics. “That is, should Greek bonds be formally discounted, the consequences of merely the political discussion of that question will be all it takes to trigger a financial crisis rivaling anything yet seen.”

He has spelled out exactly what he thinks would happen in a Haircut Contagion crisis.

“Possible immediate consequences of that discussion include a sharp spike in gold, silver, and other commodities in a flight from currency, falling equity and debt valuations, a banking crisis, and a tightening of ‘financial conditions’ in general from portfolio shifting, even as it’s fundamentally highly deflationary. And while it probably won’t last all that long, it will be long enough to seriously shake things up,” Mosler writes.

A recent paper cited by Reuters took a much more sanguine approach to the likelihood of Haircut Contagion. The ratings agency figures that countries may attempt to receive modest debt relief in exchange for giving up their rights to unilaterally change the terms of their debt. They could do this, for example, by restructuring bonds governed by domestic law into foreign law bonds, mostly likely governed by English law.

“Holders of local-law governed bonds in other euro zone countries that are perceived to be at risk might want to make a trade for English-law governed bonds,” Jeromin Zettelmeyer, deputy chief economist at the European Bank for Reconstruction and Development, and Duke University Professor Mitu Gulati, wrote in the paper. “Depending on how much these bondholders would be willing to pay to make this trade, it could serve the interest of the country as well to make it.”

Of course, countries that agreed to make this swap would be sacrificing a lot of their future flexibility. Some might find it too high a price to pay. In a sense, converting their debt to foreign jurisdiction bonds would be like doubling-down on the structural problems with the euro zone. The countries that did this would sacrifice sovereignty over their debt to achieve lower interest rates, much like they sacrificed monetary sovereignty for the currency union.

And it’s not clear that this would be all that attractive to bondholders, either. After all, a country that cannot or will not pay its debt cannot be forced to, just because the bonds are subject to foreign law.

The hope of European leaders was that preventing a disorderly default in Greece would avoid a domino effect of sovereign debt defaults. The danger, however, is that debt relief for Greece could spark a new and unexpected Haircut Contagion crisis.

Category Archives: ECB

Talk of other member nation haircuts slowly surfacing

Talk of widespread haircuts getting more serious. As previously discussed, this has the potential for catastrophic global financial meltdown.

Analysis: Greek default may be gift to other euro strugglers

By Mike Dolan

Mar 7 (Reuters) — Greece’s tortuous debt restructuring and threat of retroactive laws to compel reluctant creditors heaps regulatory risk onto investors but may make voluntary sovereign debt revamps more attractive and likely for other cash-strapped euro sovereigns and their creditors.

Thursday could mark a climax of the Greek debt workout with private creditors due to respond to an offer that would see them effectively write off more than 70 percent of the face value of their bonds in return for new debt with a series of sweeteners.

With Greek government bonds currently trading at less than 20 cents in the euro and the risk of a total wipeout if Greece decided to unilaterally refuse all payments, a majority will likely go for it. Legally-binding majorities are another matter.

Athens said this week it aims for 90 percent acceptance but if the takeup is at least 75 percent then it would consider triggering so-called “collective action clauses” retroactively inserted into the bonds issued under Greek law — about 85 percent of the 200 billion euros being restructured.

Those clauses in practice force all affected creditors to comply.

But it’s this distinction between debt issued under domestic laws and that sold under internationally-accepted English law that some say has consequences for other troubled euro nations eyeing Greece’s so-called Private Sector Involvement, or PSI.

A GIFT FROM GREECE

In essence, English-law Greek bonds, as is the case for many emerging market sovereigns, trade as if they were senior to local-law debt — at almost twice the price in fact right now. That’s because the terms of foreign-law bonds cannot be altered by an Athens parliament, and agreement for debt swaps is needed bond-by-bond, unlike local laws that aggregate majorities across all debtors and make blocking minorities more difficult to muster.

A paper released this week by Jeromin Zettelmeyer, deputy chief economist at the European Bank for Reconstruction and Development, and Duke University Professor Mitu Gulati reckons this legal gulf could well encourage other debt-hobbled euro zone countries and their creditors into mutually acceptable and beneficial debt restructurings.

This would involve an agreed switch in the legal status of the debt in return for relatively modest haircuts.

“Holders of local-law governed bonds in other euro zone countries that are perceived to be at risk might want to make a trade for English-law governed bonds,” the economists wrote. “Depending on how much these bondholders would be willing to pay to make this trade, it could serve the interest of the country as well to make it.”

The sovereign gets a chance to reduce a crippling debt burden while bondholders get greater contractual protection in any future restructuring.

Given that the Greek precedent of retroactive legislation vastly increases the allure of foreign-law bonds, which credit rating firm Moody’s says now make up less than 10 percent of all euro zone government bonds, a window of opportunity may open up.

“Effectively, this is a large gift from the Greeks to the parts of the euro zone that face debt crises. By conducting its debt exchange in the way it did, Greece has in effect resurrected the plausibility of purely voluntary debt-reduction operations in Europe.”

Although Berlin, Paris and Brussels insist the Greek case is a one-off and European Central Bank liquidity has insulated the wider banking system, Portugal’s 10-year bonds still trade as low as 50 cents in the euro and many creditors reckon it will be very difficult for the country to avoid some restructuring.

Even the 10-year debt of fellow bailout recipient Ireland, which many investors reckon has the underlying economic capacity to go back to the markets next year, is still trading at less than 90 cents in the euro and many doubt its imminent market return.

“We still expect a sizeable growth undershoot and deficit overshoot and expect that Ireland will need a second financing package (which may include PSI) beyond 2013,” economists at Citi said on Monday.

What’s more, if Europe’s new fiscal pact is rejected by voters in a planned referendum there in the coming months, Ireland would lose access to the financial backstop of the European Stability Mechanism and likely unnerve many investors.

Yet voluntary debt swaps with some debt relief stemming from more modest haircuts than Greece may well be the best way to ensure these two countries avoid outright default and return to private financing in a reasonable amount of time.

And if such exchanges were wholly voluntary, it would also mean credit default swap insurance would not pay out — a stated aim for many euro policymakers concerned about the speculative nature of a market where it’s possible to buy insurance on something you don’t own.

One danger is that the prospect of countries opting for such a swap may scare creditors in larger countries like Italy and Spain where currently no bond haircut is expected by the market, thanks in large part to the ECB’s liquidity injections.

And the upshot for many economists is that there will be a longer-term price to pay for governments for tinkering with the rules of the game, as many investors view it, via the likes of retroactive bond legislation and obfuscation of CDS markets.

“Investors will expect a premium for bearing this regulatory risk,” Morgan Stanley’s Manoj Pradhan told clients in a note, adding that only central bank liquidity floods were now obscuring the resultant higher financing costs and there would be a dangerous blurring of lines between macro and market risks.

But given that indiscriminate cheap lending was seen as at least partly responsible for the credit binge and bust of the past five years, maybe higher risk premia are not all bad.

GS: ECB Preview

I agree that the ECB is ‘backing off’ and will only again engage if it gets bad enough.

Back to the analogy of watering the flower only when it’s about to die.

They don’t realize that it needs continuous watering in the normal course of events.

14 more days to the Greek payment date.

Unfortunately, looking like darned if you do and darned if you don’t.

ECB after the LTROs: It is up to governments now

After the implementation of the second 3-year LTRO last week, the ECB now is likely to believe it has done enough to stabilise the Euro area’s financial system and, implicitly, the funding situation for peripheral governments. Any announcement of further non-standard measures seems unlikely at this stage, as the Governing Council now views the ball as being squarely in the court of governments.

Are Japanese Banks Bailing Out Europe?- John Carney reposts my article

ECB reports Spanish and Italian banks’ Dec and Jan bond buying

Looks like the drop in Spanish and Italian bond yields was at least partially driven by Spanish and Italian bank buying of their govt’s debt. While the LTRO did provide floating rate ECB term funding, funding has generally been available in any case, and the bond buying did add risk and ‘use up’ bank capital. So I suspect there is still more to it than has so far been disclosed.

ECB figures published on Monday showed that Spanish banks increased their government debt holdings by more than €23bn in January while Italian banks bought nearly €21bn – both record monthly increases. Over December and January, Italian and Spanish banks increased their holdings by 13 and 29 per cent to €280bn and €230bn respectively.

LTRO birdie telling me maybe the BOJ gave the nod to its banks

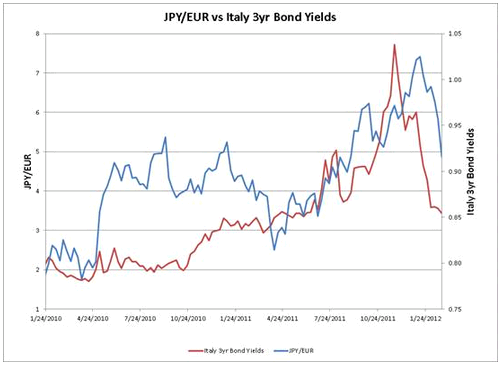

Just a hunch now, but Italian, Spanish, and related bond yields began falling coincident with the first ECB LTRO. The question is why, as I saw no operative channel of consequence from ECB liquidity provision of 3 year funds on a floating rate basis to the term structure of rates.

So it seemed to me that also coincident to the LTRO was some entity giving the nod to its banks to buy those bonds, or some reason sellers of those bonds backed off.

I’m now thinking it may have been the BOJ giving the nod to its member banks to buy euro member debt denominated in euro and keep the fx risk on their books, with the assurance govt policy would keep the yen weak and guarantee the banks an fx profit.

We learned after the fact that Japan had been selling yen well before they announced their new weak yen stance. And having their banks buy euro member euro denominated debt directly weakens the yen vs the euro.

The timing of the events- the LTRO/yen sell off/yen policy change- is close enough to get my attention.

So Japan managed to weaken the yen and firm euro member debt prices all under the cover of the ECB LTRO operation which they gladly allowed to take the credit.

In any case, I don’t expect any more from this next LTRO than I expected from the last, but I am keeping a close eye on the yen.

More on Greece and the euro

As previously discussed, all policies seem to be ‘strong euro’ first.

And the ‘success’ of the euro continues to be gauged by its ‘strength’.

The haircuts on the Greek bonds are functionally a tax that removes that many net euro financial assets. Call it an ‘austerity’ measure extending forced austerity to investors.

Other member nations will likely hold off on turning towards that same tax until after Greece is a ‘done deal’ as early noises could work to undermine the Greek arrangements, and take the ‘investor tax’ off the table.

Like most other currencies, the euro has ‘built in’ demand leakages that fall under the general category of ‘savings desires’. These include the demand to hold actual cash, contributions to tax advantaged pension contributions, contributions to individual retirement accounts, insurance and other corporate ‘reserves’, foreign central bank accumulations euro denominated financial assets, along with all the unspent interest and earnings compounding.

Offsetting all of that unspent income is, historically, the expansion of debt, where agents spend more than their income. This includes borrowing for business and consumer purchases, which includes borrowing to buy cars and houses. In other words, net savings of financial assets are increased by the demand leakages and decreased by credit expansion. And, in general, most of the variation is due to changes in the credit expansion component.

Austerity in the euro zone consists of public spending cuts and tax hikes, which have both directly slowed the economies and increased net savings desires, as the austerity measures have also reduced private sector desires to borrow to spend. This combination results in a decline in sales, which translates into fewer jobs and reduced private sector income. Which further translates into reduced tax collections and increased public sector transfer payments, as the austerity measures designed to reduce public sector debt instead serve to increase it.

Now adding to that is this latest tax on investors in Greek debt, and if the propensity to spend any of the lost funds of those holders was greater than 0, aggregate demand will see an additional decline, with public sector debt climbing that much higher as well.

All of which serves to make the euro ‘harder to get’ and further support the value of the euro, which serves to keep a lid on the net export channel. The ‘answer’ to the export dilemma would be to have the ECB, for example, buy dollars as Germany used to do with the mark, and as China and Japan have done to support their exporters. But ideologically this is off the table in the euro zone, as they believe in a strong euro, and in any case they don’t want to build dollar reserves and give the appearance that the dollar is ‘backing’ the euro.

And all of which works to move all the euro member nation deficits higher as the ‘sustainability math’ of all deteriorate as well, increasing the odds of the ‘investor tax’ expanding to the other member nations that continues the negative feedback loop.

Given the demand leakages of the institutional structure, as a point of logic prosperity can only come from some combination of increased net exports, a private sector credit expansion, or a public sector credit expansion.

And right now it looks like they are still going backwards on all three.

Greece

Comes back to the idea that resolving solvency issues in the euro zone doesn’t fix the economy.

And with negative growth the solvency math doesn’t work for any of the euro members.

And what’s with the ECB threatening to back away on liquidity support for the banking system?

So looks to me like the Greek resolution is not the end of the solvency issues, but that the focus simply moves on to the next weaker sister.

And, as previously discussed, the risk remains elevated that if Greece gets to haircut its obligations and gets funding, others will ask for the same, triggering a general, global, catastrophic financial meltdown.

My first order proposal remains an ECB distribution on a per capita basis to the euro member nations of maybe 10% of euro zone GDP per year to put the solvency issue behind them. Along with relaxed budget rules, maybe allowing deficits up to 6% of GDP annually, further supported by the ECB funding a transition job at a non disruptive wage to facilitate the transition from unemployment to private sector employment. I might also recommend deficits be increased by suspending VAT as a way to increase aggregate demand and lower prices at the same time.

Alternatively, the ECB could simply guarantee all national govt debt and rely on the growth and stability pact for fiscal discipline, which would probably require enhanced authorities.

And rather than trying to bring Greece’s deficit down to current target levels, they could instead relax the growth and stability pact limits to something closer to full employment levels. And, again, I’d look into suspending VAT to both increase aggregate demand and lower prices.

Meanwhile, elsewhere in today’s world news:

The likes of Ford adding to pension funds makes the point of the increasing and ongoing demand leakages putting a damper on GDP.

And oil prices have now crept up enough to materially cut into aggregate demand as well.

Nor are banks adding to capital to meet expanding demand for credit, which remains anemic.

Headlines:

Data Suggests Euro Zone May Slide Back Into Recession

German Manufacturing Slows as New Export Orders Fall

China’s Factory Activity Shrinks for Fourth Month

ECB Preparing to Close Liquidity Floodgates

Ford Pours $3.8 Billion Into Pension Plan

Oil Could Turn to Headwind as Dow Flirts With 13,000

UBS to Issue More Loss-Absorbing Capital

Iran ‘Winning’ on Oil Sanctions: Top Trader

Greek Bailout Puts Focus Back on Credit Default Swaps

Iran Fuels Oil-Price Rally—And Prices Could Keep Rising

Marshall Auerback video

euro zone update- markets yet to discount the discounts

The issues I’ve been discussing over the last year or two while now crystallizing, remain highly problematic.

The idea of Greek default transformed from being a Greek punishment to a gift, with the pending question: ‘If Greece doesn’t have to pay, why do I?’- threatening a far more disruptive outcome that is yet to be fully discounted.

That is, should Greek bonds be formally discounted, the consequences of merely the political discussion of that question will be all it takes to trigger a financial crisis rivaling anything yet seen.

And note, also as previously discussed, that there has yet to be an actual Greek default, and that all Greek bonds have continued to mature at par, as there has yet to be an acceptable alternative.

So what are the alternatives?

1. Continue to fund Greece with terms and conditions.

2. Don’t fund Greece which forces:

a. Greece is forced to limit spending to actual tax revenues

b. Greece moves back to the drachma

And what are the ‘terms and conditions’?

Austerity is always the lead demand, which slows both the Greek economy and to some extent the euro zone in general.

Additional demands currently include discounting Greek bonds to bring down their debt to GDP ratio to ‘sustainable’ levels. However, after 8 months of negotiations, this has proven highly problematic, probably for reasons yet to be fully disclosed. And, as just discussed, there may be a growing awareness that discounting opens Pandora’s box with the politically attractive question ‘if Greece doesn’t have to pay, why do we?’

So what actually happens?

My best guess, and not with a lot of conviction, is that nothing is concluded before the coming maturity dates, and the ECB winds up writing the check to support short term Greek funding to buy more time for more inconclusive discussion. So, again as previously discussed, seems like this is the solution- death by 1,000 cuts and reluctant ECB bond buying when push comes to shove to keep it all going.

And, currently, the catastrophic risk I’d highly recommend immediately hedging is the risk that Greek bonds are formally discounted, rapidly followed by a global discussion of ‘so why should we have to pay?’ Possible immediate consequences of that discussion include a sharp spike in gold, silver, and other commodities in a flight from currency, falling equity and debt valuations, a banking crisis, and a tightening of ‘financial conditions’ in general from portfolio shifting, even as it’s fundamentally highly deflationary. And while it probably won’t last all that long, it will be long enough to seriously shake things up.