So some was gross, not net, and some unspent:

Nomura: Asia Insights: China: Why GDP growth has weakened despite strong credit growth

- Economic growth in China has weakened surprisingly despite rapid credit growth in H2 2012 and Q1 2013.

- We believe a large part of the new credit supply in Q1 did not go into the real economy. For example, at least 20% of urban construction bond issuance was used to pay off expiring bank loans.

- Recent policy signals suggest credit growth will slow in Q2. We reiterate our view that economic growth will slow in Q2, while the market consensus expects a rebound.

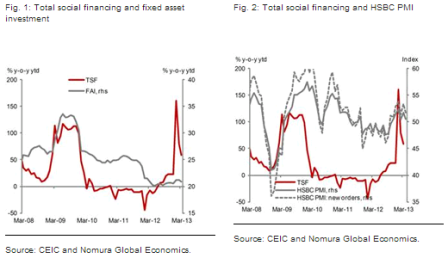

We had expected economic growth in China to rise in Q1 because of very strong credit growth, but GDP growth surprisingly slowed to 7.7% from 7.9% in Q4 2012, and economic activity in Q2 has started on a weak note. This is very different to what happened in 2009, when growth in total social financing picked up from 26.6% y-o-y in Q4 2008 to 114% in Q1 2009 and 121% in Q2 2009, growth in fixed asset investment moved up from 26.8% y-o-y in Q4 2008 to 28.6% in Q1 2009, the HSBC PMI rose to 44.8 from 40.9, and the new orders component in the HSBC PMI jumped to 43.6 from 36.1 (Figures 1, 2 and 3).

But in 2013 it is a very different story. Total social financing rose to an historical high and jumped by 160.6% y-o-y in January and by 58.2% y-o-y in Q1, but fixed asset investment (FAI) growth only picked up slightly to 21.2% y-o-y in January and February, and then slowed to 20.9% in March. GDP growth slowed to 7.7% y-o-y in Q1. The flash HSBC PMI weakened in April despite favorable seasonal factors it has only dropped once in April once during the past seven years. The new orders component of the flash HSBC PMI has dropped as well.

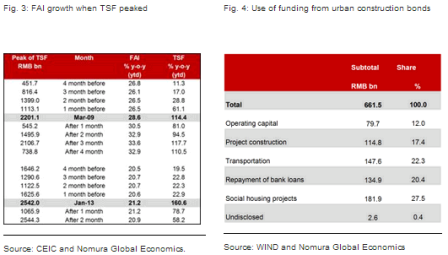

Many investors ask us the same question: where has all the money gone? We believe a large part of the new credit supply in Q1 did not go into the real economy. We do not have comprehensive information, but we provide the following two pieces of evidence. First, we collected public information on the 370 largest issues of urban construction debt that took place in 2012, and found that at least 20% of the money raised was used to repay debt (Figure 4). It is not surprising to us as many infrastructure investments projects are not yet profitable. Therefore, local government financing vehicles need to continue borrowing new funds for debt financing.

Another piece of evidence comes from a recent government policy announcement. According to a Chinese newspaper, First Financial Daily, the National Development and Reform Commission (NDRC) issued a policy notice at the end of March to ensure the funds raised for public housing construction in the bond market are not used for other purposes. We believe this policy may be triggered by cases where some funds were misused. Indeed, risks of such events have been mentioned repeatedly in government documents.

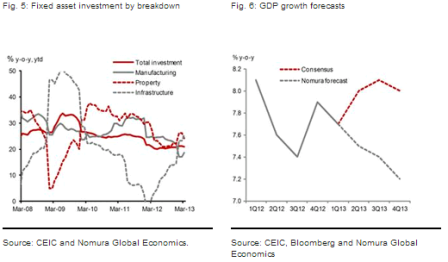

Why didnt money flow into the real economy? We think it is partly because the underlying demand for investment is weak. FAI growth for the manufacturing industry has been on a downward trend since 2011 and dropped sharply in Q1 2013 despite strong infrastructure FAI growth, which should have generated some positive spillover effects for manufacturers (Figure 5). The over-capacity problem in the manufacturing industry has been exacerbated by aggressive policy easing in 2009 and 2012.

We reiterate our view that economic growth will slow to 7.5% in Q2 as credit growth weakens (Figure 6). The consensus expects growth to recover to 8% in Q2, but recent policy signals suggest policy tightening has started and will adversely affect growth. In particular, the government has investigated several high profile corruption cases in the bond market in the past few days, and the Peoples Bank of China held a meeting on 24 April with commercial banks to clean up irregular activities in the bond market, according to a Chinese newspaper Economic Information. This initiative will likely lead to a slowdown in bond issuance and growth in total social financing in the coming months.

Full size image

Full size image

Full size image