Author Archives: WARREN MOSLER

Jobs, Philly Fed

This tick up might mean nothing,

but could also be the start of a move up due to the fall off in oil capital expenditures:

Jobless Claims

Highlights

Jobless claims jumped sharply in the January 10 week, up 19,000 to a 316,000 level that’s the highest since September. The 4-week average is up 6,750 to 298,000 which is about even with the month-ago comparison.

This tick down might mean nothing, but could also be the start of a move down due to the fall off in oil capital expenditures:

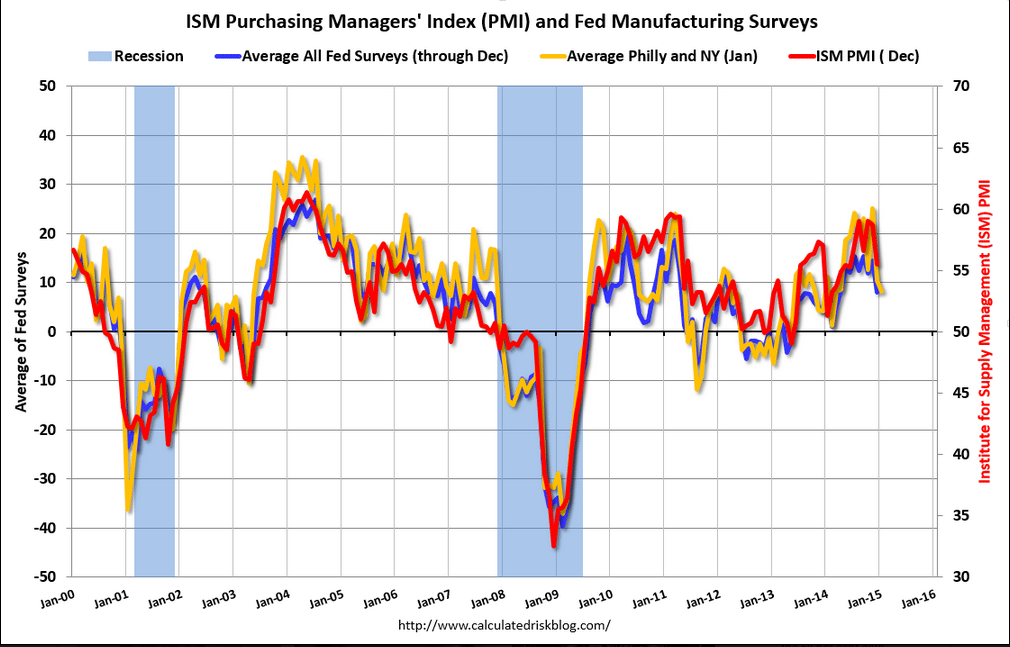

Philadelphia Fed Survey

Highlights

Abrupt slowing is the signal from the manufacturing report of the Philly Fed whose general conditions index for January fell to plus 6.3 from December’s plus 24.3 (revised from 24.5). Growth in new orders, however, does remain solid at plus 8.5 though down from December’s plus 13.6. The 6-month general outlook also is a positive, at a very strong 50.9 vs December’s 50.4.

Now the weak readings led by shipments, which are in contraction at minus 6.9 vs December’s plus 15.1, and employment, now also in contraction at minus 2.0 vs December’s plus 8.4. Unfilled orders also are in the negative column, at minus 8.6 vs plus 2.7 in December. Price readings are soft with input price inflation moderating further and output prices now in modest contraction.

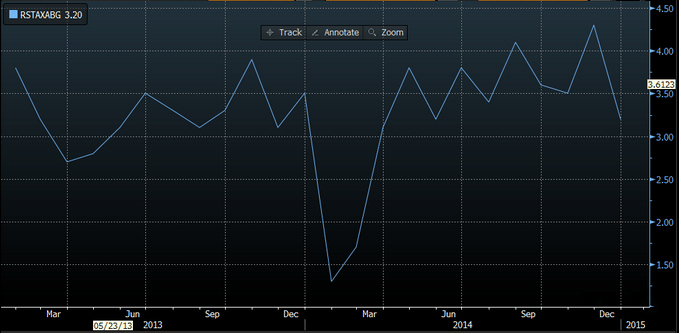

Empire did a bit better.

This came out before the Philly Fed 6.3 print so add that last data point to the red line on the chart:

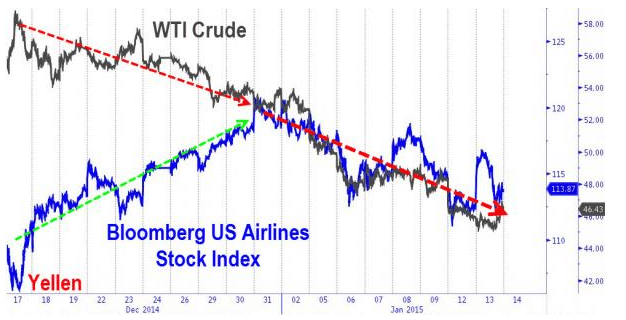

retail sales, import and export prices, business inventories, airline stocks, ECB QE comment

This is not supposed to happen with falling gas prices…

Retail Sales

Highlights

Retail sales disappointed for December. Retail sales in December fell 0.9 percent after posting a 0.4 percent gain in November and a 0.3 percent rise in October. Expectations were for a 0.1 percent decline. The December decrease is the largest negative since January 2014. Both November and October were revised down. Excluding autos, sales decreased 1.0 percent after rising 0.1 percent in November. Analysts expected a 0.1 percent decrease. Excluding both autos and gasoline sales declined 0.3 percent after advancing 0.6 percent in November. Expectations were for a 0.6 percent boost.

The motor vehicle component was weak as expected from the unit new auto sales report. Motor vehicles dipped 0.7 percent in December, following a 1.6 percent gain the month before. Gasoline station sales fell again on lower prices. Sales dropped a sharp 6.5 percent after a 3.0 percent drop in November.

Within the core weakness was broad based, led by miscellaneous store retailers (down 1.9 percent), building materials & garden supplies (down 1.9 percent), electronics & appliance (down 1.6), and general merchandise (down 0.9 percent). Notable gains were seen in furniture & home furnishings (up 0.8 percent) and food services & drinking places (up 0.8 percent).

Today’s retail sales report is a surprise on the downside. But it also is a quandary. Consumer confidence is up and discretionary income is up with gasoline prices down. It is possible that more money is going to services which do not show up in the retail sales report. Probably the biggest positive in the report is the boost in food services & drinking places which is a very discretionary spending item-suggesting a positive mood for the consumer. But looking at the numbers technically, fourth quarter GDP forecasts likely are being shaved.

‘Control Group’: Retail Sales ex food, gas, building materials, auto dealers:

Retail Sales decreased 0.9% in December

The decrease in December was well below consensus expectations of a 0.1% decrease. Both October and November were revised down.

This was a weak report even after removing the impact of lower gasoline prices.

Import and Export prices:

For November:

Airlines not flying as high as expected either:

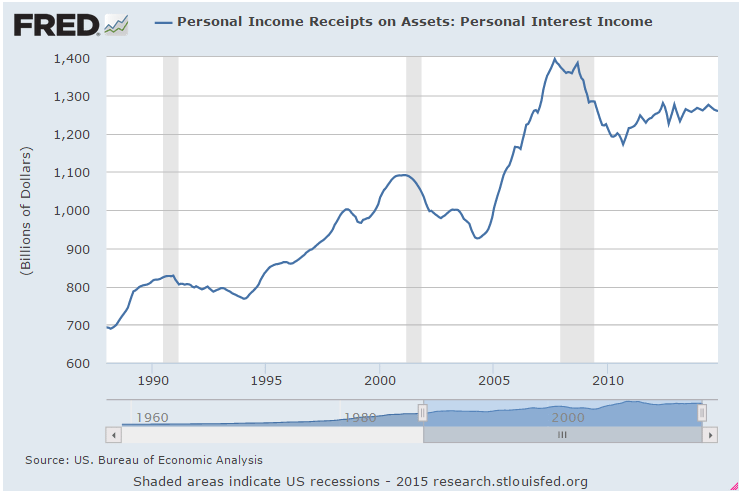

a couple of ramifications of the 0 rate policy

This traditional source of total personal income growth hasn’t been there this time around due to Fed

‘easing’. The economy is a net receiver of interest, the govt. a net payer:

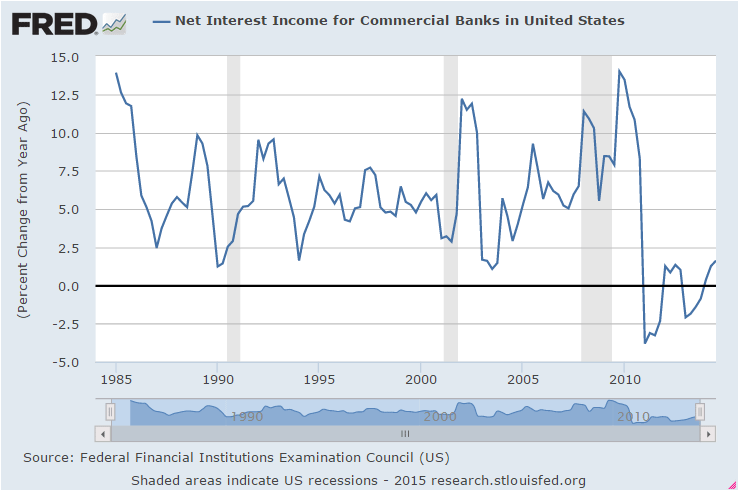

And net interest income hasn’t been growing much for banks, for example:

Brazil inflation

Maybe somehow the higher interest rates set by the CB support the higher rates of inflation?

;)

Brazil’s Inflation Rises Even Amid Low Growth (WSJ) Brazil’s official IPCA consumer-price index rose 6.41% in 2014. The IPCA rose 5.91% in 2013. Annual inflation was driven up by an 8% increase in food prices and a 8.8% surge in housing-related prices. Inflation also accelerated in December, with the IPCA rising 0.78% versus 0.51% rise in November. The central bank raised its benchmark interest rate, called Selic, to 11.75% in December, the latest in a series of increases since April 2013, when the rate was 7.25%. The Central Bank of Brazil has a tolerance band for annual inflation of between 2.5% and 6.5%.

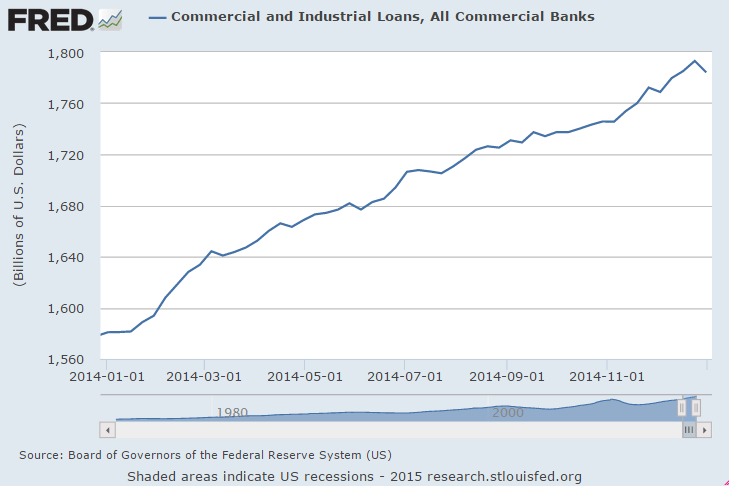

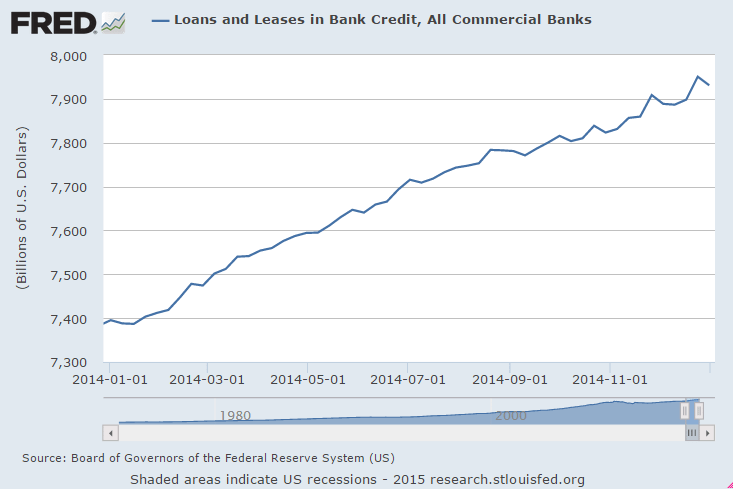

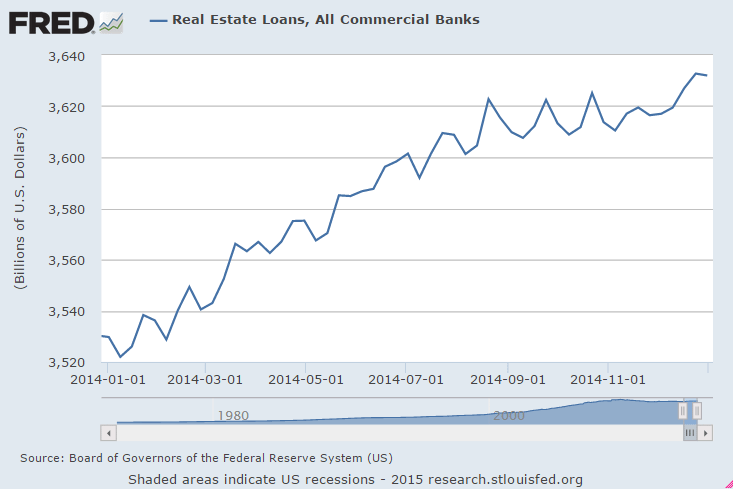

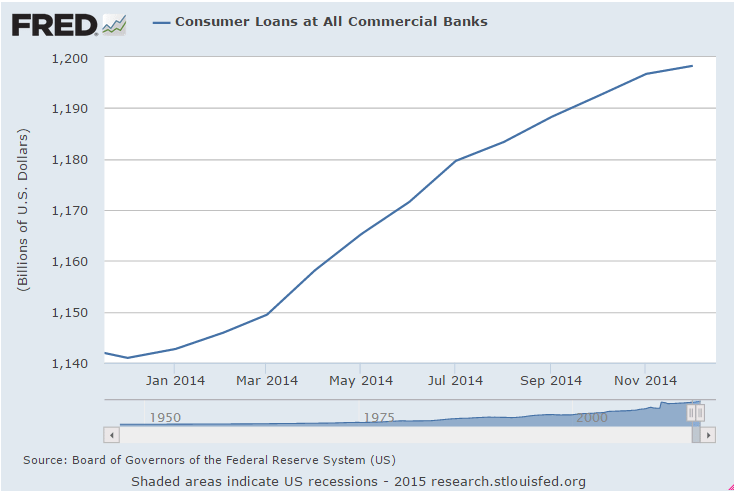

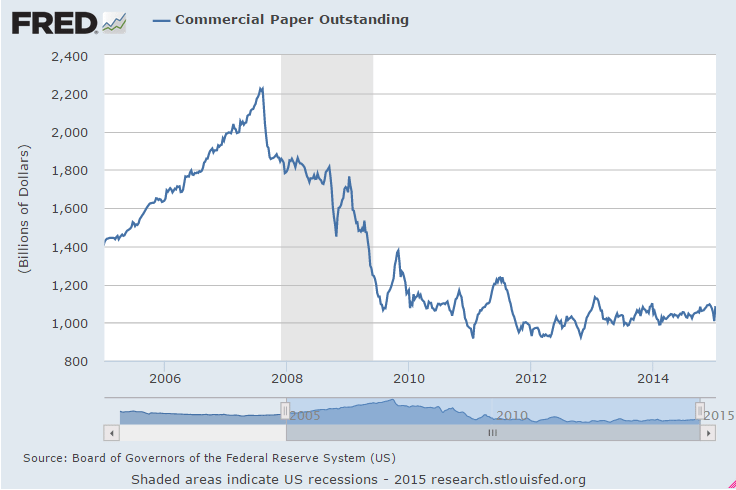

credit check

Still no sign of any kind of credit boom underway here.

Loans zigged down a bit and commercial paper zigged up a bit:

Kelton story in Forbes, attribution

Confused, of course, but in the news!

Watch Out, MMT’s About, As Bernie Sanders Hires Stephanie Kelton

By Tom Worstall

Jan 12 (Forbes) — The idea that Modern Monetary Theory might actually become vaguely mainstream, even an influence on how the Republic is governed, entirely petrifies me. It’s not actually that I disagree very much with the economics that is being laid out in MMT: indeed, I’m terribly tempted to agree that they’re actually correct in much of what they say. Rather, it’s what it will do to the political process if they do gain real policy influence. For at present there does have to be some link, however vague or tenuous, between how much money the government takes in from all of us and how much money the government spends on giving prizes to all. The basic innovation of MMT is to point out that this no longer has to be so: and that’s simply not a tool that I want politicians of any stripe to have available to them.Dylan Matthews has the story that has me hot and bothered:

President Obama’s biggest problem in the Senate is obviously its new Republican majority, but opposition from the left wing of the Democratic caucus appears to be growing too. Most prominently, Sen. Elizabeth Warren (D-MA) has clashed with the White House on a key Treasury Department position and the CRomnibus spending package. But new budget committee ranking member Sen. Bernie Sanders (I-VT) is poised to break dramatically from traditional Democratic views on budgeting, from Obama to Clinton to Walter Mondale and beyond.

His big move: naming University of Missouri – Kansas City professor Stephanie Kelton as his chief economist. Kelton is not exactly a household name, but to those who follow economic policy debates closely, tapping her is a dramatic sign.If you want all of the grubby details of MMT then I recommend that piece and those it links to. I’ll just give a pencil sketch here.

It’s most certainly not obvious that MMT proponents are all barking mad or anything. Jamie Galbraith (who I’ve had one or two very limited interactions with) is certainly a reasonable guy. And his insistence that a budget surplus, despite the ribbing he gets about it, is in fact economically contractionary doesn’t seem to have anything wrong with it. Budget deficits are fiscally expansive, a surplus is fiscally contractionary, if there’s any one statement at the heart of Keynesianism that’s it. I might differ on the desirability of a surplus at times but not on that basic point about one being contractionary. My disagreement being that the old standard Keynesianism was based on the idea that at times we want the government to be contractionary. Not as a means of paying down the debt or anything but as just general good management of the economy. Sure, let’s add to aggregate demand in a slump but the flip side of that coin is that in the boom we want to temper things. Just as the old complaint about central banking goes (“the central banker’s job is to remove the punch bowl just as the party gets going” by raising interest rates) a budget surplus is the fiscal equivalent, just part of moderating both the booms and busts to which capitalism is prone.

So I’m certainly not thinking that the MMTers are over there with David Icke and whispering about the Grey Aliens or anything.

And their basic outline about money creation is true as far as I can see. If you’re a country with your own central bank you can print as much money as you like. And sure, you could indeed finance government just by printing more money. Print money, spend it, hey presto, you’ve financed government. Standard monetary theory also recognises this: we know that the Fed makes a pretty profit each year from printing Benjamins (20 cents of paper and 3 cents of ink really is worth $100 these days) and that’s worth perhaps $20 billion a year to the US government in seignorage. We really don’t complain about it either. That standard monetary theory then also says that doing too much of this (in more detail, printing or creating lots of base money, rather than the creation of credit in the manner that the banking system does) will be highly inflationary. Standard theory points to Wiemar Germany, post WWII Hungary and modern Zimbabwe as examples (that last so fun that the end series of banknotes were only printed on one side as they didn’t have enough “real money” left to buy ink).

At which point the MMT crowd say ah, but yes, that’s what taxes are for. Print the money, spend it, thereby injecting it into the economy, and if inflation rises then taxes are what sucks that money back out of the economy and thus kills off the inflation. And it’s that bit that absolutely terrifies me. The effect that idea has on the incentives for politicians.

Given that we are discussing monetary policy it seems appropriate to bring Milton Friedman in here. And he pointed out that if you ever have a chance to cut taxes just do so. On the basis that politicians, any group of politicians, will spend the bottom out of the Treasury and more however much there is. So, the only way to stop ever increasing amounts of the the entire economy flowing through government is simply to constrain the resources they can get their sticky little mits on. We could, for example, possibly imagine a Republican from the Neanderthal wing of the party arguing that what the US really needs is another 7 carrier battle groups. And one from the even more confused than usual Progressive end of the Democratic Party arguing that each college student needs her own personal carrier battle group to protect her from the microaggressions of being asked out for a coffee. You know. Sometime. Maybe. If you want to?

A Mea Culpa and Some Comments on MMT and Fiat Currency Economics

By Warwick Smith

Jan 12 — It has recently been pointed out to me that some of my writing on monetary economics has not given proper attribution to the intellectual tradition behind the ideas that I present and that this gives the impression that these are my ideas. I’m embarrassed to admit that the criticisms are spot on and I have made a major misjudgement in how I wrote these articles (one in The Conversation and one in The Guardian). I had no intention of stealing other peoples ideas but, nevertheless, this is in effect what I did. I apologise unreservedly to those who may have felt aggrieved by my actions.

I have a history in public policy activism and I have approached my recent popular political and economic writing somewhat from an activist standpoint where I viewed the main game as advocating and causing public policy change and increasing public awareness. The branch of monetary economics known as modern monetary theory (MMT) has something of an activist element to it where a minority who hold an accurate view of how things are and, perhaps to a lesser extent, how things should be, are vying for airtime against the overwhelming majority who hold (or at least communicate) a false perspective on monetary economics and public finance.

I thought that I could add a new voice and a new strategy to that struggle by simply writing about monetary economics from an MMT perspective but as if it’s just the uncontroversial (among economists) truth about monetary economics rather than a minority view among economists. I think the complexities of intra-discipline disagreement are impenetrable for newcomers and will put most people off investing the effort to understand the arguments.

Taking this line of thinking led me to make a serious misjudgement in what I wrote and how I wrote it because MMT is more an intellectual and academic discipline than it is an activist movement and, as such, people’s careers and their professional profiles are at stake. Again, I apologise to the people whose work has inspired some of my writing who have not been properly acknowledged including Warren Mosler, Perry Mehrling, Bill Mitchell and Steven Hail.

I wrote to the Guardian editors requesting a couple of additions. They agreed to add attribution to a line early in the article that credits Warren Mosler but not to make further edits post-publication. I’m a strong believer in owning up to mistakes and trying to remedy them when others are affected.

I believe MMT faces serious challenges in part because of its name and the way it is usually presented. A better name would be something like Fiat Currency Economics because MMT is not a theory but is primarily just a description of reality and the clear consequences that flow from that reality. No economist that I’ve found has any clear and well reasoned refutation of MMT to offer. All attempts at refutation appear to rely on misunderstandings or misrepresentations. This is why I took the approach of not referring to MMT at all in the pieces that I wrote. Nevertheless, I still should have referred to the people whose work contributed to or provided the ideas for the articles and I greatly regret that I did not. I promise I will not make this mistake again.

Below is a list in rough descending order of significance with respect to influencing my views on monetary economics.

Perry Mehrling’s Coursera course The Economics of Money and Banking

Warren Mosler’s book The Seven Deadly Frauds of Economic Policy

Various presentation given by Steven Hail

University of Newcastle’s CofFEE report on the Job Guarantee

Professor Bill Mitchell’s blog – this is the most comprehensive of the sources here but it’s low on my list because I came to it quite late in the formative period of my thinking on money and finance.

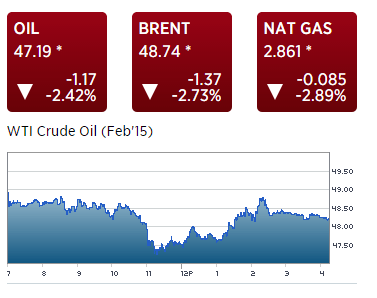

Oil, natural gas

The narrowing spread between West Texas and Brent leads me to suspect US production is slowing:

Also seems natural gas prices should be going up as shale drilling slows? Less drilling means less natural gas byproduct means tighter supplies, no?

Slowing oil production just means more imports at the same price, but we don’t import nat gas, so slowing production means shortage?

Stephanie Kelton getting serious attention

Jobs, Wages, Wholesale trade

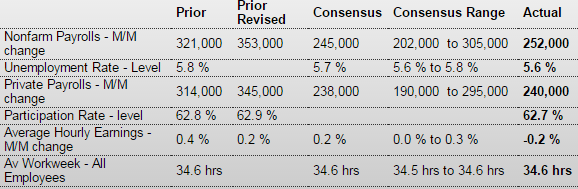

Employment Situation

Highlights

The December employment situation was somewhat stronger than expected at the headline level but the payroll numbers softened. In terms of actual numbers, the report was mixed.

Payroll jobs advanced 252,000 after jumping a revised 353,000 in November. Analysts projected a 245,000 gain. October and November were revised up notably by a net 50,000. The unemployment rate decreased to 5.6 percent from 5.8 percent in November. Expectations were for 5.7 percent. Wages actually fell back for the latest month.

Going back to the payroll report, private payrolls increased 240,000 after rising 345,000 in November. Expectations were for 238,000.

Goods-producing jobs jumped in December, led by construction which advanced 67,000 in December after a 20,000 increase the month before. Manufacturing employment increased 17,000, following a jump of 29,000 in November. Mining rose 3,000 in December, following a 1,000 boost the prior month.

Private service-providing jobs gained 173,000 after a 294,000 jump in October. The latest increase was led by professional & business services. Government jobs increased 12,000 after rising 8,000 in November.

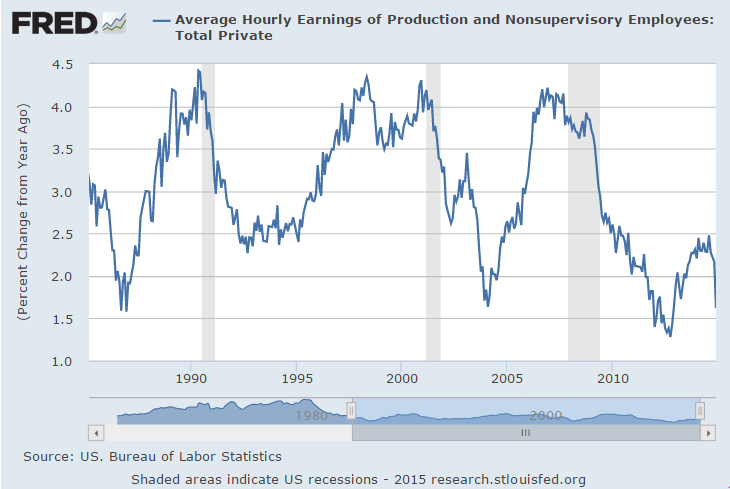

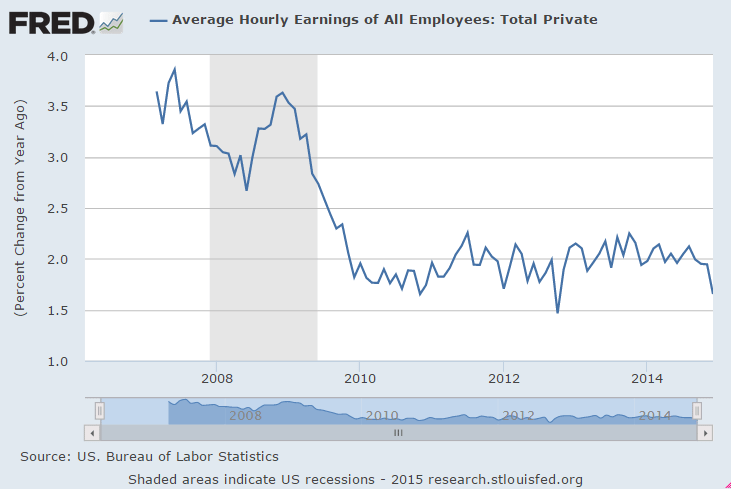

Average hourly earnings slipped 0.2 percent in December after gaining 0.2 percent the prior month. Expectations were for a 0.2 percent rise. Average weekly hours were unchanged at 34.6 hours and matched expectations.

The December jobs report was mixed. Payroll gains beat expectations but slowed from November. Wage growth softened. The unemployment rate dipped but partially on a lower participation rate. Still, the labor market is showing overall improvement. However, today’s numbers will only increase debate within the Fed on just how strong or soft the labor market really is.

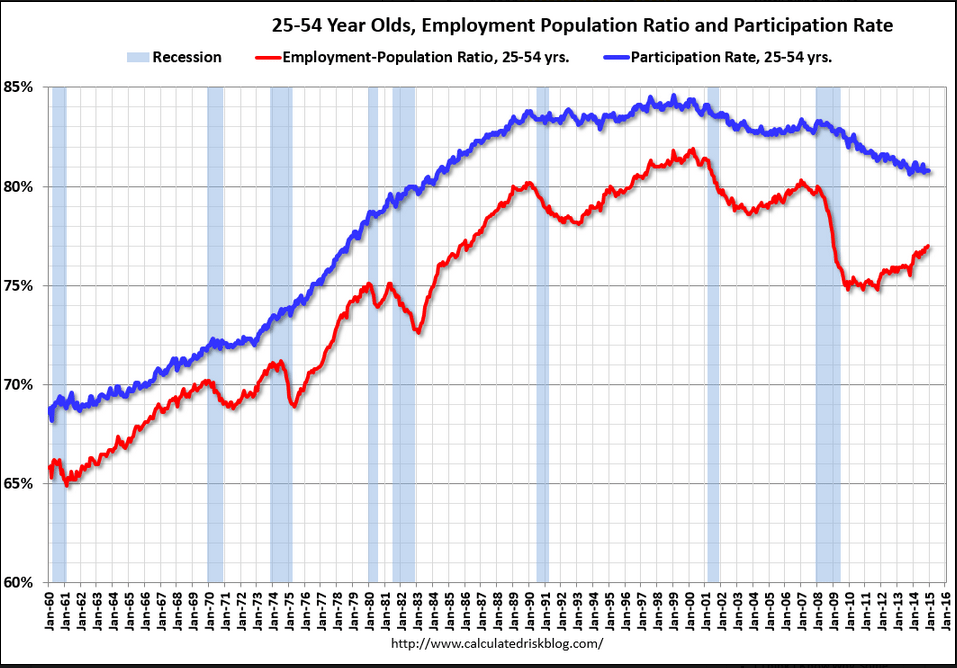

This chart takes out the ‘demographics’ by looking only at 24-55 year old Americans.

It shows how ‘the problem’ remains a massive shortage of aggregate demand:

Not long ago the mainstream raised the alarm that average hourly earnings were ‘accelerating’ and when this happens it doesn’t stop for an average of 4 years, so the Fed better hike now to avoid a serious inflation problem. When I suggested it might roll over this time as it did in 2003, that notions was immediately dismissed:

Maybe higher paying energy jobs being replaced with lower paying fast food, retail, education, and healthcare types of jobs?

Wholesale Trade

Inventories look a bit heavy in the wholesale sector, up 0.8 percent in November vs a 0.3 percent decline in sales that lifts the stock-to-sales ratio to 1.21 from October’s 1.20 and compared to 1.19 in September. Weak sales made for unwanted inventory builds in metals, chemicals, lumber, machinery and farm products.

The nation’s inventories have been steady though today’s report does hint at slowing demand going into year end. Watch for the final data on November inventories in Wednesday’s business inventories report.

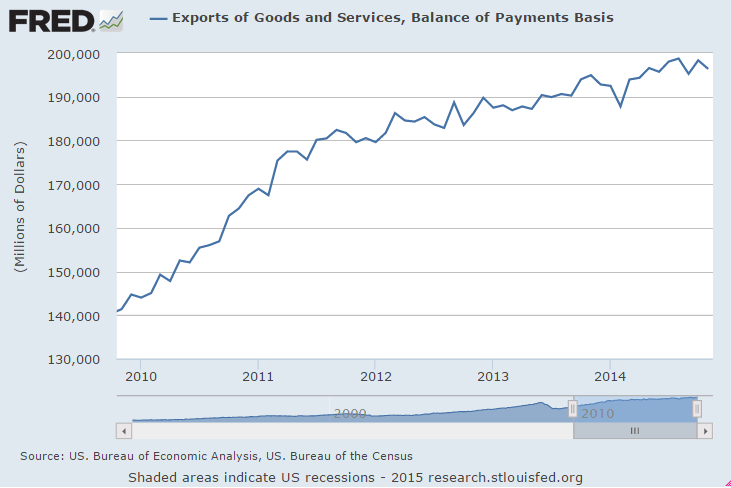

I’m suspecting US exports are in the process of declining due to the lower oil price and the weak global economy. Oil producers both have less to spend due to falling revenues and they will also reduce capital expenditures that are no longer profitable.

And while ‘global consumers’ will have more to spend due to falling fuel costs, seems to me that nations other than the US will benefit from that type of spending.

You can see how US exports have rolled over recently:

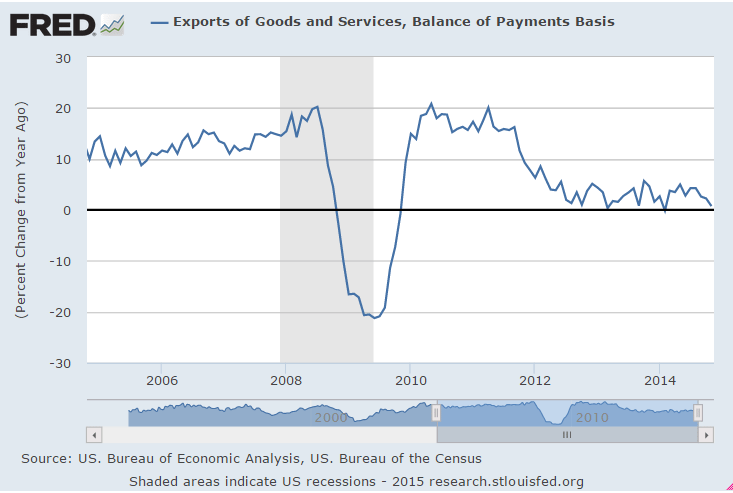

Year over year growth is now near 0:

To the point of ‘bad inflation’ in Japan:

Japanese People Feel Their Lives Are Worse Off

Jan 8 (WSJ) — A Bank of Japan survey of more than 2,000 people found that falling real incomes and rising prices have made people feel worse off than at any time in the past three years. About 51% said the comfort of their life has diminished over the past year, while just 4% felt life was getting better. The differential, about 47 percentage points, was the worst level since December 2011, the central bank said. Respondents to the survey also tended to be pessimistic about the year ahead. Nearly 38% said they thought the economy would get worse over the next year. In the previous poll, taken in September 2014, only about 32% thought that. And more than half of respondents said they believed growth in the future would be lower than it is now.