Wal-Mart CEO pushes plan to keep retailer growing

CEO Mike Duke assured shareholders that the “greatest priority” is to get its revenue at stores open at least a year — a key measure of a retailer’s health — to rise again. Shoppers are focusing on groceries and little else, said Bill Simon, president and CEO of its U.S. namesake business. He noted to reporters that it’s seeing the widest swing ever in spending around when shoppers get their paychecks. That’s making Wal-Mart scramble harder to offer smaller packages for shoppers at the end of the month and alter its staff scheduling. “Customers are struggling,” he said. Rising costs in commodities are also putting more pressure on Wal-Mart, which can’t pass big price increases along to its already-stressed shoppers.

Daily Archives: June 6, 2011 @ 10:27 am (Monday)

China- private sector also front loads lending?

Weekly Credit Graph Packet – 06/06/11

Recognizing that ‘it’s all one piece’

The rest of the credit stack seems to be moving up in yield roughly in line with equities.

The slowdown seems to be getting serious.

Hopefully the euro zone and UK haven’t yet reached the tipping point where austerity shifts from reducing deficits to adding to them (due to induced economic weakness).

And hopefully Japan decides to go with an all out reconstruction plan without increasing taxes or otherwise ‘paying for it.’

And hopefully China’s second half weakness doesn’t get out of hand.

And hopefully the US Congress doesn’t accomplish any serious near term deficit reduction.

And hopefully the Fed informs us all that QE and 0 rates reduce interest income for the economy, as indicated in Bernanke’s 2004 published paper. And therefore, as he indicated, a fiscal adjustment is called for to sustain aggregate demand at congressionally mandated levels.

Credit Graph Packet

Mike Norman!

as if the Saudis aren’t the price setter…

Oil below $115 on demand worries

June 6 (Reuters) — Brent crude slipped toward $115 a barrel on Monday as concern about demand ahead of a key OPEC meeting later this week weighed on the market.

Signs that high prices are destroying demand in the West, confirmed by the worst U.S. jobs report since September, are worrying a group of OPEC’s core members led by Saudi Arabia.

They will push for a rise in output to reduce prices and support economic growth but are expected to meet opposition from Iran and Venezuela.

“There is no need to increase OPEC production in the 159th meeting of this organisation,” said Iran’s OPEC governor, Mohammad Ali Khatibi, according to reports citing the Oil Ministry website SHANA.

Brent crude was down, while U.S. light, sweet crude slipped.

Funds Boost Bullish Commodity Bets on Global Growth Prospects

Story behind prior post on China.

Not to forget that biofuels are burning up large % of our food as motor fuel.

Funds Boost Bullish Commodity Bets on Global Growth Prospects

By Yi Tian

June 6 (Bloomberg) — Funds boosted bets on rising commodity prices to the highest in four weeks, led by copper, amid signs that the global economic recovery will remain resilient and boost demand for raw materials.

Speculators raised their net-long positions in 18 commodities by 7.3 percent to 1.26 million futures and options contracts in the week ended May 31, government data compiled by Bloomberg show. That’s the highest since May 3. Copper holdings more than doubled. A measure of bullish agriculture bets also climbed as adverse global weather curbed crop production.

The Standard & Poor’s GSCI Spot Index rose for a fourth straight week as Chinese metal inventories plunged and droughts lingered in the Asian country and Europe, trimming prospects for wheat and cotton crops. The global recovery “is gaining strength,” the Group of Eight leaders said May 27 after a summit in Deauville, France. In the U.S., consumer sentiment rose to a three-month high in May, a private report showed last month.

“We are seeing a reasonable rate of growth in worldwide economic activity,” said Michael Cuggino, who helps manage $12 billion at Permanent Portfolio Funds in San Francisco. “The supply-demand associated with that growth, combined with a weaker dollar, probably explains the move into commodities.”

Copper prices have jumped 40 percent in the past year while wheat has surged 75 percent and corn has more than doubled amid increasing demand from China and other emerging economies. Raw materials have also gained as investors boosted holdings as an alternative to the dollar, which has slumped more than 6 percent this year against a six-currency basket.

$130 Million

Investors poured $130 million into commodity funds in the week ended June 1, the second straight increase, according to EPFR Global, a Cambridge, Massachusetts-based researcher. The previous week had inflows of $702.8 million.

Managed-money funds and other large speculators boosted bullish bets on New York copper prices by 4,604 contracts to 7,304. The jump was the biggest since October 2009. Stockpiles of the metal monitored by Shanghai Futures Exchange have plunged 51 percent since mid-March.

“Destocking cannot continue indefinitely, and market participants will have to return to the market at the latest in the fourth quarter, if not for re-stocking then at least for spot purchases,” Bank of America Merrill Lynch said in a report last week.

Agriculture Bets

Speculators raised their net-long positions in 11 U.S. farm goods by 4.6 percent to 756,629 contracts as of May 31, the second straight increase. Holdings of wheat jumped 14 percent, and bets on a cotton rally gained up 12 percent, the most since August.

“It has basically been a year of the wrong weather at the wrong time, starting with the Russian droughts and then most recently excessive rains in the U.S.,” said Nic Johnson, who helps manage about $24 billion in commodities at Pacific Investment Management Co. in Newport Beach, California. Agriculture “prices could move materially higher because of low inventories and if we have below-trend yields of crops like corn.”

China Has Divested 97 Percent of Its Holdings in U.S. Treasury Bills

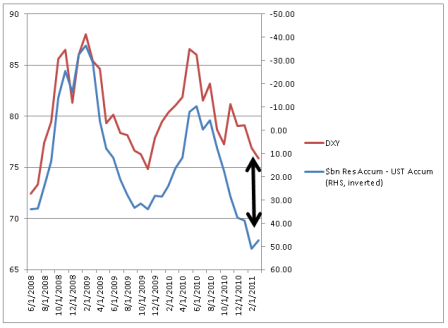

So it looks like QE2 indeed managed to scare China out of the dollar. This is the portfolio shifting previously discussed that’s been dragging down the dollar even though, fundamentally sound, as Fed Chairman Bernanke correctly stated.

And when China (and Japan) offered to buy Spanish and other euro zone national govt debt to ‘help out’, the euro zone fell for that one, watching their currency rise against their better judgement with regards to their euro wide exports.

And maybe Fed Chairman Bernanke is aware of this, and has assured China he does favor a strong dollar as per his latest public statements, and let them know that QE3 is unlikely, and has ‘won them back’? No way to tell except by watching the market prices.

And with most everyone out of paradigm with regards to monetary operations, there’s no telling what they all might actually do next.

What is known is that world fiscal balance is tight enough to be slowing things down, and looking to keep getting tighter.

And QE/lower overall term structure of rates removes interest income from the economy, and shifts income from savers to bank net interest margins.

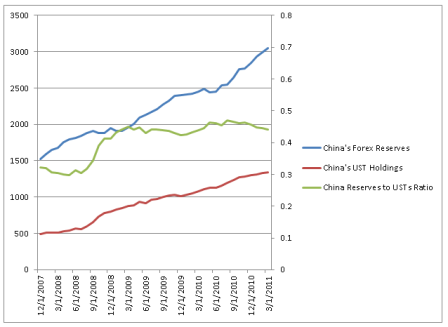

And if China’s growth is going to slow dramatically, its most likely to happen the second half as they tend to front load their state lending and deficit spending each year.

And all the while our own pension funds continue to allocate to passive commodity strategies, distorting those markets and sending out price signals that continue to bring out increasing levels of supply that are filling up already overflowing storage bins.

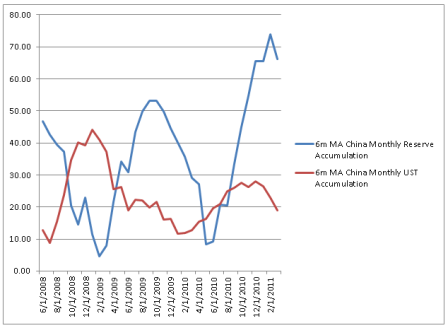

Note in particular that reserve accumulation has been high and rising recently, though UST accumulation has been moderate.

China Has Divested 97 Percent of Its Holdings in U.S. Treasury Bills

By Terence P. Jeffrey

Jun 4 (CNSNews.com) — China has dropped 97 percent of its holdings in U.S. Treasury bills, decreasing its ownership of the short-term U.S. government securities from a peak of $210.4 billion in May 2009 to $5.69 billion in March 2011, the most recent month reported by the U.S. Treasury.

Treasury bills are securities that mature in one year or less that are sold by the U.S. Treasury Department to fund the nation’s debt.

Mainland Chinese holdings of U.S. Treasury bills are reported in column 9 of the Treasury report linked here.

Until October, the Chinese were generally making up for their decreasing holdings in Treasury bills by increasing their holdings of longer-term U.S. Treasury securities. Thus, until October, China’s overall holdings of U.S. debt continued to increase.

Since October, however, China has also started to divest from longer-term U.S. Treasury securities. Thus, as reported by the Treasury Department, China’s ownership of the U.S. national debt has decreased in each of the last five months on record, including November, December, January, February and March.

Prior to the fall of 2008, acccording to Treasury Department data, Chinese ownership of short-term Treasury bills was modest, standing at only $19.8 billion in August of that year. But when President George W. Bush signed legislation to authorize a $700-billion bailout of the U.S. financial industry in October 2008 and President Barack Obama signed a $787-billion economic stimulus law in February 2009, Chinese ownership of short-term U.S. Treasury bills skyrocketed.

By December 2008, China owned $165.2 billion in U.S. Treasury bills, according to the Treasury Department. By March 2009, Chinese Treasury bill holdings were at $191.1 billion. By May 2009, Chinese holdings of Treasury bills were peaking at $210.4 billion.

However, China’s overall appetite for U.S. debt increased over a longer span than did its appetite for short-term U.S. Treasury bills.

In August 2008, before the bank bailout and the stimulus law, overall Chinese holdings of U.S. debt stood at $573.7 billion. That number continued to escalate past May 2009– when China started to reduce its holdings in short-term Treasury bills–and ultimately peaked at $1.1753 trillion last October.

As of March 2011, overall Chinese holdings of U.S. debt had decreased to 1.1449 trillion.

Most of the U.S. national debt is made up of publicly marketable securities sold by the Treasury Department and I.O.U.s called “intragovernmental” bonds that the Treasury has given to so-called government trust funds—such as the Social Security trust funds—when it has spent the trust funds’ money on other government expenses.

The publicly marketable segment of the national debt includes Treasury bills, which (as defined by the Treasury) mature in terms of one-year or less; Treasury notes, which mature in terms of 2 to 10 years; Treasury Inflation-Protected Securities (TIPS), which mature in terms of 5, 10 and 30 years; and Treasury bonds, which mature in terms of 30 years.

At the end of August 2008, before the financial bailout and the stimulus, the publicly marketable segment of the U.S. national debt was 4.88 trillion. Of that, $2.56 trillion was in the intermediate-term Treasury notes, $1.22 trillion was in short-term Treasury bills, $582.8 billion was in long-term Treasury bonds, and $521.3 billion was in TIPS.

At the end of March 2011, by which time the Chinese had dropped their Treasury bill holdings 97 percent from their peak, the publicly marketable segment of the U.S. national debt had almost doubled from August 2008, hitting $9.11 trillion. Of that $9.11 trillion, $5.8 trillion was in intermediate-term Treasury notes, $1.7 trillion was in short-term Treasury bills; $931.5 billion was in long-term Treasury bonds, and $640.7 billion was in TIPS.

Before the end of March 2012, the Treasury must redeem all of the $1.7 trillion in Treasury bills that were extant as of March 2011 and find new or old buyers who will continue to invest in U.S. debt. But, for now, the Chinese at least do not appear to be bullish customers of short-term U.S. debt.

Treasury bills carry lower interest rates than longer-term Treasury notes and bonds, but the longer term notes and bonds are exposed to a greater risk of losing their value to inflation. To the degree that the $1.7 trillion in short-term U.S. Treasury bills extant as of March must be converted into longer-term U.S. Treasury securities, the U.S. government will be forced to pay a higher annual interest rate on the national debt.

As of the close of business on Thursday, the total U.S. debt was $14.34 trillion, according to the Daily Treasury Statement. Of that, approximately $9.74 trillion was debt held by the public and approximately $4.61 trillion was “intragovernmental” debt.