Karim writes:

- Very substantive speech from Bernanke

- Message is basically, ‘growth has slowed more than we expected’ BUT ‘conditions are ALREADY in place for a pick-up’ and if we are wrong, we are ready to take action, which contrary to some perceptions, will be effective

Yes, contrary to my opinion. This about managing expectations. With falling inflation and unemployment this high it makes no sense that they would be holding back something that could make a material difference.

- To me, they lay out very credible factors for a pick-up in growth.

Agreed.

- The risk of either an undesirable rise in inflation or of significant further disinflation seems low-THIS LINE ARGUES AGAINST ANY NEAR-TERM ACTION

Again, if they did have anything that would substantially increase agg demand they’d have done it.

- When listing available options for further action if needed, he clearly favors further ‘credit easing’ relative to the other choices. He states why they reinvested in USTs vs MBS.

Yes, and, again, it’s doubtful lower credit spreads will do much for the macro economy but would shift a lot of credit risks to the Fed for very little gain.

- Selected excerpts in italics, with key comments in bold.

At best, though, fiscal impetus and the inventory cycle can drive recovery only temporarily.

That is not correct. Fiscal adjustment can sustain demand at any politically desired level.

For a sustained expansion to take hold, growth in private final demand–notably, consumer spending and business fixed investment–must ultimately take the lead. On the whole, in the United States, that critical handoff appears to be under way.

Agreed that hand off is slowly materializing and private sector debt expansion will then drive additional growth. But sustained expansion could come immediately from a fiscal adjustment as well.

However,although private final demand, output, and employment have indeed been growing for more than a year, the pace of that growth recently appears somewhat less vigorous than we expected.

Agreed.

Among the most notable results to emerge from the recent revision of the U.S. national income data is that, in recent quarters, household saving has been higher than we thought–averaging near 6 percent of disposable income rather than 4 percent, as the earlier data showed.

Non govt net savings of financial assets = govt deficit spending by identity, and with foreign sector savings relatively constant, the majority of the increase is in the domestic economy, either businesses or households.

That means in general household savings goes up with the deficit regardless of the level of consumer spending.

However, when household savings does start to fall, it’s due to household credit expansion, at which time, if the deficit is unchanged, the savings of financial assets is shifted to either the business or the foreign sector.

And, as growth accelerates, the automatic fiscal stabilizers- increased federal revenues and falling transfer payments- reduce the deficit and therefore reduce the growth in the total net savings of the other sectors.

So the hand off process is usually characterized by the federal deficit falling as private sector debt expands to ‘replace it.’

This continues until the private sector again necessarily gets over leveraged, ending the expansion.

3 On the one hand, this finding suggests that households, collectively, are even more cautious about the economic outlook and their own prospects than we previously believed.

At best his means that he thinks with this much savings households would start leveraging more.

But on the other hand, the upward revision to the saving rate also implies greater progress in the repair of household balance sheets. Stronger balance sheets should in turn allow households to increase their spending more rapidly as credit conditions ease and the overall economy improves.

Yes, as I explained. He seems to understand the sequence of the data but doesn’t seem to be quite there on the causation.

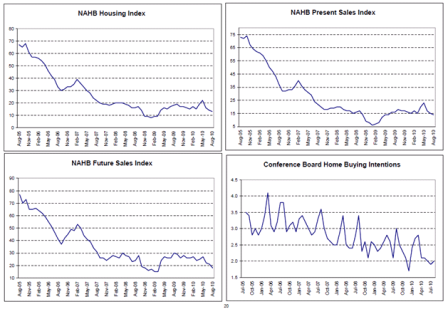

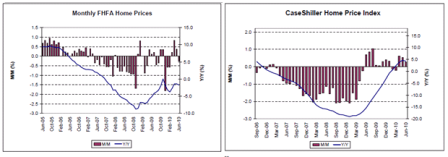

Going forward, improved affordability–the result of lower house prices and record-low mortgage rates–should boost the demand for housing. However, the overhang of foreclosed-upon and vacant housing and the difficulties of many households in obtaining mortgage financing are likely to continue to weigh on the pace of residential investment for some time yet

Yes, which is a traditional source of private sector credit expansion, along with cars, that drives the process.

Generally speaking, large firms in good financial condition can obtain credit easily and on favorable terms; moreover, many large firms are holding exceptionally large amounts of cash on their balance sheets. For these firms, willingness to expand–and, in particular, to add permanent employees–depends primarily on expected increases in demand for their products, not on financing costs.

I couldn’t agree more!

Employment is primarily a function of sales as discussed in prior posts.

Bank-dependent smaller firms, by contrast, have faced significantly greater problems obtaining credit, according to surveys and anecdotes. The Federal Reserve, together with other regulators, has been engaged in significant efforts to improve the credit environment for small businesses. For example, through the provision of specific guidance and extensive examiner training, we are working to help banks strike a good balance between appropriate prudence and reasonable willingness to make loans to creditworthy borrowers. We have also engaged in extensive outreach efforts to banks and small businesses. There is some hopeful news on this front: For the most part, bank lending terms and conditions appear to be stabilizing and are even beginning to ease in some cases, and banks reportedly have become more proactive in seeking out creditworthy borrowers.

Another problem is that the regulators are forcing small banks to reduce what’s called ‘non core funding’ in a confused strategy to enhance small bank ‘deposit stability.’ Unfortunately, at the local level the regulators have interpreted the rules to mean, for example, it’s better for a small bank’s financial stability to fund, for example, a 3 year business loan with 1 year local deposits, vs funding it with a 5 year advance from the Federal Home loan bank. It’s also a fallacy of composition, as at the macro level there aren’t enough core deposits to fund local small businesses, as many larger corporations and individuals use money center banks and leave their deposits with them. The regulatory insistence on small banks using ‘core deposits’ rather than ‘wholesale funding’ recycled from the larger banks causes a shortage of local deposits and forces the small banks to pay substantially higher rates as they compete with each other for funding artificially limited by regulation.

In lieu of adding permanent workers, some firms have increased labor input by increasing workweeks, offering full-time work to part-time workers, and making extensive use of temporary workers.

Yes, and when you include this growth in employment the economy is doing better than most analysts seem to think.

Like others, we were surprised by the sharp deterioration in the U.S. trade balance in the second quarter. However, that deterioration seems to have reflected a number of temporary and special factors. Generally, the arithmetic contribution of net exports to growth in the gross domestic product tends to be much closer to zero, and that is likely to be the case in coming quarters.

Also, part of the hand off will be US consumers going into debt (reducing savings) to buy foreign goods and services, which increases foreign sector savings of financial assets.

Overall, the incoming data suggest that the recovery of output and employment in the United States has slowed in recent months, to a pace somewhat weaker than most FOMC participants projected earlier this year. Much of the unexpected slowing is attributable to the household sector, where consumer spending and the demand for housing have both grown less quickly than was anticipated. Consumer spending may continue to grow relatively slowly in the near term as households focus on repairing their balance sheets. I expect the economy to continue to expand in the second half of this year, albeit at a relatively modest pace.

Agreed.

Despite the weaker data seen recently, the preconditions for a pickup in growth in 2011 appear to remain in place.

Agreed.

Monetary policy remains very accommodative,

Yes, for many borrowers, but the lower rates have also net reduced incomes. QE alone resulted in some $50 billion of ‘profits’ transfered to the Treasury from the Fed that would have been private sector income, for example.

and financial conditions have become more supportive of growth, in part because a concerted effort by policymakers in Europe has reduced fears related to sovereign debts and the banking system there.

Agreed.

Banks are improving their balance sheets and appear more willing to lend.

Agreed, though via a reduction in interest earned by savers that’s gone to increased net interest margins for banks.

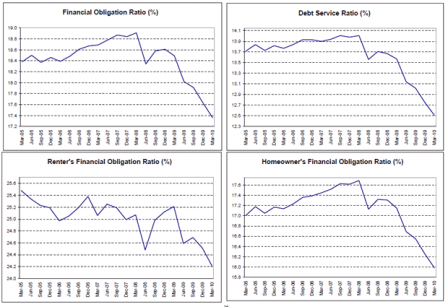

Consumers are reducing their debt and building savings, returning household wealth-to-income ratios near to longer-term historical norms.

Yes, ‘funded’ by the federal deficit spending.

Stronger household finances, rising incomes, and some easing of credit conditions will provide the basis for more-rapid growth in household spending next year.

Yes, and that basis is credit expansion.

On the fiscal front, state and local governments continue to be under pressure; but with tax receipts showing signs of recovery, their spending should decline less rapidly than it has in the past few years. Federal fiscal stimulus seems set to continue to fade but likely not so quickly as to derail growth in coming quarters.

Yes, and traditionally matched or exceeded by private sector credit expansion as above.

Recently, inflation has declined to a level that is slightly below that which FOMC participants view as most conducive to a healthy economy in the long run. With inflation expectations reasonably stable and the economy growing, inflation should remain near current readings for some time before rising slowly toward levels more consistent with the Committee’s objectives. At this juncture, the risk of either an undesirable rise in inflation or of significant further disinflation seems low. Of course, the Federal Reserve will monitor price developments closely.

The channels through which the Fed’s purchases affect longer-term interest rates and financial conditions more generally have been subject to debate.

With the debate subsiding as more FOMC participants, but far from all of them, seem to be coming to understand the quantity of the reserves per se has no consequences.

I see the evidence as most favorable to the view that such purchases work primarily through the so-called portfolio balance channel, which holds that once short-term interest rates have reached zero, the Federal Reserve’s purchases of longer-term securities affect financial conditions by changing the quantity and mix of financial assets held by the public. Specifically, the Fed’s strategy relies on the presumption that different financial assets are not perfect substitutes in investors’ portfolios, so that changes in the net supply of an asset available to investors affect its yield and those of broadly similar assets. Thus, our purchases of Treasury, agency debt, and agency MBS likely both reduced the yields on those securities and also pushed investors into holding other assets with similar characteristics, such as credit risk and duration. For example, some investors who sold MBS to the Fed may have replaced them in their portfolios with longer-term, high-quality corporate bonds, depressing the yields on those assets as well.

This is evidence Bernanke himself has come around to the understanding that the quantity of reserves at the Fed per se is of no further economic consequence.

We decided to reinvest in Treasury securities rather than agency securities because the Federal Reserve already owns a very large share of available agency securities, suggesting that reinvestment in Treasury securities might be more effective in reducing longer-term interest rates and improving financial conditions with less chance of adverse effects on market functioning.

Again, it shows the understanding that QE channel is price (interest rates) and not quantities.

This is a very constructive move from understanding indicated in prior statements.

Also, as I already noted, reinvestment in Treasury securities is more consistent with the Committee’s longer-term objective of a portfolio made up principally of Treasury securities. We do not rule out changing the reinvestment strategy if circumstances warrant, however.

In particular, the Committee is prepared to provide additional monetary accommodation through unconventional measures if it proves necessary, especially if the outlook were to deteriorate significantly. The issue at this stage is not whether we have the tools to help support economic activity and guard against disinflation. We do. As I will discuss next, the issue is instead whether, at any given juncture, the benefits of each tool, in terms of additional stimulus, outweigh the associated costs or risks of using the tool.

Notwithstanding the fact that the policy rate is near its zero lower bound, the Federal Reserve retains a number of tools and strategies for providing additional stimulus. I will focus here on three that have been part of recent staff analyses and discussion at FOMC meetings: (1) conducting additional purchases of longer-term securities, (2) modifying the Committee’s communication, and (3) reducing the interest paid on excess reserves. I will also comment on a fourth strategy, proposed by several economists–namely, that the FOMC increase its inflation goals.

In my humble opinion those tools carry no risk and provide no reward to the macro economy.