Slow down! We have too many cars: AutoNation CEO

Automakers should watch their bloated inventories even though 2014 seems like it will be a good year for car sales, AutoNation Chairman and CEO Mike Jackson told CNBC on Thursday.

The automakers have a “pretty bizarre” way of calculating inventories to justify these levels, he said in a “Squawk Box” interview. “But if you cut through the bogus calculations and look at dealer inventory for the Detroit 3, it’s over a 100-day supply. And it simply doesn’t need to be there.”

In response, Joe Hinrichs president of the Americas at Fordtold CNBC: “We have been cutting some production in the fourth quarter of last year and in the first quarter of this year on a couple of our product lines where we saw the inventory grow a little bit.”

But Hinrichs added, “The industry is a little different now. With our capacity running max out, we actually grow an inventory in the winter, come down in the spring and summer because we run our plants full all year round. In the old days when we had excess capacity, we’d take the plants down in the winter and work overtime in the spring/summer to supply to the demand.”

He added: “We’re watching it carefully, but I think we’re going to be OK.”

Author Archives: WARREN MOSLER

Turkey’s Prime Minister on rates and inflation

Turkey’s central bank prepared to tighten policy further

“Mr Erdogans own resistance to interest rate rises goes deep: on the flight, the prime minister insisted that, contrary to economic theory, increases in interest rates cause inflation. I believe that inflation and interest rates are not inversely proportional but in direct proportion, he told reporters. In other words, the relationship between inflation and interest is cause and effect: the interest rate is the cause, inflation is the result. If you increase the rate, inflation increases. If you reduce it, both drop together. When you think they are inversely proportional you always get much more negative results.

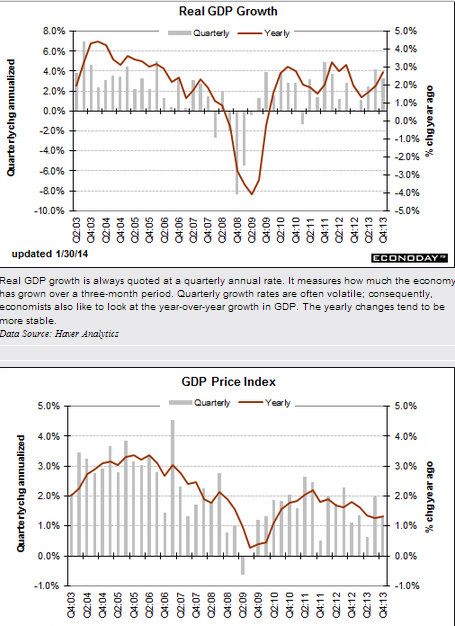

GDP and unemployment claims charts

Highlights

The economy ended the year on a moderately positive note, rising an annualized 3.2 percent in the advance estimate for the fourth quarter. This followed a 4.1 percent boost in the third quarter. The consensus expected a 3.0 percent rise in the fourth quarter.

But demand was not as strong. Final sales of domestic demand gained 2.8 percent after a 2.5 percent boost in the third quarter. Final sales to domestic purchasers slowed to 1.4 percent in the fourth quarter after a 2.3 percent increase the prior quarter. The softening was largely due to a drop in government purchases. A positive was improvement in consumer spending.

Inflation is soft with the GDP price index rising only 1.3 percent after a 2.0 percent increase in the third quarter. The core price index eased to 1.7 percent, following a 1.9 rise in the third quarter.

Highlights

A surprise 19,000 rise in initial jobless to a much higher-than-expected 348,000, together with a rising trend for continuing claims, are not pointing to much improvement for the labor market, at least for January. But a plus in the data is the 4-week average for initial claims, up only slightly to 333,000 which is more than 20,000 below the month-ago trend.

Another plus is a 16,000 dip in continuing claims to 2.991 million in data for the January 18 week. The 4-week average, however, is up sharply, 43,000 higher to 2.970 million which is the highest reading since August. The unemployment rate for insured workers, which had been as low as 2.1 percent in November, is at 2.3 percent for a 3rd straight week.

There are no special factors at play in today’s report though the latest initial claims are for the shortened Martin Luther King week which raises the risk of adjustment volatility. The Fed yesterday cited improvement underway in the labor market but its hard to find convincing proof in this report.

Growing Pains

FLASH- Fed to taper another $10 billion

Maybe they are concerned about all the interest income they are removing from the economy?

;)

General comments:

For GDP to grow at 3% all the pieces have to ‘average’ 3% growth

And if anything is growing at a slower pace than last year, something else has to grow at a faster pace or GDP growth slows.

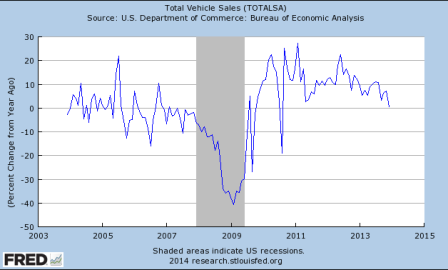

So the growth rate of car sales has slowed and is expected to slow further this year:

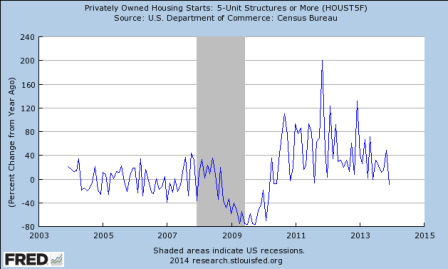

How about housing?

Pending home sales year over year change:

New mortgage applications to purchase homes:

Purchase apps year over year:

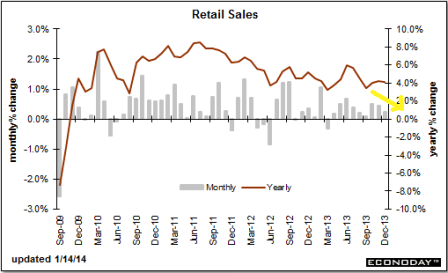

Retail sales growth has been generally slowing and has yet to show signs of increasing:

How about orders for durable goods?

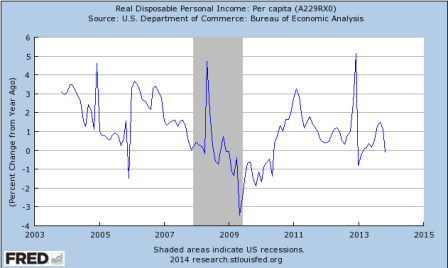

Is the income growth there to support higher levels of spending?

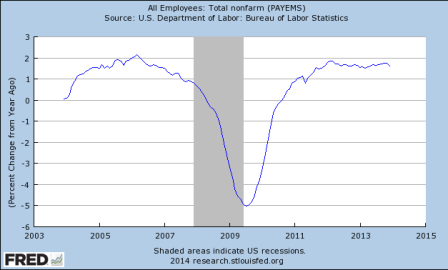

Is the growth rate of employment increasing?

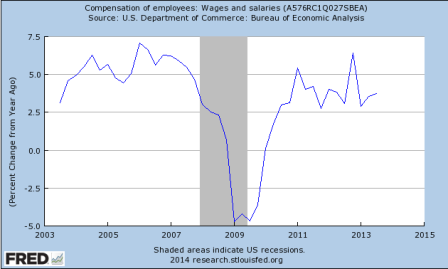

Compensation?

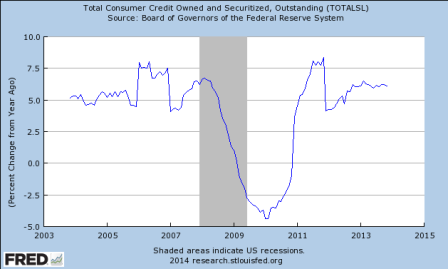

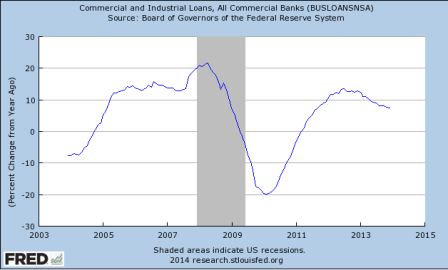

Maybe consumers are somehow borrowing to spend at a higher rate?

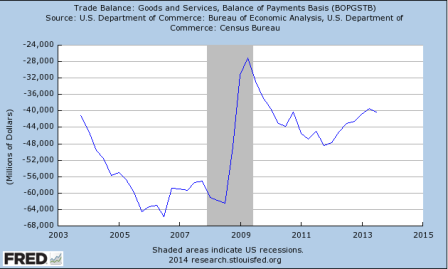

How about the foreign sector?

Well, it was helping, but we need the rate of change to increase to have more of an impact than last year. And with GDP around $17 trillion, last year’s rate of increase has to be exceed by about $7 billion/mo to add an additional .5 to GDP. And the substantial currency depreciation of the EM’s isn’t going to help any.

Just saying, something big needs to start growing a lot just to keep GDP growth positive?

So what happened to growth?

Private sector spending (including non residents) in excess of income may no longer be keeping up with the reduction in the federal govt’s spending in excess of its income (deficit spending spending)?

Maybe the federal deficit is too low for current credit and financial conditions?

Deficit as a % of GDP through Sept 13. It’s even lower currently:

Durable goods less the expected…

What a good economy should look like

What a good economy should look like

Warren Mosler, from a talk in Chianciano, Italy, on January 11, 2014 entitled Oltre L’Euro: La Sinistra. La Crisi. L’Alternativa.

What a good economy should look like

I just want to say a quick word about what a good economy is because it’s been so long since we’ve had a good economy. You’ve got to be at least as old as I am to remember it. In a good economy business competes for people. There is a shortage of people to work for business. Everybody wants to hire you. They’ll train you, whatever it takes. They hire students before they get out of school. You can change jobs if you want to because other companies are always trying to hire you. That’s the way the economy is supposed to be but that’s all turned around. For one reason, which I’ll keep coming back to, the budget deficit is too small. As soon as they started tightening up on budget deficits many years ago, we transformed from a good economy where the people were the most important thing to what I call this ‘crime against humanity’ that we have today……

So what you do is you target full employment, because that’s the kind of economy everybody wants to live in. And the right size deficit is whatever deficit corresponds to full employment…

Credentials!!!

PDF: New Credentials

ECB proposals to buy loans to households and companies

This is highly problematic.

If the ECB takes the risk, there is extreme moral hazard. If they don’t, lending won’t likely increase:

ECB poised for battle to ward off deflation

January 26 (FT) — Mario Draghi has signalled that he would be prepared for the ECB fight deflation in Europe by buying packages of bank loans to households and companies. Since the corporate bond market was small and working well, he said, there is no need to do something in that field. As the ECB does not issue debt and a decline in net lending remains a deep problem in peripheral eurozone countries, Mr Draghi said he favoured looking at a way to package bank loans to the private sector and for the ECB to buy them if economic conditions got worse. Mr Draghi said: What other assets would we buy? One thing is bank loans?.?.?.?the issue for further thinking in the future is to have an asset that would capture and package bank loans in the proper way. Right now securitisation is pretty dead, he said adding, that there was a possibility of buying asset backed securities if they were easy to understand, price and trade and rate.

State deficits turning to surplus

Just like any other agent, when they spend more than their income they are adding that much to growth, and as their deficits fall the are net adding that much less.

States Weigh New Plans for Revenue Windfalls

By Mark Peters

January 26 (WSJ) — Governors across the U.S. are proposing tax cuts, increases in school spending and college-tuition freezes. The strengthening in tax revenue started in late 2012 as higher-income residents in many states took increased capital gains among other steps to avoid rising federal tax rates on certain income. Those tax payments spilled over into 2013, and further fuel for collections came from a record stock market and improving economy. State tax revenue nationally climbed 6.7% in the fiscal year ended June 30, 2013, Moody’s Analytics says. Still, state spending last year remained below peak levels in 2008 when adjusted for inflation, while state reserves hit their highest level since the recession, reaching a total of $67 billion nationally, or 9.6% of state spending, according to a report last month from the National Association of State Budget Officers.

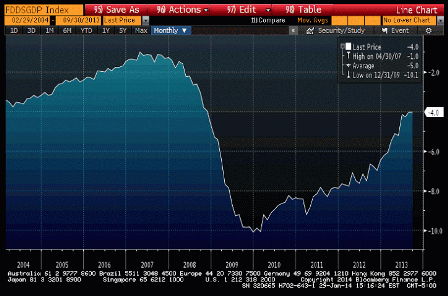

Interest rates and consumption

Who would have thought?

;)

Thanks Art.

The equation at the core of modern macro

By Noah Smith

“…the Euler Equation says that if interest rates are high, you put off consumption more. That makes sense, right? Money markets basically pay you not to consume today. The more they pay you, the more you should keep your money in the money market and wait to consume until tomorrow. But what Canzoneri et al. show is that this is not how people behave. The times when interest rates are high are times when people tend to be consuming more, not less.”