This plays to investors who think a drop in govt spending is good for the private sector as it ‘gets govt out of the way’ and ‘opens the door’ for that much more private sector growth in short order.

While this could be sort of but not necessarily true at full employment, it is of course not true in any case with with today’s excess capacity.

Seems they forget that today, cuts in govt spending immediately translate into cuts in private sector sales, which are the driver of private sector output and employment.

Yes, private sector credit expansion has (had?) begun to ‘kick in’, somewhat more than replacing the decline in govt deficit spending from the ‘automatic fiscal stabilizers’ of slowing transfer payments and rising revenues from higher incomes. The causation was from more ‘borrowing to spend’ in the economy to less deficit spending.

And that all can accelerate and continue for many years before, left alone, the deficit gets too small (and shrinking) to support the growing private sector credit expansion, as it all becomes unsustainable and implodes.

But at any point during that credit expansion, a pro active dose of govt deficit reduction can remove sufficient income to restrict the private sector’s credit expansion. People who may have borrowed to buy a house or a car, for example, suddenly losing their jobs and those purchases not happening, etc.

So the idea that 3% GDP is a ‘given’ due to private sector credit expansion and therefore a proactive tax hike and spending cut of maybe 1.25% of GDP will lower that to 1.75% growth misses that dynamic, as it presumes the proactive fiscal adjustments don’t throw a monkey wrench into the credit expansion dynamics. Like what’s been happening in the euro zone.

—– Original Message —–

At: Apr 26 2013 07:39:34

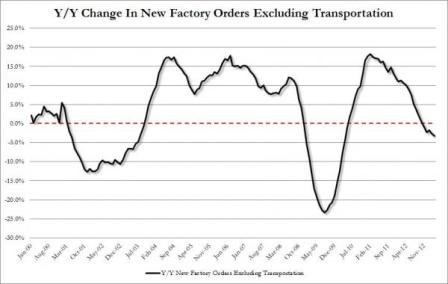

The miss was mostly a result of government declining, again. This is really the surprise. Trade was also a drag, but from a surprise perspective government is the winner. In all, gov subtracted a chunky 0.8ppts from the topline – meaning if you add it back Q1 would have printed 3.3%.

Having said that, this a rearview mirror report and what we already know about the handoff to Q2 is that it was weak. Indeed, we are looking for a rather paltry 1% outcome here in Q2.

Finally, in terms of today’s report, no underlying detail is inconsistent with our thinking about the handoff to Q2.