Inventories looking excessive:

Wholesale Trade

Highlights

The economy may be solid right now but inventories at the wholesale level look heavy, rising 0.1 percent in December vs a noticeable 0.4 percent decline in sales at the wholesale level. The mismatch drives up the stock-to-sales ratio by 1 tenth to 1.22 which is the heaviest reading since way back in the troubled days of late 2009. This ratio was at 1.17 through the middle of last year but has since been moving higher.

December’s unwanted wholesale build is centered in the non-durable component where sales, in contrast to durable goods which rose 1.1 percent, fell 1.7 percent in the month. Here the culprit is petroleum where sales, reflecting both price effects and lower demand, fell 13.7 percent in the month. And the supply overhang, based on weekly petroleum inventory data, has continued to build into the new year. Showing a big draw in the month are lumber and electrical goods, two products that may be signaling rising demand out of the construction sector.

The nation’s inventories have been moving higher but the imbalance has been centered in the wholesale sector, though inventories at the factory level are showing a little pressure. Watch Thursday for the business inventories inventory report which will round out December’s data with data on the retail sector.

Wholesale inventories up 0.1% in December, versus expectations for 0.2% gain

Feb 10 (Reuters) — U.S. wholesale inventories barely rose in December, the latest suggestion that fourth-quarter growth could be revised lower.

The Commerce Department said on Tuesday wholesale inventories edged up 0.1 percent as lower crude oil prices weighed on the value of petroleum stocks. Stocks at wholesalers had increased by an unrevised 0.8 percent in November.

Economists polled by Reuters had forecast wholesale inventories rising 0.2 percent in December.

Inventories are a key component of gross domestic product changes. The component that goes into the calculation of GDP – wholesale stocks excluding autos—nudged up 0.1 percent.

The report, together with last week’s data showing a 0.3 percent fall in manufacturing inventories in December, suggested the boost to GDP growth from restocking in the fourth quarter was probably not as large as initially thought.

The government estimated last month that inventories added 0.8 percentage point to the economy’s annualized 2.6 percent growth pace in the fourth quarter.

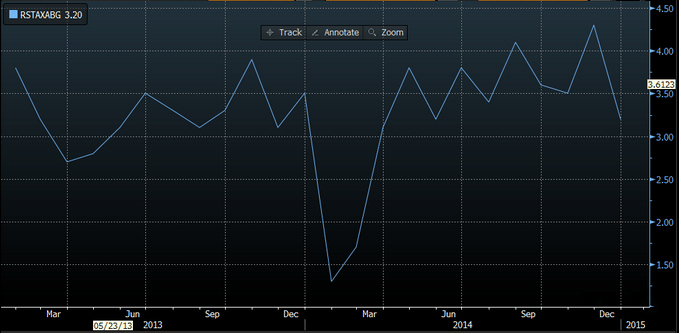

Sales at wholesalers fell 0.4 percent in December after a similar decline in November. At December’s sales pace it would take 1.22 months to clear shelves, down from 1.21 months in November.

The last thing Greece needs are collaborators. First Italy and now the BOE:

BOE’s Carney Applauds ECB Policy (WSJ) “There are many reasons why the ECB’s actions are important, one of them is it shows the ECB has the full tool kit to support the underlying economy as necessary…the ECB is taking bold action,” BOE Governor Mark Carney said. While the ECB move is constructive, it won’t deliver medium-term prosperity to the eurozone economy, Mr. Carney said.

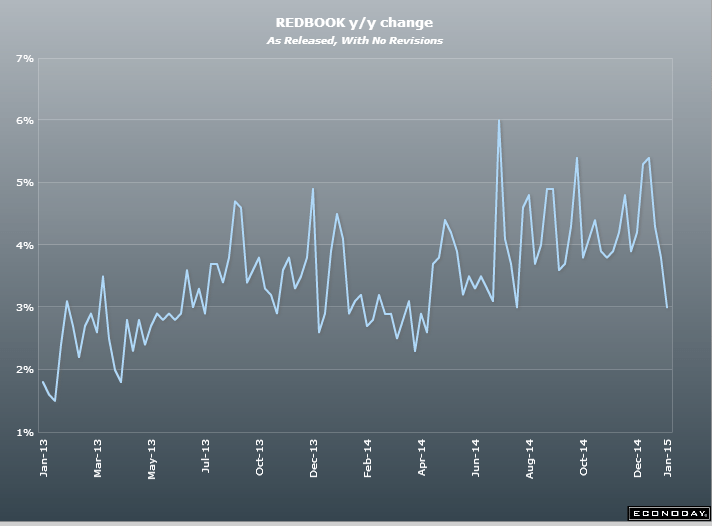

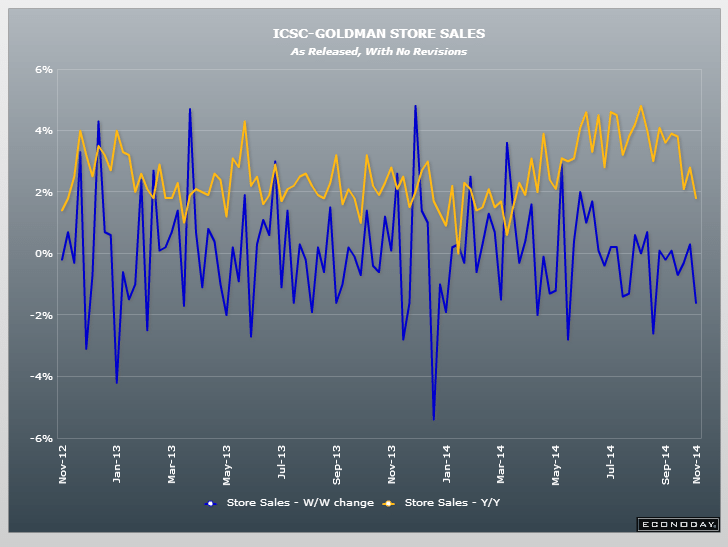

This isn’t supposed to be declining with the presumed boost to the consumer from low oil prices:

Redbook

Highlights

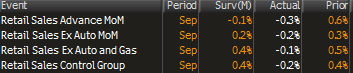

Retail sales slowed substantially in the February 7 week, to a year-on-year plus 2.1 percent from 3.8 percent in the prior week. The 2.1 percent rate is very low which the report attributes to the Super Bowl which diverted consumer attention. Redbook sees sales picking up in the next report due to Valentine’s Day. The government’s retail sales report this Thursday is the week’s big event on the calendar and is expected to show a bounce-back rise in core sales for January (ex-auto ex-gas).

JOLTS

Highlights

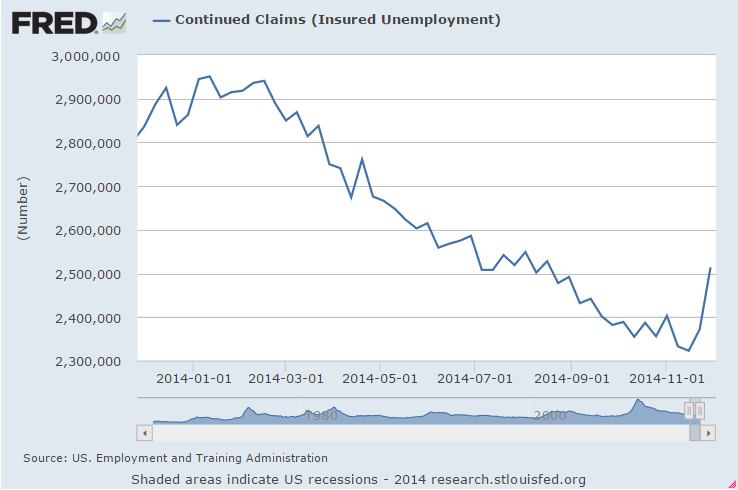

There were 5.028 million job openings on the last business day of December, slightly improved from 4.847 million in November. Hires (5.148 million) and separations (4.886 million) were little changed in December. Within separations, the quits rate (1.9 percent) and the layoffs and discharges rate (1.2 percent) were unchanged. This release includes estimates of the number and rate of job openings, hires, and separations for the nonfarm sector by industry and by four geographic regions.

There were 5.148 million hires in December, slightly higher than November’s 5.054 million. This was the highest level of hires since November 2007. The hires rate in December was 3.7 percent. The number of hires was little changed for total private and government. Hires increased over the month in construction.

Total separations include quits, layoffs and discharges, and other separations. Total separations are referred to as turnover. Quits are generally voluntary separations initiated by the employee. Therefore,

the quits rate can serve as a measure of workers’ willingness or ability to leave jobs. Layoffs and discharges are involuntary separations initiated by the employer. Other separations include separations

due to retirement, death, and disability, as well as transfers to other locations of the same firm.

There were 4.9 million total separations in December, little changed from November. This was the highest level of separations since October 2008. The separations rate was 3.5 percent. The number of total separations was little changed for total private and government.

There were 2.717 million quits in December, little changed from November. The quits rate in December was 1.9 percent. The number of quits was little changed for total private and government. Quits increased in construction and durable goods manufacturing. The number of quits was little changed in all four regions.

Overall, the JOLTS numbers portray a slowly improving jobs market with job openings rising along with hires.