Agreed with Karim, the relatively modest recovery remains on track.

Left alone, I see GDP in the 3.5%-5.5% range for next year, and possibly more.

Though they didn’t add much, the latest tax adjustments did take away the down side risk of taxes going up at year end.

I do, however, see several negatives with maybe up to 25% possibilities each, meaning collectively the odds of any one of them happening are a lot higher than that.

The new Congress is serious about deficit reduction. The risk is they will be successful, and it seems they even have the votes to get a balanced budget amendment passed.

China could get it wrong in their fight against inflation and cause a pretty severe slump. In fact, I can’t recall any nation that didn’t cause a widening of their output gap in their various fights against inflation.

The ECB’s imposed austerity in return for funding at some point reverses the current modest growth of that region. Not to mention the small but real risk the ECB decides to not buy any more member nation debt in the secondary markets.

While a less important economy for the world, the UK austerity looks ill timed as well.

The Saudis could continue to hike their posted prices which could reduce US demand for domestic output. The spike to the 150 level in 08 was a significant contributor to the severity of the financial collapse that followed.

There are also several lesser factors I’ve been listing the last few weeks that could cause aggregate demand to disappoint.

On the positive side is always the possibility of a private sector credit expansion taking hold.

Traditionally that would be borrowing to spend on housing and cars.

Federal deficit spending has done its job of restoring incomes and monetary savings, and will continue to do so.

Financial burdens ratios are down, car sales are showing some modest growth, and housing looks to have at least bottomed. And both are at low enough levels where there could be a lot of growth and they’d still be very low, especially housing.

I don’t see inflation as a risk (unless crude spikes a lot higher), nor deflation (unless one of the above shocks kicks in).

And I do see the ‘because we think we could be the next Greece we’re turning ourselves into the next Japan’ theme continuing, as it seems highly unlikely to me we will get back to, say, the 4% unemployment level for a very long time, if ever, until there’s a paradigm change regarding fiscal policy.

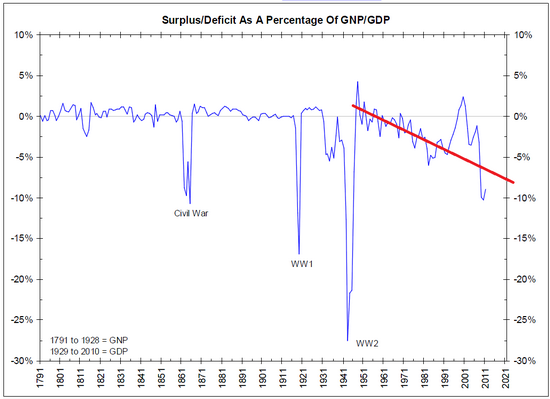

The full employment budget deficit might be up to 4% of GDP or higher, and our current tax structure probably still delivers a cycle ending surplus at full employment.

In other words, with our current tax structure and size of govt, full employment remains unsustainable.

Lastly, my feel is that there’s about a better than even chance of an equity and commodity sell off. Stocks as well as commodities look like they are pretty much pricing in all the good economic news, some of which is bogus, like QE being inflationary, as previously discussed. There could also be dollar strength which would contribute to equity and commodity weakness. And the stock and commodity weakness would also work to bring the term structure of rates lower as well, particularly as rates seem to have gone higher recently more due to supply factors during a holiday week and maybe year end selling than anything else. The forwards ED forwards don’t look to me to be at all low with respect to mainstream expectations of future fed rate settings. And it also looks like the annual portfolio rebalancing will be that of selling stocks which went up last year and buying bonds which went down, to get all the portfolio ratios back in line with marching orders from higher ups.

HNY!!!

Karim Basta wrote:

· Another major milestone in the recovery story.

· Initial claims fall below 400k for the first time since summer 2008;dropping 34k for the week to 388k.

· Labor department states ‘no special factors’ in the data.

I recall a senior Fed official once telling me if he were stranded on a desert island and could only receive 1 data point to keep up with the direction of the U.S. economy that it would be initial claims. So forecasts likely being revised higher as I write this.