By Edward Harrison

April 30 — Regular readers know that, while I have a little of what Marshall Auerback calls deficit terrorism in my DNA, I fully support fiscal stimulus as a means to arrest a deep downturn.

Yes, though I like to say ‘removing fiscal drag’ but same thing.

The horrendous Keynesian nightmare

My move into Keynesian mode came in December 2008 with Confessions of an Austrian economist. In fact, I have argued the ObamaAdministration needed to use more stimulus in early 2009, not less (see January 2009’s Obama’s stimulus bill is a tough sell so far as an example).

Yes, needed to remove more drag.

As early as February 2009, I argued that Obama took a middle road on stimulus and taxes that leads nowhere which would discredit stimulus as a policy tool. And that is indeed what has happened.

Agreed. Which would be ok if they recognized it and opted for further adjustment.

Now, of course many of you don’t feel that way because you share my visceral disaffection for deficit spending.

Given there is a ‘right size’ govt based on public purpose of the public sector, and not revenues, the fiscal adjustments fall on the tax side.

So I feel the visceral disaffection for the over taxation that comes from a too small deficit.

But I laid out where the US economy is headed without stimulus in “The recession is over but the depression has just begun” six months ago. And right now we are heading exactly where I said we would. Witness my last post on the economy “US GDP growth rate is unsustainable; recovery will fade”

Anyway, the point is that the US economy will not be able to sustain recovery for long without stimulus. The likely result of withdrawing stimulus is a recession that is deeper than the last one aka a major depression.

Yes, it sure looks like the shortfall in aggregate demand calls for an immediate fiscal adjustment.

Deficits as far as the eye can see

But right now, a lot of talking heads are trying to bamboozle people with tales of woe about hyperinflation and sovereign bankruptcy in the US to support specific claims about what deficit spending can and can’t do. Deficit hawks, in particular, are on the warpath – a completely predictable outcome since I anticipated it just as Obama was elected in November 2008 (see Beware of deficit hawks).

Agreed!

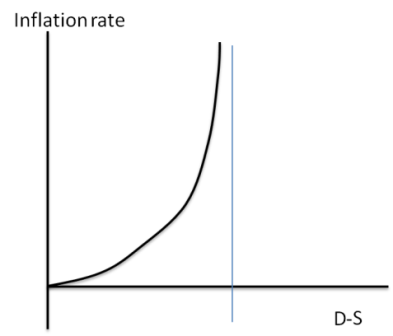

Of course the US deficits are too large. Come on: 10% deficits as far as the eye can see are unsustainable over the long-term.

I don’t see that. Especially if govt spending isn’t ‘forced’ into the economy which would be evidenced by a closing of the output gap.

Until the output gap closes, deficits are simply offsetting non govt ‘savings desires’ for dollar financial assets.

That is, deficits add directly to non gov savings and until those savings desires are saturated govt isn’t ‘forcing’ financial assets into the economy.

The key word, however, is long-term. However, no one seems to understand the difference between short-term and long-term and the debate has become an ideological free-for-all.

It would help if they realized there is not necessarily a long term problem either.

Earlier this month, I told you I am throwing in the towel on policy makers because it’s clear that Obama has been captured by the deficit hawks and we are headed for a painful recession within the next two years (maybe even as soon as next year).

Agreed!

Policy is exogenous and deficits are endogenous

So let’s stop talking about policy as if we are going to change anything. I started moving away from stimulus happy talk to focus on malinvestment in December of last year.

The policy debates aren’t working because the actual mechanics of a fiat monetary system are being obscured by ideological political debates. So, what I want to do is lay the foundations of modern money with you so we can strip away the politics and ideology from the economics.

The goal is to demonstrate that fiscal deficits and surpluses are endogenous to our economic system and depend on exogenous policy decisions which are inherently political and ideological.

Let me give you an example. What if we allowed the US economy to proceed without making one economic policy decision for the next two years? What would happen? The answer is that the government would have a fiscal deficit of X billions of dollars exactly matched by X billions of surpluses in the non-government sector (remember the sectors must balance). The deficit outcome is endogenous. It is a function of the inputs i.e. of the private sectors desire to save and the government’s spending decisions.

Agreed, as above.

On the other hand, government economic policy decisions are exogenous. They are input variables which alter outcomes. This is an important point because if we know how the monetary system works, then we can get a much better handle on how different policy decisions actually affect deficits and surpluses. And remember, policy decisions are almost entirely political. That is they are driven by ideological positions.

Agreed.

So, if I say to you that I am against government spending and it must be cut, this creates a specific outcome path. On the other hand, if I say I am pro-stimulus, this too creates a specific outcome.

Modern Money

Here’s how I am going to go about this one:

I went to a conference on Modern Monetary Theory (MMT) on Wednesday. Over the next few weeks, I will present some ideas from the Modern Money people (Randy Wray, Marshall Auerback, Bill Mitchell, etc). I’ll start the post titles with “MMT:….”

Yes, good to see you there!

I will take a somewhat antagonistic approach because I think that’s probably going to the best way to introduce this to people who have a more libertarian bent like myself.

Now, my bio says:

From an ideological perspective, Edward calls himself a libertarian realist: a firm believer in the primacy of markets over a statist approach. but not in an ideological way. Often government intervention and oversight is not just wanted but warranted.

What that essentially means is that when I think about government, I view it with suspicion and my inclination is to seek to limit its size and scope.

Yes, there is a right sized govt that serves public purpose that varies from person to person. It’s a political decision.

That means I have an innate disaffection for big government,

Ok, that’s a legitimate political position shared by tens of millions, and maybe a majority.

deficit spending,

That’s the size of additions to net non govt savings which can only come from fiscal balance. The political decision here is the outcome (growth, employment, etc.) Of the level of savings govt allows through its policy.

money printing,

That’s a gold standard term relating to the ratio of paper claims on the gold reserves to the actual gold reserves. It’s no longer applicable as originally defined, so needs to be redefined or otherwise specified.

For example, the fed buying securities is an exchange of financial assets, both of which generally fall under some monetary aggregate, at which level that aggregate remains unchanged.

etc. – but not in an ideological way. It all depends on the circumstances. (For instance, see “A brief philosophical argument about the role of government” and “A few thoughts about the limitations of government” which outline my ideological positioning).

So, my goal in this is to separate the policy and the politics from the mechanics of how our fiat money system operates. That way it will be clear what is actually happening in our monetary system right now and what is pure political posturing. You will also then probably see a lot of congruence between how I see the economic mechanics and how Marshall sees them. The difference, of course, is ideology.

The way I intend to position this is that Modern Money Theory economists are really the True Modern Money Operations economists because they present the true mechanics of modern fiat money operation, which I will show you.

Now, policy decisions are largely political, exogenous decisions about which informed decision-makers can disagree. However, if we aren’t at least informed about the mechanics of how modern money works, it is very difficult to have an intelligent debate about deficits, social security, fiscal stimulus or anything else for that matter.

I know that I have learned a lot from what the likes of Randy Wray and Bill Mitchell have said (remember, I studied economics in a time heavily influenced by the prevailing economic orthodoxy). I don’t ‘buy into’ a lot of what they propose on policy, but on modern money they have it right.

Agreed, though i probably support most of their policies as well. But not always.

The purpose is to present the underpinnings where we can all agree and separate it from the ideological piece. My ideological foil in this will be Marshall Auerback. Afterward, I hope we can have a framework from which to talk about the political piece.

I hope you enjoy the debate and a presentation of the ideas.

Looking forward to it, thanks!!!

Best,

Warren