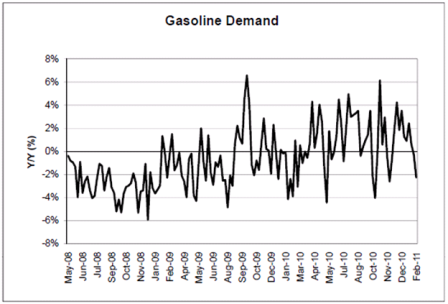

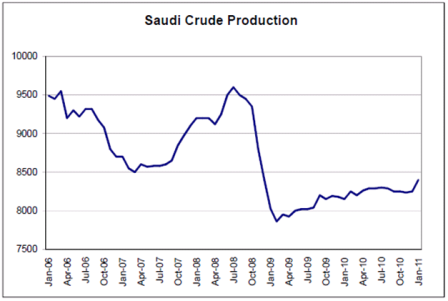

US demand continues to go nowhere, and may even be softening

And with Saudis posting prices to their refiners and letting quantity adjust, it doesn’t look like net world demand is doing much either

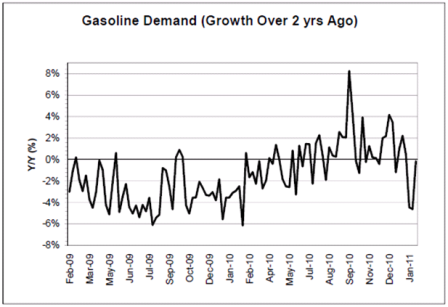

US demand continues to go nowhere, and may even be softening

And with Saudis posting prices to their refiners and letting quantity adjust, it doesn’t look like net world demand is doing much either

“If government debt and deficits were actually to grow at the pace envisioned, the economic and financial effects would be severe,” Federal Reserve Chairman Ben S. Bernanke told the House Budget Committee Feb. 9. “Sustained high rates of government borrowing would both drain funds away from private investment and increase our debt to foreigners, with adverse long-run effects on U.S. output, incomes, and standards of living.”

>

> (email exchange)

>

> On Tue, Feb 22, 2011 at 9:15 PM, wrote:

>

> Paul Krugman gave a speech at Florida Atlantic University and agreed

> to a brief meeting with our econonomics club.

>

> I thought you might enjoy the attached picture.

>

This only works to raise the cost of funds for the targeted banks.

It’s still about price, not quantity

So far the actual quantitative measures remain the govt telling its banks to lend less, or else.

That does work.

The problem is it works via a hard landing/widening output gap.

From Yang Kewei

As small and medium sized banks contributed ~70% of new loans in 2011. It makes sense the PBOC implemented punitive required reserves on them. Given that, the tight liquidity reflected on 7d repo is explainable as S&M sized banks have to borrow to meet their RRR. This gave big local banks great opportunity to squeeze on tenor repos, but o/n is still stable given ample liquidity 1) cash back to banks from households after LNY 2) pboc bill maturing (most are held by big banks) 3) FX reserve accumulation (one indicator is that o/n repo is still quite stable which signals current liquidity situation.).

One additional impact of significant net amount of PBOC bill expiring since 4Q10 is that big banks have been passively extending duration of their assets. To maintain balanced balance sheet, banks could have some adjustment on their asset allocation going fwd.

China has slapped punitive reserves on multiple banks

* First official confirmation of punitive reserve moves

* Differentiated reserves key part of central bank policy

* China is trying to slow credit and money growth

February 22 (Reuters) — China has already imposed punitive required reserve increases on more than 40 banks this year, targeting those that have issued too many loans, state news agency Xinhua reported on Tuesday.

This approach, formally known as “dynamic differentiated required reserve ratios”, has been effective in restraining lending by banks and will be continued as a core part of the government’s efforts to control inflation, Xinhua said, citing an unnamed central bank source.

The report was the first official confirmation that Beijing has been using a complex new system for tweaking mandatory reserve levels on a regular basis as a way of disciplining unruly and especially profligate banks.

China has increased reserve requirements across the board for all banks twice this year. The dynamic increases have been on top of those and can be reversed once banks fall back into line with official lending and capital guidelines.

“Since the start of 2011, the central bank has already started using dynamic differentiated required reserve ratios as a tool in its monetary and credit controls,” Xinhua said.

“It has already imposed differentiated reserve requirements on more than 40 local financial institutions that had low capital adequacy ratios, overly fast credit growth and increasing cyclical risks,” it added.

The report did not name any of the targeted banks, nor did it disclose the magnitude of the punitive reserve increases.

It did say that the central bank would continue to draw on a mixture of tools, including interest rates and required reserves, in implementing a prudent monetary policy.

NEW TOOL

A local magazine said on Monday that China had abandoned dynamic differentiated reserves because the formula for determining them was too complex, but the central bank denied that.

The Xinhua report served to underscore that differentiated reserves have, in fact, become an essential component of China’s monetary policy toolkit.

The People’s Bank of China first unveiled plans for “dynamic differentiated required reserve ratios” last year to keep a tighter leash on banks.

Higher reserves force banks to lock up more of their deposits at the central bank, inhibiting their ability to lend and slowing money growth. Excess cash in the economy has been one of the root causes of the run-up in Chinese inflation, which hit an annual pace of 4.9 percent in January, near a two-year high.

China had previously imposed differentiated reserve requirement ratios on banks as a way to punish rampant lending.

But a “dynamic differentiated” system marks a departure from the past because the central bank has been reviewing lenders’ balance sheets on an on-going basis and looking at a wider range of indicators, including lending, capital and liquidity levels.

Chinese inflation is expected to quicken in coming months as global commodity prices and domestic food costs climb.