Abe revived this panel. Lots of cross pressures as to whether to increase deficit spending or not. If not, they could continue to be the land of the rising yen, as ‘monetary policy’ short of actual fx purchases doesn’t cut it.

As previously discussed, while reported reserves have remained flat since the last announced intervention, there are signs actual fx reserves have been rising from what is functionally intervention not counted as official intervention, but I can’t yet say for sure.

And note that the purchase of a US Treasury $1 trillion platinum coin would weaken the yen and put off the US debt ceiling issue…

;)

Govt Starts Talks On Fiscal Reform At Revived Key Policy Panel

TOKYO (Kyodo) — A revived Japanese government economic policy panel started discussions Wednesday on how to rehabilitate the nation’s finances in the longer term, with the government’s plan to issue more debt to fund a stimulus package stirring concern over the nation’s fiscal health.

The meeting of the Council on Economic and Fiscal Policy was the first in three and a half years. The panel had played a leading role in putting together economic and fiscal policy under the government of Prime Minister Junichiro Koizumi of the Liberal Democratic Party.

During Wednesday’s meeting of the panel revived by Prime Minister Shinzo Abe, who took office on Dec. 26, participants exchanged views on an emergency economic stimulus package slated to be approved by the Cabinet on Friday.

The government led by the LDP, which returned to power in the Dec. 16 general election after three years in opposition, also began discussions on mapping out the basic policy for an initial budget for the next fiscal year starting April and medium-to-long term economic and fiscal policy blueprints.

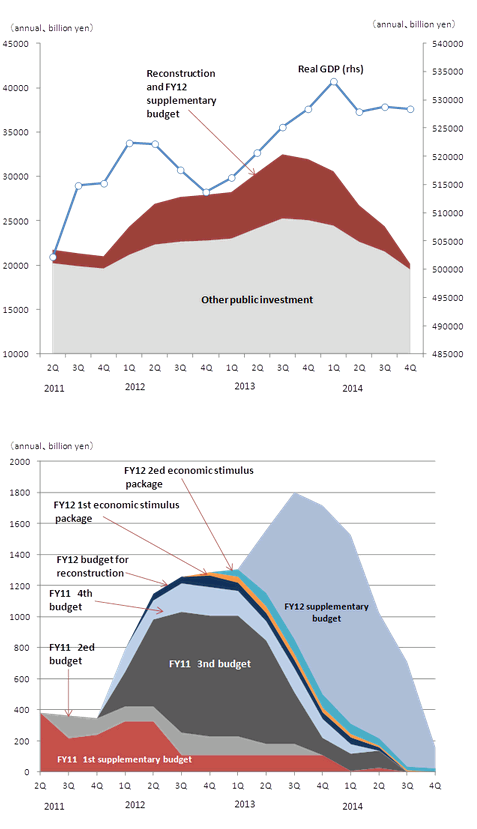

Abe’s government is considering approving an emergency stimulus package of over 20 trillion yen ($228.7 billion) to boost Japan’s slowing export-reliant economy, and compiling a 13.1 trillion yen extra budget for the current fiscal year to finance it, sources close to the matter said Tuesday.

To cover the shortfall in revenue needed to pay for the supplementary budget, Tokyo is making arrangements to issue an additional 5.2 trillion yen in construction bonds for fiscal 2012, the sources said.

The move has focused attention on how the LDP-led government will show a commitment to restoring Japan’s precarious fiscal health, the worst among major developed countries.

If fears intensify that progress on fiscal reform has stalled, long-term interest rates could spike as investors become reluctant to buy government bonds due to fears of default, dampening corporate and private investment and dragging down the broader economy, some analysts have warned.

The previous government led by the Democratic Party of Japan had set as its fiscal reform target halving Japan’s primary balance deficit — total expenditures in excess of total revenues, excluding interest payments on debt — by the end of fiscal 2015.

Abe is eager to finalize by June the basic fiscal policy, which could include a plan to put Japan on a path toward fiscal restoration, the sources said.

The Council on Economic and Fiscal Policy, first established in 2001 but put on ice after the DPJ took power in 2009, would function as the “control tower” of Japan’s macroeconomic policies, Abe has said.

The Bank of Japan governor is requested to join the council’s meetings along with business leaders and academics, with Abe saying he wants to deepen communication with the central bank chief there.

Abe has pledged to beat the nation’s chronic deflation, urging the BOJ to aggressively ease monetary policy until a 2 percent inflation rate is achieved.

Financial market participants said they are paying attention to whether Abe will put additional pressure on current BOJ Governor Masaaki Shirakawa to do more during the meeting late Wednesday, ahead of the BOJ’s Policy Board meeting on Jan. 21 and 22, at which the central bank is expected to introduce a 2 percent inflation target, as requested by Abe.