When the growth rate was even modestly increasing it made the news.

Now that it’s decelerating not a word…

When the growth rate was even modestly increasing it made the news.

Now that it’s decelerating not a word…

Still negative:

Chicago Fed National Activity Index

Highlights

December was a weak month for the U.S. economy but a little less weak than November, based on the national activity index which improved to minus 0.22 from minus 0.36 (revised lower from minus 0.30). The improvement is centered in the production component as contraction in industrial production eased to minus 0.4 percent from November’s very deep minus 0.9 percent. Other components were steady with sales/orders/inventories and consumption & housing both slightly negative. The only component in positive ground is employment, unchanged in the month at a solid plus 0.12. Despite the improvement in December, the 3-month average fell to minus 0.24 from minus 0.19 in November. This report is a reminder that economic activity is subdued which is a major factor, aside from low oil and commodity prices, holding down inflation.

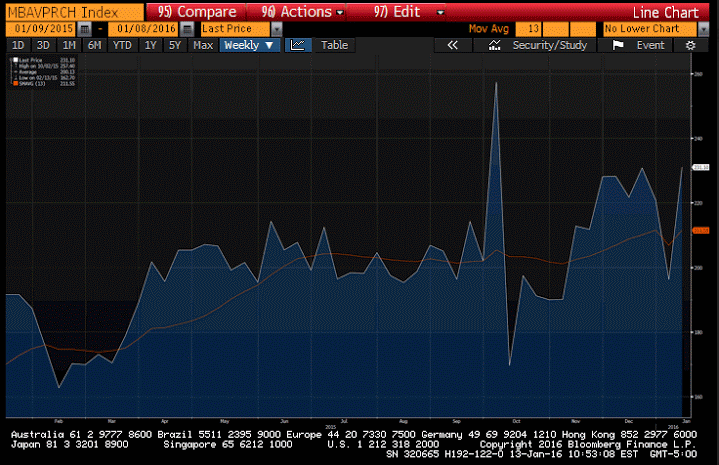

Up more than expected, but from the chart you can see the average of the last two volatile months is still down a bit vs prior months:

Possible bottom and now moving higher:

This month’s negative reading doesn’t look so bad because the revised last month’s down so much…

;)

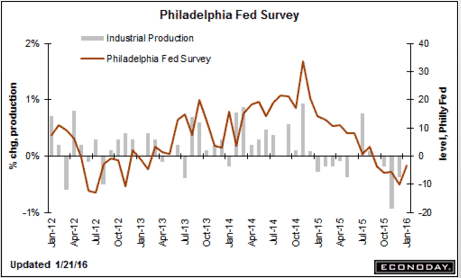

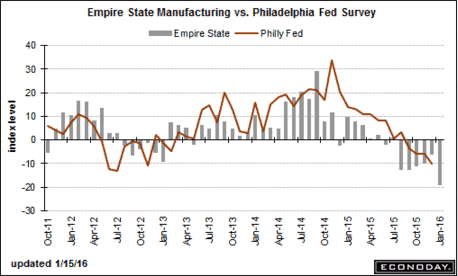

Philadelphia Fed Business Outlook Survey

Highlights

The factory sector continues to slow this month though, in good news, the rate of contraction is flattening out. The Philly Fed’s general business conditions index for January is minus 3.5, a little better than the Econoday consensus for minus 4.0 and the best reading since all the back in August. The new orders index likewise is improving, at minus 1.4 for the best reading since September. And shipments, for the first time also since September, are positive, at a strong 9.6.

But most readings in this report are in the negative column including employment, unfilled orders, the workweek, and also inventories where destocking is becoming more aggressive. And judging by the six-month outlook, down 5 points to 19.1 for the softest level since 2012, the destocking is defensive and intentional.

Price data are also negative but less so than prior months. And this is the clear theme from this report, that the factory sector may be beginning to level out following a very flat 2015 that was held down by weak global demand and weak energy markets.

Looks to have stopped growing about 10 months ago:

Remains seriously depressed:

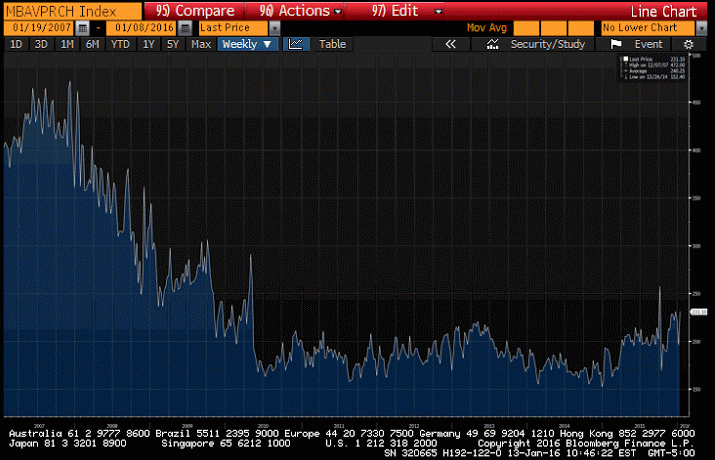

MBA Mortgage Applications

Not long ago they blamed cold weather, now it was the warm weather.

And this time not a word about the consumer not spending his gas savings…

;)

Holiday sales fall short of forecasts: NRF

Jan 15 (CNBC) — The National Retail Federation said Friday that holiday sales increased 3 percent to $626.1 billion in November and December, falling short of the trade group’s forecast for 3.7 percent growth, as unseasonably warm weather and low prices weighed on results.

The news came shortly after the Commerce Department said retail sales posted an unexpected drop in December, falling 0.1 percent from the previous month. Compared with the prior year, December sales rose 2.2 percent, to $448.1 billion, according to the government data.

During the October to December period, total sales rose 1.8 versus the prior year, according to the department. Total sales for all of 2015 increased 2.1 percent, representing their weakest result since 2009, Reuters said.

“Make no mistake about it, this was a tough holiday season for the industry,” said NRF President Matthew Shay. “Weather, inventory challenges, advances in consumer technology and the deep discounts that started earlier in the season and that have carried into January presented stiff headwinds.”

“Despite these factors, the industry rallied, consumers responded and sales still grew at a healthy rate.”

How the industry generated this growth, however, remained a top concern among analysts. They cautioned that profitability will likely take a hit when retailers start rolling out their fourth-quarter earnings results in coming weeks, thanks to aggressive discounts.

“Knowing that the topline growth was fueled by promotions tells us that the real number for us to focus on is … the individual bottom-line results for retailers, because that’s where we’re going to see the real profitability numbers,” said Steve Barr, PwC’s U.S. retail and consumer leader.

Industry forecasts had called for modest sales growth this holiday season, as low gas prices and a stronger economy battled against muted wage gains and higher rent and health-care costs. Retailers that cater to middle-income shoppers faced even more headwinds, including price deflation and a shift in consumer spending toward dining out or travel.

As a result, the National Retail Federation predicted retail sales excluding autos, gas and restaurants would increase 3.7 percent in November and December, compared with the prior year’s 4.1 percent growth.

In the same vein, consulting firm AlixPartners forecast holiday sales (excluding motor vehicles, food services and dining, and gas stations) would rise 2.8 to 3.4 percent during the final two months of the year, compared with 4.4 percent growth in 2014.

And Deloitte, whose prediction covers the November through January period (but excludes motor vehicles and gasoline) predicted a 3.5 to 4 percent increase. That would mark a slowdown from its recorded 5.2 percent gain the prior year.

As the season progressed, however, analysts grew more pessimistic that sales would meet these forecasts. Despite retailers’ best efforts to get shoppers into their stores earlier, November got off to a slow start. Then, over the critical Black Friday weekend, ShopperTrak data indicated that sales fell an estimated 10.4 percent.

What’s more, unseasonably warm weather through December took a huge bite out of retailers’ traffic and sales, with Planalytics calculating a $572 million sales loss for specialty apparel stores during the final two months. That figure does not even take into account department stores, which also rely heavily on apparel. In its holiday sales release,Macy’s blamed 80 percent of its 4.7 percent same-store sales decline on cold-weather goods.

Down again, now forecasting only .6% GDP growth for Q4:

Looks like the Fed hiked during a recession.

Should make for interesting Congressional testimony…

Maybe the hundreds of $ millions they spend on economic research isn’t enough???

;)

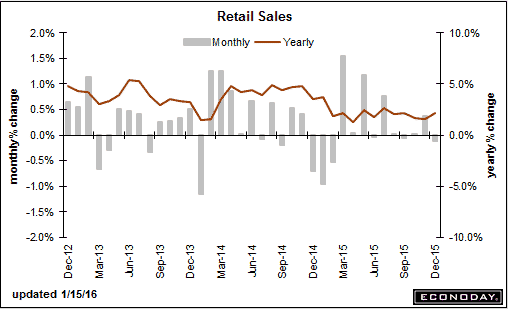

Sales remain at recession levels:

Retail Sales

Highlights

Retail sales proved disappointing in December, down 0.1 percent in a headline that is not skewed by vehicles or even that much by gasoline. Ex-auto sales also fell 0.1 percent while the core ex-auto ex-gas reading came in unchanged which is well below both expectations as well as low-end expectations. The Beige Book yesterday warned us about weak apparel sales which in this report fell a very steep 0.9 percent, in a decline that likely reflects more than just import-price contraction. The general merchandise category, which is very large, fell 1.0 percent in the month. Electronics & appliances also show contraction.

December winds up what was a not-so-great year for the nation’s retailers. Total sales rose only 2.1 percent in the year, the smallest gain since 2009 and well down from 3.9 percent in 2014. Excluding motor vehicles, sales rose 0.9 percent, far lower than 2014’s 3.1 percent.

There are, however, some positives in the report including another strong gain for restaurants, up 0.8 percent, and also another gain for furniture & home furnishings, up 0.9 percent in strength that confirms ongoing improvement in the housing sector. But sales at non-store retailers rose only 0.3 percent for a second straight month which are moderate gains that do not confirm anecdotal reports of unusual holiday strength for online shopping.

Upward revisions do take some of the sting out of the December report but not much. November total sales are revised 2 tenths higher to plus 0.4 percent and reflects a sharp upward revision to vehicle sales to plus 0.5 percent. But vehicle sales couldn’t muster any strength in December, coming in unchanged. And sales at gasoline stations extended their long run of contraction that reflects falling oil prices, down 1.1 percent in December.

There’s plenty of jobs for consumers and gas prices are low — but so are wages. The consumer started to slow down at year end and that was before the new trouble in China. Today’s data will pull down expectations for fourth-quarter growth.

Retail Sales ‘control group’ (retail sales excluding food, auto dealers, building materials, and gas stations)

More recession evidence, and maybe worse…

Empire State Mfg Survey

Highlights

The contraction in factory activity in the New York manufacturing region, which began way back in August, unfortunately is picking up a lot of steam this month, at minus 19.37 for the January headline which is the lowest reading since April 2009. New orders, at minus 23.54, are contracting for an eighth straight month and at the sharpest pace since March 2009. Unfilled orders, at minus 11.00, are in an even deeper string of contraction. Employment, at minus 13.00, is down for a sixth straight month as is the workweek, at minus 6.00. And there’s a crumbling going on in the 6-month outlook which, at 9.51 is still in the positive column but shows the least optimism since way back in March 2009. This report is grim and offers an initial look at January’s factory activity which, based on these results, appears to be getting hit by global concerns.

More recession evidence, or worse…

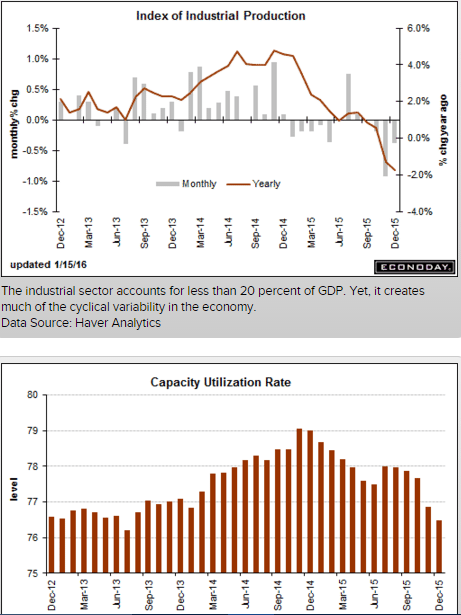

Industrial Production

Highlights

December was not a good month for the industrial economy as industrial production fell a sharper-than-expected 0.4 percent. Utility output, down 2.0 percent, declined for a third straight month reflecting unseasonably warm temperatures. Mining, reflecting low commodity prices and contraction in energy extraction, has also been week, down 0.8 percent for a fourth straight decline. Turning to manufacturing, which is the most important component in this report, production fell 0.1 percent for a second straight month (November revised downward from an initial no-change reading).

Details on manufacturing include a second straight contraction for vehicles, down 1.7 percent following November’s 1.5 percent decline. Weakness here, along with weakness in the motor vehicle component of this morning’s retail sales report, will raise talk that the auto sector, which had been one of the highlights of the 2015 economy, may slow down in 2016, at least the early part of the year. Construction supplies are a positive, up 0.6 percent for the second strong showing in three months and confirming strength underway in data for construction spending.

Capacity utilization fell 4 tenths from a downwardly revised November to 76.5 percent. A low utilization rate, which is running roughly 4 percentage points below its long-term average, holds down the cost of goods.

Year-on-year rates confirm weakness, down 1.8 percent overall with utilities down 6.9 percent and mining down 11.2 percent. Manufacturing is in the plus column but it’s nothing spectacular, at plus 0.8 percent.

Making matters worse is a downward revision to November, now at minus 0.9 percent vs an initial decline of 0.6 percent. Looking at the annualized rate for the fourth quarter, industrial production fell 3.4 percent though manufacturing did increase but not much, up 0.5 percent. Weather factors are skewing utility output but otherwise, readings are fundamentally soft and reflect the downturn in global demand made more severe for U.S. producers by strength in the dollar.

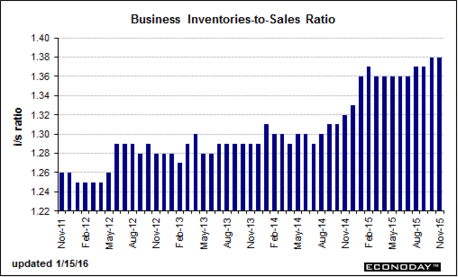

Inventories down some but sales down same so relative to sales inventories remain way high, another recession indication:

Business Inventories

Highlights

Inventories are contracting, the result of defensive draws in the wholesale and manufacturing sectors. Business inventories fell 0.2 percent in November following a decline in October of 0.1 percent. Wholesale inventories fell 0.3 percent for a second straight month with manufacturing down 0.3 percent following October’s 0.2 percent draw. Retail, up 0.2 and 0.1 percent in November and October, was the only sector adding inventories and today’s weak results for December retail sales may point to an unwanted build for December.

Relative to sales, which also fell 0.2 percent and were down 0.3 percent in October, total inventories are stable, at a ratio of 1.38. This report is indicative of economic weakness and will not be building expectations for fourth-quarter growth let alone the outlook for first-quarter growth.

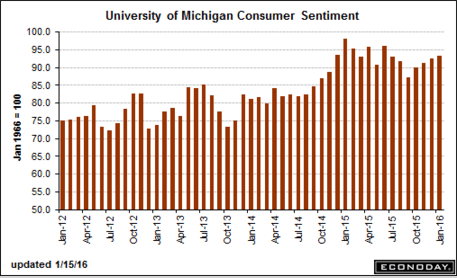

This was up a tad so they have something to report on the news. But even here the current conditions took a dive. And, as previously discussed, this is one man one vote, not one dollar one vote, and total spending has been decelerating:

Consumer Sentiment

Highlights

The first indication of the China effect on U.S. consumers looks positive but ultimately is mixed. January’s flash consumer sentiment index did rise 7 tenths from final December to 93.3 but current conditions, the component that picks up the immediate impact of special factors, fell 3.0 points to 105.1. Should volatility in markets begin to ease and confidence in China improve, this reading could pop back as quickly as month end.

Lifting the mid-month index is a rise in the expectations component, up 3.0 points 85.7. Behind this gain is strength in the jobs market and perhaps even falling oil prices as 1-year inflation expectations are down a sizable 2 tenths to 2.4 percent. This is offset in part by a 1 tenth rise in 5-year expectations to 2.7 percent.

The resilience in long-term optimism is a plus for the U.S. economy though the eroding in short-term inflation expectations will not be encouraging to Federal Reserve policy makers who have launched a rate-hike sequence for an economy still struggling against deflation. The Dow is moving off opening lows in early reaction to this report.

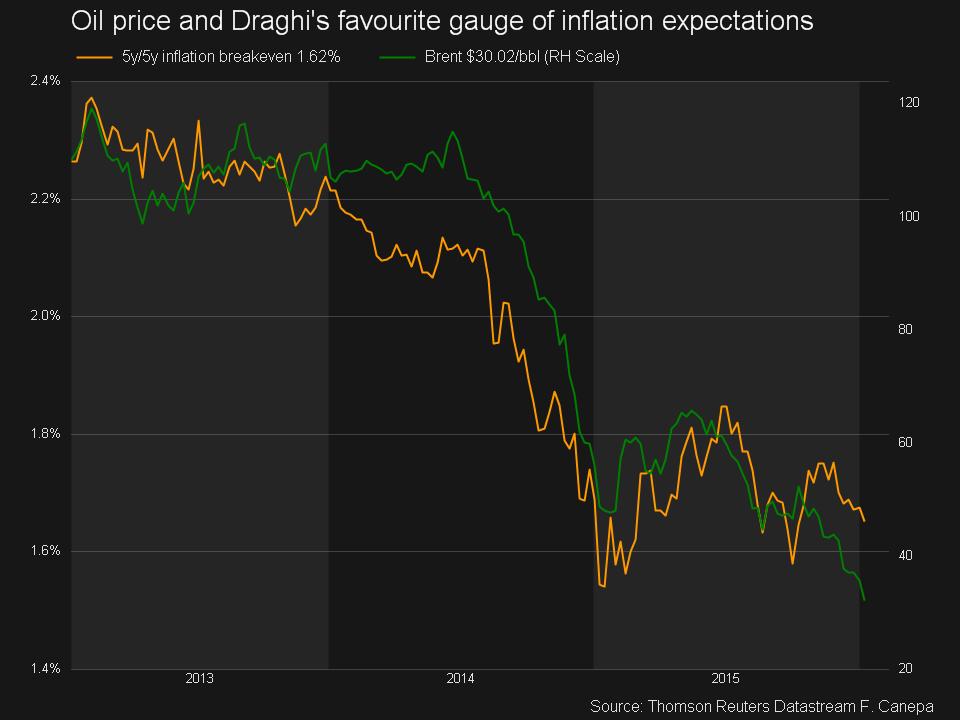

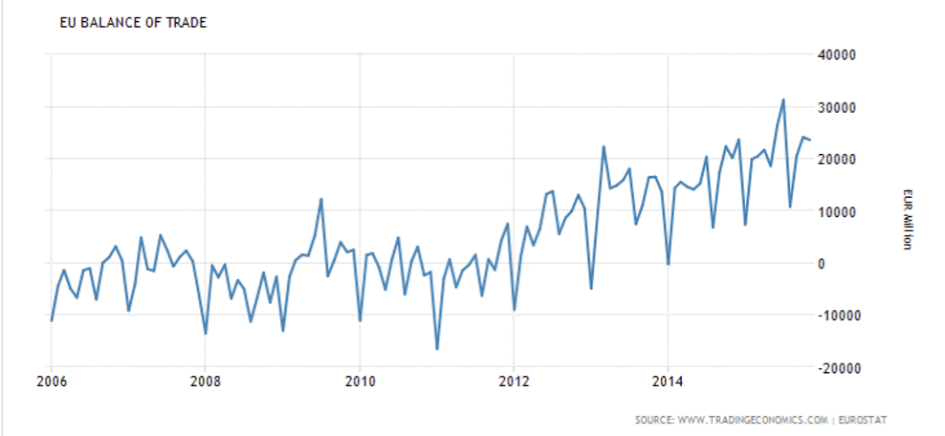

This just keeps going up, which fundamentally tends to drive up the euro which tends to continue to be subject to said upward pressure until the trade picture reverses:

Euro Area Balance of Trade

The Eurozone trade surplus increased to €23.6 billion in November of 2015 compared to a €20.2 billion surplus a year earlier. Exports recorded the highest annual gain in four months and imports rebounded.

Potential showdown that could drive up Spanish rates:

Guindos Ditches Pledge on Spain Deficit to Push Growth

By Maria Tadeo

Jan 14 (Bloomberg) — Spanish finance chief Luis de Guindos ditched his promise to meet European Union budget goals saying shoring up economic growth is more important for his country’s future.

De Guindos said worrying about whether the budget deficit comes in a few tenths of a percentage point above the country’s 4.2 percent target for 2015 would be a distraction from the fundamental challenge of protecting the economic recovery.

“What is important is to maintain the pace of growth of the Spanish economy,” he told reporters on Thursday before meeting euro-area finance ministers for the first time since December’s general election left the parliament divided between four major parties.

“The biggest risk for budget policy is that the Spanish economy slows down,” de Guindos added.

Spain risks being drawn into a clash with the European Commission which has been warning since October that the spending plans acting Prime Minister Mariano Rajoy pushed through ahead of the election don’t do enough to curb the currency union’s biggest budget shortfall. Eurogroup chief Jeroen Dijsselbloem, who saw off a challenge from de Guindos to hang on to his job last year, said this month that Spain won’t be allowed any more flexibility over its target, according to El Pais newspaper.

Speaking to reporters on Thursday, Dijsselbloem said Brussels would “wait for the outcome of the domestic political process,” before taking further action.

Looks like they are again making hawkish noises, taking the lead of the Fed:

ECB wary of further action despite uncertain future

By: Balazs Koranyi and John O’Donnell

Jan 14 (Reuters)

* Many governors sceptical of need for further action in near term

* Governors urge countries to act instead with reform

* Oil price and inflation expectations:

Many European Central Bank policy makers are sceptical about the need for further policy action in the near term, conversations with five of them indicate, even as inflation expectations sink and some investors bank on more easing.

Next week’s rate meeting is expected to be relatively uneventful with the big test coming when the ECB releases its initial 2018 growth and inflation forecasts on March 10.

But apparently recent market action has got the Fed thinking twice about it’s hiking intentions:

China may slow Fed’s interest rate rises: Fed officials

Jan 13 (Reuters) — The rout in China’s stock market, weak oil prices and other factors are “furthering the concern that global growth has slowed significantly,” Boston Fed President Eric Rosengren said. Rosengren also said a second hike will face a strict test as the Fed looks for tangible evidence that U.S. growth will be “at or above potential” and inflation is moving back up toward the Fed’s 2 percent target. “It’s something that’s got to make you nervous,” Chicago Fed chief Charles Evans said of the drag slower growth in China could have on economies like the United States that don’t do much direct trade. Evans also said he was nervous about inflation expectations not being as firmly anchored as a year ago, and added it could be midyear before the Fed has a good picture of the inflation outlook.

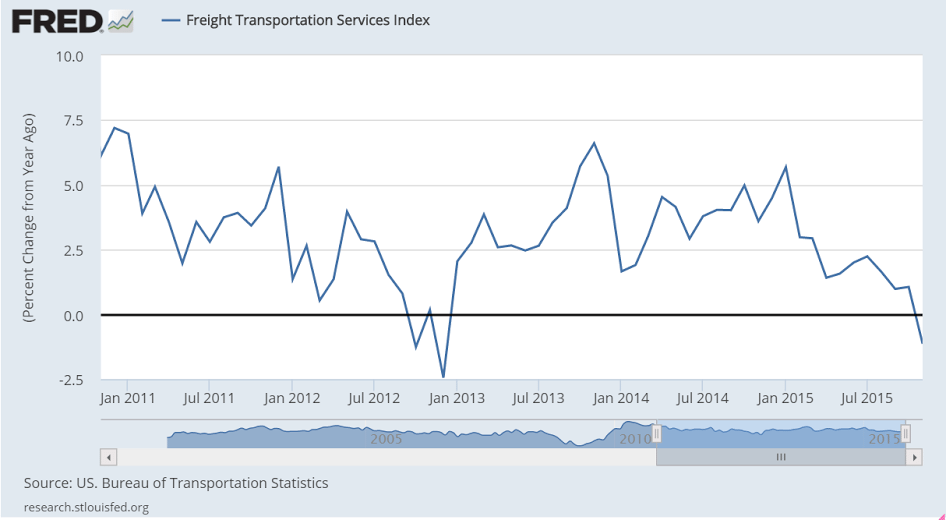

Confirming the rail traffic indicators:

CSX fourth quarter profit falls on lower freight volumes

Jan 13 (Bloomberg) — CSX said freight volumes fell 6 percent in the fourth quarter, with a huge 32 percent decline in the amount of coal hauled. Fourth-quarter net income was $466 million or 48 cents per share, down 5 percent from $491 million or 49 cents per share a year earlier. Revenue in the quarter was $2.78 billion, down nearly 13 percent from $3.19 billion a year earlier. “We have not seen these kind of pressures in so many different markets because you have multiple aspects working against you: Low gas prices, low commodity prices, strength of the dollar,” CEO Michael Ward said on the call. Except auto, housing, “you are seeing pressure on most of the markets.”

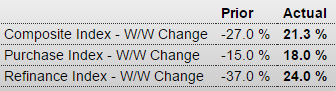

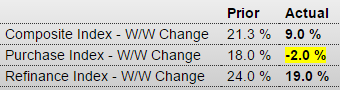

Lots of up and down right now.

The chart indicates purchase apps may be up a bit but still depressed historically.

MBA Mortgage Applications

Highlights

The new year is seeing a surge in mortgage activity reflecting a strong jobs market and low rates, according to the Mortgage Bankers Association’s weekly report. Purchase applications surged 18 percent in the January 8 week with refinancing applications up 24 percent. These gains, however, also reflect volatility in weekly measures and largely reverse giant swings in the prior week’s data. The average rate for conforming loans ($417,000 or less) fell 8 basis points in the week to 4.12 percent.

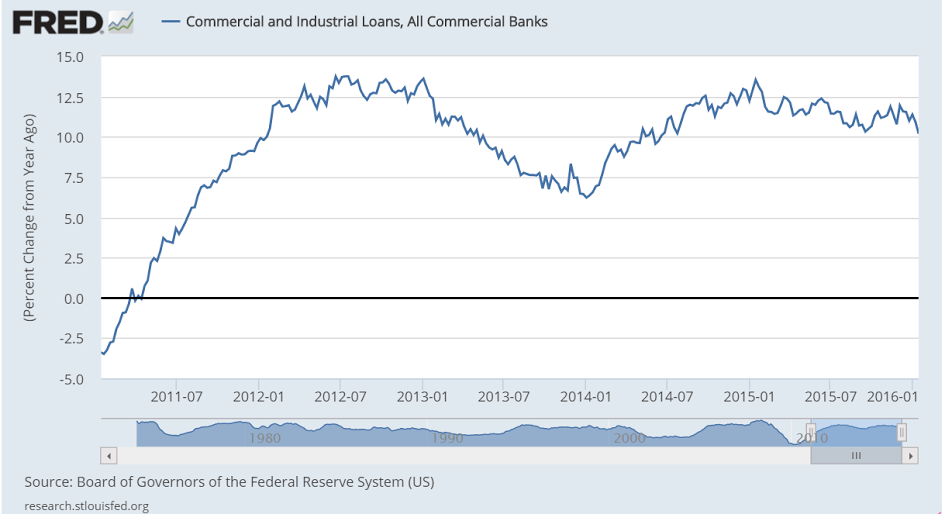

This shows the 3 month moving average in orange for just the last year:

This kind of trade surplus ultimately supports the currency, though FDI flows can can and have been much larger recently as previously discussed:

China Trade Surplus Widens in December

China trade surplus increased to USD60.09 billion in December of 2015 from USD49.61 billion reported a year earlier and beating market consensus, as exports and imports fell much less than expected. Year-on-year, outbond shipments declined by1.4 percent to USD224.19 billion, the sixth straight month of fall and the smallest drop since June. Imports dropped by 7.6 percent to USD164.10 billion, the 13th consecutive month of contraction, as a result of declining commodity prices and weak demand.

This time the warm weather is cited for the weakness as utility spending fell. Yes, capitalism is about sales, and unspent income reduces sales, unless other agents spend more than their income, etc. etc.

And with the private sector in general necessarily pro cyclical, unspent income stories beg fiscal adjustments, which at the moment are universally out of style.

U.K. Industrial Output Plunges Most in Almost Three Years

By Jill Ward

Jan 12 (Bloomberg) — UK industrial production fell the most in almost three years in November as warmer-than-usual weather reduced energy demand.

Output dropped 0.7 per cent from the previous month, with electricity, gas and steam dropping 2.1 per cent, the Office for National Statistics said in London on Tuesday. Economists had forecast no growth on the month.

The data highlight the uncertain nature of UK growth, which remains dependent on domestic demand and services. After stagnating in October and falling in November, industrial production will have to rise 0.5 per cent to avoid a contraction in the fourth quarter.

Manufacturing also delivered a lower-than-forecast performance in November, with output dropping 0.4 per cent on the month. On an annual basis, factory output fell 1.2 per cent, a fifth consecutive decline.

To the same point, capital expenditures constitute spending that offsets unspent income, etc. And so without some other spending stepping up to replace this lost capex GDP goes nowhere, as previously discussed. This $90 billion cut is only one source of capex reductions:

Oil Plunge Sparks Bankruptcy Concerns

Jan 11 (WSJ) — As many as a third of American oil-and-gas producers could tip toward bankruptcy and restructuring by mid-2017, according to Wolfe Research. Together, North American oil-and-gas producers are losing nearly $2 billion every week at current prices, according to AlixPartners. American producers are expected to cut their budgets by 51% to $89.6 billion from 2014, according to Cowen & Co. In a biannual review by a trio of banking regulators, the value of loans rated as “substandard, doubtful or loss” among oil and gas borrowers almost quintupled to $34.2 billion, or 15% of the total energy loans evaluated. That compares with $6.9 billion, or 3.6%, in 2014.

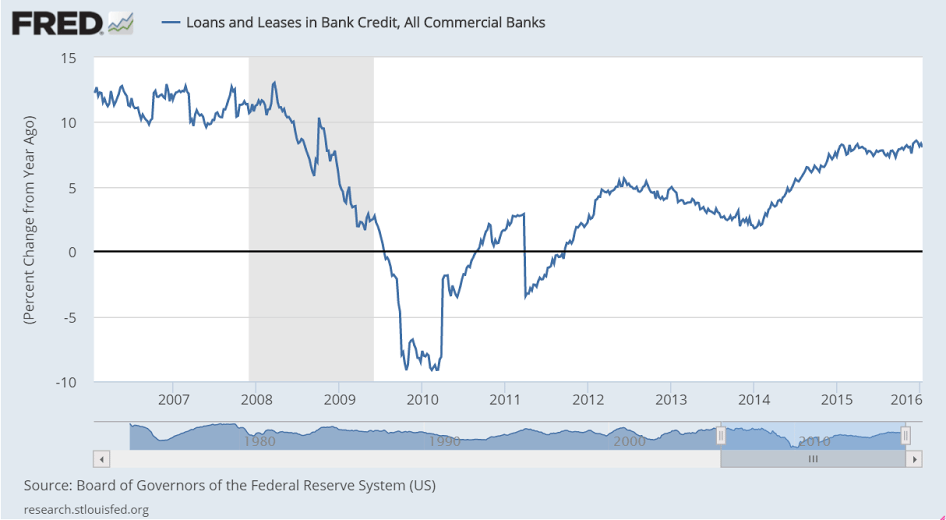

Still trending lower since the oil capex collapse a little over a year ago: