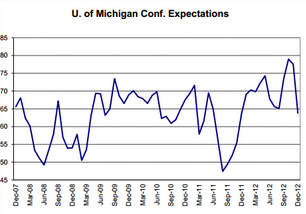

Very informative set of charts, particularly in regard to fiscal drag

Category Archives: GDP

the macro cons

Skipping the pros and focusing on the cons regarding the economy:

1. 0 rates (including QE) continue to be a highly deflationary bias that require deficits to be that much higher.

2. The FICA hike’s a serious setback that reduces growth from 3 or 4% to 1.5 or 2.5% or less.

3. Corporate cash building, foreign dollar accumulation, pension fund rebuilding, etc. are demand leakages

4. Past expansions were fueled by things we won’t do again- sub prime fraud, tech/y2k bubble, S&L expansion leg, emerging market fx debt fueled bubble, etc.- and that Japan has been careful to avoid.

5. Global austerity, where, in general, everyone of consequence thinks the problem is deficits are too large when in fact they are far too small for current credit conditions.

The January ‘bounce back’ from avoiding the cliff, debt ceiling delay, ideologues angry at the election results, etc. and the head fakes from the accelerated dividends and bonuses in Dec, seasonal issues with claims, the strong euro, some relatively modest China strength, and a few other things, is all fading fast.

Friday update

So just like Japan, as soon as the economy starts doing a bit better we hike taxes. Still too early to say how the FICA hike will impact sales and profits, but it will. And spending cuts are on the way, though they may be delayed.

Not to forget the debt ceiling thing about to be kicked 3 months down the road as it stands guard to ensure ‘meaningful’ spending cuts.

Oil firm, but can still go either way. WTI converging to Brent indicates the seaway pipeline capacity increase may be enough to drain the surplus at pad 2, bringing wti up to brent, but too soon to tell for sure. And looks like the demand for saudi crude is dropping some, but not enough to dislodge them from being

swing producer/price setter.

Looks to me like the whole world is becoming ‘more competitive’ so it all cancels out. Bad for people, ok for stocks, with profits running at record highs as a % of GDP. Meaning the federal deficit has to be that much higher, all else equal, to fill the output gap.

The yen keeps going down. Looking more and more to me it’s off the radar screen intervention by the likes of insurance co’s, pension funds, and other quasi govt agencies got the note to buy fx denominated bonds in size. Not sure how far they will take it, but they have a serious herd instinct that has formed serious multi year bubbles in the past.

Europe? They fixed the solvency issue, sort of, and now just have the economy thing to deal with. Problem is the ECB grants solvency only with conditionality. Good luck to them.

Growth Impact from Yesterday’s Deal

Karim writes:

The straight Keynsian impact (i.e., assume multiplier of 1) of the measures announced yesterday work out to a 1.25% drag on GDP, mostly felt in the first few months of the year. This reflects the payroll tax rise (about 0.7%), the rise in taxes and tighter rules on deductions for higher incomes (about 0.4%) and Obamacare fees (about .05%).

What remains unknown and could remain a drag just based on uncertainty effects are the 2mth delay in deciding on sequestration cuts (which may or may not happen), and obviously the debt ceiling. Both of these deadlines are likely to occur within 2weeks of each other in late Feb/early March.

Uncertainty has been removed in making lower and middle income tax rates permanent as well as the permanent patch for the AMT.

The current structure for unemployment benefits was extended by a year.

The MMT Grand Bargain: Raise Social Security Benefits and Suspend FICA!!!

Fact:

Every serious economic forecaster cuts his GDP and employment estimate

with tax hikes and spending cuts.

(AKA, the looming ‘fiscal cliff’!)

Fact:

Every serious economic forecaster would raise his GDP and employment estimate

with tax cuts and spending increases.

Fact:

All agree there would be no moral hazard or a waste and fraud issue with an increase in Social Security payments.

All agree that FICA is a highly regressive punishing tax on people working for a living, ideologically unacceptable to the ‘left’, and, of course, the ‘right’ is against any tax.

Fact:

Even with the presumed ‘current unsustainable path of future spending’ the Fed’s long term CPI (aka ‘inflation’) forecast remains at 2%, market participants via inflation indexed securities forecast equally low long term CPI increases, and there are no credible forecasts for any kind of ‘inflation’ problem from excess aggregate demand.

Fact:

The August 2011 debt ceiling debacle and downgrade of US credit, at the ‘worst possible time’, demonstrated that because the US ‘prints its own money’ the US government can’t run out of dollars; always has the unlimited ability to make any size dollar payment on a timely basis; is not dependent on and can never be dependent on dollar funding from foreigners, the IMF, or anyone else; pays interest rates based on rates voted on by the Federal Reserve; and is in no way is at any kind of risk whatsoever of becoming ‘Greece’.

Conclusion:

The MMT Grand Bargain for Prosperity:

1. Raise the minimum Social Security payment to $2,000 per month,

AND

2. Suspend FICA taxes

What’s so hard about this?

Feel free to distribute, particularly to your Congressmen!!!

Cliff notes

Jobless Claims Fell More Than Expected, Down by 25,000 to 370,000

I haven’t written much this week because I haven’t seen much to write about.

Still looks like both the economy and the markets are discounting the cliff. And still looks to me like ex cliff GDP would be growing at about 4% this quarter, with the Sandy-cliff related cutbacks keeping that down to maybe 2.5%. And going over the full cliff is taking off maybe 2% more, leaving GDP modestly positive.

Which is what stocks and bonds seem to be fully discounting.

As previously discussed, the housing cycle seems to have turned up, which looks to be an extended, multi year upturn with a massive ‘housing output gap’ to be filled. And employment is modestly improving as well, also with a large output gap to fill. Car sales are back over 15 million, and also with a large output gap to fill.

The way I see the politics unfolding, the full cliff will be avoided, if not in advance shortly afterwards, as fully discussed to a fault by the media. That means GDP growth head back towards 4% (and maybe more)

Nor do I see anything catastrophic happening in the euro zone. They continue to ‘do what it takes’ to keep everyone funded and away from default. And conditionality means continued weakness. Q3 GDP was down .1%, a modest improvement from down .2% in Q2, and a flat Q4 wouldn’t surprise me. The rising deficits from ‘automatic fiscal stabilizers’ (rising transfer payments and falling revenues) have increased deficits to the point where they can sustain what’s left of demand. And the recent report of German exports to the euro zone rising at 3.5% maybe indicating that the overall support for GDP will continue to come disproportionately from Germany. And rising net exports from the euro zone will continue to cause the euro to firm to the point of ‘rebalance’ which should mean a much firmer euro. And as part of that story, Japan may be buying euro to support it’s exports to the euro zone, as per the prior ‘Trojan Horse’ discussions, and as evidenced by the yen weakening vs the euro, also as previously discussed.

And you’d think with every forecaster telling the politicians that tax hikes and spending cuts- deficit reduction- causing GDP to be revised down and unemployment up, and the reverse- tax cuts and spending hikes causing upward GDP revisions and lower unemployment- they’d finally figure this thing out and act accordingly?

Probably not…

Huffington post- It’s not the deficit, stupid!

more on the cliff

Stocks down again yesterday but interestingly bond yields up a tad, dollar down a tad, oil and metals up, and even long BMA ratios holding steady, etc.

The cliff isn’t nearly as large and threatening as the debt ceiling cliff would have been in 2011 if that thing hadn’t been extended, and we’d gone cold turkey into an immediate and forced balanced budget. But that event is the stock market’s ‘recent memory’ of stock market reaction functions.

And this time GDP is being supported by a private sector credit expansion/housing expansion, with private debt service ratios substantially lower due to cumulative federal deficits adding to nominal ‘savings’. And the federal deficit remains well above 5% of GDP, which historically has been more than enough to reverse a recession.

And then there’s the election factor. Post election I’m hearing (anecdotally) distraught Romney supporters thoroughly convinced the President is a ‘socialist’ bent on destroying capitalism, taxing the rich ‘job creators’ and giving it to what Romney called ‘the 47%’ dependent class, etc. etc. etc. Merits of this ‘belief’ aside, it looks to me it’s driving portfolios to shift out of equities. However, if not supported by an actual decline in earnings, which is how I see it, it’s all a case of ‘pushing on a spring’.

Yes, the euro zone is a problem, with Q3 GDP just reported at -.1%. But that’s an ‘improvement’ from q2’s -.2% as larger deficits are acting counter cyclically to cushion the austerity driven decline. And Rehn was just quoted on Spain favoring not adding to austerity measures, perhaps indicating a move to ‘let it be’ for a while, which will allow GDP to stabilize at modestly positive levels.

And China is no longer going backwards, so that negative has been reversed as well.

Back to the cliff, in fact letting tax rates go up for high income earners should have little effect on GDP, as the marginally propensity to spend for that segment is reasonably low. (of course that means there’s no point in taxing that income in the first place, but that’s another story). Nor does it mean investment or employment will suffer since investment is driven by sales prospects. And with higher tax rates, and business expense tax deductible, the after tax cost of investment goes down with higher tax rates. For example, in the 70’s, when my tax rate was around 70%, I clearly recall making very high risk investments figuring it was better than giving 70% to the govt. Point is, taxing income and savings that isn’t going to be spent is about social engineering, and not ‘funding the deficit’ or altering aggregate demand, and is intellectually honestly framed as such. So point here is, I score the effect of raising the highest tax rates at 0 regarding aggregate demand.

This all supports my take that the stock market has over discounted the cliff, partly for ideological reasons, partly due to the recent memory of what stocks did during the debt ceiling debacle, and partly from fear of what’s going on in the rest of the world.

So as we get through it all with modest top line and earnings growth continuing, I’m looking for valuations to quickly return to at least where they were before the election.