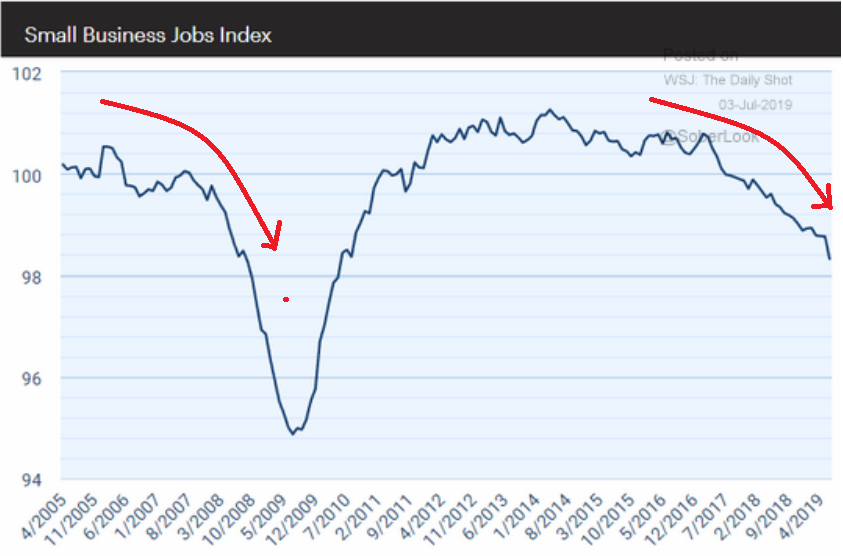

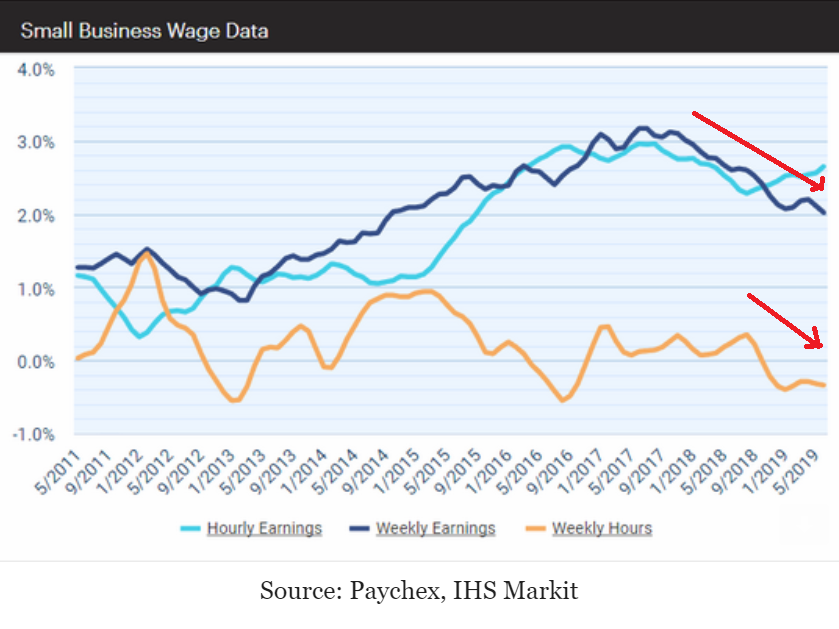

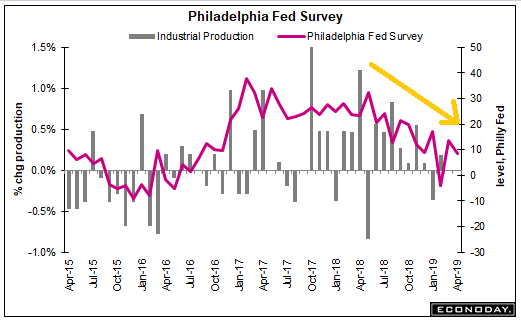

Up this month but trending lower:

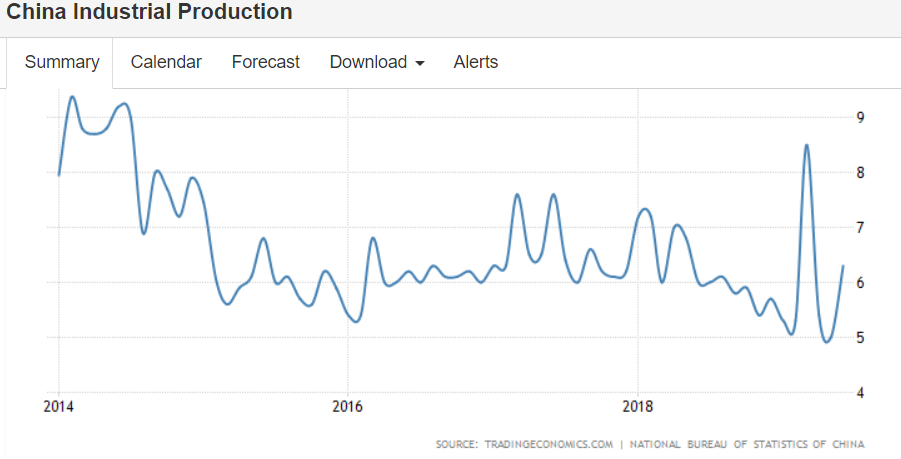

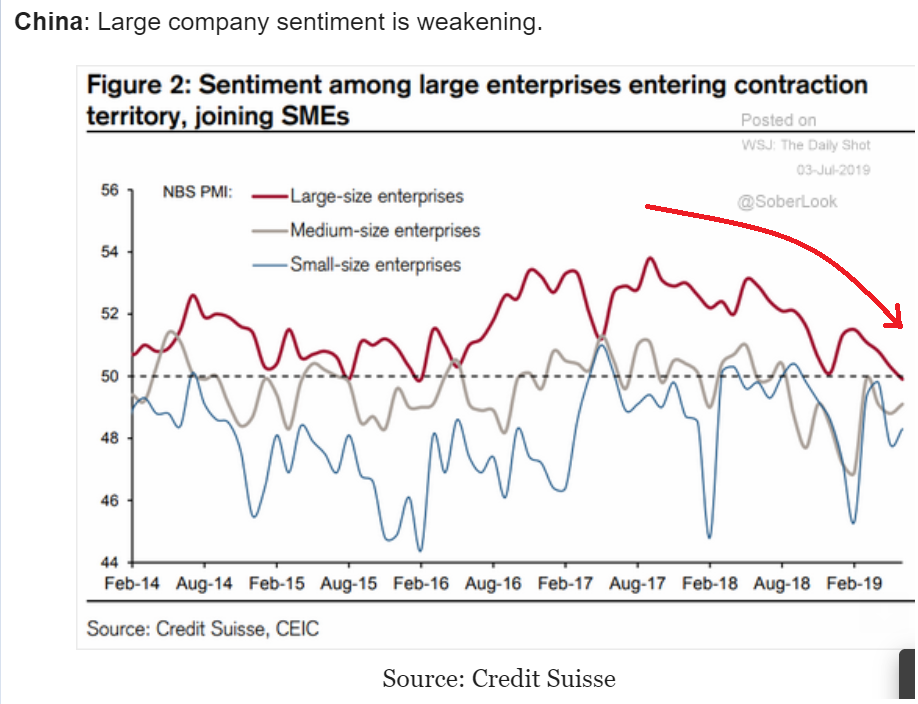

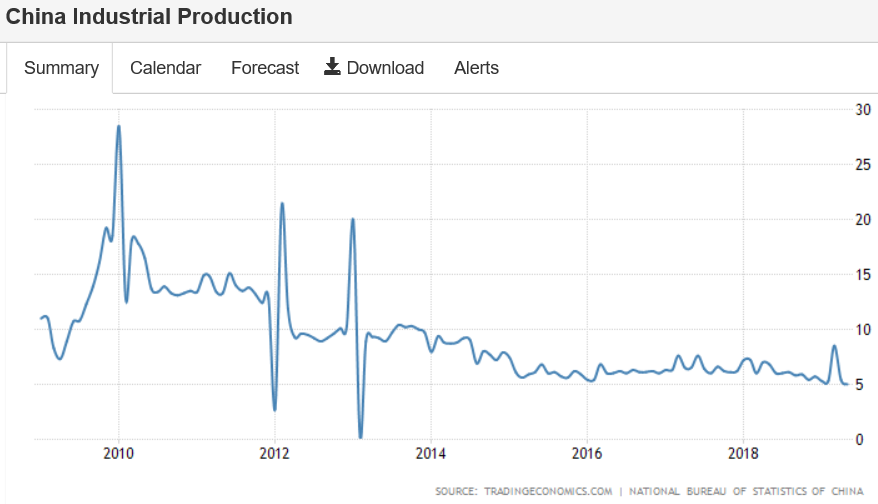

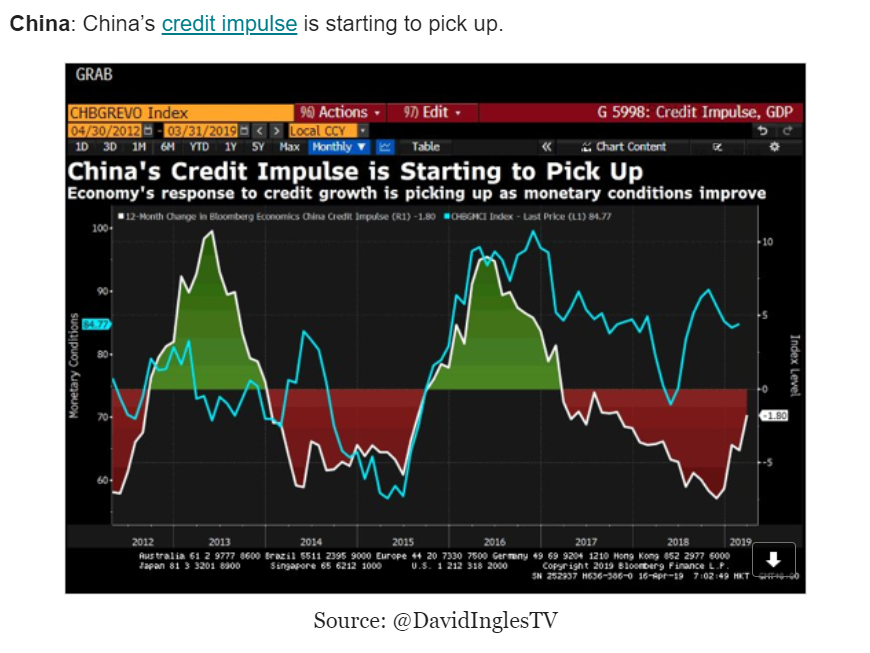

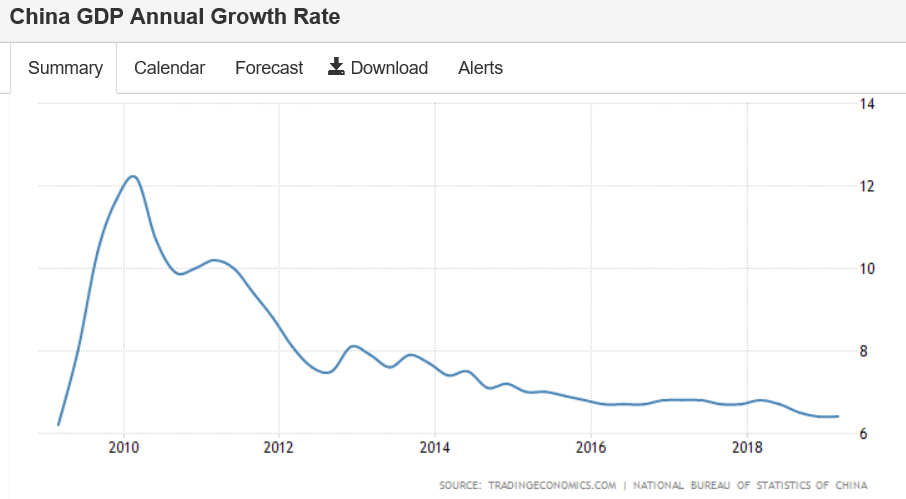

China has been trying to recover with fiscal adjustments:

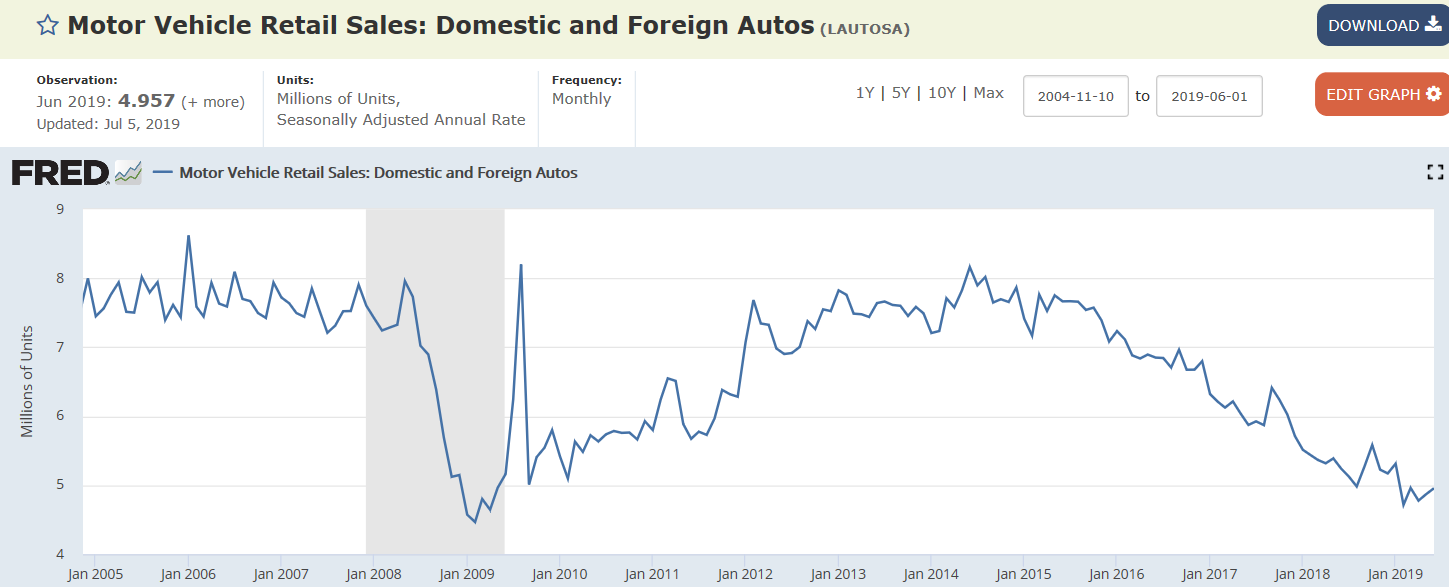

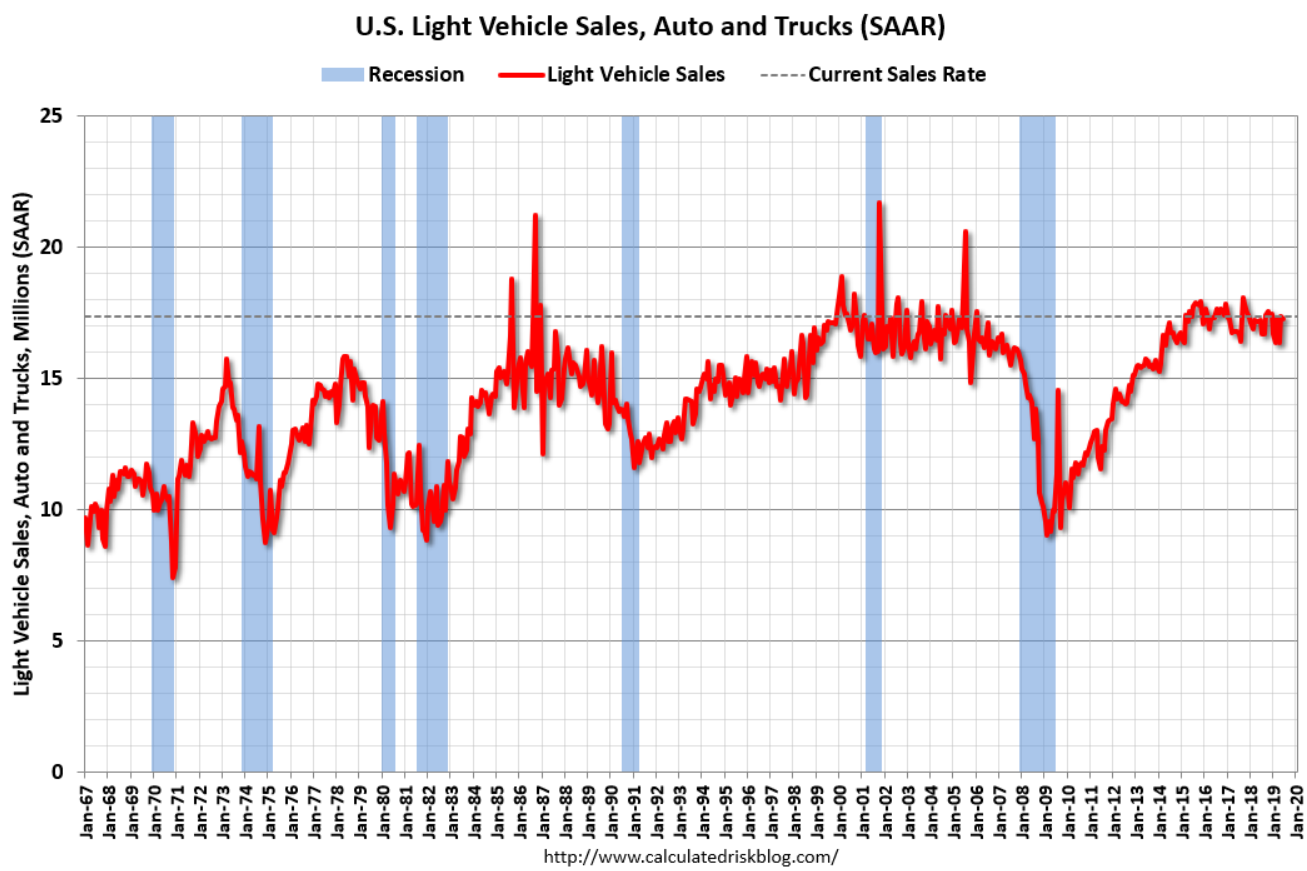

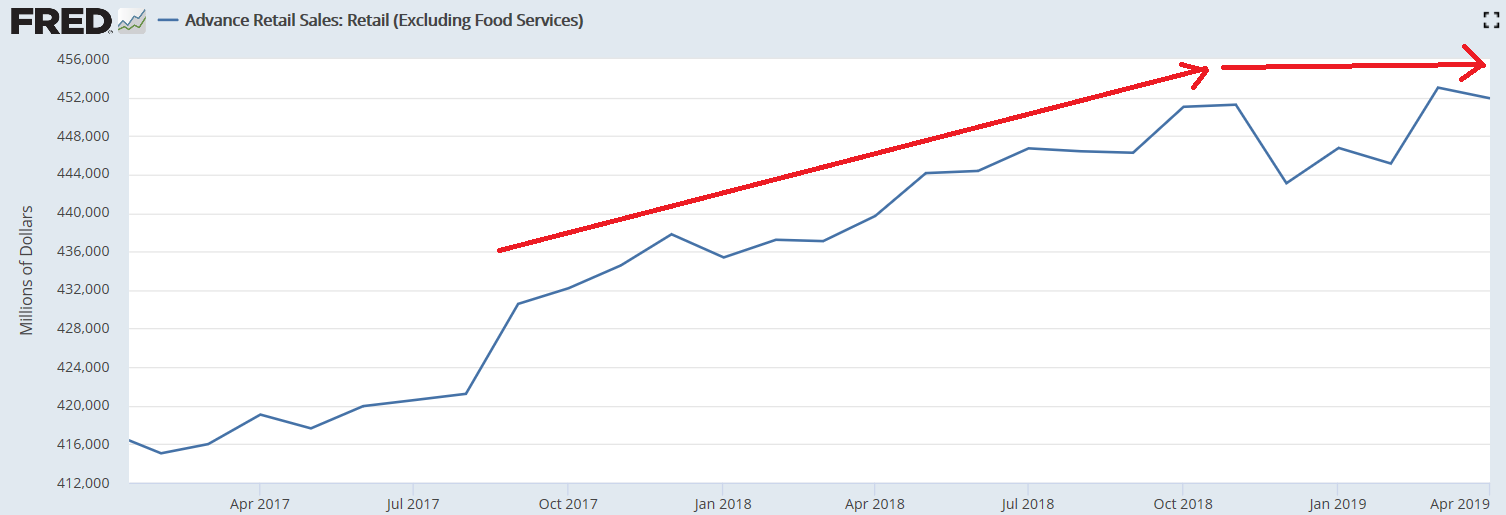

Doesn’t include pickups and other light trucks:

Up this month but trending lower:

China has been trying to recover with fiscal adjustments:

Doesn’t include pickups and other light trucks:

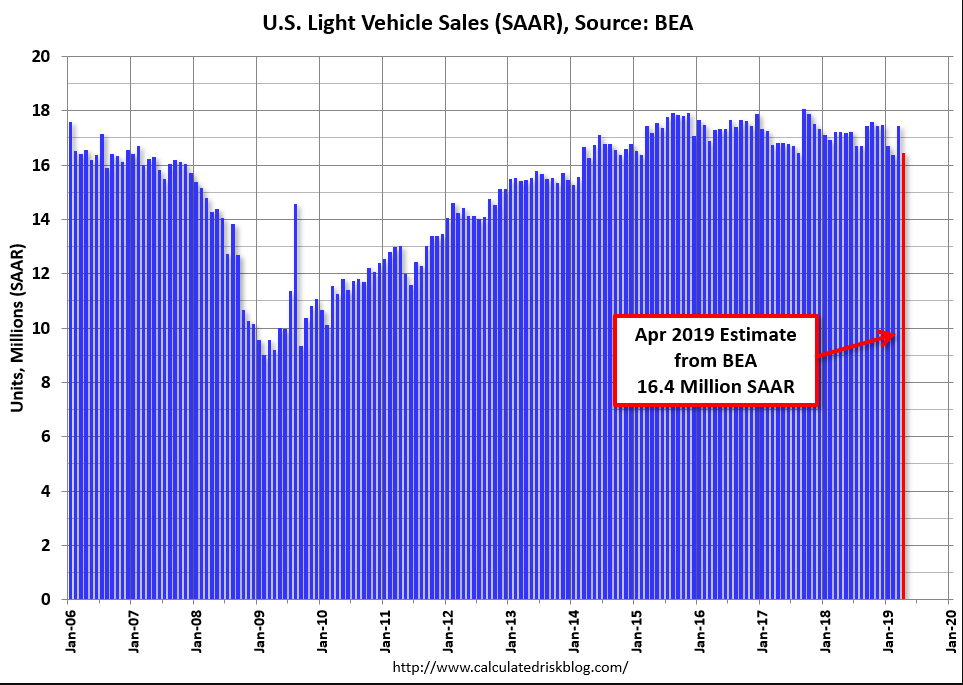

Light vehicle sales peaked a while back:

Been helping to support the $US:

Eurozone Retail Sales Fall Unexpectedly

Retail trade in the Euro Area fell 0.3% in May, following a 0.1% drop in April and missing expectations of a 0.3% growth, as sales declined for all main categories. Among the bloc’s largest economies, Germany’s retail trade decreased for the second month, while gains were recorded in France and Spain. Year-on-year, retail sales rose 1.3%, also missing forecasts of 1.6%.

Not adjusted for inflation:

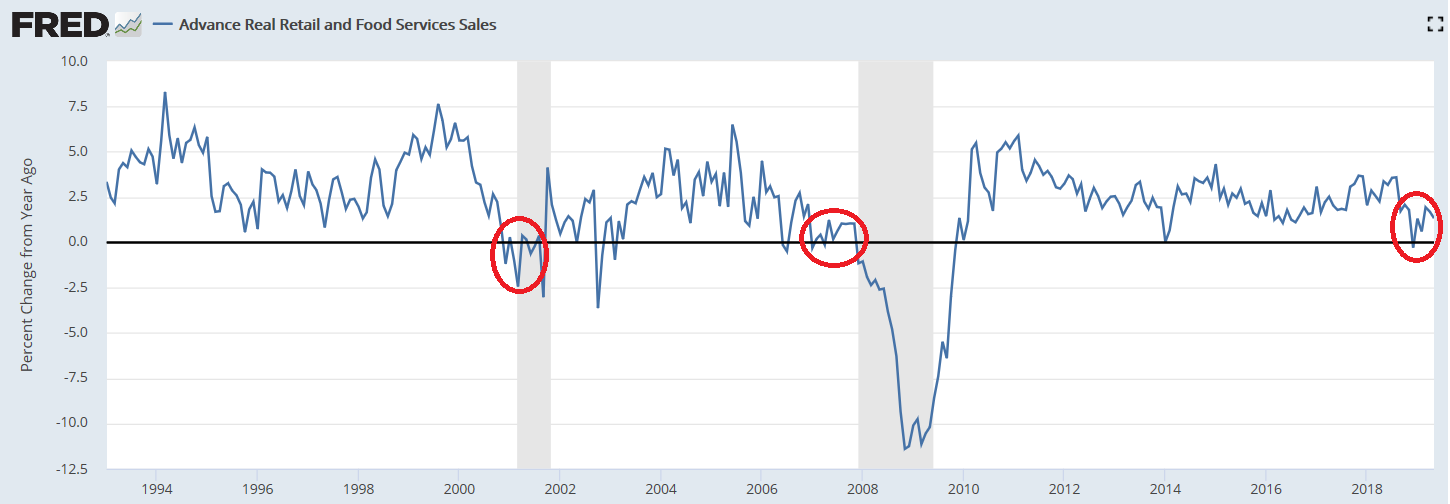

Adjusted for inflation:

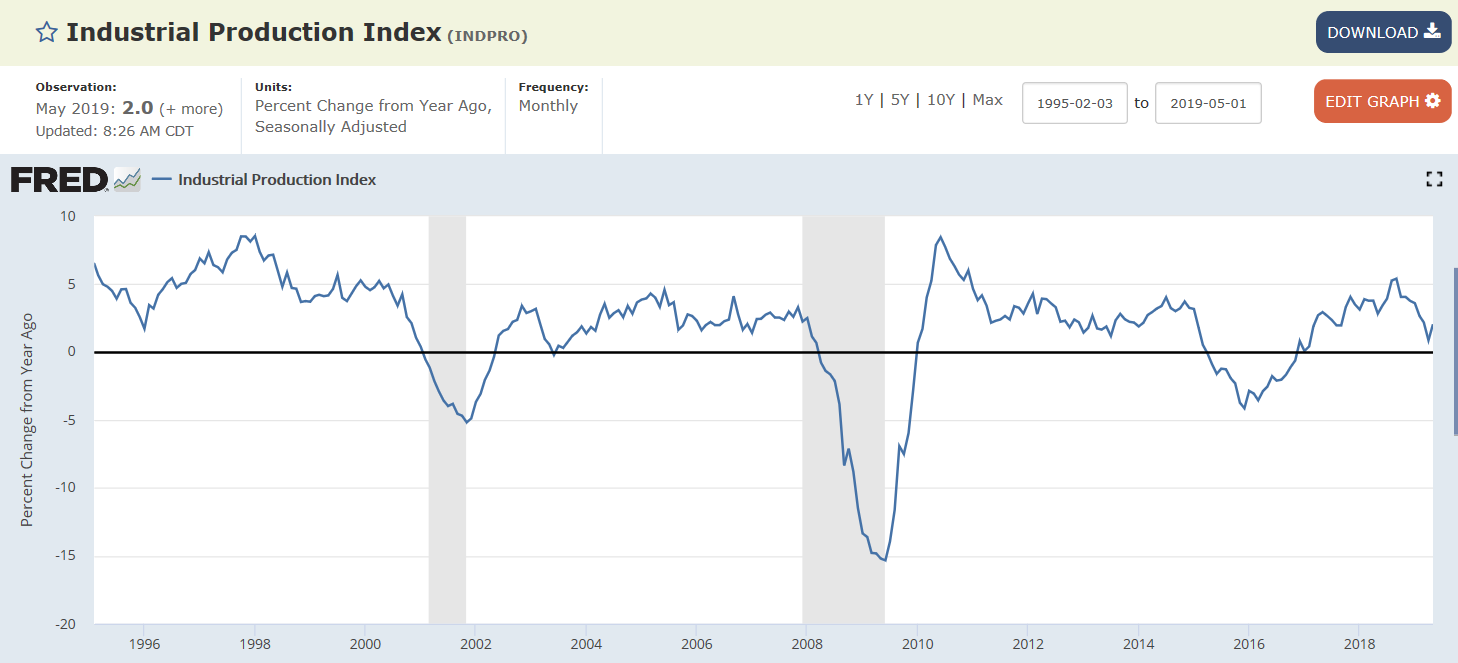

Still looking down:

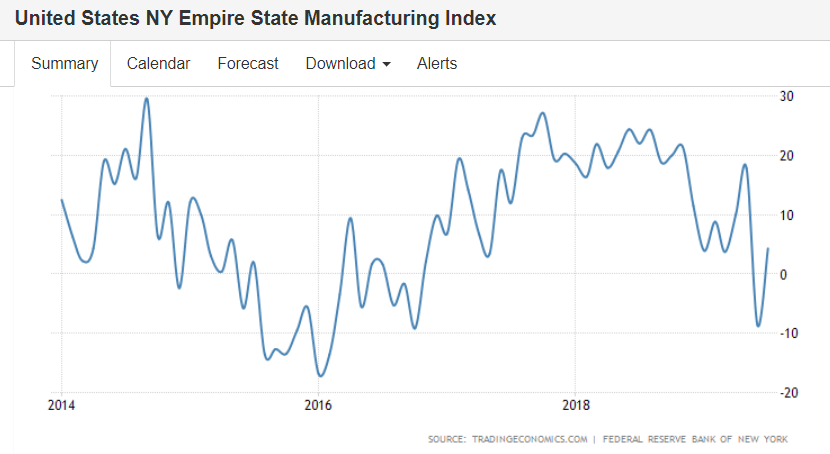

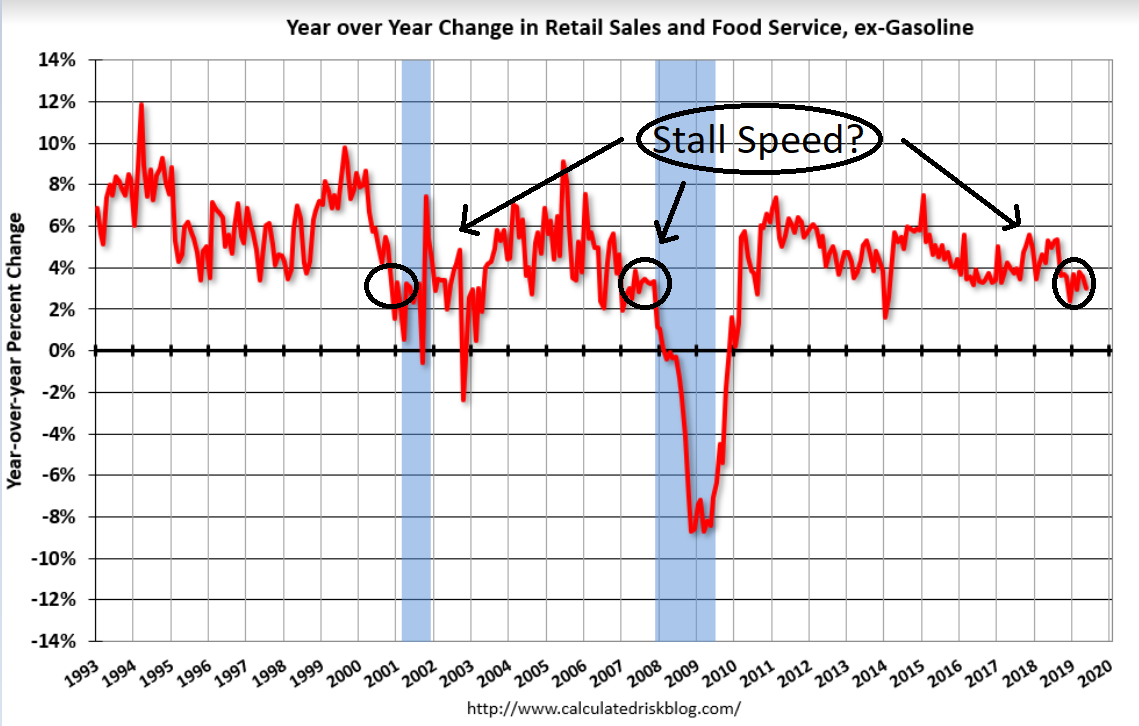

Remember when last month’s spike higher was presumed to be the start of a turn around?

.

.

Interest-Rate Policy Is Backward, Modern Monetary Theory Pioneer Mosler Says

Under consumption identity: for ever agent that spent less than his income, another must have spent more, or the output would not have been sold.

In other words, deficit spending, private or public, is the ‘offset’ to unspent income (savings). The chart shows one of the components of private sector deficit spending which appears to align with economic growth:

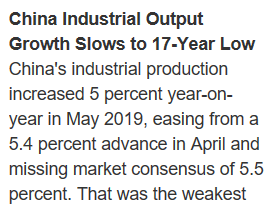

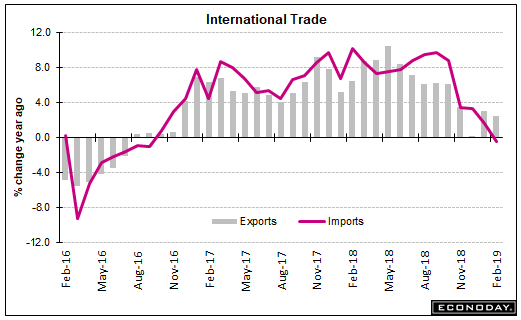

Tariffs (levied on the grounds that China and others weren’t charging us enough…) causing the collapse in exports globally, and import weakness most often is a sign of domestic demand weakness:

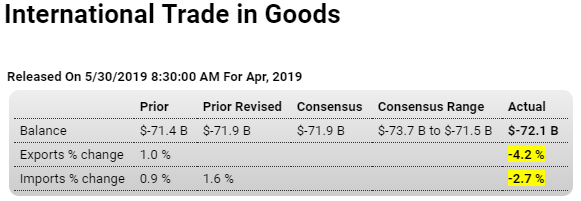

Highlights

Sharp declines in exports are unwelcome headlines in April’s advance data on goods trade. The monthly deficit remains very deep, at $72.1 billion with exports falling 4.2 percent year-on-year and with imports also down, 2.7 percent lower. The deficit compares unfavorably with a $71.3 billion monthly average in the first quarter that marks a weak opening for net exports in the second quarter.

Capital goods are the US’s largest exports and these fell 6.5 percent in the month to $44.3 billion. Compared with April last year, capital goods exports are down 3.7 percent. Auto exports are also down, 7.2 percent lower to $12.9 billion and 6.7 percent below last year. The only export component showing a gain is food & feeds which rose 0.5 percent to $11.2 billion but which is nevertheless 6.2 percent below April last year.

The decline on the import side is also led by a 3.5 percent decline for capital goods ($55.4 billion) but also includes 3.1 percent and 2.3 percent monthly declines in autos ($30.9 billion) and consumer goods ($54.2 billion) as well as a 1.1 percent drop in foods ($12.8 billion).

Global trade figures have been contracting and the latest US numbers are part of that picture. Today’s report gets second-quarter GDP, already held down by contractions for April retail sales and industrial production, off to a slow start.

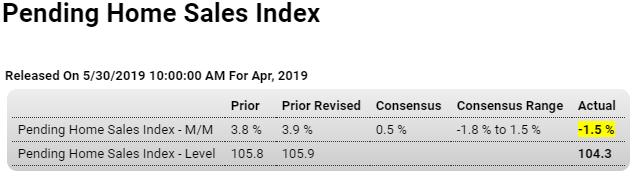

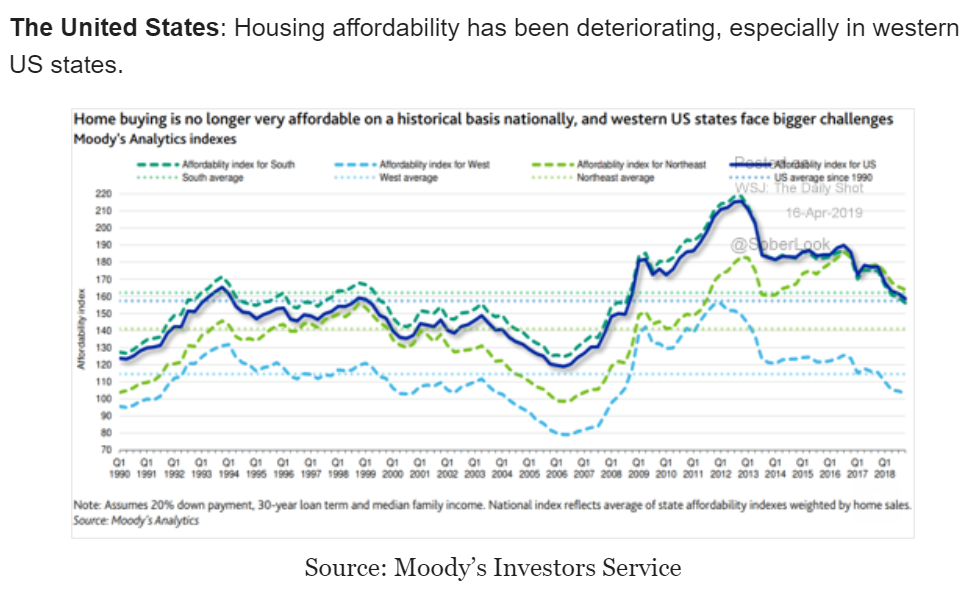

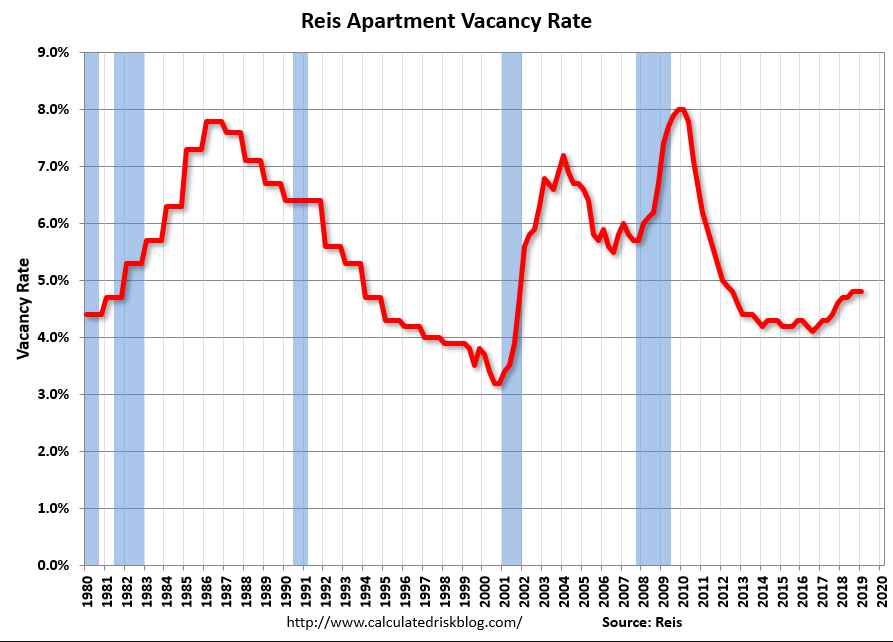

Weakness in housing continues:

Highlights

The forecasters were optimistic but pending home sales couldn’t deliver. The index fell 1.5 percent in April vs a consensus for a 0.5 percent gain, yet the monthly drop does follow an outsized 3.9 percent revised gain in March which makes for a hard comparison. Nevertheless a decline in April is not a good indication for momentum in the spring sales season. Existing home sales have been moving higher this year but today’s report will hold down expectations for May and June.

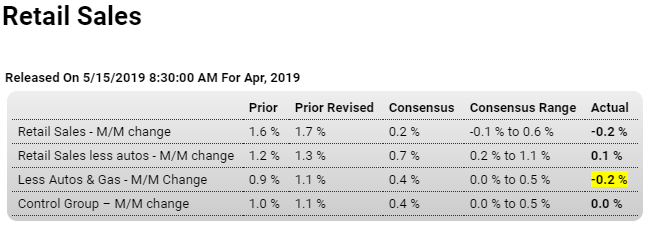

Weak and weaker than expected:

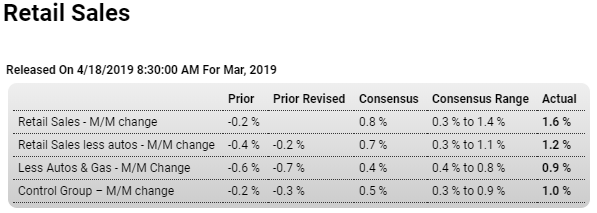

Highlights

The second quarter gets off to a stumbling start pulled down by a 0.2 percent headline decline in an April retail sales report where the core details show unexpected weakness. Excluding autos, in which sales were already expected to fall sharply, April sales managed only a 0.1 percent gain to fall underneath Econoday’s consensus range. Excluding autos and also gasoline sales, which were already expected to rise sharply, sales fell 0.2 percent in April to also fall below the consensus range. Just making the consensus range is a no change result for the control group, a component used in the calculation of GDP and pointing squarely to early second-quarter deceleration in consumer spending which had already decelerated sharply in the first quarter.

A 1.1 percent decline in auto sales (signaled by the prior release of unit sales at manufacturers) is no surprise and neither is a 1.8 percent jump at gasoline stations, signaled here by the price of gas. The big surprise is a 1.3 percent drop at electronics & appliance stores that follows a 4.3 percent tumble in March. Weakness here hints at lower prices for consumer electronics and also lower spending on home improvements. Furniture sales also hint at trouble for residential investment, coming in unchanged following March’s 3.1 percent decline, as do sales of building materials which fell 1.9 percent in April following, however, a 1.2 percent rise in March.

The best news in the report comes from its weakest sub-component, department stores where April sales jumped 0.7 percent. This was enough, however, to give only a small 0.2 percent lift to the overall general merchandise component. Another positive is restaurants where sales rose 0.2 percent on top of a great monthly surge of 5.7 percent in March.

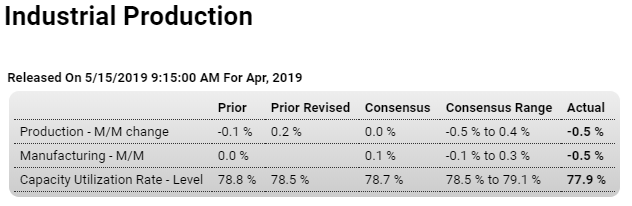

Another negative surprise:

Highlights

Like retail sales earlier this morning, the headline 0.5 percent decline for April industrial production is not masking strength underneath. Also falling 0.5 percent was production at manufacturers which is even more unexpected than the headline decline.

Motor vehicles and parts, where consumer sales have been mostly soft this year, fell 2.6 percent in April for a second monthly decline and year-over-year contraction of 4.4 percent. Business equipment fell 2.1 percent in the month for yearly growth of only 0.1 percent which doesn’t point to acceleration for business investment. Consumer goods also fell, down 1.2 percent in the month with construction supplies up only 0.1 percent that follows March’s 1.7 percent dip in readings that don’t point to strength for construction in general. Selected hi tech is a positive for April, up 0.6 percent with annual growth here at 3.2 percent.

Also positive is a 1.6 percent jump in mining volumes which rose 1.6 percent in April that follows, however, three straight months of declines. Output at utilities fell 3.5 percent in April with the yearly rate of minus 4.7 percent also pointing to general industrial weakness.

However tight the US labor market may be, capacity does not appear to be tight in the industrial sector as capacity utilization fell 6 tenths in April to a much lower-than-expected 77.9 percent. Utilization in the manufacturing sector is down 5 tenths to 75.7 percent.

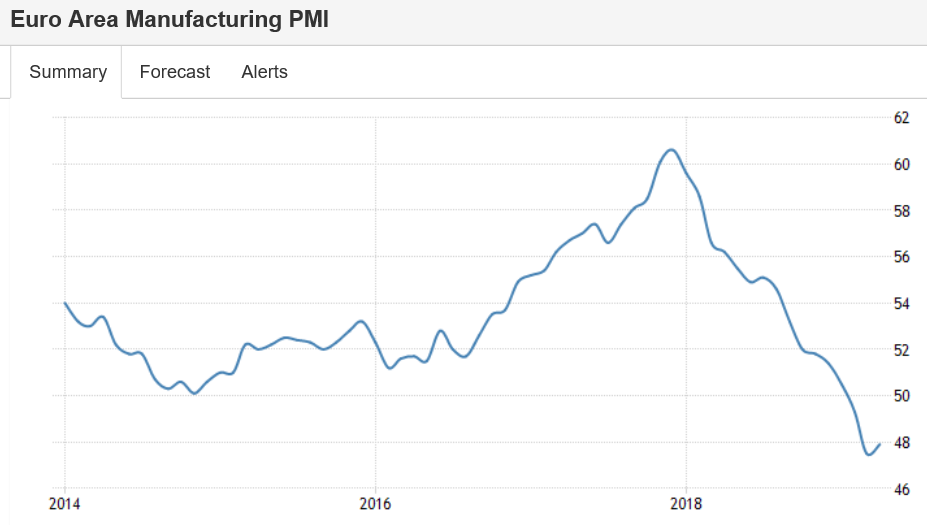

This report doesn’t breakdown production of goods aimed for the domestic market and those for the foreign market but it will nevertheless offer a baseline for the overall effects of increased US-China tariffs. Going into those tariffs, the manufacturing sector, which first began to slow late last year, appeared to be flat at best.

Rolling over:

Corporate Japan logs first profit dip in 3 years as China slows

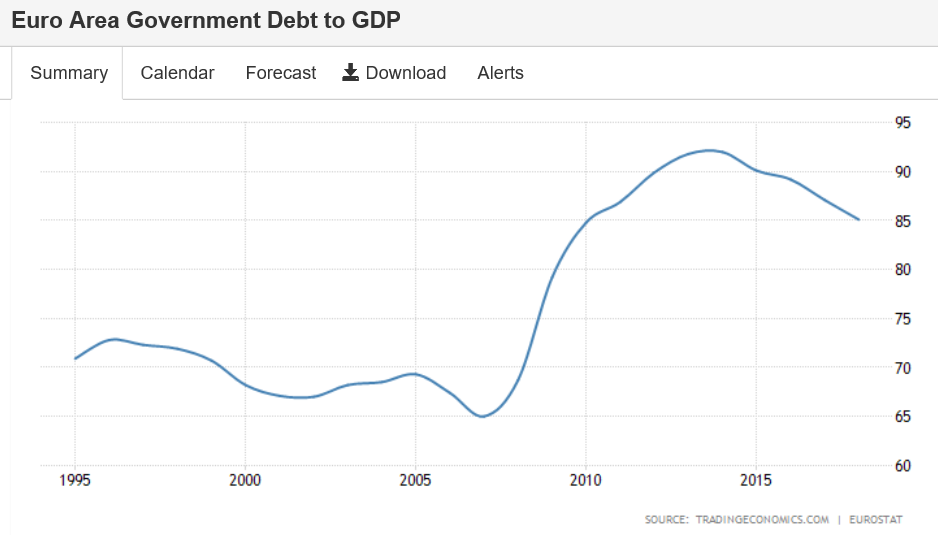

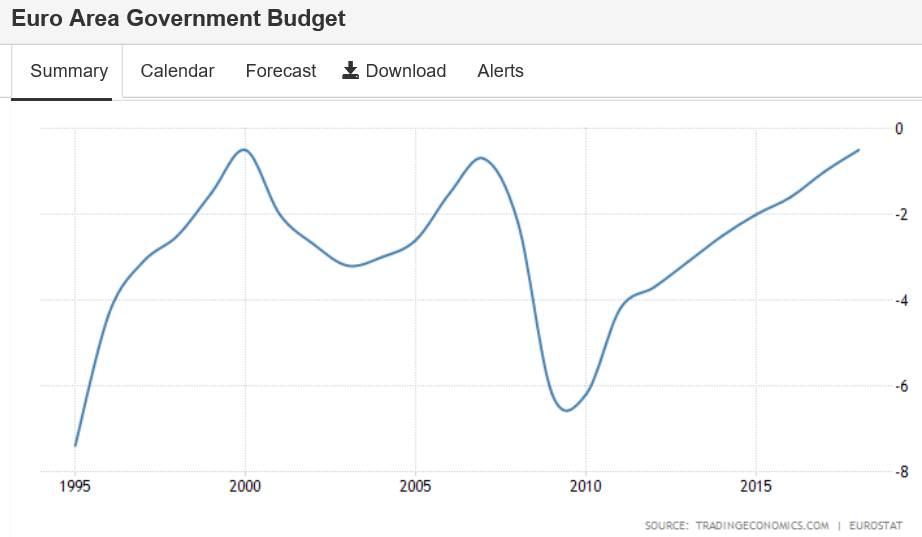

Fiscal has tightened in the euro area, and now with the global trade collapse prospects are looking grim:

Euro Area recorded a Government Budget deficit equal to 0.50 percent of the country’s Gross Domestic Product in 2018. Government Budget in the Euro Area averaged -2.84 percent of GDP from 1995 until 2018, reaching an all time high of -0.50 percent of GDP in 2000 and a record low of -7.40 percent of GDP in 1995.

Continues to decelerate:

Highlights

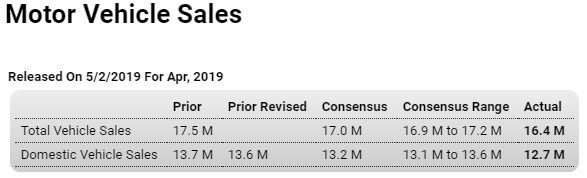

Jerome Powell may have cited March auto sales as an economic plus in yesterday’s FOMC press conference, but April sales couldn’t keep up the pace. Unit vehicle sales managed only a 16.4 million annual rate in April which was far below March’s 17.5 million rate and well below Econoday’s consensus range. The setback returns the sales pace to the disappointing mid-16 million range of January and February that was a ratcheting down from the fourth-quarter pace in the mid-17 million range.

Sales of domestic-made vehicles came in at a 12.7 million rate in April, also below the consensus range. Today’s results point to trouble for the motor vehicle component of the April retail sales report and, though unit sales data are a clouded mix of business and consumer sales, nevertheless hint strongly at an inauspicious second-quarter opening for consumer spending in general.

Deep in negative territory as trade wars continue:

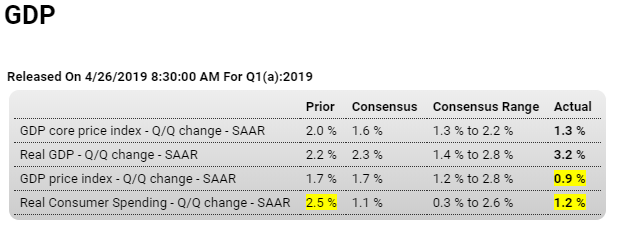

Headline number looks strong, but details show weakness, particularly personal consumption expenditures which continue to decelerate:

Highlights

The consumer isn’t on fire but still contributed to a very solid 3.2 percent growth rate for first-quarter GDP. Net exports are the driving force of the headline rate, still deeply negative at minus $899.3 billion but nevertheless contributing 1.03 percentage points to the quarter’s calculation though trade data for March, which have yet to be released, were imputed. Inventories rose sharply and added 0.65 points but whether the build was desired may be in question, that is given what was less than robust strength in consumer demand.

Consumer spending (personal consumption expenditures) rose at a modest-to-moderate and largely as expected 1.2 percent pace but nevertheless contributed 0.82 points to the quarter though spending on durables, a discretionary component, fell very steeply and pulled the quarter 0.38 points lower. But spending on nondurables and especially services was strong, contributing 0.24 and 0.96 points respectively. Not strong at all was residential investment which contracted at a 2.8 percent annual pace — the fifth straight quarterly contraction — and subtracted 0.11 points from the quarter.

In contrast once again was business investment which rose at a very favorable 2.7 percent pace and added to the quarter 0.38 points. Government purchases were also very strong, at a 2.4 percent growth rate for a 0.41 point contribution.

A clearer look on underlying domestic demand comes from final sales to domestic purchases, a reading that excludes both net exports and inventories and where the growth rate was only 1.4 percent. Lack of consumer punch is a bit of a puzzle at least based on the strength of the labor market. Price readings in today’s report are very subdued at 0.9 percent for the overall index and only 1.3 percent for the core. The pace of the nation’s economy isn’t as strong today’s headline suggests with questions over the consumer, first raised by the 1.6 percent plunge in December retail sales, still persisting.

Not looking good:

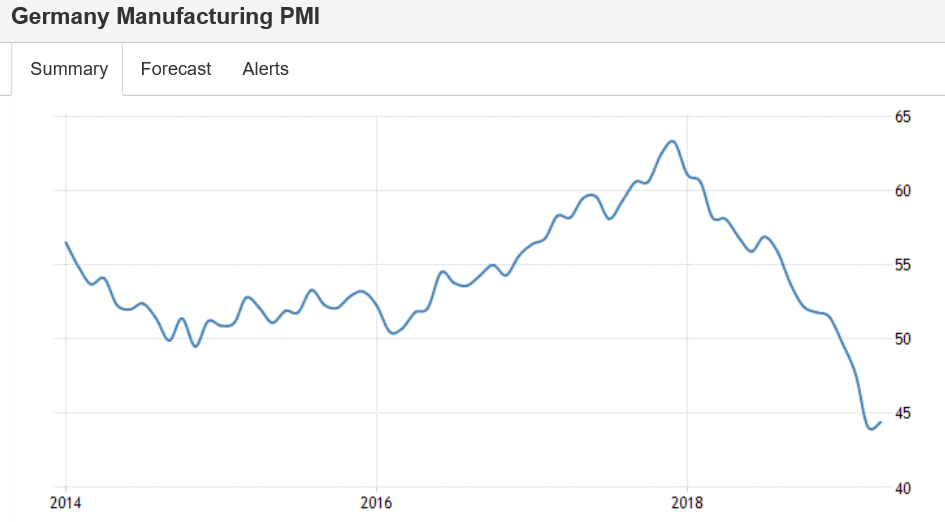

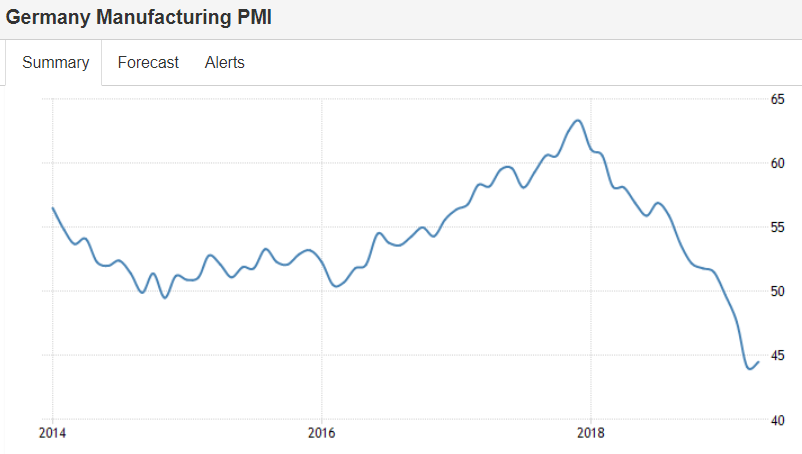

German Factory Activity Continues to Contract in April

The IHS Markit Germany Manufacturing PMI rose to 44.5 in April 2019 from the previous month’s near seven-year low of 44.1, but below market expectations of 45, a preliminary estimate showed. Still, the latest reading pointed to a sharp contraction in the manufacturing sector, as inflows of new business fell for a fourth straight month led by a further steep decline in new export orders, which dropped at the second-fastest rate in the past ten years. Firms highlighted weak demand across the automotive sector in particular, whilst also suggesting some hesitancy among UK based clients. In addition, work-in-hand at manufacturers declined the most for almost a decade while employment levels were unchanged. Looking ahead, business confidence towards the year-ahead outlook was the weakest since November 2012.

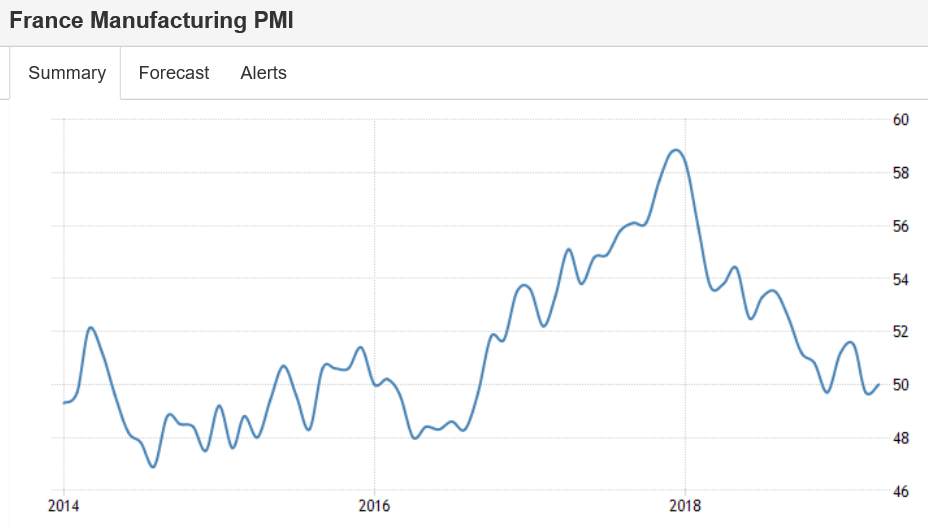

French Factory Activity Contracts the Most in 2-1/2 Years

The IHS Markit France Manufacturing PMI edged down to 49.6 in April 2019 from 49.7 in the previous month, missing market expectations of 50, a preliminary estimate showed. The latest reading pointed to the steepest contraction in the manufacturing sector since August 2016, as output fell the most in four years. On the other hand, new orders and export sales both declined at a softer pace while employment growth accelerated.

Back in negative territory:

In contrast, this is an upbeat report (subject to revision) for March, though the chart doesn’t look so good:

Highlights

The optimists weren’t quite optimistic enough as March retail sales, across all major readings, came in just above Econoday’s high estimates. Still, the trend is uneven and not pointing with certainty to acceleration ahead for consumer spending.

Total retail sales jumped 1.6 percent in March which exactly matches the decline in the much more important month of December. February sales are unrevised at the headline level at minus 0.2 percent with January sales revised 1 tenth higher to a gain of 0.8 percent.

Ex-auto sales show a bit less strength over this period, rising 1.2 percent in March but falling 2.1 percent in December with February revised to a 0.2 percent decline and January holding at an increase of 1.4 percent. Other core readings are similar, showing strength in March following bumpy results previously with ex-autos ex-gas rising 0.9 percent in the latest month and control group sales, which are inputs into GPD, up a helpful 1.0 percent.

Vehicle sales stand out sharply in March, up 3.3 percent following declines in the two prior months. Sales at gasoline stations also stand out, up 3.5 percent for a second straight month but boosted by price effects for fuel.

Convincing strength is evident once again for non-store retailers which, after falling 4.5 percent in December, have posted three straight strong gains including 1.2 percent in both March and February. Restaurants are also convincing, up 0.8 percent in the latest month for a third straight gain in what speaks directly to discretionary strength. Furniture & home furnishing stores are also doing well with three straight gains including a 1.7 percent March jump.

Lagging are department stores, unchanged following three straight declines which may reflect a shift underway in consumer habits away from traditional malls than weakness in consumer demand. General merchandise, which is the broader category that includes department stores, rose 0.7 percent in March but failed to make up for recent weakness.

Yet this report is not about weakness but about strength, and the results are certain, like yesterday’s trade data for February, to give a lift to first-quarter GDP estimates. The economy’s soft patch so far this year isn’t as soft as it once looked, but questions remain.

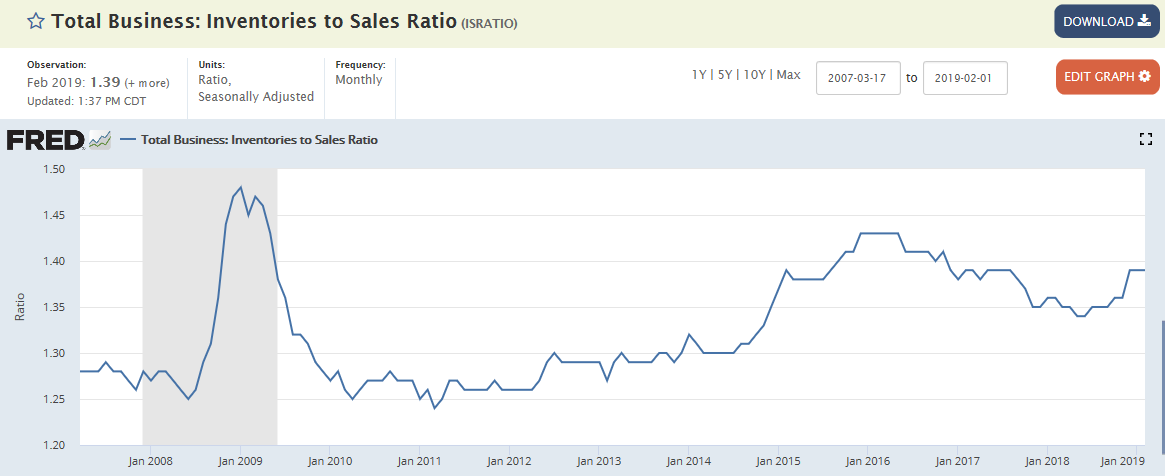

Elevated inventories are not a good sign:

(Reuters) The U.S. central bank’s “Beige Book” report found economic activity grew at a slight-to-moderate pace in March and early April. Prices have risen modestly since the last Beige Book, with tariffs, freight costs and rising wages often cited as key factors, the Fed said. It added that consumer spending was mixed but suggested sluggish sales for both general retailers and auto dealers. Wages grew moderately in most districts for both skilled and unskilled workers. In terms of the manufacturing sector, the Fed said contacts in many districts reported that trade-related uncertainty was weighing on activity.

Imports and exports both decelerating indicates a weaker global economy, and weak US retail sales indicates domestic consumer spending growth is slowing:

Highlights

First-quarter GDP looks to get a major boost from improvement in the nation’s trade deficit which, for February, came in at much lower-than-expected $49.4 billion. And the positives are more than just a technical calculation as exports, driven by aircraft, jumped 1.1 percent in the month on top of January’s 1.0 percent gain.

Exports of goods rose 1.5 percent to $139.5 billion as civilian aircraft rose $2.2 billion in the month. Outside of aircraft, however, gains are less striking with auto exports up $0.6 billion and with monetary gold and consumer goods showing marginal gains. For farmers, the results are slightly in the negative column with exports down $0.2 billion. But exports of services, at $70.1 billion in the month and usually a reliable plus, rose 0.3 percent.

Imports rose only 0.2 percent in the month, totaling $259.1 billion but with consumer goods showing yet another large increase of $1.6 billion in the month. Imports of industrial supplies fell $1.2 billion despite a 0.8 billion rise in the oil subcomponent. Imports for other categories were little changed.

Bilateral country deficits show a sharp decline with China, down $24.8 billion in unadjusted monthly data that are hard to gauge given strong calendar effects during the lunar new year. But year-to-date, the deficit with China is at $59.2 billion and down sizably from $65.2 billion in the comparison with the 2018 period. February’s deficit with both the European Union and Canada narrowed while deficits with Japan and especially Mexico, at $7.4 billion vs January’s $5.8 billion, deepened.

Today’s results are certain to lift first-quarter GDP estimates which had been roughly at the 2 percent line. The average deficit for the first two months of the quarter is $50.3 billion which is well under the $55.6 billion monthly average in the fourth quarter. And the easing deficit with China may well ease immediate tensions in U.S.-Chinese trade talks.

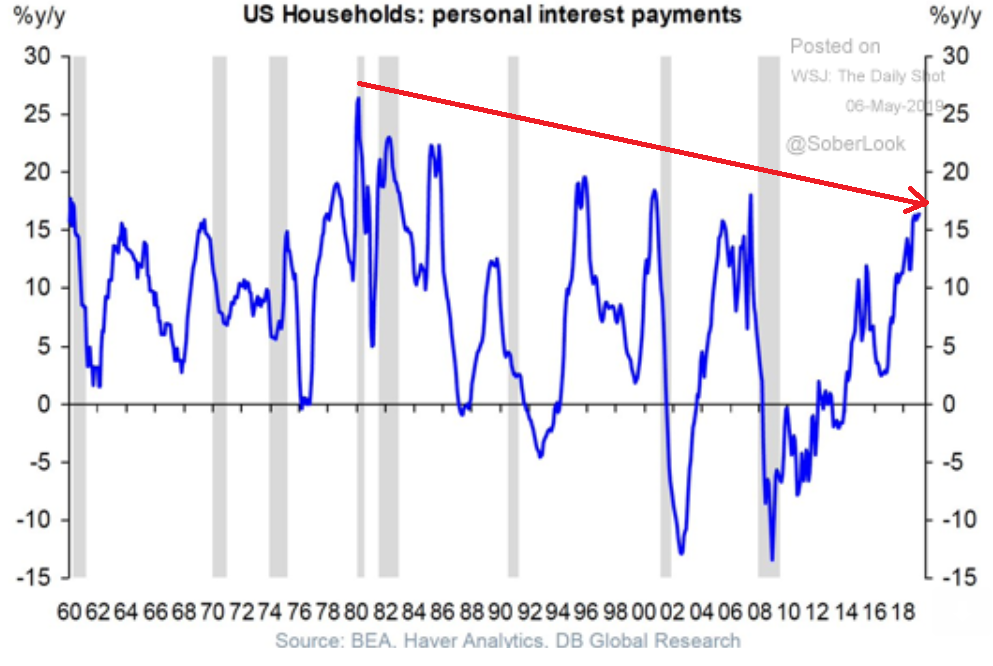

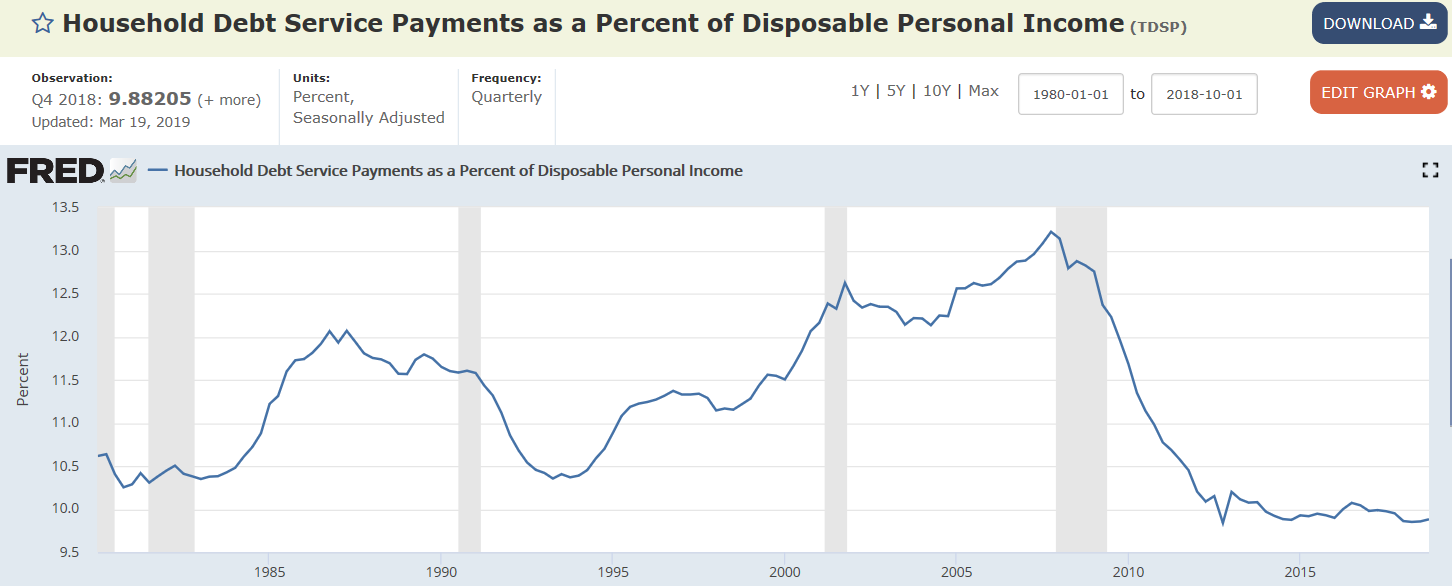

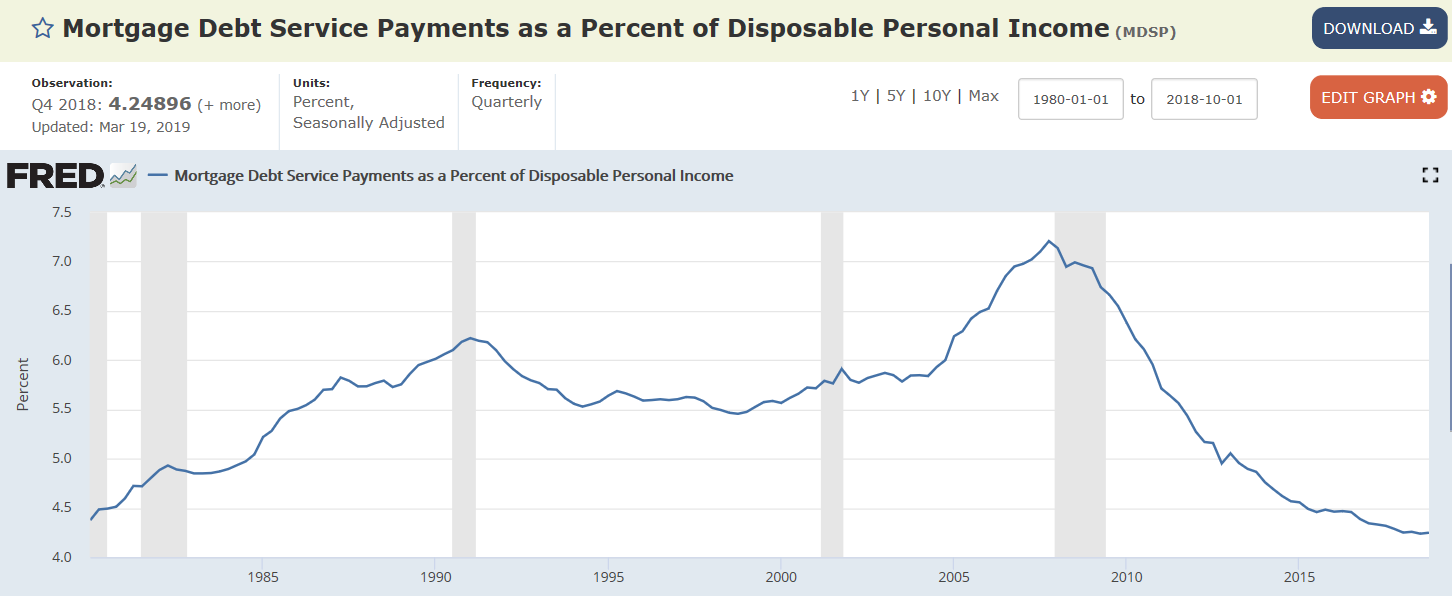

Interesting as debt service and financial burdens ratios remain historically low:

They’ve made fiscal adjustments that may be kicking in:

Bank of Japan to be top shareholder of Japan stocks

Bank of Japan to be top shareholder of Japan stocks (Nikkei) The BOJ held over 28 trillion yen ($250 billion) in exchange-traded funds as of the end of March — 4.7% of the total market capitalization of the first section of the Tokyo Stock Exchange. Assuming that the bank maintains its current target of 6 trillion yen in new purchases a year, its holdings would expand to about 40 trillion yen by the end of November 2020. This would place it above the GPIF’s TSE first-section holdings of more than 6%. The BOJ has likely also become the top shareholder in 23 companies through its ETF holdings. It was among the top 10 for 49.7% of all Tokyo-listed enterprises at the end of March.

This could explain why same store sales have been growing by about 5% year over year:

CNN: American retailers already announced 6,000 store closures this year. That’s more than all of last year.

Not looking good:

Not looking good:

In contraction:

South Korea March exports contract for fourth month

(Reuters) Overseas sales slid 8.2 percent in annual terms in March. Imports shrank by 6.7 percent in March from a year earlier. This produced a $5.22 billion trade surplus, nearly doubling the amount in February, the Korea Customs Service data showed on Monday. Analysts say the fall in exports was led by a slump in semiconductor business, the country’s key export, as well as cooling demand from China, its biggest market, amid the trade war with the United States. Bank of Korea Governor Lee Ju-yeol said last week the central bank may change its current neutral stance on monetary policy should “recovery sentiment” worsen significantly.

Trump’s Great Lakes Whoppers

Trump, March 28: I support the Great Lakes. Always have. They’re beautiful. They’re big. Very deep. Record deepness, right? And I’m going to get, in honor of my friends, full funding of $300 million for the Great Lakes Restoration Initiative, which you’ve been trying to get for over 30 years. So we’ll get it done. It’s time. It’s time. You’ve been trying to get it over 30 years. I would say it’s time, right?

In its first fiscal year, Obama recommended — and the initiative received — $475 million. After that high point, funding dropped in fiscal year 2011 to just under $300 million. And funding has stayed steady around that level ever since.

In his last two budget proposals, including the fiscal year 2020 budget released this month, Trump proposed just $30 million — the equivalent of a 90 percent cut. In his first proposed budget for fiscal year 2018, the president allotted zero funding for the program.