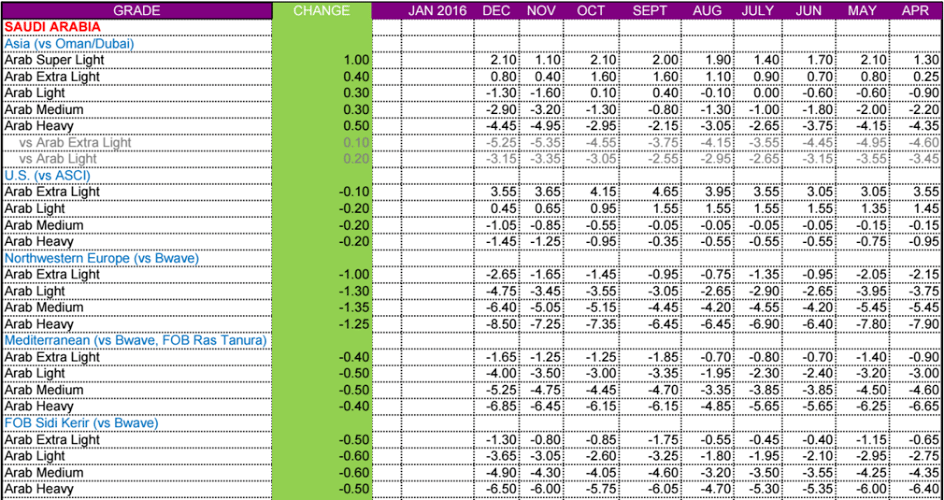

This means they continue with their discount policy until their entire output capacity is being sold, and then continue to sell their full output capacity at ‘market prices’. That is, they no longer want the high priced producers to benefit from their willingness to to be swing producer and support prices by not selling their full output:

Moving ahead, Opec — led by Saudi Arabia — plans to pump as much as it can towards meeting global oil demand, leaving higher-cost producers to make up the remainder.

For higher-cost producers, “$100 oil was perceived as a guarantee of no risk for investment”, said Mr Falih. “Now, the insurance policy that’s been provided free of charge by Saudi Arabia does not exist any more.”

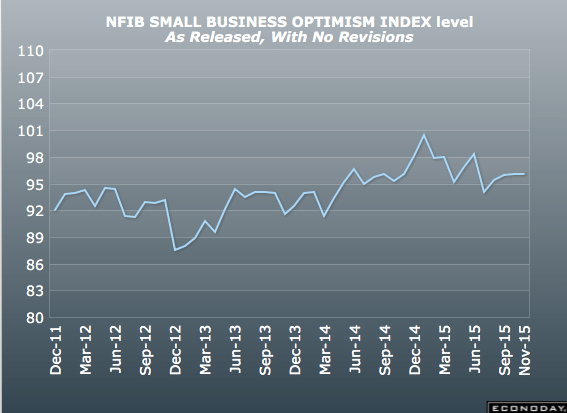

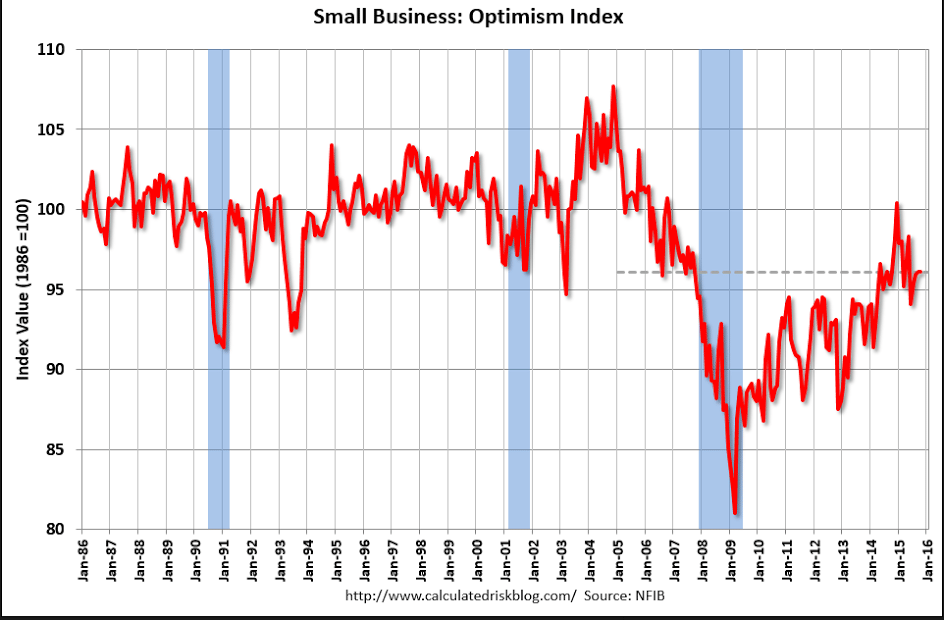

Regarding the NFIB small business survey for October released yesterday:

GDP growth languished in Q3, and will not likely impress in Q4. The industrial sector is weakening and the small business sector has not returned to its historical role in the production of GDP and jobs. The October NFIB survey gave no indication of a resurgence in growth in the small business sector, readings remaining below average.

NFIB chief economist Bill Dunkelberg states:

The October NFIB survey gave no indication of a resurgence in growth in the small business sector with the Index remaining below the 42 year average of 98. The labor market components might have held at historically strong levels but this time owners reported no net growth in employment, which is a significant drop from reports in the previous four months.

Profits and Wages. Earnings trends deteriorated 3 points, falling to a negative 16 percent. Far more owners are reporting profits lower quarter to quarter than higher. A seasonally adjusted net 21 percent of owners reported raising worker compensation, down 2 points from September and 4 points below the expansion high reading reached in January and May. The net percent planning to increase compensation rose 1 point to 17 percent, still strong for this recovery.

Labor Markets. Reported job creation came to a halt in October, with owners adding a net 0.0 workers per firm in recent months. Fifty-five percent reported hiring or trying to hire (up 2 points), but 48 percent reported few or no qualified applicants for the positions they were trying to fill. Fourteen percent reported using temporary workers, unchanged from September. Twentyseven percent of all owners reported job openings they could not fill in the current period, unchanged from September. A seasonally adjusted net 11 percent plan to create new jobs, down 1 point. A seasonally adjusted net 21 percent of owners reported raising worker compensation, down 2 points from the past few months. The percent of owners citing the difficulty of finding qualifed workers as their Most Important Business Problem fell 3 points to 13 percent, but still third on the list of problems behind taxes and regulations and red tape.

Profits and Wages. Earnings trends deteriorated 3 points, falling to a negative 16 percent. Far more owners are reporting profits lower quarter to quarter than higher. A seasonally adjusted net 21 percent of owners reported raising worker compensation, down 2 points from September and 4 points below the expansion high reading reached in January and May. The net percent planning to increase compensation rose 1 point to 17 percent, still strong for this recovery.

Inventory and Sales. The net percent of all owners (seasonally adjusted) reporting higher nominalsales in the past 3 months compared to the prior 3 months deteriorated 7 percentage points to a net negative 8 percent. Twelve percent cited weak sales as their top business problem, up 1 point. Expected real sales volumes posted a 3 point improvement, rising to a seasonally adjusted net 4 percent of owners expecting gains, a long way down from the 20 percent reading in December 2014. Overall, not a very positive outlook, but at least positive. The net percent of owners reporting inventory increases was a net negative 2 percent (seasonally adjusted), down 2 points. The net percent of owners viewing current inventory stocks as “too low” was unchanged a net negative 4 percent, as weak sales made current stocks look excessive and future sales are not expect to grow much. The net percent of owners planning to add to inventory fell 3 points to a net 0 percent, not much help for Q4 GDP growth.

Capital Spending. Fifty-eight percent reported capital outlays, unchanged from August and September. The percent of owners planning capital outlays in the next 3 to 6 months gained 1 point to 26 percent, not a strong reading historically but among the best in this expansion. Owner expectations for the economy overall appear to anticipate a continuation of “under-performance”. Investment plans remain historically sub-par, and owners have little interest in borrowing to support investment spending that promises little return. The small business sector remains in “maintenance mode”.