- ABC Consumer Confidence (Released 17:00 EST)

ABC Consumer Confidence (May 4)

| Survey | -41 |

| Actual | -46 |

| Prior | -41 |

| Revised | n/a |

This is a one man vote survey, and a lot of low income people are getting hurt by this shift to an export economy.

[top]

| Survey | -41 |

| Actual | -46 |

| Prior | -41 |

| Revised | n/a |

This is a one man vote survey, and a lot of low income people are getting hurt by this shift to an export economy.

[top]

TABLE-US chain store sales fell 0.2 pct last week-ICSC

Tue May 6, 2008 7:45am EDT

NEW YORK, May 6 (Reuters) – The International Council ofShopping Centers and UBS Securities on Tuesday released the following seasonally adjusted weekly data on U.S. chain store retail sales.

WEEK ENDING INDEX 1977=100 YEAR/YEAR CHANGE (%) WEEKLY CHANGE (%) May 3 495.4 2.3 -0.2 April 26 496.3 1.9 0.9 April 19 491.8 1.4 -0.7 April 12 495.3 1.8 0.9 The ICSC-UBS weekly U.S. retail chain store sales index is ajoint publication between ICSC and UBS Securities LLC. It measures nominal same-store sales, excluding restaurant and vehicle demand, and represents about 75 retail chain stores.

Muddling through like most export economies.

Year over year looks okay.

(an interoffice email)

A few observations:1) when chart 1 peaked in 5/01, we still had six months of recession to deal

with and the Fed didn’t stop cutting until 12/01 at 1.75%.

2) data only goes back to 1990, but the 5/90 peak was BEFORE the recession even

started, it didn’t end until 3/91 and the Fed didn’t stop cutting until 8/92 @

3%.

3) EDM9 has two + hikes priced in (three at the recent lows). the EDZ8 thru

EDU9 part of the eurodollar curve seems awfully cheap to me.

*FED REPORTS NEAR-RECORD PACE OF BANKS TIGHTENING LOAN TERMS

*FED SAYS CONSUMER, BUSINESS LOANS WEAKER FOR PAST THREE MONTHS

*FED SAYS 55% OF BANKS TOUGHENED BUSINESS LENDING SINCE JANUARY

*FED SURVEY GAUGES LENDING POLICY BY 56 U.S., 21 OVERSEAS BANKS

*FED SAYS DEMAND MORE RESTRAINED FOR CONSUMER, BUSINESS LOANS

*FED SENIOR LOAN OFFICERS SURVEY COVERS PAST THREE MONTHS==============================

============================== ==================

April  Jan.  Oct.  July April  Jan.  Oct.  July

2008  2008  2007  2007  2007  2007  2006  2006

============================================================ ===================

——————Percentage of Total——————

Large & mid-market     100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Tightened considerably  3.6%  1.8%  1.9%  0.0%  0.0%  0.0%  0.0%  0.0%

Tightened somewhat     51.8% 30.4% 17.3%  9.4%  3.8%  5.3%  7.4%  5.4%

Basically unchanged    44.6% 67.9% 80.8% 88.7% 88.7% 89.5% 85.2% 80.4%

Eased somewhat          0.0%  0.0%  0.0%  1.9%  7.5%  5.3%  7.4% 14.3%

Eased considerably      0.0%  0.0%  0.0%  0.0%  0.0%  0.0%  0.0%  0.0%

——————–Number of Banks——————–

Large & mid-market         56    56    52    53    53    57    54    56

Tightened considerably     2     1     1     0     0     0     0     0

Tightened somewhat        29    17     9     5     2     3     4     3

Basically unchanged       25    38    42    47    47    51    46    45

Eased somewhat             0     0     0     1     4     3     4     8

Eased considerably         0     0     0     0     0     0     0     0

============================================================ ===================

NOTE: Large and middle-market firms are those with annual sales of $50 million

or more.SOURCE: Federal Reserve FRBA <GO>

Thanks,

Don’t forget to add ‘and the economy is improving’ with GDP looking a lot like it bottomed in Q4.

With fiscal adding a quick $170 billion or so of net financial assets/spending power to demand over the next few months watch for additional price pressures across the board.

| Survey | 49.1 |

| Actual | 52.0 |

| Prior | 49.6 |

| Revised | n/a |

[top]

Nice bounce back, above expectations, back above 50, but the chart still looks like it’s slowly working its way lower.

The table shows gains in employment to 50.8 from 46.9, and Prices Paid up to a 5 month high of 72.1

Twin themes intact: weakness (but no recession) and rising prices.

Crude just printed above $120, as Saudis remain firmly in control.

[top]

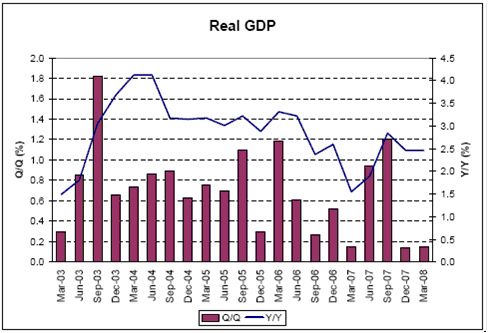

U.S. First Quarter Advance GDP: Statistical Summary (Table)

by Kristy Scheuble

(Bloomberg) Following is a summary of Gross Domestic Product from the Commerce Department.

1Q 4Q 3Q 2Q 1Q 4Q 3Q 2008 2007 2007 2007 2007 2006 2006 Annualized Quarterly Change

Real GDP 0.6% 0.6% 4.9% 3.8% 0.6% 2.1% 1.1% YOY percent 2.5% 2.5% 2.8% 1.9% 1.5% 2.6% 2.4%

Year over year looks fine.

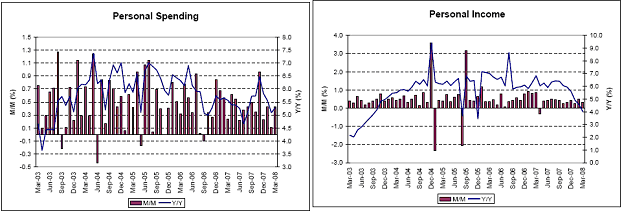

Personal consumption 1.0% 2.3% 2.8% 1.4% 3.7% 3.9% 2.8%

Down, but holding positive as income continues to grow.

Durable goods -6.1% 2.0% 4.5% 1.7% 8.8% 3.9% 5.6% Nondurable goods -1.3% 1.2% 2.2% -0.5% 3.0% 4.3% 3.2% Services 3.4% 2.8% 2.8% 2.3% 3.1% 3.7% 2.0%

Services picking up the slack from goods.

Gross private investment -4.7% -14.6% 5.0% 4.6% -8.2% -14.1% -4.1% Fixed investment -9.7% -4.0% -0.7% 3.2% -4.4% -7.1% -4.7% Nonresidential -2.5% 6.0% 9.3% 11.0% 2.1% -1.4% 5.1% Structures -6.2% 12.4% 16.4% 26.2% 6.4% 7.4% 10.8% Equipment & software -0.7% 3.1% 6.2% 4.7% 0.3% -4.9% 2.9% Residential -26.7% -25.2% -20.5% -11.8% -16.3% -17.2% -20.4%

Housing still subtracting quite a bit, has to taper off as it bottoms albeit at very low levels.

1Q 4Q 3Q 2Q 1Q 4Q 3Q 2008 2007 2007 2007 2007 2006 2006 Exports 5.5% 6.5% 19.1% 7.5% 1.1% 14.3% 5.7% Goods 5.2% 3.9% 26.2% 6.6% 0.9% 9.6% 7.4% Services 6.1% 13.2% 4.0% 9.6% 1.6% 26.0% 2.0%

March trade report could revise exports much higher…

Imports 2.5% -1.4% 4.4% -2.7% 3.9% 1.6% 5.4% Goods 2.4% -2.6% 4.8% -2.9% 4.2% -0.6% 6.2% Services 3.5% 5.5% 1.7% -1.7% 2.3% 14.2% 1.3%

and imports lower.

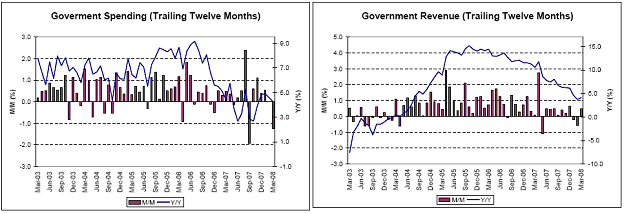

| Government consumption | 2.0% | 2.0% | 3.8% | 4.1% | -0.5% | 3.5% | 0.8% |

| Federal | 4.6% | 0.5% | 7.1% | 6.0% | -6.3% | 7.3% | 0.9% |

| National defense | 6.0% | -0.5% | 10.1% | 8.5% | -10.8% | 16.9% | -1.5% |

| Nondefense | 1.8% | 2.8% | 1.1% | 0.9% | 3.8% | -10.0% | 6.0% |

Federal government spending deferred from 2007 kicking in, especially defense..

State and local 0.5% 2.8% 1.9% 3.0% 3.0% 1.3% 0.7%

As state and local growth slows.

| Change in inventories $B | $1.8 | -$18.3 | $30.6 | $5.8 | $0.1 | $17.4 | $53.9 |

| Net exports $B | -$496 | -$503 | -$533 | -$574 | -$612 | -$597 | -$634 |

| Real final sales | -0.2% | 2.4% | 4.0% | 3.6% | 1.3% | 3.5% | 1.0% |

| Gross domestic purchases | 0.4% | -0.4% | 3.3% | 2.4% | 1.1% | 0.8% | 1.3% |

| Final sales to dom purch | -0.4% | 1.3% | 2.5% | 2.1% | 1.7% | 2.1% | 1.2% |

| Real GDP | 0.6% | 0.6% | 4.9% | 3.8% | 0.6% | 2.1% | 1.1% |

If revised up with March trade numbers, Q4 would have been the bottom.

Personal consumption 0.68% 1.58% 2.01% 1.00% 2.56% 2.68% 1.88% Durables -0.48% 0.15% 0.35% 0.14% 0.67% 0.30% 0.43% Motor Vehicle -0.37% 0.09% -0.17% -0.10% 0.35% 0.00% 0.16% Nondurables -0.27% 0.25% 0.46% -0.10% 0.61% 0.86% 0.64% Services 1.43% 1.18% 1.20% 0.96% 1.28% 1.52% 0.81% Housing 0.23% 0.34% 0.27% 0.29% 0.26% 0.20% 0.18%

Again, services picking up the slack.

Gross pvt dom invest -0.70% -2.40% 0.77% 0.71% -1.36% -2.50% -0.70% Fixed investment -1.50% -0.62% -0.11% 0.49% -0.70% -1.19% -0.80% Nonresidential -0.28% 0.63% 0.96% 1.12% 0.22% -0.15% 0.53% Structures -0.23% 0.41% 0.52% 0.78% 0.20% 0.23% 0.31% Equipment & software -0.05% 0.22% 0.44% 0.34% 0.02% -0.38% 0.21% Info processing 0.23% 0.51% 0.24% 0.36% 0.56% -0.06% 0.24% Computers 0.12% 0.20% 0.08% 0.08% 0.25% 0.03% 0.09% Software 0.13% 0.18% 0.07% 0.16% 0.14% 0.04% 0.05% Residential -1.23% -1.25% -1.08% -0.62% -0.93% -1.04% -1.33%

Soft quarter for investment at least partially due to the widespread recession psychology.

| 1Q | 4Q | 3Q | 2Q | 1Q | 4Q | 3Q | |

| 2008 | 2007 | 2007 | 2007 | 2007 | 2006 | 2006 | |

| Change in inventories | 0.81% | -1.79% | 0.89% | 0.22% | -0.65% | -1.31% | 0.10% |

| Nonfarm | 0.93% | -1.69% | 0.87% | 0.27% | -0.69% | -1.56% | 0.01% |

| Net exports | 0.22% | 1.02% | 1.38% | 1.32% | -0.51% | 1.25% | -0.25% |

| Exports | 0.67% | 0.77% | 2.10% | 0.85% | 0.13% | 1.51% | 0.62% |

| Goods | 0.45% | 0.33% | 1.96% | 0.53% | 0.07% | 0.73% | 0.56% |

| Services | 0.22% | 0.45% | 0.14% | 0.33% | 0.05% | 0.78% | 0.07% |

| Imports | -0.44% | 0.24% | -0.72% | 0.47% | -0.63% | -0.26% | -0.88% |

| Goods | -0.35% | 0.39% | -0.67% | 0.42% | -0.57% | 0.09% | -0.84% |

| Services | -0.09% | -0.15% | -0.05% | 0.05% | -0.06% | -0.35% | -0.03% |

| Govt. consumption | 0.39% | 0.38% | 0.74% | 0.79% | -0.09% | 0.66% | 0.14% |

| Federal | 0.32% | 0.04% | 0.50% | 0.41% | -0.46% | 0.50% | 0.06% |

| National defense | 0.28% | -0.03% | 0.47% | 0.39% | -0.54% | 0.74% | -0.07% |

| Nondefense | 0.04% | 0.06% | 0.03% | 0.02% | 0.08% | -0.24% | 0.14% |

| State and local | 0.07% | 0.34% | 0.24% | 0.37% | 0.36% | 0.16% | 0.08% |

| GDP | 2.6% | 2.4% | 1.0% | 2.6% | 4.2% | 1.7% | 2.4% |

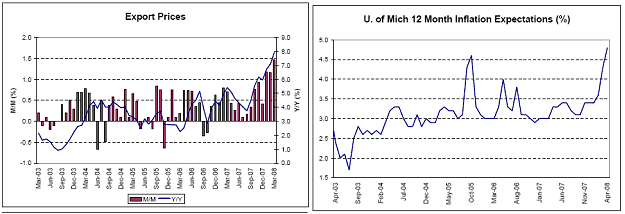

And higher numbers are in the pipeline as per the PPI and CPI reports.

Gross domestic purchases 3.5% 3.7% 1.7% 3.8% 3.8% 0.1% 2.5%

Not bad.

1Q 4Q 3Q 2Q 1Q 4Q 3Q 2008 2007 2007 2007 2007 2006 2006 Price Indexes

GDP 2.6% 2.4% 1.0% 2.6% 4.2% 1.7% 2.4% YOY percent 2.2% 2.6% 2.4% 2.7% 2.9% 2.7% 3.2% Personal consumption 3.5% 3.9% 1.8% 4.3% 3.5% -0.9% 2.6% YOY percent 3.4% 3.4% 2.1% 2.3% 2.3% 1.9% 2.9%

Moving up.

| ex food and energy | 2.2% | 2.5% | 2.0% | 1.4% | 2.4% | 1.9% | 2.3% |

| Real final sales | 2.7% | 2.4% | 1.0% | 2.7% | 4.2% | 1.7% | 2.3% |

Moving up.

Gross domestic purchases 3.5% 3.7% 1.8% 3.8% 3.8% 0.1% 2.5% Unannualized Quarterly Change

Current GDP 0.8% 0.7% 1.5% 1.6% 1.2% 0.9% 0.9% Real GDP 0.1% 0.1% 1.2% 0.9% 0.2% 0.5% 0.3%

Seen a lot worse..

Weakness but no recession and even some improvement on the horizon as government and exports pick up the slack from housing and the financial sector.

Employment softer but still reasonably firm by mainstream standards with unemployment at 5%.

Prices continue firm as Saudis continue to hike crude prices, even as other commodities settle down some.

Hence, I see a narrowing output gap and higher prices on the horizon, and Fed rate hikes at least as aggressive as currently priced by the FF futures market.

[top]

No recession here, and Q1 likely to be revised higher when March trade numbers come out.

Q3 could be 2% depending on the multiplier from the fiscal package, and by Q3 other government spending will be kicking in for the elections and housing is unlikely to be subtracting from GDP. It could even be adding by then.

As suspected, the current weak housing market has been offset by strong exports.

Financial sector losses have nothing to do with GDP unless they somehow reduce aggregate demand.

The prime suspect was the credit channel, but so far the evidence shows only limited damage due to tighter credit conditions, and not the downward spiral feared by the Fed and many other private economists.

On the soft side, but no recession.

The consumer is muddling through as best as can be expected in an export economy.

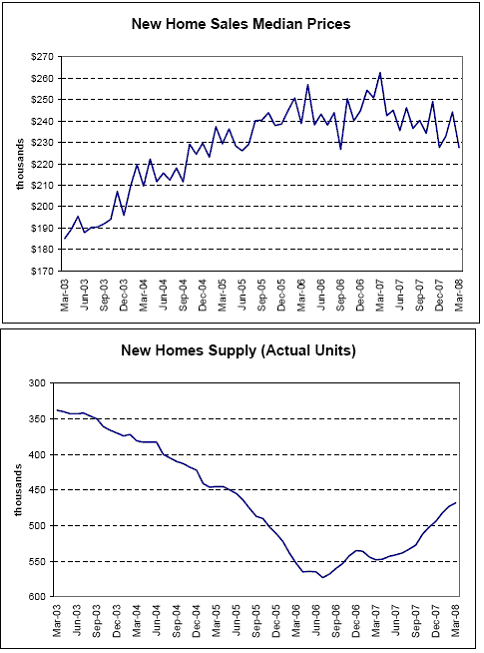

Median prices are soft and may or may not have bottomed, as actual inventories have worked their way down to relatively normal levels for a relatively normal sales pace (which we don’t have yet).

The bulk of the adjustment may have been bottoming around October/November.

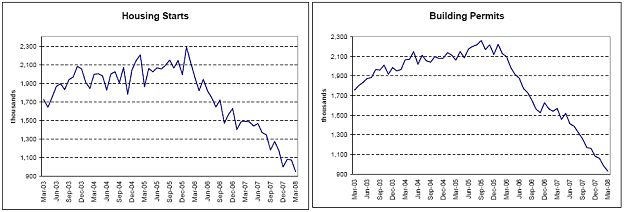

Low starts have reduced supply as builders and buyers remain cautious.

Government spending is roaring back and added nicely to Q1 GDP (March print above has timing issues and wasn’t functionally as low as indicated).

Revenue also holding up, indicating no recession yet.

Every price chart is looking higher, and expectations have elevated, and the Fed keeps cutting rates. Who would’ve thought?

Fisher and Plosser make the mainstream case and are outvoted.

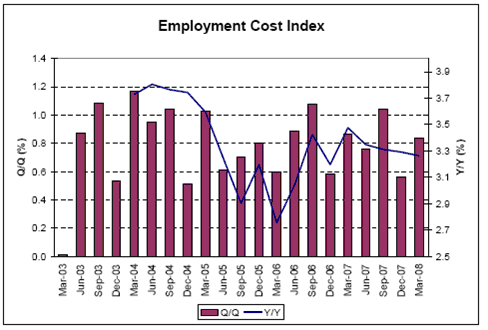

Wages remain ‘well contained’.

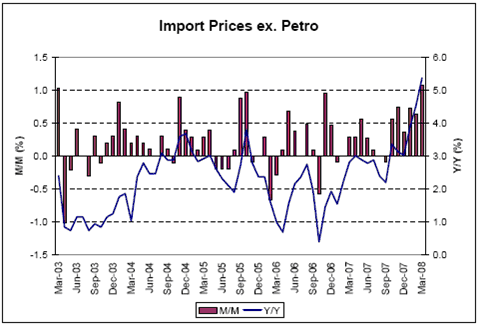

(If you don’t count import prices from China..)

Globalization is now inflationary.

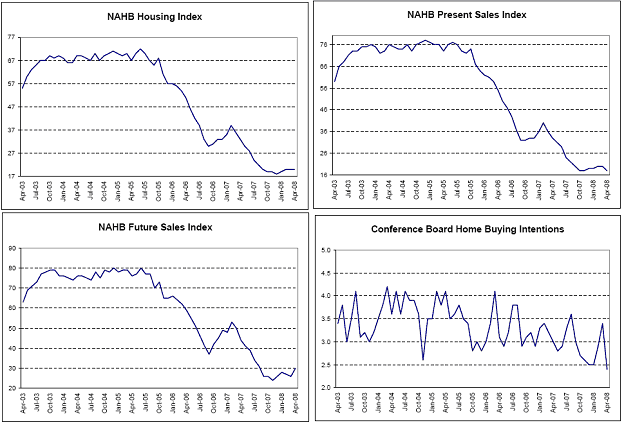

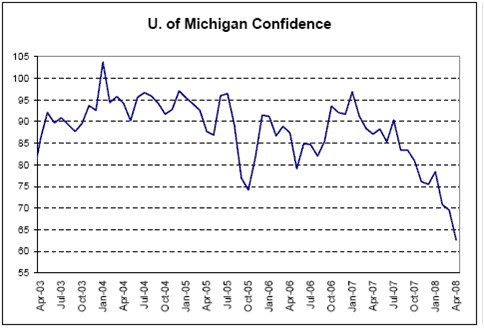

All the confidence surveys look about this weak, and at recession type levels, and about 90% of voters think we are in a recession.

American’s aren’t used to an export economy with declining real terms of trade – a mercantilist concept publicly supported by Bernanke and Paulson.

And they don’t seem to like it.

[top]

| Survey | -75K |

| Actual | -20K |

| Prior | -80K |

| Revised | -81K |

Upside surprise – staying above recession levels, and a lagging indicator.

[top]

| Survey | 5.2% |

| Actual | 5.0% |

| Prior | 5.1% |

| Revised | n/a |

Still trending higher, but not at recession levels, and a lagging indicator as well.

And still very near what the fed considers full employment, putting inflation expectations at risk of elevating for the mainstream.

[top]

| Survey | -35K |

| Actual | -46K |

| Prior | -48K |

| Revised | n/a |

Better than expected, not at recession levels.

[top]

| Survey | 0.3% |

| Actual | 0.1% |

| Prior | 0.3% |

| Revised | n/a |

Lower than expected, indicating wages still well anchored, at least in this report.

[top]

| Survey | 3.6% |

| Actual | 3.4% |

| Prior | 3.6% |

| Revised | n/a |

Coming off some but still moving up at a reasonably pace.

[top]

| Survey | 33.7 |

| Actual | 33.7 |

| Prior | 33.8 |

| Revised | n/a |

[top]

| Survey | 0.2% |

| Actual | 1.4% |

| Prior | -1.3% |

| Revised | -0.9% |

[top]

Upside suprise, same story – domestic weak, export sector strong.

[top]

(an email exchange)

On Fri, May 2, 2008 at 9:44 AM, Jeff wrote:

The Fed announced today that, starting May 5th, it was expanding its cash-loan biweekly auctions for banks (Term Auction Facility or TAF) by 50% to $75 billion each auction. This was the third increase in the four months the program has existed. The Fed also expanded the collateral accepted for the US Treasuries to include other AAA private-label mbs securities,

good, it should be open to any member bank assets- they are all occ legal anyway

in addition to the residential and commercial mbs and agency CMOs that it already accepts. It also increased its currency swap facility with the ECB to $50 billion and with the Swiss National Bank to $12 billion and extended the terms through January 2009.ÂÂÂ

interesting that the ECB needs more dollars. if there is going to be a systemic failure it’s in the eurozone.

On Thu, May 1, 2008 at 7:43 AM, Karim wrote:

Sorry for delayâ€â€Âwas in transit yday.

Recent information indicates that economic activity remains weak. Household and business spending has been subdued and labor markets have softened further. Financial markets remain under considerable stress, and tight credit conditions and the deepening housing contraction are likely to weigh on economic growth over the next few quarters.

Note: Economic activity not weakening further and credit conditions not tightening further, but remain ‘weak’ and ‘tight’, respectively. Housing contraction still deepening and labor market still softening.

So we remain stuck around 0% growth with tight credit conditions and a worsening labor market..

Although readings on core inflation have improved somewhat, energy and other commodity prices have increased, and some indicators of inflation expectations have risen in recent months. The Committee expects inflation to moderate in coming quarters, reflecting a projected leveling-out of energy and other commodity prices and an easing of pressures on resource utilization. Still, uncertainty about the inflation outlook remains high. It will be necessary to continue to monitor inflation developments carefully.

Note: Removed ‘inflation remains elevated’ and uncertainty about inflation has not increased, but ‘remains high’.

Feeling a little better about inflation but way too early to sound all-clear.

The substantial easing of monetary policy to date, combined with ongoing measures to foster market liquidity, should help to promote moderate growth over time and to mitigate risks to economic activity. The Committee will continue to monitor economic and financial developments and will act as needed to promote sustainable economic growth and price stability.

Note: Removed downside risks remain and ‘act in a timely manner’.

Don’t see growth falling much below the -1% to +1% range and will likely not ease at the June meeting.

I agree with former FOMC member Poole who described the statement as ‘hardly a loud and clear signal’ of a pause.

I think the Fed stands ready to ease further if fiscal action (notable in its absence in the statement) and prior eases don’t gain traction over the course of H2.

Agreed with all.

The FOMC continues to ‘trust their models’ and forecast declining inflation.

The economy continues to muddle through with GDP just north of 0, with CPI remaining north of 4% for what is adding up to a substantial period of time.

What the Fed is saying is that the current output gap/’resource utilization level’ is more than adequate to bring down cpi as per their forecasts.

This is what the mainstream would call a very high risk strategy, with the risk being that the cost of bringing down inflation later will be a lot higher than it would have been to bring it down sooner.

| Survey | n/a |

| Actual | 27.4% |

| Prior | 9.4% |

| Revised | n/a |

Seem to be drifting higher.

[top]

| Survey | 0.4% |

| Actual | 0.3% |

| Prior | 0.5% |

| Revised | n/a |

Not the stuff of recessions.

[top]

| Survey | 0.2% |

| Actual | 0.4% |

| Prior | 0.1% |

| Revised | n/a |

Muddling through.

[top]

| Survey | 3.2% |

| Actual | 3.2% |

| Prior | 3.4% |

| Revised | n/a |

Still far too high for comfort for a mainstream economist.

[top]

| Survey | 0.1% |

| Actual | 0.2% |

| Prior | 0.1% |

| Revised | n/a |

I’m anticipation more 0.3%s for the rest of this year.

[top]

| Survey | 2.0% |

| Actual | 2.1% |

| Prior | 2.0% |

| Revised | n/a |

Starting to move back up.

[top]

| Survey | 365K |

| Actual | 380K |

| Prior | 342K |

| Revised | 345K |

No recession yet.

[top]

| Survey | 2950K |

| Actual | 3019K |

| Prior | 2934K |

| Revised | 2945K |

No recession yet.

[top]

| Survey | 48.0 |

| Actual | 48.6 |

| Prior | 48.6 |

| Revised | n/a |

Staying above recession levels.

[top]

| Survey | 83.5 |

| Actual | 84.5 |

| Prior | 83.5 |

| Revised | n/a |

Inflation ripping!

[top]

| Survey | -0.7% |

| Actual | -1.1% |

| Prior | -0.3% |

| Revised | 0.4% |

[top]

| Survey | n/a |

| Actual | -3.4% |

| Prior | -2.2% |

| Revised | n/a |

Still weak.

[top]

| Survey | 15.0M |

| Actual | — |

| Prior | 15.1M |

| Revised | — |

[comments]

[top]

| Survey | 11.4M |

| Actual | – |

| Prior | 11.1M |

| Revised | – |

[comments]

[top]