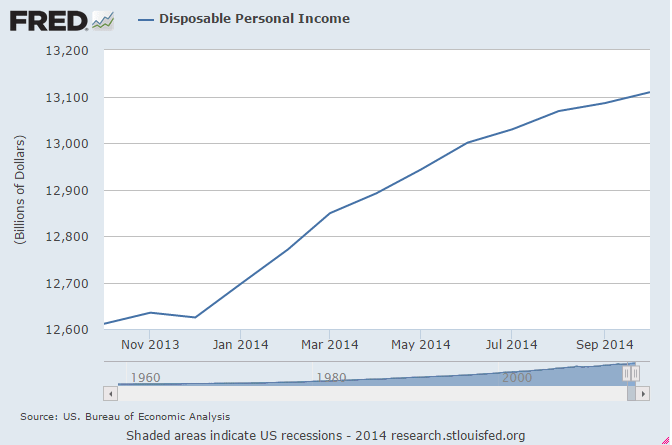

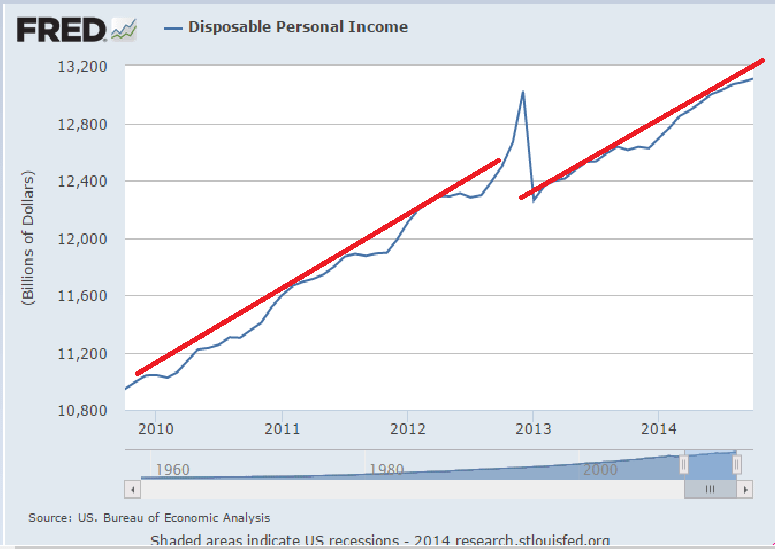

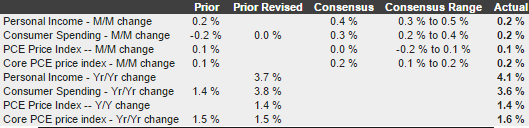

This is after tax personal income not adjusted for inflation. Note that there was anticipation of an acceleration from the first quarter, but now it looks like the growth has slowed and rolled over:

Here you can see how it was growing steadily, then shifted down when my payroll tax holiday expired, sort of resumed growing at the same rate, and now may be falling off, even with what the mainstream call ‘solid’ payroll growth:

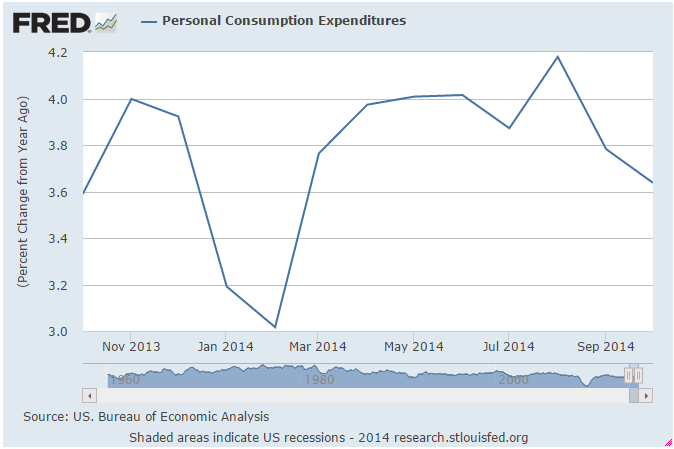

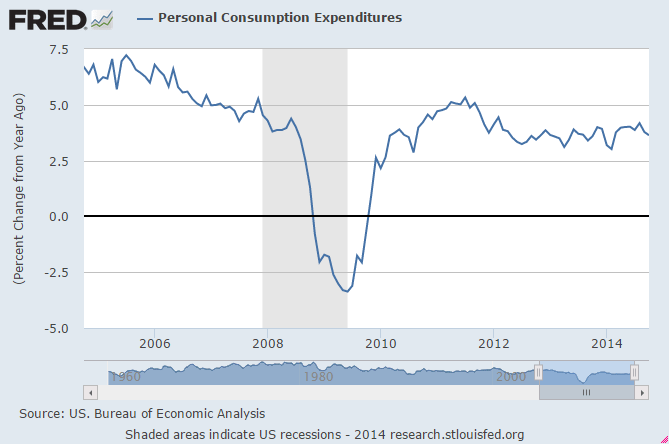

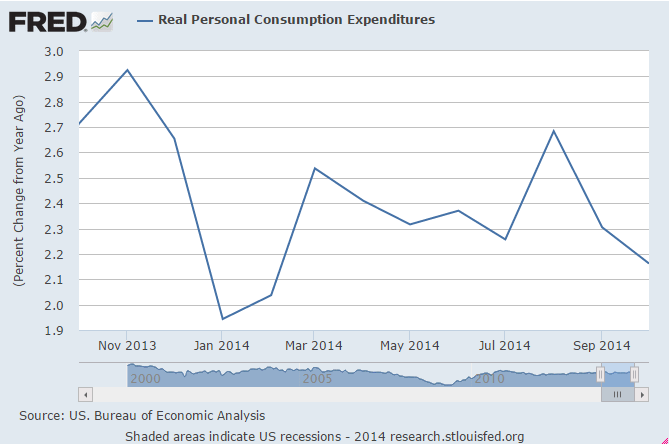

Likewise, there’s been a lid on the growth personal consumption expenditures where the growth rate dipped for the cold winter, recovered, and then fell off some:

Adjusted for inflation/cpi the pattern is the same:

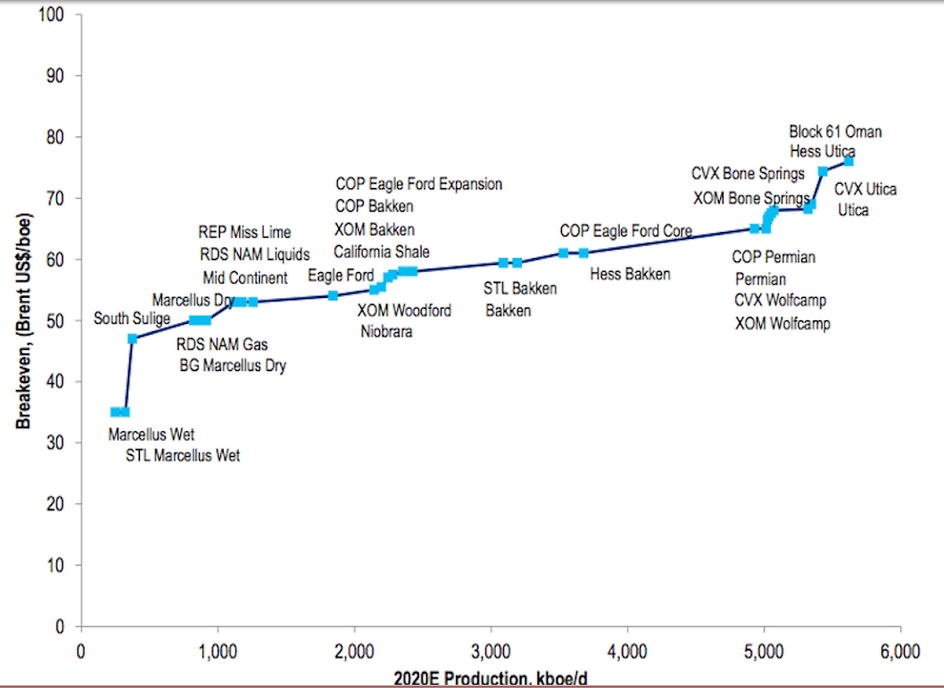

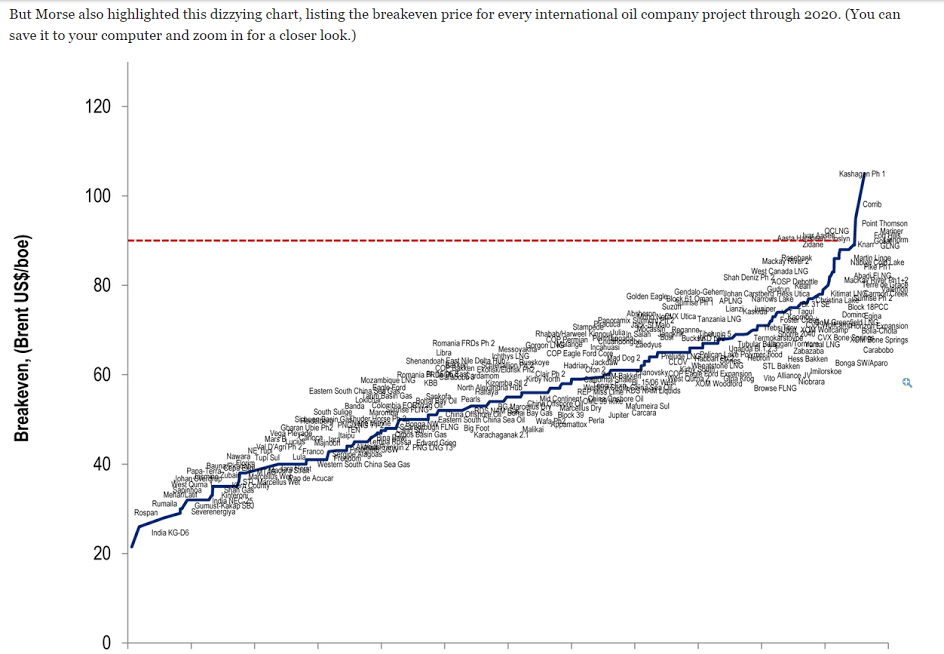

Oil- Not all that much to it.

The Saudis remain price setter as a simple point of logic.

No telling what their price target may be at any time, but they simply set price for their refiners and let them buy all they want at that price. And no one else has the excess capacity to do that.

Possible motives?

Put high priced producers out of business with $trillions of losses to make sure that when the subsequently raise prices to 150(?) new investment in high priced crude will then be considered to risky for anyone to finance?

And/or it’s not illegal for insiders to have gotten short for their personal accounts prior to the price cuts and subsequently covering prior to increasing prices, functionally transferring a bit of wealth from the state to private accounts?

Ramifications for the US:

US consumers helped a bit- about $100 billion/year last I heard?

Capex gets hurt by at least that much?

Trillions in value lost from loans and investments going south?

Thousands of high paying jobs lost in North Dakota, etc. due to reduced capex?

(EU not so much as they don’t invest nearly as much in high priced energy exploration/production?)

Canada, Mexico, Venezuela, Australia etc. economies and related securities/investments toast?

etc.

{kind=link}