By Robert Reich

August 14 — It’s nonsense to think of the economy heading downward again into a double dip when most Americans never emerged from the first dip. We’re still in one long Big Dipper.

More people are out of work today than they were last year, counting everyone too discouraged even to look for work. The number of workers filing new claims for jobless benefits rose last week to highest level since February. Not counting temporary census workers, a total of only 12,000 net new private and public jobs were created in July — when 125,000 are needed each month just to keep up with growth in the population of people who want and need to work.

Not since the government began to measure the ups and downs of the busines cycle has such a deep recession been followed by such anemic job growth. Jobs came back at a faster pace even in March 1933 after the economy started to “recover” from the depths of the Great Depression. Of course, that job growth didn’t last long. That recovery wasn’t really a recovery at all. The Great Depression continued. And that’s exactly my point. The Great Recession continues.

Even investors are beginning to see reality. Starting in February the stock market rallied because corporate profits were rising briskly. Investors didn’t mind that profits were coming from payroll cuts, foreign sales, and gimmicks like share buy-backs — none of which could be sustained over the long term. But the rally died in April when investors began to see how paper-thin these profits actually were. And now the stock market is back to where it was at the start of the year.

What to do? First, don’t listen to Wall Street and the right.

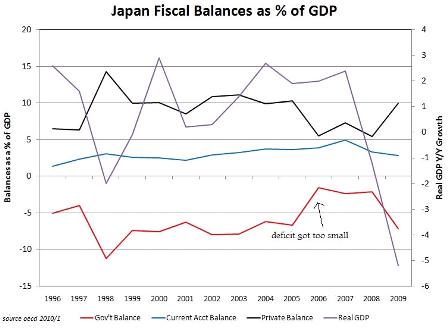

Forget the Neo-Hoover deficit hawks who day we have to cut government spending and trim upcoming deficits. We didn’t get into this mess and aren’t remaining in it because of budget deficits. In fact, the only way to reduce long-term deficits is to restore jobs and growth so government revenues rise and expenses like unemployment insurance drop.

There you go, Bob, reinforcing the myth that getting long term deficits down has value.

That makes you part of the problem, and not part of the answer.

Ignore the government haters who say we have to void or delay upcoming regulations of Wall Street and big business. We got here because Wall Street went bonkers, the housing bubble burst, and the middle class couldn’t continue to spend becuase their health-care bills were soaring and their pay was stagnating. New regulations of Wall Street and big business are necessary to avoid a repeat.

And don’t believe the supply-siders who say we have to extend the Bush tax cuts for the wealthy. Because the wealthy save rather than spend most of their incomes,

If you believe this, and understand taxing functions to regulate aggregate demand, why would you care if their taxes went up or not? Just like getting them angry?

extending their tax cut won’t do squat. And restoring their marginal tax rate to what it was under Bill Clinton won’t harm the economy. The Clinton years had the best sustained economy in American history.

The central problem is lack of demand — and that’s what has to be tackled.

Right! Which will eventually come back. The deficits are high enough for that. But there’s nothing to be gained by waiting around with maybe 20% real unemployment for private credit expansion to kick in like it did in the 90’s.

Three of the four sources of demand have stopped working. (1) Consumers can’t and won’t buy because they’re still under a huge debt load, can’t get more credit, are afraid of losing their jobs (or already have), depend on two wage earners at least one of whom is working part-time and pulling in less, or have to save. (2) Businesses won’t invest and spend on creating more jobs if they don’t see consumers willing to buy more.

Agreed on those two!

(3) Exports are stalled because the dollar is so high they cost too much, much of the rest of the world is still struggling with recession, and American firms can make things for sale abroad more cheaply abroad.

That’s a good thing- means we can have even lower taxes to sustain domestic demand and be able to buy all we can produce at full employment plus whatever the world wants to net sell to us.

That leaves only one remaining source of demand — government. We need a giant jobs program to hire people and put money in their pockets that they’ll spend and thereby create more jobs. Put ideology aside and recognize this fact. If it makes you more comfortable call it the National Defense Jobs Act. Call it the WPA. Call it Chopped Liver. Whatever, we have to get the great army of the unemployed and underemployed working again.

How about my $8/hr transition job proposal?

Also: Put more money in consumer’s wallets by eliminating payroll taxes on the first $20K of income (and make it up by applying payroll taxes to incomes over $250K.)

Why not just suspend FICA taxes entirely?

What are you afraid of?

The federal deficit?

Also: Get more hiring by giving the states and locales interest-free loans — so they can rehire all the teachers, fire fighters, police officers, and sanitation workers they’ve fired — to be repaid when their state employment rates hit 5 percent or below.

Why not simple federal revenue distributions on a per capita basis to make it fair?

What are you afraid of?

The federal deficit?

Also: Get more credit by having the Fed return to “quantitative easing” — expanding the money supply by purchasing mortgage-backed and other types of securities.

And you don’t have a clue on how monetary operations and reserve accounting work.

Otherwise you’d know this does nothing of macro consequence except take more interest income out of the private sector and shift a bit of interest from savers to borrowers.

If we let the deficit hawks and government haters dominate this debate, as they have, the Big Dipper will continue for years. The Great Depression lasted twelve.

If you’d get up to speed on monetary operations and stop supporting the deficit hawks, the true doves might have a fighting chance.

If any of you have Bob’s email address please forward this to him, thanks!