More modest signs of improvement in Japan, with employment and spending improving.

Unfortunately, the Prime Minister seems be about to make the same mistake of past Prime Ministers and take action to reduce the govt’s deficit.

In contrast, China seems to have recognized govt spending spending (and lending by state owned banks that is in fact thinly disguised govt spending) is not operationally dependent on revenue, and that there is no solvency issue nor external constraints on local currency expenditure. China seems to understand the risks are inflation, making adjustments as they see that political threat arise.

See comments below.

Aug Job-To-Applicant Ratio: 0.54% vs 0.54% (expect) / 0.53% (last)

Aug Jobless Rate: 5.1% vs 5.1% (expect) / 5.2% (last)

Aug Household Spending (YoY): 1.7% vs 1.4% (expect) / 1.1% (last)

Sep Tokyo CPI (YoY): -0.6% vs -0.9% (expect) / -1.0% (last)

Sep Tokyo CPI Ex-Fresh Food (YoY): -1.0% vs -1.0% (expect) / -1.1% (last)

Sep Tokyo CPI Ex-Fresh Food & Energy (YoY): -1.3% vs -1.4% (expect) / -1.4% (last)

Aug National CPI (YoY): -0.9% vs -0.9% (expect) / -0.9% (last)

Aug National CPI Ex-Fresh Food (YoY): -1.0% vs -1.0% (expect) / -1.1% (last)

Aug National CPI Ex-Fresh Food & Energy (YoY): -1.5% vs -1.5% (expect) / -1.5% (last)

October (Reuters) — Japan’s prime minister warned on Friday that the country’s fiscal situation was unsustainable given its huge public debt, and called for multiparty tax reform talks as he struggles with a fragile economy and a divided parliament.

With perhaps the world’s largest public debt, severe prior downgrades by the ratings agencies, perhaps the strongest currency in the world, mild deflation, and yet ten year JGB’s hovering around 1%, you’d think the historical evidence alone would convince them there is no solvency or funding or ‘sustainability’ issue. But clearly it doesn’t. And while those in monetary operations at the BOJ understand there is no sustainability issue, it is not their place to mention it (much like the US).

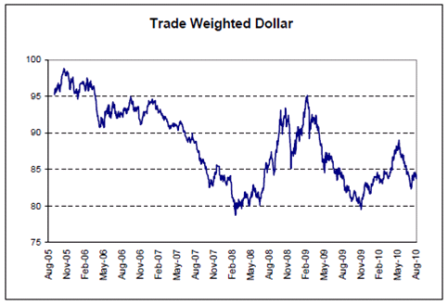

Naoto Kan also repeated his resolve to curb a rise in the yen that threatens to derail Japan’s export-led economic recovery, urged the central bank to do more to fight deflation, and expressed hope that opposition parties would join in talks on a extra budget he wants to enact soon.

This seems to indicate he’s pushing for a higher deficit? Or will there be a new tax to ‘pay for it?’ And the only way to weaken the yen vs the dollar is to buy dollars, which is what I call off balance sheet deficit spending. It ‘works’ and there are no operational limits to the amount of fx a CB can buy. But it’s a poor second choice to a domestic tax cut or spending increase.

Japan’s core consumer prices marked their 18th straight month of annual declines in August, as deflation grips an economy struggling with a rising yen, slowing exports and a surprise decline in output. But the jobless rate fell and the availability of jobs improved slightly, data showed on Friday.

Yes, the deficit did go up in the financial crisis slowdown and got large enough to support growth. The question is whether they allow that to continue.

Kan, who took office in June as Japan’s fifth leader in three years, faces a tough time wooing the opposition support that is vital to enact laws since his Democratic Party of Japan (DPJ) and a tiny partner lack a majority in parliament’s upper house.

The government faces the delicate task of reining in debt while keeping the economy going. Japan has built up a huge public debt burden, now nearly twice the size of its $5 trillion economy, during two decades of economic stagnation.

It might help if the media stopped calling it a burden, as it’s clearly not a burden in any sense. particularly with a 0 rate policy (not that it matters for solvency).

“If the current fiscal situation is left alone, it will be unsustainable at some point,” Kan said in a speech at the start of an extra session of parliament.

I doubt he could define ‘unsustainable’ but no one asks as the errant sustainability assumption is pervasive.

He also vowed to achieve Tokyo’s goal of bringing the primary budget balance, which excludes revenue from bond sales and debt-servicing costs, into the black within a decade.

Extra Budget

Kan, whose past calls for debating a hike in the 5 percent sales tax had contributed to a July upper house election defeat, said Japan needs a social welfare system that citizens could trust even if that meants added financial burden on the public.

Multiparty debate on tax reform including the sales tax is thus indispensable, Kan said, reiterating that he would seek a mandate from voters before deciding on the sale tax rise.

The government is crafting an extra budget for the fiscal year to March 31 to stimulate the economy by supporting job seekers and families with children, but has sent mixed signals about the size of the package and how it will fund it.

It does look like they plan on ‘funding it’

Some in the cabinet, such as the economics minister, have said new debt issuance should not be ruled out, but the finance minister is firmly against the idea.

National Strategy Minister Koichiro Gemba has said Japan could fund measures worth around 4.6 trillion yen ($55 billion) by tapping reserves, thereby avoiding new bond issuance.

Functionally this would be the same as deficit spending.

“The biggest task for this parliamentary session is enacting a supplementary budget to finance economic steps. I sincerely hope for constructive debate among ruling and opposition parties,” Kan said in the speech.

Efforts to gain such opposition support will be complicated by a bitter feud with China.

Kan is under fire for appearing to cave in to Beijing’s demands to free a Chinese fishing boat captain detained last month after his trawler collided with Japanese patrol boats near disputed islands in the East China Sea.

The prime minister on Friday reiterated that good ties with China, in the process of replacing Japan as the world’s second-biggest economy, were vital but also expressed concern about Beijing’s military buildup and aggressive maritime activities.

China still has bitter memories of the last war with Japan.