They give some indication of the macro economy

Texas drilling permits dropped 50 percent, Railroad Commission reports

By James Osborne

Oil drilling activity in Texas is falling dramatically, as the steep decline in crude prices since the summer takes hold, state regulators reported Tuesday.

The Texas Railroad Commission issued 1,353 permits for oil drilling last month, 50 percent less than it did the previous month. And in the months ahead, that will likely translate to rigs being shut down and layoffs across oil fields in West and South Texas.

“There’s more to come in the months ahead,” said Pavel Molchanov, an energy analyst with Raymond James. “This isn’t pleasant, but this is how the market rebalances itself.”

For now drilling rig counts are holding relatively steady, as companies wind down their contracts. Since peaking in October, the number of drilling rigs operating in the United States has declined by just 5 percent, according to the oil field service company Baker Hughes.

That number should continue a steady decline as companies make the decision to delay drilling on their leased land.

In recent weeks companies including Conoco Phillips and Marathon have both announced their drilling budgets for next year will be 20 percent less than 2014. For smaller companies, which fill out the bulk of the oil field, the reductions are even more dramatic.

Even so, oil production in Texas continues to grow, as existing wells flow and new wells come online. The Railroad Commission reported Texas produced 2.2 millions barrels a day in October, a modest increase from the previous month.

West Texas Intermediate, the U.S. benchmark, closed at $57 Tuesday, down more than 45 percent over the past five months. If that price holds, analysts are predicting U.S. production will continue to grow into mid-2015, at which point it will flatline though to the end of the year.

“2016 depends on what happens to oil prices between now and then. We think prices will be higher a year from now but there’s a lot of moving parts,” Molchanov said.

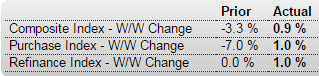

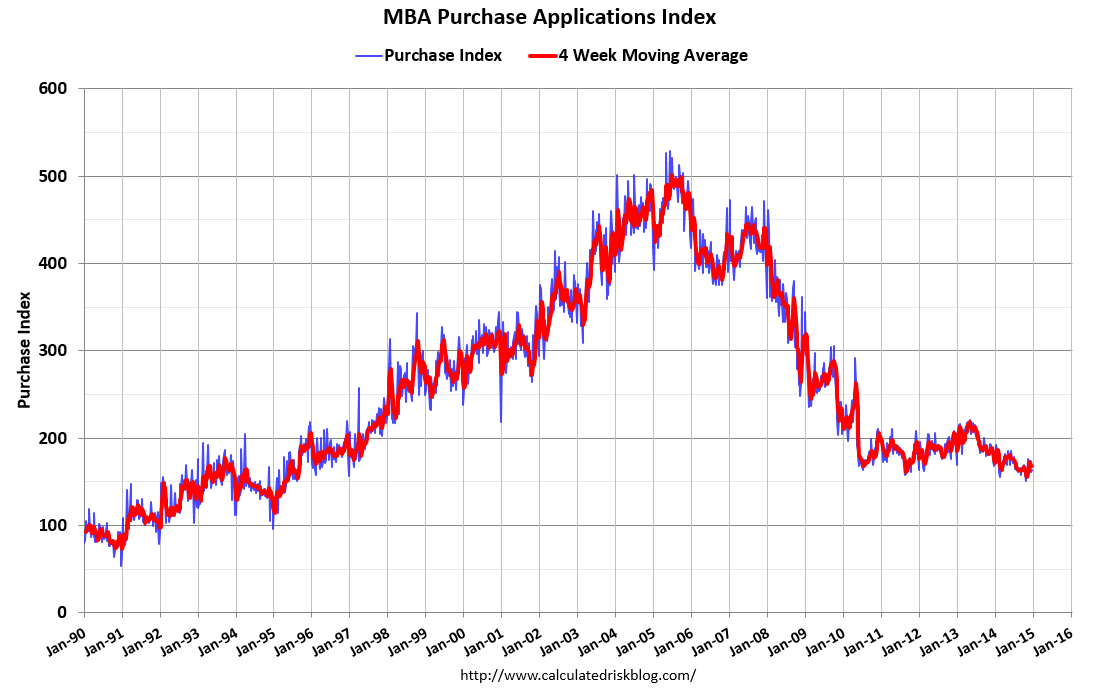

With cash sales down and mtg purchase apps still down year over year seems total sales would be down as well:

MBA Purchase Applications

Highlights

The purchase index showed a little life in the December 19 week, up 1.0 percent to help lift the year-on-year rate from the negative middle single digits to the low single digits at minus 1.0 percent.

New jobless claims remain low largely as a function of time since the last recession.

We’ll see what happens as oil sector cuts go into effect.

Jobless Claims

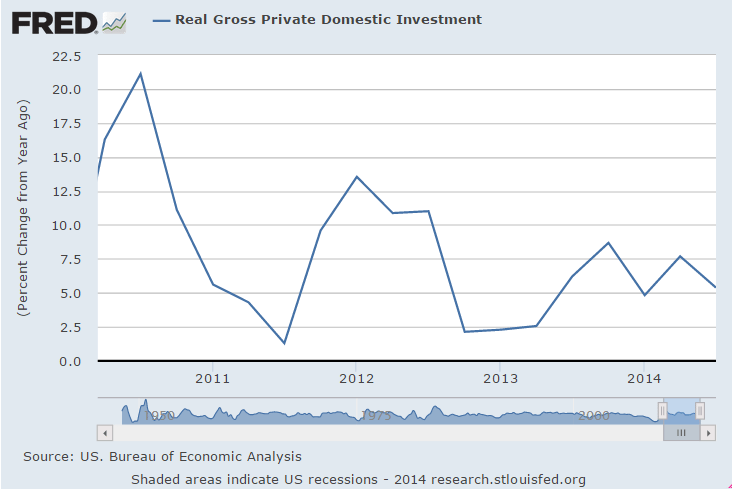

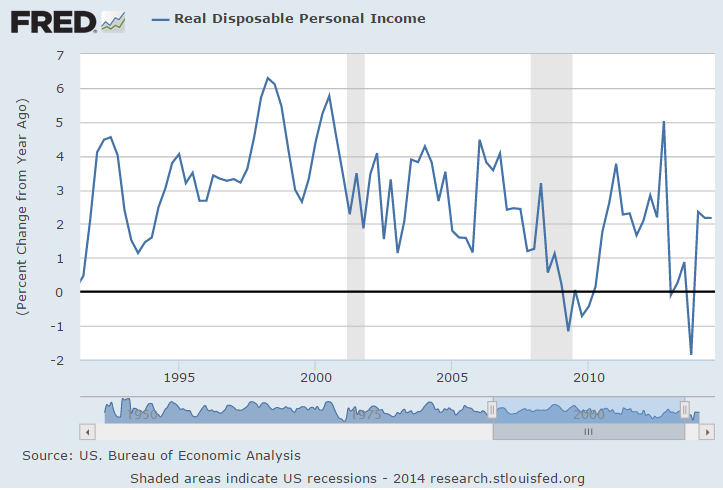

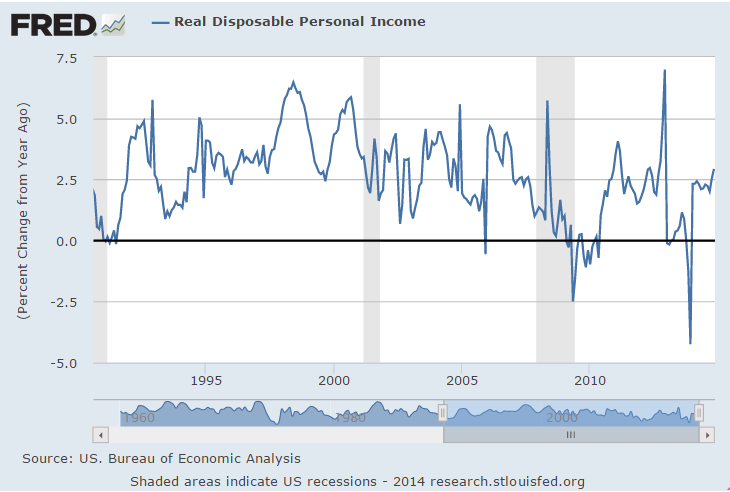

This was up 7.2% for Q3 from Q2 and should revert:

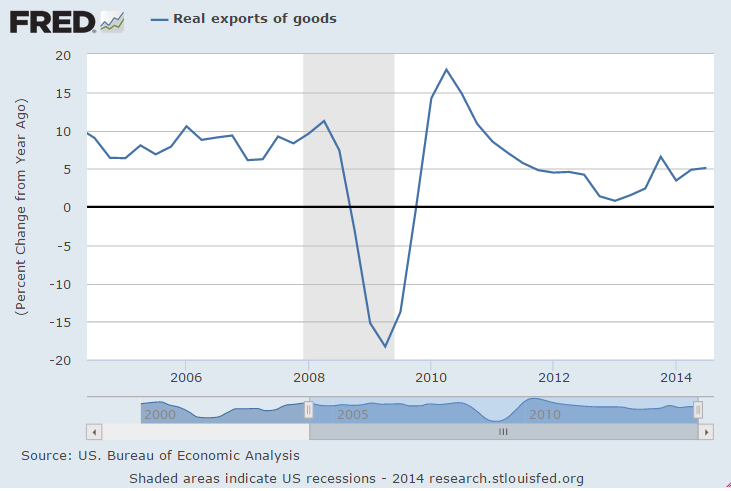

Exports of goods were up 7.5% and should revert:

(this chart hasn’t been updated today but it’s very close)

Near stall speed through Q3:

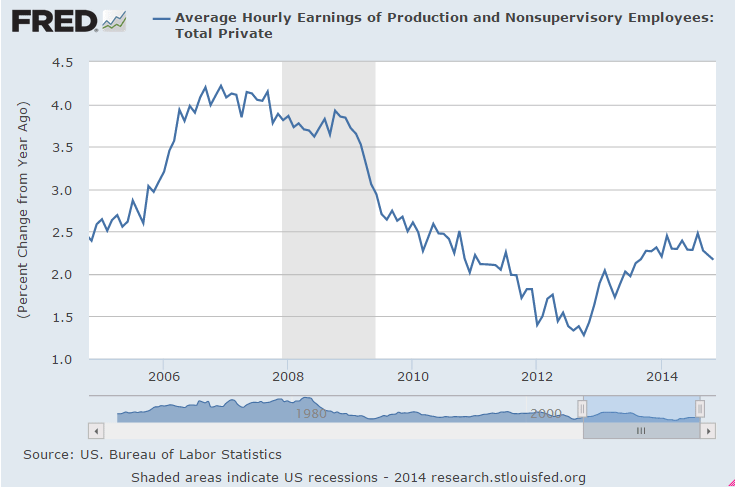

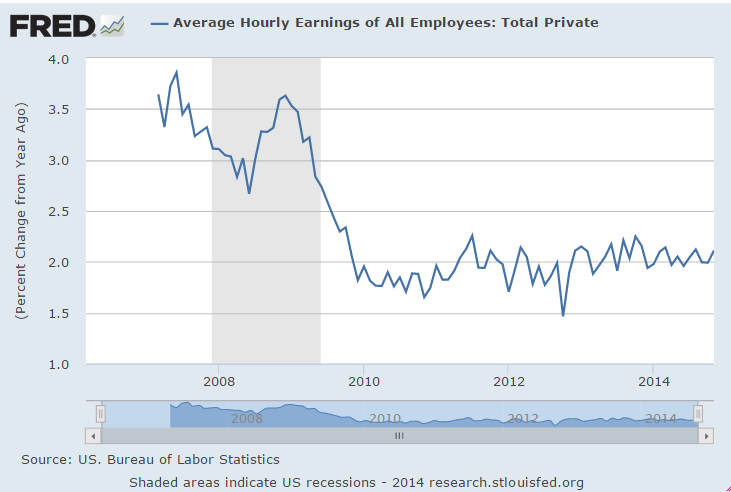

The monthly number just reported a blip up but the growth rate remains low and slowing, and it looks a lot worse when you take out the top 1% of course:

This is from the Dec 5 release:

This is the release from earlier today.

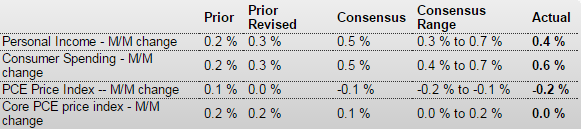

(These are not inflation adjusted):

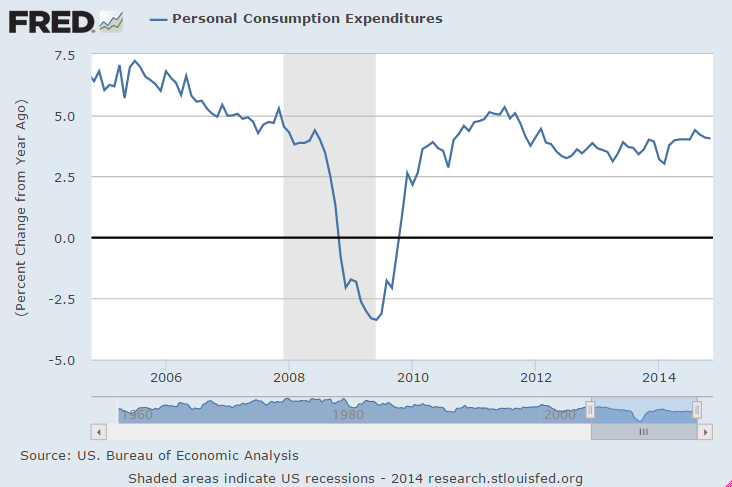

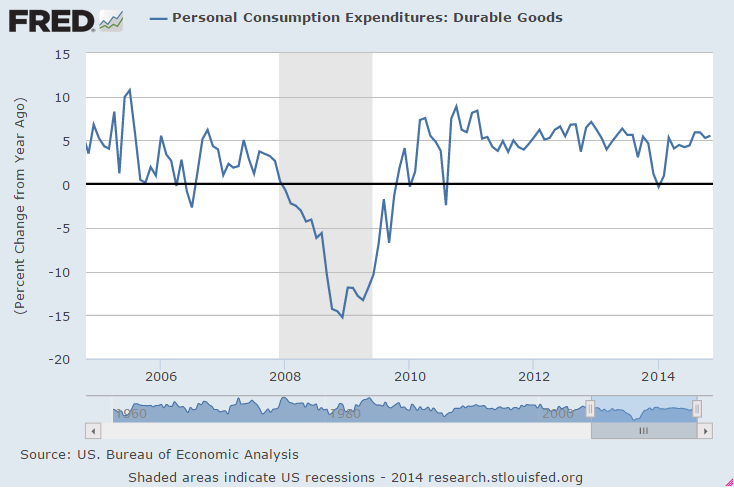

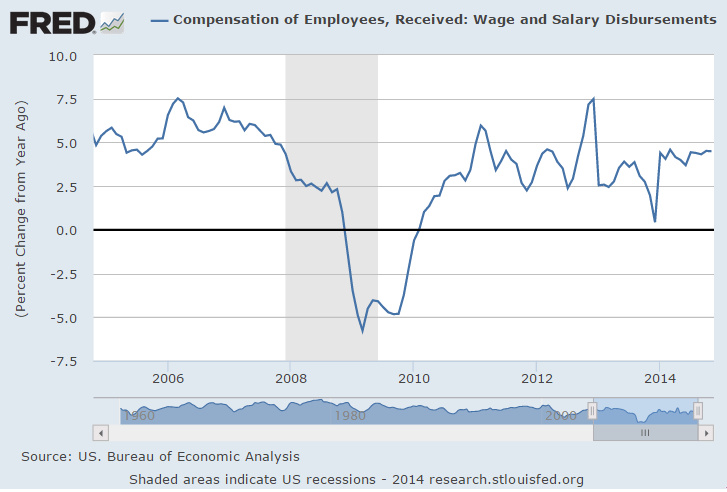

Personal Income growth remains anemic, particularly when the distribution of income gains is factored in. The gain in consumer spending was all durable goods, which has already reversed as per today’s earlier release.

Personal Income and Outlays

Highlights

The consumer sector continues to improve with gains in income and spending but inflation remains weak. Personal income advanced 0.4 percent in November after growing 0.3 percent in October. The wages & salaries component increased 0.5 percent, following a gain of 0.3 percent the month before.

Personal spending grew 0.6 percent, following 0.3 percent in October.

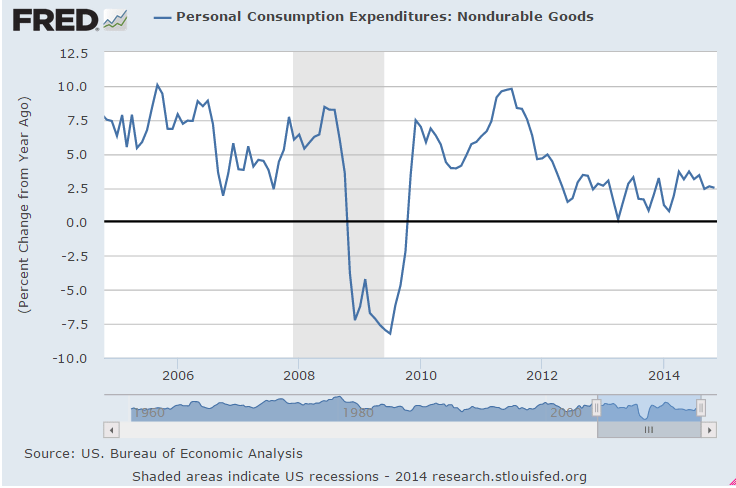

Strength was in durables which jumped 1.6 percent, following a rise of 0.3 percent in October. Nondurables were unchanged in November after decreasing 0.3 percent the prior month. Services improved 0.6 percent after rising 0.4 percent in October.

PCE inflation continues to be weak-largely due to lower energy costs. Headline inflation posted at a minus 0.2 percent on a monthly basis, following no change in October. Core PCE inflation was flat in November, following a 0.2 percent rise in October.

On a year-ago basis, headline PCE inflation eased to 1.2 percent in November from 1.4 percent the prior month. Year-ago core inflation came in at 1.4 percent in November compared to 1.5 percent in October. Both series remain below the Fed goal of 2 percent year-ago inflation.

Overall, the consumer sector is slowly improving even though inflation is below the Fed’s goal. In fact, lower gasoline prices are improving discretionary income and boosting spending elsewhere.

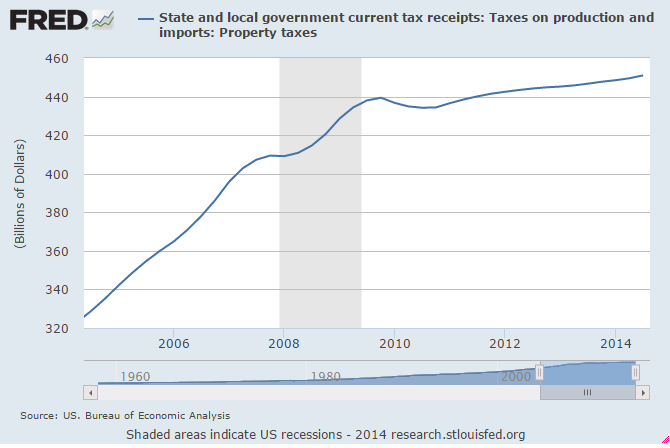

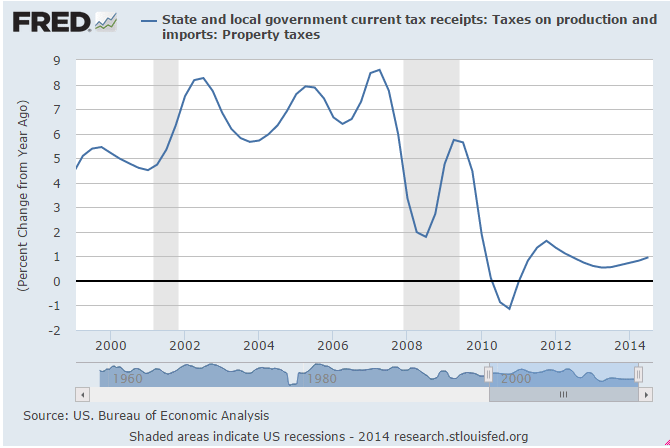

FHFA prices for home sales were up as the number of cheaper distressed sales declined.

Still looking like the cycle has peaked.

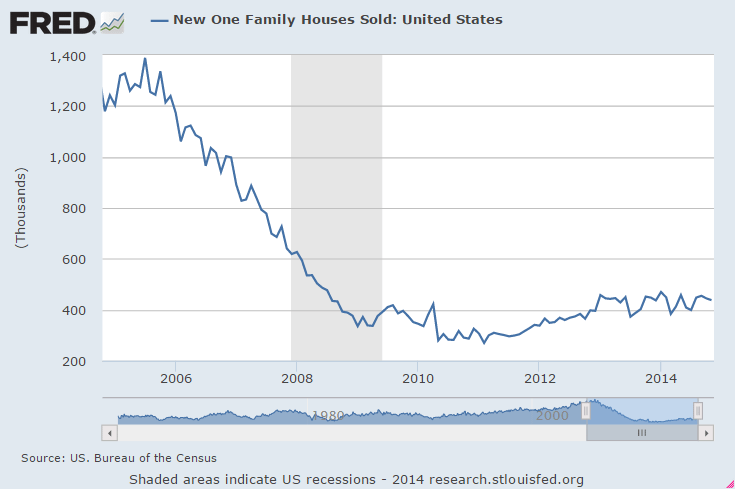

Yet another reversal from a blip up in Q3, and new home sales are a contributor to GDP, so this should cause more downward revisions to Q4 GDP

New Home Sales

Highlights

Like yesterday’s existing home sales report, today’s report on new home sales came in below low-end expectations, down 1.6 percent in November to an annual sales rate of 438,000 vs expectations for 460,000 and Econoday’s low-end estimate for 440,000.

Also like yesterday’s existing home sales report, price data show weakness with the median price down 3.2 percent in the month to $280,000. Year-on-year, the median price is up only 1.4 percent which, in what at least doesn’t point to an imbalance, is largely in line with year-on-year sales which are down 1.6 percent.

Supply data are stable with 213,000 new homes on the market vs 210,000 in October. Supply relative to sales is up slightly, to 5.8 months from 5.7 and 5.5 months in the prior two months. Regional sales data show declines in 3 of 4 regions including the South, which is larger than all other regions combined in this report, and a gain in the West.

Housing had been showing some life going into the fourth quarter but the readings on November have been a surprising disappointment and won’t be good reading for the nation’s builders.

Richmond Fed Manufacturing Index

Highlights

Activity has picked up this month in the Richmond’s Fed manufacturing district, to 7 from 4 in November. New orders show relative strength, at 4 vs November’s 1, but are still on the soft side. Order backlogs, however, show outright contraction for a second month, at minus 5 vs minus 2 in November.

Shipments show relative strength to November, at 5 vs 1, but, like new orders, are still on the soft side. A definitive sign of strength, however, comes from employment which is up 3 points to a very solid 13 in a reading that points to underlying confidence among the region’s manufacturers. Price data are soft in line with declining fuel costs.

Early readings on December’s manufacturing activity are mixed with today’s report and last week’s report from Kansas City pointing to slight acceleration for December but the reports from the New York and Philly Feds, along with the PMI national flash report, pointing to softness. Reports on November have also proven mixed with last week’s industrial production report showing outstanding strength in contrast to this.

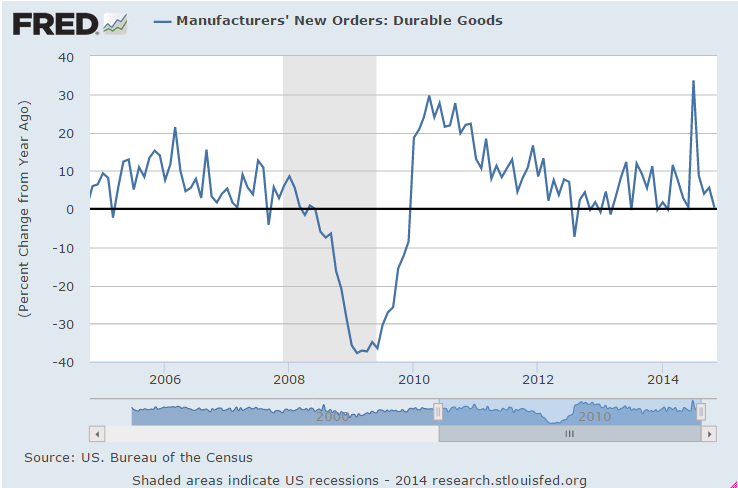

Durables not good, as Q4 deterioration continues:

Durable Goods Orders

GDP for Q3 revised up to 5%. Lots of volatile bits blipped up above their trend growth at the same time, which tends to reverse the next quarter.

Defense was up 16% from Q2, exports of goods up 7.5%, durable goods up 9.2%, and gross private domestic investment up 7.2% for example, while Q3 disposable personal income growth fell to 3.3% from 3.6% in the prior Q3 release.

GDP

The Saudis never ‘cut production’

They just set price and let the world buy what it wants at their price.

No one seems to know that.

As no one ever asks if they are going to raise price.

OPEC leader vows not to cut oil output even if price hits $20

“It is not in the interest of Opec producers to cut their production, whatever the price is,” he told the Middle East Economic Survey.

“Whether it goes down to $20, $40, $50, $60, it is irrelevant.”

In the MEES interview, Mr Naimi said Saudi Arabia and other Gulf oil producers would be able to withstand a long period of low crude prices, largely because their production costs were so low — at only about $4-$5 a barrel.

But he said the pain will be much greater for other oil regions, such as offshore Brazil, west Africa and the Arctic, whose costs are much

higher.

“So sooner or later, however much they hold out, in the end, their financial affairs will limit their production,” he said.

“We want to tell the world that high efficiency producing countries are the ones that deserve market share,” said Mr Naimi added. “If the

price falls, it falls . . . Others will be harmed greatly before we feel any pain.”

The bluntness of Mr Naimi’s message took even seasoned Opec observers by surprise. “I’m more bearish than most people looking at the

oil price, but even I am stunned how aggressive his comments are about this radical departure from policy,” said Yasser Elguindi of

Medley Global Advisors.

Bad.

And prices down again.

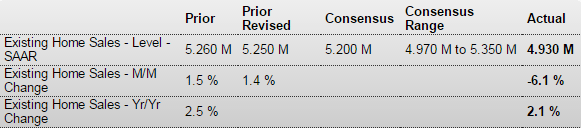

As previously discussed, with mtg purchase apps down and cash buyers down it’s hard to see how sales can rise…

Existing Home Sales

Highlights

Existing home sales had been showing some life but not in November, sinking a very steep 6.1 percent to a 4.93 million annual rate which is below the low end of the Econoday consensus (4.97 million to 5.35 million). November, a month when the nation’s weather proved mostly mild and which should have given a boost to sales, ends 5 straight months of plus 5.0 million rates.

November’s weakness is broad based with all 4 regions showing single digit monthly declines. But the good news is that the weakness in sales is not inflating supply which, due to a draw down of homes on the market to 2.09 million from 2.24 million, held steady relative to sales, at 5.1 months.

Lower prices don’t seem to be giving a boost to sales. The median fell for a 5th straight month, down 1.1 percent in November to $205,300. Year-on-year the median price, where growth had been in the double digits through most of last year, is up 5.5 percent, holding in the mid-single digit area where it’s been since March.

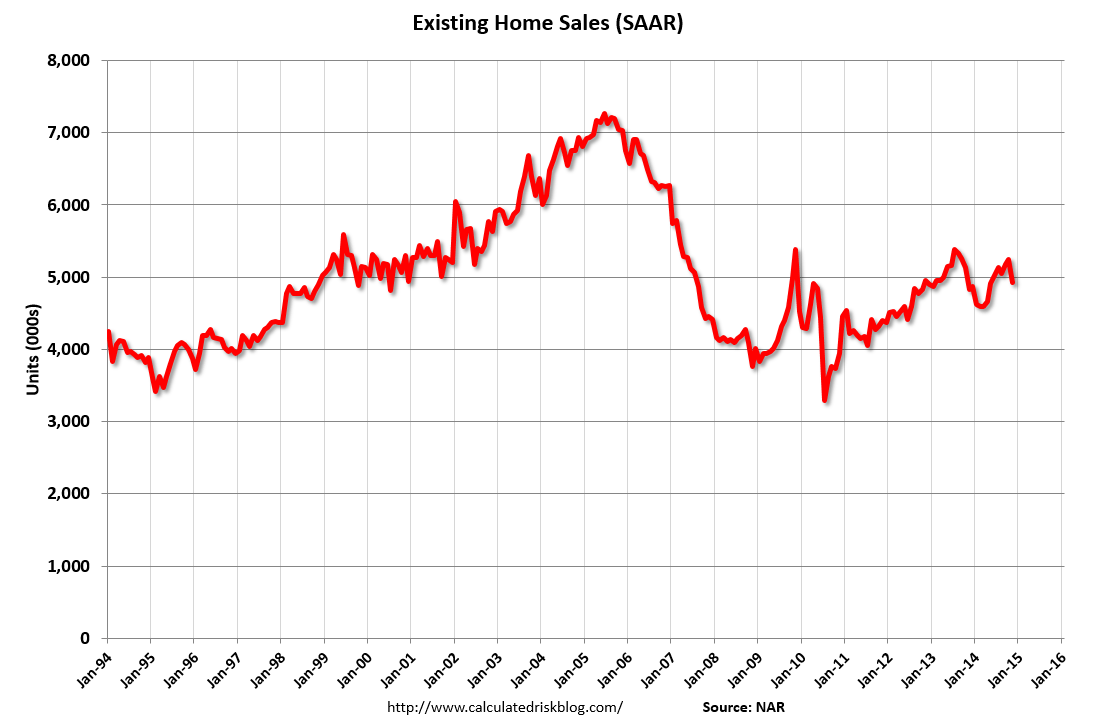

Existing Home Sales in November: 4.93 million SAAR, Inventory up 2.0% Year-over-year

By Bill McBride

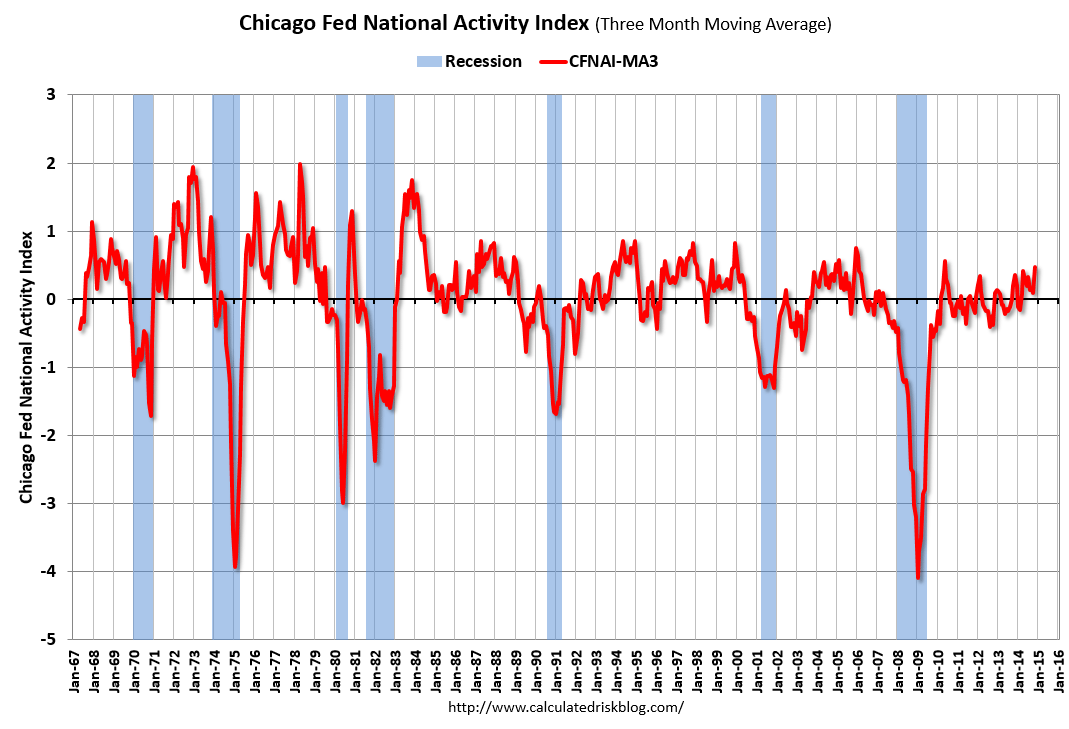

A bit of a blip up in manufacturing, the rest not good:

Chicago Fed National Activity Index

Highlights

The big 1.1 percent jump in the manufacturing component of the industrial production fed a very strong plus 0.73 percent reading for November’s national activity index vs a revised plus 0.31 in October. Other components in November, however, were flat with the positive contribution from employment edging lower while the positive contribution from sales/orders/inventories all but disappeared. The drag from consumption & housing remained moderate. The outsized manufacturing gain also boosted the 3-month average which rose to plus 0.48 in November from October’s revised plus 0.09 for its strongest reading since May 2010.

Banks getting hurt as feared.

Bank Revenues Plummet 17% In October And November According To Citi