MMT interview:

Defining the Modern Monetary Theory

As in the US, with a large federal budget deficit consumers can spend out of income rather than debt and the economy do reasonably well.

And should they start spending out of both income and debt it gets that much better.

Bank of England Interest Rates to Reach 8% by 2012, Lilico Says

By Scott Hamilton

Aug. 23 (Bloomberg) — Bank of England policy makers will

raise the benchmark interest rate to about 8 percent in 2012 to

combat surging inflation sparked by “explosive” economic

growth, Policy Exchange Chief Economist Andrew Lilico said.

Annual consumer-price gains may accelerate to more than 6

percent in two years as officials expand bond purchases and keep

the interest rate at a record low of 0.5 percent to fight the

threat of a renewed recession, Lilico said in a telephone

interview from the London-based research group today.

While “a dip down in the economy” will slow interest-rate

increases, that will leave the Bank of England “behind the

curve” when it needs to tackle inflation, Lilico said.

The U.K. economy grew 1.1 percent in the second quarter in

the fastest expansion for four years. Bank of England Governor

Mervyn King said this month that inflation, at 3.1 percent in

July, has been faster than officials forecast and may keep

exceeding the government’s upper 3 percent limit into next year.

“The scope for a very strong recovery is definitely

there,” Lilico said. “Once it’s going they’ll find it very

hard to control because the growth will explosive. They’ll get a

big boom and then they’ll have to tighten hard. Our ideas of

what a normal interest rate is to deal with a boom need to be a

bit more realistic than they are now.”

Bank of England officials this month maintained emergency

stimulus to aid the economy during the biggest budget squeeze

since World War II.

Policy makers “need to do enough in terms of keeping

interest rates low and probably doing additional quantitative

easing to avoid that double dip turning into a double slump,”

Lilico said. “It’s not that policy makers are getting it wrong

— they’re getting it right — I just think the consequences of

them getting it right will in the end be inflation.”

U.K. Consumer Finance, Business Confidence Show Weakness

By Craig Stirling

Aug. 23 (Bloomberg) — A U.K. index of consumer finances

stayed close to the lowest level in almost a year in August and

a quarterly gauge of business confidence weakened, evidence

Britain’s economic recovery may be waning.

The measure of finances, based on a survey of 2,000

households, was at 37.9, little changed from July’s reading of

37.2, Markit Economics Ltd. and YouGov Plc said in an e-mailed

statement today. Readings below 50 indicate deterioration. The

index of business confidence fell 4 points in the third quarter

to 21.5, Grant Thornton and the Institute of Chartered

Accountancy in England and Wales said, citing a survey of 1,000

members.

“A downbeat mood spans the household income spectrum, but

remains most acute amongst the lowest earners,” Tim Moore, an

economist at Markit, said in the statement. “Household finances

continue to suffer from a backdrop of squeezed disposable

income, stubbornly high inflation and ongoing public sector

spending cuts.”

While economists predict gross domestic product data this

week will confirm Britain had its best growth since 2006 in the

second quarter, surveys have signaled the pace of expansion may

have weakened since then. Bank of England policy makers kept

open the option of adding emergency stimulus this month to aid

the economy as public-spending cuts loom.

Grant Thornton and the ICAEW conducted their quarterly

survey by telephone from April 29 to July 22. YouGov collected

responses online for the monthly Markit household survey.

Still feels like the weakness is coming out of events in the euro zone,

as evidenced by the euro going down as gold goes up phenomena re emerging

It’s all being held together by the ECB buying national govt debt in the secondary market.

The question I’ve seen, is how long can the ECB keep doing this/what are the limits?

The short answer is there are no nominal limits, just political limits.

And the political limit is tolerance of inflation, and inflation control is their single mandate.

They don’t want deflation or inflation.

They are buying national govt debt to prevent a euro zone wide deflationary collapse.

So how much can they buy before it’s all inflationary?

Inflation comes from spending.

Traditionally, knowing the ECB is buying your debt and that you can’t default opened the door to moral hazard issues

A nation being supported would expand spending as much as possible.

But the ECB is first imposing ‘terms and conditions’ to prevent that before buying the national govt bonds.

So not only is (deficit) spending not being expanded, it is being cut back.

And, in any case, the euro zone national govts are complying with ECB demands, directly or indirectly.

So if it doesn’t work, it’s up to the ECB to implement alternative strategies.

It would make no sense for the ECB to cut off funding because an ECB directed policy fails.

With the ECB directly or indirectly in control of member nation fiscal policy,

And with no one increasing their spending in any material way,

I don’t see a demand pull inflation possible as a function of ECB securities buying, no matter how large.

And with deficits over there already high enough for at least modest growth, which seems to be materializing,

it will be a while before fiscal gets too tight for modestly positive growth.

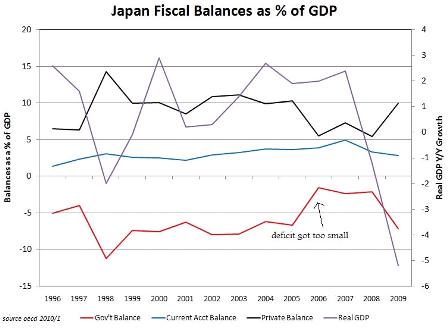

I suggest we be careful about letting our deficit get too small like Japan did should our economy begin to recover.

And if we do, I suggest we stand ready to reverse any decline in the deficit immediately should things begin to turn south.

The right size deficit is the one that coincides with full employment.

And it’s the same size deficit that coincides with ‘net savings desires’ for that currency.

This varies from nation to nation, and also over time with changing financial conditions.

Good news on the proposed ‘stimulus’ even in the face of 200% type debt to GDP ratios.

Someone over there must get it?

They obviously don’t like the way the yen is going, which calls for deficit spending to reverse it.

(Budget deficits are like bumper crops, which put downward pressure on the price of the crop. Budget surpluses are like crop failures which do the reverse)

The off balance sheet way to deficit spend to weaken the yen is to buy fx, as they used to do, and, from the charts on their US Tsy holdings, they may currently be quietly doing just that.

The other way is to cut taxes to spur private sector demand, or increase govt spending to provide more public goods.

The exporters like the latter even though it does add to private sector demand some.

Japan Headlines,

Govt To Mull Extra Stimulus: Arai

Kan Says Govt Considering Additional Economic Stimulus

Inventory, Capital Spending Fall Short Of Economist Estimates

Forex: Dollar Remains in Lower Y85 Range in Tokyo on Weak US Data

Stocks: Nikkei Hits New 2010 Closing Low;Firmer Yen Trips Tech Shares

Bonds: JGB Yields At Multi-Year Lows On Views BOJ May Ease Policy

Govt To Mull Extra Stimulus: Arai

TOKYO (NQN)–Minister of Economy and Fiscal Policy Satoshi Arai said Tuesday the government will start discussing extra stimulus measures later this week.

“From around Friday, we’ll begin discussions on whether to implement (an additional pump-priming package),” Arai said in a speech at a Tokyo hotel that afternoon.

As for the need to compile a supplementary fiscal 2010 budget to finance the extra measures, “Prime Minister Naoto Kan will start hearing from ministries and agencies involved from Friday,” the minister said.

Kan Says Govt Considering Additional Economic Stimulus

TOKYO (Nikkei)–Prime Minister Naoto Kan said Monday that the government may offer another round of stimulus measures in a bid to underpin the economy.

On Monday, Kan instructed Minister of Economy and Fiscal Policy Satoshi Arai, Minister of Finance Yoshihiko Noda and Minister of Economy, Trade and Industry Masayuki Naoshima to examine the current economic conditions and report back with specific proposals.

Japan’s preliminary real gross domestic product showed a tepid 0.4% growth for the April-June quarter, while a strong yen and weak stocks threaten to derail the economic turnaround. “We need to closely monitor developments, along with currency conditions,” Kan told reporters at his official residence.

The stimulus steps could include extending such consumer spending incentives as the eco-point program for energy-saving electronics, which is set to expire at the end of December. Programs to support job-hunting graduates and measures to aid small and midsize businesses beleaguered by a strong yen are also believed to be in the works.

The government is expected to have around 900 billion yen in leftover funds in the fiscal 2010 budget originally earmarked for the economic crisis and regional revitalization. And an additional 800 billion yen of surplus money from the fiscal 2009 budget gives it a combined 1.7 trillion yen to fund additional stimulus.

But government officials are reluctant to increase bond issuances, citing concerns about the nation’s deteriorating finances.

(The Nikkei Aug. 17 morning edition)

Forget a Double Dip. We’re Still in One Long Big Dipper.

By Robert Reich

August 14 — It’s nonsense to think of the economy heading downward again into a double dip when most Americans never emerged from the first dip. We’re still in one long Big Dipper.

More people are out of work today than they were last year, counting everyone too discouraged even to look for work. The number of workers filing new claims for jobless benefits rose last week to highest level since February. Not counting temporary census workers, a total of only 12,000 net new private and public jobs were created in July — when 125,000 are needed each month just to keep up with growth in the population of people who want and need to work.

Not since the government began to measure the ups and downs of the busines cycle has such a deep recession been followed by such anemic job growth. Jobs came back at a faster pace even in March 1933 after the economy started to “recover” from the depths of the Great Depression. Of course, that job growth didn’t last long. That recovery wasn’t really a recovery at all. The Great Depression continued. And that’s exactly my point. The Great Recession continues.

Even investors are beginning to see reality. Starting in February the stock market rallied because corporate profits were rising briskly. Investors didn’t mind that profits were coming from payroll cuts, foreign sales, and gimmicks like share buy-backs — none of which could be sustained over the long term. But the rally died in April when investors began to see how paper-thin these profits actually were. And now the stock market is back to where it was at the start of the year.

What to do? First, don’t listen to Wall Street and the right.

Forget the Neo-Hoover deficit hawks who day we have to cut government spending and trim upcoming deficits. We didn’t get into this mess and aren’t remaining in it because of budget deficits. In fact, the only way to reduce long-term deficits is to restore jobs and growth so government revenues rise and expenses like unemployment insurance drop.

There you go, Bob, reinforcing the myth that getting long term deficits down has value.

That makes you part of the problem, and not part of the answer.

Ignore the government haters who say we have to void or delay upcoming regulations of Wall Street and big business. We got here because Wall Street went bonkers, the housing bubble burst, and the middle class couldn’t continue to spend becuase their health-care bills were soaring and their pay was stagnating. New regulations of Wall Street and big business are necessary to avoid a repeat.

And don’t believe the supply-siders who say we have to extend the Bush tax cuts for the wealthy. Because the wealthy save rather than spend most of their incomes,

If you believe this, and understand taxing functions to regulate aggregate demand, why would you care if their taxes went up or not? Just like getting them angry?

extending their tax cut won’t do squat. And restoring their marginal tax rate to what it was under Bill Clinton won’t harm the economy. The Clinton years had the best sustained economy in American history.

The central problem is lack of demand — and that’s what has to be tackled.

Right! Which will eventually come back. The deficits are high enough for that. But there’s nothing to be gained by waiting around with maybe 20% real unemployment for private credit expansion to kick in like it did in the 90’s.

Three of the four sources of demand have stopped working. (1) Consumers can’t and won’t buy because they’re still under a huge debt load, can’t get more credit, are afraid of losing their jobs (or already have), depend on two wage earners at least one of whom is working part-time and pulling in less, or have to save. (2) Businesses won’t invest and spend on creating more jobs if they don’t see consumers willing to buy more.

Agreed on those two!

(3) Exports are stalled because the dollar is so high they cost too much, much of the rest of the world is still struggling with recession, and American firms can make things for sale abroad more cheaply abroad.

That’s a good thing- means we can have even lower taxes to sustain domestic demand and be able to buy all we can produce at full employment plus whatever the world wants to net sell to us.

That leaves only one remaining source of demand — government. We need a giant jobs program to hire people and put money in their pockets that they’ll spend and thereby create more jobs. Put ideology aside and recognize this fact. If it makes you more comfortable call it the National Defense Jobs Act. Call it the WPA. Call it Chopped Liver. Whatever, we have to get the great army of the unemployed and underemployed working again.

How about my $8/hr transition job proposal?

Also: Put more money in consumer’s wallets by eliminating payroll taxes on the first $20K of income (and make it up by applying payroll taxes to incomes over $250K.)

Why not just suspend FICA taxes entirely?

What are you afraid of?

The federal deficit?

Also: Get more hiring by giving the states and locales interest-free loans — so they can rehire all the teachers, fire fighters, police officers, and sanitation workers they’ve fired — to be repaid when their state employment rates hit 5 percent or below.

Why not simple federal revenue distributions on a per capita basis to make it fair?

What are you afraid of?

The federal deficit?

Also: Get more credit by having the Fed return to “quantitative easing” — expanding the money supply by purchasing mortgage-backed and other types of securities.

And you don’t have a clue on how monetary operations and reserve accounting work.

Otherwise you’d know this does nothing of macro consequence except take more interest income out of the private sector and shift a bit of interest from savers to borrowers.

If we let the deficit hawks and government haters dominate this debate, as they have, the Big Dipper will continue for years. The Great Depression lasted twelve.

If you’d get up to speed on monetary operations and stop supporting the deficit hawks, the true doves might have a fighting chance.

If any of you have Bob’s email address please forward this to him, thanks!

Negative headline for a slight miss, and 3.8% top line growth and double digit earnings growth year over year.

And that is in Q2 where GDP growth was probably only 1% or so, and still looking a bit higher for Q3, supported by ongoing 8%+ federal budget deficits.

Not a good economy for sure, as shockingly high unemployment continues and the federal govt does nothing to further support aggregate demand, because they all believe the myth that the federal govt has run out of money and in order to spend have to borrow from the likes of China and leave the debts for our children to pay back.

Lowe’s results miss estimates

August 16th (Reuters) — Home improvement chain Lowe’s Cos

missed quarterly profit and sales estimates as benefits from the homebuyer tax credit and cash for appliances programs waned.

Net income rose to $832 million, or 58 cents a share, in the second quarter ended July 30 from $759 million, or 51 cents a share, a year earlier.

Analysts on average were expecting 59 cents a share, according to Thomson Reuters I/B/E/S.

Sales rose 3.8 percent to $14.36 billion, but missed the average estimate of $14.52 billion.

I’ve been on the road, and not as close to things as usual, so from what I’ve seen and heard:

Looking at the market prices I’d guess yesterday’s sell off was a euro zone credit response.

The euro dropped a quick 3% and gold went up enough to be up even in dollars.

When Europeans get scared they often run to gold and dollars.

The ECB reportedly bought some Irish paper, indicating concern and also showing they will continue to support national govt funding.

Liquidity is not what it used to be. Sudden violent moves can just as easily be due to relatively small buyers and sellers and not any kind of fundamental shift. It can all reverse just as quickly as it sold off.

I’d key off the euro. It was up a tad last I checked, and stocks were stabilizing.

The fact that q2 earnings were very strong even as Q2 GDP was not so strong is a good sign for stocks.

Congress has extended unemployment benefits, approved 26 billion for the states, and is toying with extending the tax cuts set to expire, all indicating there will not be any serious deficit reduction interference for at least the rest of the year.

Last I checked Federal revenues had bottomed and were starting to rise indicating an underlying positive tone to the economy.

8%+ continuing Federal deficits are a very large tailwind that I expect to keep GDP in positive territory.

Weekly claims are on the high side, but not at double dip levels and continuing claims continue to fall. And the combo of hours worked and new jobs shows ongoing improvement.

Lack of consumer credit expansion (borrow to buy) keeps it all moderate, though poised for expansion as debt to income ratios have continued to fall due to the federal deficits.

Federal deficits have added to net financial assets and incomes of households, allowing them to spend from income and also add to savings, as indicated by firm final demand in the Q2 GDP revisions.

Lastly, Q3 has shown declines in a variety of markets over the last few years making rear view mirror traders more than cautious.