Volkswagen to Pare, Delay Capital Investments

Oct 6 (WSJ) — Volkswagen AG plans to slash an €86 billion ($96 billion) investment plan and step up cost-cutting as it grapples with fallout from its emissions scandal, Chief Executive Matthias Müllersaid on Tuesday.

Global Oil to Cut Spending by $130 Billion, OPEC Says

Germany : Industrial Production

Highlights

Industrial production was weaker than expected in August. A 1.2 percent monthly fall exactly reversed an upwardly revised gain in July but with base effects favourable, annual seasonally and workday adjusted growth was boosted from 0.9 percent to 2.5 percent.

The monthly headline decline reflected worryingly broad-based losses. Hence, capital goods output was down 2.1 percent, consumer goods 0.4 percent and intermediates were only flat. Energy decreased 1.4 percent and construction was off 1.3 percent.

Despite August’s setback average industrial production in July/August was still 0.4 percent above its mean level in the second quarter. However, output will need to expand 0.5 percent in September for the third quarter just to match the previous period. As such, the likelihood is that goods production provided at best only a limited boost to real GDP in July-September which in turn increases the risk of a disappointingly sluggish increase in whole economy output.

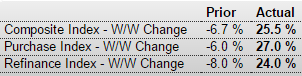

Up big but front loaded:

“The number of applications for purchase and refinance mortgages soared last week due both to renewed rate volatility and as many applications were filed prior to the TILA-RESPA regulatory change,” said Lynn Fisher, the MBA’s vice president of research and economics.

The change is part of a move by federal regulators to further protect borrowers by forcing lenders to disclose all details of a loan at least three days prior to closing; it went into effect October 3rd.

MBA Mortgage Applications