>

> Here is the original one we did for the CFEPS digest

>

Full size image

Even at the right price, investing in single family houses to put them up for rent is a tough trade:

Investors are moving out of housing. Here’s why

By Diana Olick

July 22 (CNBC) — They swarmed the distressed housing market, buying thousands of foreclosed properties and pushing prices higher faster than anyone expected. Now investors are pulling back, dissuaded by the higher prices they themselves brought about.

“Perhaps the numbers aren’t working out,” said Lawrence Yun, chief economist of the National Association of Realtors, which reported that just 15 percent of June sales were by investors. That is the lowest share since the association began tracking this cohort in October 2008.

Current homeowners are now driving the housing market, as even investor traffic fell in June for the fourth straight month, according to Campbell/Inside Mortgage Finance. That could mean slower sales going forward, as still tight inventory keeps move-up buyers in place. That, and negative home equity.

Seriously!

:(

Here’s what could make or break Abe’s reform plan

By Dhara Ranasinghe

July 22 (Bloomberg) — If Japan’s Prime Minister Shinzo Abe, riding high on Sunday’s election victory for his ruling coalition, is serious about transforming the economy, it’s crucial that he pushes ahead with plans to raise a controversial consumption tax, analysts say.

The tax on goods and services, under the current law, is due to rise to 8 percent next April from 5 percent and to 10 percent in 2015, although there has been a heated debated within the government as to whether this should happen.

On the one hand a consumption tax is seen as a key measure to improving Japan’s fiscal health. Japan, the world’s third biggest economy, has a debt pile that is the highest among industrialized nations and its debt-to-GDP ratio is expected to top 245 percent this year.

But on the other hand, the tax could hurt consumer spending and stifle the economic recovery Abe is trying to engineer through a mix of fiscal spending and aggressive monetary stimulus.

“The decision on whether to raise the sales tax as early as next April is a finely balanced one with significant implications – both for the economy and for the perceived credibility of Abenomics,” said Nicholas Spiro, managing director at Spiro Sovereign Strategy.

“The last consumption tax increase in Japan ended in disaster, helping trigger a recession. Yet if Mr Abe puts it off, doubts about the fiscal credibility of his project will grow, potentially spooking the bond market,” he added

First, this isn’t even being reported on CNBC and is only way down on Bloomberg’s website.

Second, this is the last thing an economy faced with a demand shock from tax hikes and sequesters needs. Housing is the sector of hope for agents’ spending more than their incomes to offset the mounting demand leakages.

Third, the Fed Chairman’s remarks regarding fiscal headwinds having more effect than expected and continuing longer than expected have largely gone unreported as well. He’s right, of course, and in fact the ‘permanent’ deficit reduction is just that, and not only doesn’t go away but makes the fiscal headwinds of the automatic stabilizers that much more of an obstacle.

Fourth, seems ‘confidence’ isn’t all it’s been cracked up to be, as previously discussed…

Housing Starts in U.S. Unexpectedly Fall to Lowest in a Year

Starts of new U.S. homes unexpectedly fell in June to the lowest level in almost a year, indicating a pause in the industry’s progress.

Work began on 836,000 houses at an annualized rate last month, the least since August 2012 and down 9.9 percent from a revised 928,000 pace in May, figures from the Commerce Department showed today in Washington. The reading was weaker than projected by any economist in a Bloomberg survey, and permits for future projects also declined.

The decline was led by a slump in multifamily projects, which can be volatile, and the level of permits remained higher than starts, which may point to a rebound this month. A limited supply of land is also a hurdle for housing, even as near record-low mortgage rates and improving job opportunities draw buyers.

“Housing will continue to grow, but it will be at a gradual pace,” Sean Incremona, a senior economist at 4Cast Inc. in New York and the top forecaster for housing starts in the past two years, according to data compiled by Bloomberg, said before the report.

The median estimate of 83 economists surveyed by Bloomberg was for a 960,000 rate. Forecasts ranged from a 915,000 pace to a 1.03 million rate after an initially reported 914,000 annualized rate in May.

Building permits decreased 7.5 percent to a 911,000 annualized rate in June, compared to a median forecast of 1 million.Single Family

Construction of single-family houses fell 0.8 percent to a 591,000 rate, the fewest since November, from 596,000 the prior month.

Work on multifamily projects such as apartment buildings slumped 26.2 percent to an annualized rate of 245,000, the lest since August 2012.

Karim writes:

Something for everyone (even uses on the other hand in his remarks); base case remains in place for tapering in September. First mention Ive seen on nature of rate hike cycle: will be gradual. Seems to be looking past the first hike!

Sequencing in these paragraphs is telling. Base case first; risks second(bold). Same pattern appeared in the Minutes. Effective way to stick to your forecast but to try and keep rates in check.

Same for Tapering:

6.5% threshold and first mention (that Ive seen) on the pace of rate hikes

All unspent income is called a ‘demand leakage’ as it means the output can’t get sold unless another agent spends more than his income. (by identity, not ‘theory’) And unsold output leads to cuts in output, cuts in employment, etc. etc. and down you go until some agent spends enough more than his income to offset the demand leakages. Invariably that agent is govt, as the automatic fiscal stabilizers increase the deficit. Of course they also work in reverse, providing an increasing headwind to the economy as it grows, via higher revenues and lower transfer payments. Like what’s happening now, which has brought the deficit down dramatically over the last few of years..

Anyway, when a bank has income and pays it out as shareholder income, that’s not a demand leakage. And if the shareholders don’t spend their income, that is a demand leakage. etc.

But if a bank earns income and doesn’t pay it out or spend it, but instead lets its equity capital increase, that is a demand leakage.

So what’s happening in general is top line growth is pretty much flat, with earnings not being spent, but instead adding to net worth and therefore the earnings are demand leakages. This includes the housing agencies/banks who are now turning over their incomes to govt.

Remember this from the Fed?

The Automatic Stabilizers: Quietly Doing their Thing

By Darrel S. Cohen and Glenn R. Follette

Abstract: This paper presents theoretical and empirical analysis of automatic fiscal stabilizers, such as the income tax and unemployment insurance benefits. Using the modern theory of consumption behavior, we identify several channels–insurance effects, wealth effects and liquidity constraints- -through which the optimal reaction of household consumption plans to aggregate income shocks is tempered by the automatic fiscal stabilizers. In addition we identify a cash flow channel for investment. The empirical importance of automatic stabilizers is addressed in several ways. We estimate elasticities of the various federal taxes with respect to their tax bases and responses of certain components of federal spending to changes in the unemployment rate. Such estimates are useful for analysts who forecast federal revenues and spending; the estimates also allow high- employment or cyclically-adjusted federal tax receipts and expenditures to be estimated. Using frequency domain techniques, we confirm that the relationships found in the time domain are strong at the business cycle frequencies. Using the FRB/US macro-econometric model of the United States economy, the automatic fiscal stabilizers are found to play a modest role at damping the short-run effect of aggregate demand shocks on real GDP, reducing the “multiplier” by about 10 percent. Very little stabilization is provided in the case of an aggregate supply shock.

GDP measures domestic spending on output, and when it falls for any reason there is that much less reason to employ, unless productivity is falling fast enough, which generally isn’t the case.

When govt ‘gets out of the way’ with sequesters, income and jobs vanish, as does spending that depended on that income and employment. Likewise, tax increases remove funds that were supporting spending, output, and employment. Of note I just read that consumer spending is now forecast to decelerate further to something under 3% for Q2.

What ‘remains’ is an economy with that much less ‘external funding’, which is then relying on ‘internal’ increased deficit spending to fund its ongoing demand leakages. Not to forget the ‘automatic fiscal stabilizers’ which means to grow the ‘forces of growth’ have to be strong enough (enough credit expansion) to accommodate govt incrementally removing funding via higher tax payments and reduced transfer payments associated with growth.

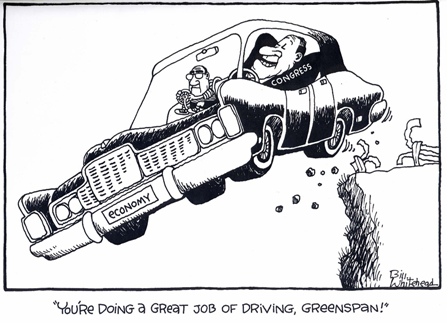

Meanwhile, markets are supported by confidence that QE is the ‘Bernanke put’/safety net that can reverse any decline by simply increasing it as needed, when in fact we are flying without a net.

And the trajectory, to me, at the moment, continues to look downward- the stuff of bursting bubbles.

Today’s industrial production releases, attached, support the same continuing modest deceleration theme.

So let’s hope mtg apps are up sharply tomorrow, and claims down sharply Thursday!