Might be more early evidence of FICA hike biting.

Skipping the pros and focusing on the cons regarding the economy:

1. 0 rates (including QE) continue to be a highly deflationary bias that require deficits to be that much higher.

2. The FICA hike’s a serious setback that reduces growth from 3 or 4% to 1.5 or 2.5% or less.

3. Corporate cash building, foreign dollar accumulation, pension fund rebuilding, etc. are demand leakages

4. Past expansions were fueled by things we won’t do again- sub prime fraud, tech/y2k bubble, S&L expansion leg, emerging market fx debt fueled bubble, etc.- and that Japan has been careful to avoid.

5. Global austerity, where, in general, everyone of consequence thinks the problem is deficits are too large when in fact they are far too small for current credit conditions.

The January ‘bounce back’ from avoiding the cliff, debt ceiling delay, ideologues angry at the election results, etc. and the head fakes from the accelerated dividends and bonuses in Dec, seasonal issues with claims, the strong euro, some relatively modest China strength, and a few other things, is all fading fast.

For all practical purposes this is about and part of ‘official policy’ to weaken the yen if they do it.

That is, it’s not a reaction to govt policy, it is govt policy.

Japan Pension Funds Bonds Too Many on Abe Plan, Mitani Says

By Anna Kitanaka, Toshiro Hasegawa & Yumi Ikeda

Feb 4 (Bloomberg) — Japans public pension fund, the worlds biggest manager of retirement savings, is considering the first change to its asset balance as a new governments policies could erode the value of $747 billion in local bonds.

Managers of the Government Pension Investment Fund, which oversees about 108 trillion yen ($1.16 trillion) in assets, will begin talks in April about reducing its 67 percent target allocation to domestic bonds, President Takahiro Mitani said in a Feb. 1 interview in Tokyo. The fund may increase holdings in emerging market stocks and start buying alternative assets.

The GPIF, created in 2006, didnt alter the structure of its holdings during the worst global financial crisis in 80 years or in response to the 2011 earthquake and nuclear disaster. Prime Minister Shinzo Abe and the Bank of Japan (8301) have pledged to restore economic growth and spur inflation, which will mean higher interest rates, Mitani said.

If we think about the future and if interest rates go up, then 67 percent in bonds does look harsh, said Mitani, who was appointed in 2010 after serving as an executive director at the Bank of Japan. We will review this soon. We will begin discussions for this in April-to-May. Any changes to our portfolio could begin at the end of the next fiscal year.

GPIF, one of the biggest buyers of Japanese government bonds, held 69.3 trillion yen, or 64 percent of total assets, in domestic debt at the end of September, according to its latest quarterly financial statement. That compares with 12 trillion yen, or 11 percent, in Japanese stocks; 9.6 trillion yen, or 9 percent, in foreign bonds; and 12.6 trillion yen, or 12 percent, in overseas stocks.

Relative Yield

The fund, which took over management of government employee retirement savings when it was set up, returned to profit in the three months ended Dec. 31 from a 1.4 percent loss in the first six months of the fiscal year, Mitani said. He declined to be more specific. It needs to raise about 6.4 trillion yen this fiscal year through March 31 to meet payments.

The yield on Japans 10-year government bond climbed 3.5 basis points to 0.8 percent as of 4:35 p.m. in Tokyo today. By comparison, the projected dividend yield for the Topix Index (TPX), the countrys broadest measure of equity performance, is 2.05 percent. The Topix added 1.4 percent today.

Japans bonds handed investors a 1.8 percent return in 2012, according to a Bank of America Merrill Lynch Index, compared with the 18 percent surge in the Topix.

Even as shares jumped amid optimism surrounding Abes stimulus plans, benchmark Japanese government bond yields have remained below their five-year average yield of 1.18 percent. Benchmark 10-year yields are the lowest in the world after Switzerland and are less than half the level in the U.S.

Rates Outlook

JGBs were how we made money over the past 10 years, Mitani said. The BOJ said that they are increasing buying bonds, but theyre also putting power into lowering interest rates. If the economy gets better, then long-term interest rates like a 10-year yield at less than 1 percent are unlikely.

The five-year JGB rate touched a record low 0.14 percent last month amid speculation the Bank of Japan will expand bond purchases as part of the monetary easing advocated by Abe.

The comments by Mitani show the pension manager needs to consider higher-risk, higher-yield assets to help fund retirements of the worlds oldest population. About 26 percent of the nation is older than 65, according to data compiled by Bloomberg.

Under Mitanis leadership, the GPIF began buying emerging- market assets in September 2011 and started purchasing shares in countries included in the MSCI Emerging Market Index (MXEF) last year. Mitani said in July 2012 that the fund was selling JGBs to pay for peoples entitlements and might consider alternative investments as it seeks better returns.

100 Years

We havent changed the core portfolio for a long time so it was thought that its about time to review this, Mitani said. The portfolio was based on a prerequisite of things such as long-term interest rates at 3 percent on average for the next 100 years. Whether this is good will be a possible point of discussion.

Holdings have been broadly unchanged since inception, when the fund was formulated with an outlook for consumer prices to rise 1 percent annually. Instead, the nations headline CPI has fallen an average 0.1 percent each month since the start of 2006, according to data compiled by Bloomberg.

The Bank of Japan last month doubled its inflation target to 2 percent, a level last seen in 1997, when a sales tax was increased, with no sustained price gains of that magnitude in two decades. Falling prices reduce incentives to borrow and invest in new business projects, erode tax receipts and increase the attractiveness of saving in cash rather than spending or putting money into stocks or bonds.

Topix Surge

GPIF is the biggest pension fund in the world by assets, followed by Norways government pension fund, according to the Towers Watson Global 300 survey in August.

Japans Topix Index surged 30 percent from Nov. 14, when elections were announced, through Feb. 1 on optimism the Liberal Democratic Party will lead the economy out of recession and end deflation. The yen weakened almost 14 percent against the dollar in that time, and touched its lowest level since May 2010 last week.

Even after 12 straight weekly advances, the longest streak in 40 years, the Topix is still 67 percent below its December 1989 record high.

Relative Value

The measure trades for 1.1 times the value of net assets. That compares with 2.3 times for the S&P 500, 1.6 times for the Hang Seng Index and 1.9 times for the MSCI World Index. A reading above one means investors are paying more for a company than the value of its net assets.

The yen dropped 11 percent last year versus the dollar, the most since 2005. A weaker yen increases the value of exports and typically raises import costs, boosting consumer prices.

Japanese stocks do not look expensive, Mitani said. Were still in the middle of a rising stocks, weakening yen trend. It will continue for a while.

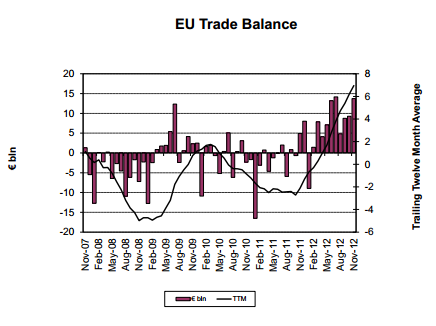

As previously discussed, the euro looks to keep going up until the trade surplus reverses. Problem is the strong euro doesn’t necessarily cause the trade surplus to reverse, at least not in the short term. But it does tend to work against earnings and growth. And there’s nothing the ECB can do about it, short of buying dollars via direct intervention, which would be counter to their core ideology, as building dollar reserves would give the appearance of the dollar backing the euro. The solvency issue has now been behind them for quite a while, and still no sign of any ‘official’ recognition that deficits need to be higher to restore output and employment.

And, also as previously discussed, while the future was looking up for the US a few months ago, the caveat of ‘austerity’ has come into play with the year end FICA and other tax hikes, and now the odds are the sequesters are allowed to come into play March 1 as well. Note this has been Japan’s policy as well- fiscal tightening at the first sign of any hope for expansion. Fed policy also looks to remain restrictive as blatantly evidenced by the recent turn over of some $90 billion of ‘profits’ to the Treasury that otherwise would have been earned by the economy.

The headline ‘deficit doves’ pushing for larger deficits with their ‘out of paradigm’ arguments are also serving to continue to support austerity. They have been arguing that the low interest rates are a signal from the markets (as if they know anything about markets) indicating the economy wants the govt to sell more bonds. This is in response to the hawk’s equally out of paradigm argument that financing deficits will eventually drive up interest rates. So now that interest rates have started going higher, the dove’s case is for higher deficits is pretty much gone, removing the resistance to ‘getting our fiscal house in order’ just as the sequester date is approaching. Whether it’s gross ignorance or intellectual dishonesty doesn’t matter all that much at this point- it’s happening. At the same time oil and gasoline prices have been creeping up, taking a few more shekels away from consumers. January and it’s strong equity inflows/allocations and releases of December’s stats ends tomorrow. February’s releases of Jan stats will bring more post FICA hike clarity.

Japan’s weak yen, pro inflation policy seems to have been all talk with only a modest fiscal expansion to do the heavy lifting. Changing targets does nothing, nor does the BOJ have any tools that do the trick as evidenced now by two decades of using all those tools to the max. And while I’ve been saying all the while that 0 rates, QE, and all that are deflationary biases that make the yen stronger, there is no sign of that understanding even being considered by policy makers, so expect more of same. What has been happening to weaken the yen is a quasi govt policy of the large pension funds and insurance companies buying euro and dollar denominated bonds, which shifts their portfolio compositions from yen to euros and dollars, thereby acting to weaken the yen. I have no idea now long this will continue, but if history is any guide, it could go on for a considerable period of time. Yes, it adds substantial fx risk to those institutions, but that kind of thing has never gotten in the way before. And should it all blow up some day, look for the govt to simply write the check and move on.

Not conclusive but a bit of evidence the FICA hike is beginning to take a toll.

From Gail:

The Conference Boards Consumer Confidence Index decreased to 58.6, the weakest since November 2011, from a revised 66.7 in December

January 29 — Says Lynn Franco, Director of Economic Indicators at The Conference Board: Consumer Confidence posted another sharp decline in January, erasing all of the gains made through 2012. Consumers are more pessimistic about the economic outlook and, in particular, their financial situation. The increase in the payroll tax has undoubtedly dampened consumers spirits and it may take a while for confidence to rebound and consumers to recover from their initial paycheck shock. Consumers appraisal of current conditions deteriorated in January. Those claiming business conditions are good declined to 16.7 percent from 17.2 percent, while those stating business conditions are bad increased to 27.4 percent from 26.3 percent. Consumers assessment of the labor market has also grown more negative. Those saying jobs are plentiful declined to 8.6 percent from 10.8 percent, while those claiming jobs are hard to get increased to 37.7 percent from 36.1 percent.

Debt approaching 1 quadrillion, and the highest as a % of GDP anywhere I know of, and still no bond vigilantes in sight!

Who would have thought???

Not to mention decades of 0 rates, massive QE, and in general the BOJ trying as hard as it can to inflate.

Maybe it’s not all that easy for a CB to cause inflation???

Anyway, net fiscal will add a bit to GDP, but nothing serious, and the hawkish rhetoric doesn’t seem to have changed any.

And note the cuts in welfare ‘paying for’ the increases in defense and infrastructure.

Of the Y92.6 trillion yen in spending, Y43.1 trillion will be financed with tax revenues and Y42.9 trillion with issuance of new bonds, adding to Japan’s massive public sector debt that already totals nearly Y1 quadrillion.

The FY2013 budget does show clear differences from those of the previous DPJ administration, with a clear shift away from social welfare toward defense and infrastructure programs.

It calls for a reduction of Y67 billion in welfare benefits over the next three years, an increase of Y712 billion, or 15.6% in public works programs and a Y35 billion, or 0.8% increase in spending for the Self-Defense Forces.

“Adequate amounts have been provided to ensure the safety of public infrastructure and to address public concerns about national defense,” Mr. Aso said.

The LDP’s call for aggressive public works spending got better reception after the collapse of an expressway tunnel in December that killed nine people. Simmering tensions with China have also increased support for spending programs to improve security of Japanese territory.

In a policy address Monday, Mr. Abe vowed to erase fiscal deficits in the medium-to-long term, but stopped short of saying when, leaving the task to his economic advisory panel.

Sayuri Kawamura, a Japan Research Institute economist, is worried that not enough attention has been given to the risk of fiscal implosion.

“As debt piles up, the cost of servicing that debt also goes up, eating deeper into tax revenue, and leaving less and less for policy programs. The government hasn’t explained how they are going to deal with this challenge,” Ms. Kawamura said.

Agreed with Karim. So far no signs of actual damage from the FICA hike. Even bonds now indicating same.

The problem is personal- it’s hard for me to fathom FICA going up that much without some meaningful damage to GDP.

So I remain on the sidelines pending more Jan data.

ICSC 3% Retail Sales Growth Maintained for January, Fiscal Year (ICSC) January sales growth is tracking above ICSC’s 3% estimate for the month, even with a slight moderation of yoy sales growth as the month has progressed. All Super Bowl shopping will fall in January this year, so sales should gain momentum as the month closes. January U.S. store traffic growth continued to slow in the third week of the month, rising 3.1%, as stores transition from post-holiday clearance to more everyday merchandise. Traffic at enclosed malls remained unchanged yoy and apparel stores declined by low-single digits for the first time since the lull in early December. The 12% month-to-date traffic gain stems from large increases in early January. U.S. same store sales excluding Wal-Mart rose 2.7 percent in Dec. from a year earlier.

ICSC index drops every January but this year higher than last, as Karim indicated.

January auto sales seen continuing 2012’s strong pace (Reuters) Auto sales in January are expected to continue the torrid pace set at the end of last year, with sales rising as much as 15 percent. J.D. Power and LMC Automotive, in a joint press release, said they expect U.S. retail sales in January to reach the highest rate in five years. Including fleet sales to commercial customers, the research firms expect an annual sales rate for the month of 15 million vehicles. That would follow the strong showings in November and December, when the rate topped 15 million. “The year is off to a fast start, which bodes well for the remainder of 2013,” J.D. Power Senior Vice President John Humphrey said.

Strongest manufacturing expansion since March 2011 (Markit) The Markit Flash U.S. Manufacturing PMI rose to 56.1 in January from 54.0 in December. The output index rose to 57.2 from 54.5, the new orders index rose to 57.7 from 54.7, the new export orders index fell to 51.3 from 52.6, and the backlog of orders index fell to 49.5 from 50.3. Manufacturers reported a further rise in production levels during January. Companies attributed faster output growth to an increase in new orders. Overall incoming new work rose at the fastest rate since May 2010, largely reflecting higher demand in the domestic market. New export orders continued to increase, up for the third month running, albeit at a slower rate than in December. Asia was mentioned by survey respondents as a key source of new business.