So does the US have a strong dollar policy, a weak dollar policy, or an ‘unchanged’ dollar policy?

In any case, President Obama and Congress still fail to recognize that imports are real benefits and exports real costs. And that net imports mean taxes can be lower and/or spending higher to sustain full employment levels of demand.

So what would you rather have?

1. A strong dollar, rising net imports, and lower taxes, or

2. A weak dollar, falling net imports, and higher taxes?

How hard is this???

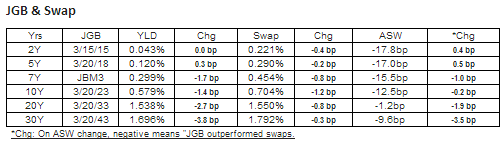

As for Japan, the BOJ hasn’t actually done anything to weaken the yen. Nor has fiscal policy, at least yet, though if the announced deficit hike goes through it could be a modestly weakening influence. The trade flows going into deficit from surplus have hurt the yen, as gas and oil replaced the nukes that were shut down, though they are in the process of relighting them. And portfolio shifting has probably weakened the yen the most, with life insurance companies, pensions, etc. reportedly adding risk to their portfolios by shifting from yen assets to dollar and euro assets. Yes, this is a ‘one time’ adjustment, but it can be sizable and take years, or it could have already run its course. I personally have no way of knowing, but no doubt ‘insiders’ are fully aware of how this will play out.

Furthermore, the US is going the other way with tax hikes and spending cuts a firming influence on the dollar, which is at least part of the yen/dollar weakness.

Too many cross currents for me to bet on one way or another. If you have to trade it go by the charts and don’t watch the news…

U.S. Warns Japan on Yen

By Thomas Catan and Ian Talley

April 12 (WSJ) — The Obama administration used new and pointed language to warn Japan not to hold down the value of its currency to gain a competitive advantage in world markets, as the new government in Tokyo pursues aggressive policies aimed at recharging growth.

In its semiannual report on global exchange rates, the U.S. Treasury on Friday also criticized China for resuming “large-scale” market interventions to hold down the value of its currency, calling it a troubling development. The U.S. stopped short of naming China a currency manipulator, avoiding a designation that could disrupt relations between the world powers.

The Chinese Embassy didn’t immediately respond to a request for comment. A Japanese government official reached early Saturday in Tokyo declined to comment directly on the Treasury report, but said, “We will continue to abide by” recent commitments by global financial policy makers to avoid intentional currency devaluation”as we have done until now.”

The Treasury report appears to be part of a broader strategy by the Obama administration in response to a sharp shift in economic policy in Japan under new Prime Minister Shinzo Abe.

Hours before the currency warning, the White House said it had accepted Mr. Abe’s request to join negotiations to create an ambitious pan-Pacific free trade zone, despite objections from the American auto industry and other domestic sectors worried about new competition from Japan. The U.S. government is welcoming economic reforms in Japan while trying to discourage Tokyo from reverting to prior tactics of trade manipulation.

The Bank of Japan kicked off the latest drop in the yen by shocking markets last week by announcing plans for a massive increase in money supply, pledging a sharp increase in purchases of government bonds and other assets. The dollar has risen nearly 7% against the yen since then, and is up 15% since Mr. Abe came into power on Dec. 26.

Policy makers in Japan sensitive to currency complaints and warnings have repeatedly insisted in recent days that the yen’s sharp fall has merely been a byproduct of its stimulus policies, not a goal.

“We have no intention to conduct monetary policy targeting the exchange rate,” Haruhiko Kuroda, the new Bank of Japan governor whose policies have helped push down the yen, said in a Tokyo speech Friday. The BOJ’s policies, he added, were aimed at pulling Japan out of its long slump and that “achieving this goal will eventually provide the global economy with favorable effects.”

Amid sluggish global growth, governments face the temptation to lower the value of their currencies to juice exports. Those pressures are aggravated as central banks in the U.S., Europe and Japan seek to spur their economies by pushing cash into the systempolicies that have the effect of weakening their currencies. Seeking higher returns, investors are putting their money into emerging markets, putting upward pressure on those countries’ currencies and making their exports more expensive abroad.

The U.S. said it would “closely monitor” Japan’s economic policies to ensure they are aimed at boosting growth, not weakening the value of the currency. The yen is now hovering near a four-year low against the dollar, in response to Mr. Abe’s policies.

“We will continue to press Japanto refrain from competitive devaluation and targeting its exchange rate for competitive purposes,” the Treasury report said.

The yen quickly strengthened following the report, pulling the dollar to as low as 98.08, its lowest level this week, in a thin Friday afternoon market. The yen later gave back some of those gains, as investors came to see the comments less as criticism than as a statement of fact.

American officials have been walking a tightrope in recent months. While worried about a deliberate currency devaluation, they have also tried to encourage Japan’s attempts to jump-start growth, after years of frustration in Washington that Tokyo wasn’t doing enough to fix its economy.

“The wording does make it clear that the U.S. Treasury is watching extremely closely” to ensure that Japan lives up to promises not to purposely weaken its currency, said Alan Ruskin, a currency strategist at Deutsche Bank in New York. But, he added, “the report does not infer that Japan is breaking any agreement.”

The Treasury report, required by Congress and closely followed by markets, highlighted the need for more exchange-rate flexibility in many Asian countries, most notably China.

The Treasury used tougher-than-usual language on China, saying Beijing’s “recent resumption of intervention on a large scale is troubling.” While it noted that China had allowed the yuan to appreciate by about 10% against the dollar since June 2010or 16% including inflationthe report said the Chinese currency remained significantly undervalued and “further appreciation” was warranted.

The Treasury in recent years under both Republican and Democratic administrations has declined to formally label China as a currency manipulator, with officials suggesting publicly and privately that such a step would hurt efforts to encourage Beijing to let the yuan rise.

Still, the question of China’s currency has become shorthand in Washington for the broader debate over the economic relationship between the two countries. It was a frequent topic on the campaign trail for both President Barack Obama and GOP challenger Mitt Romney last year, as Mr. Romney pledged that if elected, he would label China a currency manipulator.

On Friday, some U.S. manufacturers criticized the Obama administration for its reluctance to call China a currency manipulator. “The Treasury Department’s latest refusal to label China a currency manipulator once again demonstrates President Obama’s deep-seated indifference to a major, ongoing threat to American manufacturing’s competitiveness, and to the U.S. economy’s return to genuine health,” said the U.S. Business and Industry Council, an industry lobby group.

The Treasury report also took South Korea to task for seeking to keep a lid on the won as foreign investors flood the economy with cash. “Korean authorities should limit foreign-exchange intervention to the exceptional circumstances of disorderly market conditions,” and capital controls should only be used to prevent financial instability, not reduce upward pressure on the exchange rate, Treasury said.