If these numbers don’t turn up q2 gdp could be a lot worse than q1:

Real consumer spending revised up a bit, and not to forget that includes health care premiums, and q2 now looking a lot worse than previously expected:

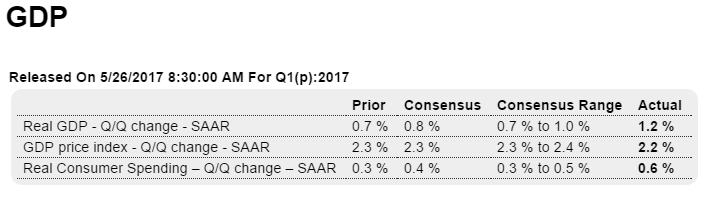

Highlights

First-quarter GDP gets a small but much needed upgrade, now at a 1.2 percent rate of annualized growth which is nearly double the advance estimate. The gain is centered where it is best, in consumer spending where the rate did double to 0.6 percent. This is still slow but is an improvement with durable goods, at minus 1.4 percent, showing less contraction and services showing greater growth, at 0.8 percent.

Boosted by strong and sudden acceleration in both structures and equipment, nonresidential fixed investment is also upgraded, to 11.4 percent for a 2 percentage point gain. Government purchases are also upgraded, down 1.1 percent for a 6 tenths improvement that pulls less on GDP. Other readings are stable with a slowing build in inventories still a major negative (a negative for GDP but not for the second-quarter outlook).

But the second-quarter outlook, which was once very positive, is mostly in question following a run of weak data for April including this morning’s durable goods report. And the first-quarter is a little less of an easy comparison now for the second quarter where early estimates, once as high as 3 and 4 percent, have been coming down to the 2 percent area.

Should muddle through at modest levels of growth:

Highlights

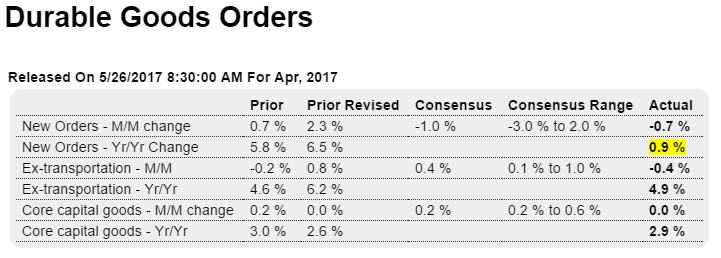

Yet another piece of the second-quarter puzzle is not favorable. Durable goods orders, down 0.7 percent in April, do not confirm the month’s big jump in industrial production nor all the strength in the regional factory reports. Aircraft is not a factor in today’s report as the ex-transportation reading is also negative, at minus 0.4 percent which is well below Econoday’s low estimate. Also below the estimate are orders for core capital goods (nondefense ex-aircraft) which came in unchanged following a downward revised unchanged reading in March.

Manufacturing output soared in the industrial production report but shipments in this report fell 0.3 percent and follow March’s 0.1 percent decline. Shipments of core capital goods, which are an important input into second-quarter GDP, also fell 0.1 percent. And the weakness in capital goods orders does not point to shipment strength in June or July.

Inventories edged only 0.1 percent higher but, given the decline in shipments, the inventory-to-shipments ratio moved one notch higher to a less lean 1.69. A plus in the report is unfilled orders which, after long contraction, have put together two straight positive months, at 0.2 and 0.3 percent.

Another positive is an upward revision to March, but that was back in the first quarter which was already weak anyway. There really aren’t a lot of positives in today’s report. The nation’s factory sector, despite recovery in energy equipment, is not showing the promise indicated by sentiment reports. Weak foreign demand remains a likely suspect for the struggling performance.

As previously discussed, seems to me it’s unlikely any of the trumped up expectations will

come to pass:

McConnell: ‘I don’t know how we get to 50’ votes on ObamaCare repeal (The Hill) Senate Majority Leader Mitch McConnell says he doesn’t know how Senate Republicans are going to get enough votes to pass an ObamaCare replacement bill. “I don’t know how we get to 50 [votes] at the moment. But that’s the goal,” McConnell told Reuters in an interview Wednesday. McConnell opened the interview by saying “There’s not a whole lot of news to be made on healthcare.” The majority leader expressed more optimism about tax reform, calling chances for passage “pretty good” and saying it is “not in my view quite as challenging as healthcare.”

So much for the border tax and eliminating business interest deductions:

Ryan: House could pass bill that doesn’t include border tax (The Hill) Speaker Paul Ryan said Wednesday that he can see a scenario in which the House passes a tax reform bill that does not include a border-adjustment tax. Ryan said that congressional Republicans and the White House agree on about 80 percent of the elements of tax reform and are discussing how to broaden the tax base to pay for lower tax rates. “A border adjustment basically taxes the trade deficit, gets you revenue to lower your tax rates,” he said. “If you’re not going to tax our trade deficit, like every other country does, then you’ll have to get your base broadening from within the country. And that’s the kind of conversation we’re going to have all summer long.”

Mnuchin wants to keep deduction for businesses’ interest expenses (The Hill) “On the business tax, my preference is to maintain interest deductibility, which is important for small- and medium-sized businesses,” Treasury Secretary Steven Mnuchin said during a House Ways and Means Committee hearing. Mnuchin added, however, that the administration is looking at the deduction “like everything else that’s on the table.” The House GOP blueprint proposes eliminating the deduction for businesses’ net interest expenses because it would instead allow businesses to immediately deduct the full costs of their capital investments.

Nor has this stuff gone away:

Freedom Caucus opposes clean debt ceiling increase (The Hill) The conservative House Freedom Caucus said on Wednesday that it opposed a “clean” increase of the debt ceiling. “We oppose any clean raising of the debt ceiling, we call for the debt ceiling to be addressed by Congress prior to the August Recess, and we demand that any increase of the debt ceiling be paired with policy that addresses Washington’s unsustainable spending by cutting where necessary, capping where able, and working to balance in the near future,” an official statement from the caucus said. If all 30 members of the Freedom Caucus oppose a “clean” increase, the House would need Democratic support in order to raise the debt ceiling.

No comment…

;)

Trump slams North Korea leader as a ‘madman’ who cannot be let on the loose (Reuters) In a call last month with the Philippines’ president, U.S. President Donald Trump described North Korea’s leader Kim Jong Un as a “madman with nuclear weapons” who could not be let on the loose, according to a leaked Philippine transcript of their call.

And 100 years ago, in the year 2017, we now have evidence that the mighty tech gurus had no idea how their own monetary system worked:

Mark Zuckerberg joins Silicon Valley bigwigs in calling for government to give everybody free money

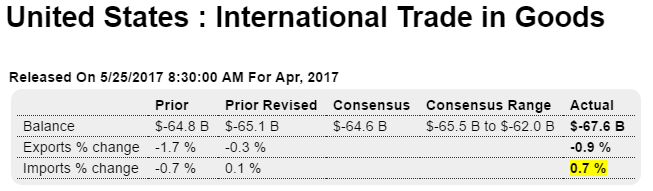

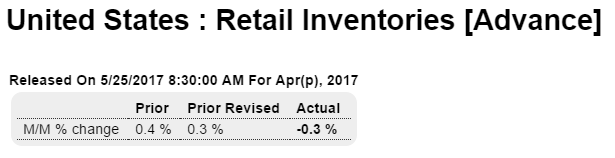

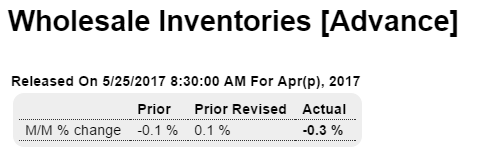

Larger than expected and last month revised higher, indicating GDP was a bit lower than estimated, and weak sales matched with weak inventories don’t clear the shelves:

Highlights

A key early indication on the strength of second-quarter GDP is not favorable as the nation’s goods deficit widened $2.5 billion in April to $67.6 billion. Exports of goods continue to show weakness, down 0.9 percent in the month to $125.9 billion that show sharp declines for vehicles and consumer goods. Imports of goods, which are a subtraction in the national accounts, rose 0.7 percent in the month with consumer goods and agriculture both rising.

Highlights

Also released with this report are advance data on wholesale and retail inventories, both down 0.3 percent in the month and also negatives for GDP.

A widening trade deficit that includes a weakening in exports is a negative for the economy, pointing to currency outflow and soft global demand. In contrast, the draws in inventories, though negatives for GDP, are positives for the outlook, lowering the risk of unwanted overhang and pointing to the promise of having to rebuild stocks.

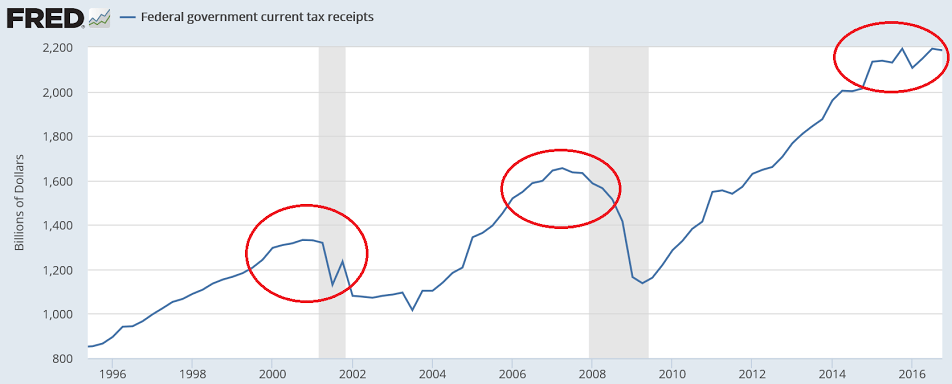

Mnuchin asks for clean debt ceiling increase before August

“My understanding is that the receipts currently are coming in a little bit slower than expected, and you may soon hear from Mr. Mnuchin regarding a change in the date,” Mulvaney said at a House Budget Committee hearing.

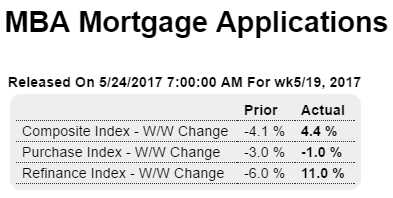

Not good:

Highlights

Purchase applications for home mortgages fell a seasonally adjusted 1 percent in the May 19 week, but refinancing applications rose 11 percent from the previous week to the highest level since March. The drop in purchase applications follows a 3 percent decrease in the prior week and takes the year-on-year purchase index gain down 6 percentage points to 3 percent. Lower rates during the week gave a big boost to refinancing, and the refinancing share of mortgage activity rose to 1.8 percentage points to 43.9 percent. The average interest rate on 30-year fixed-rate conforming mortgages ($424,000 or less) fell to the lowest level since November 2016, down 6 basis points from the prior week to 4.17 percent. The second weekly decline in purchase applications despite more attractive mortgage rates casts further doubts on the strength of the housing market, which opened the year strongly but may be slowing during the Spring selling season, as seen in the significant weakness shown yesterday’s new home sales report for April and housing starts reported last week.

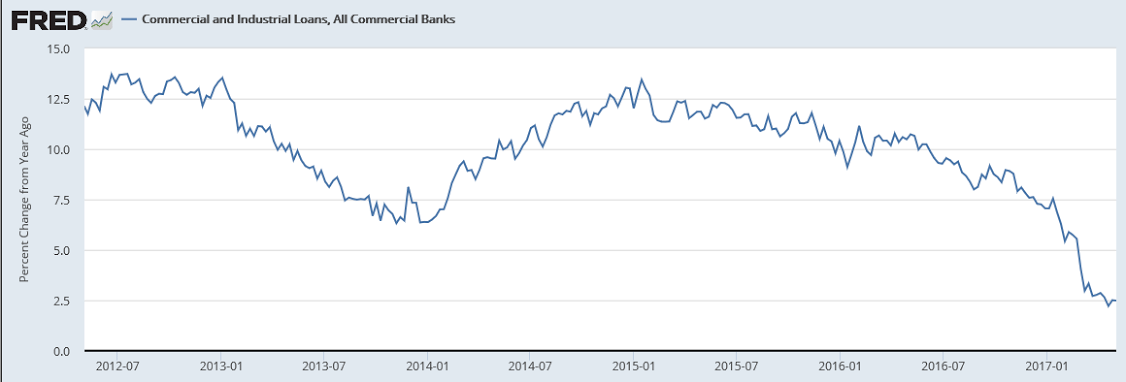

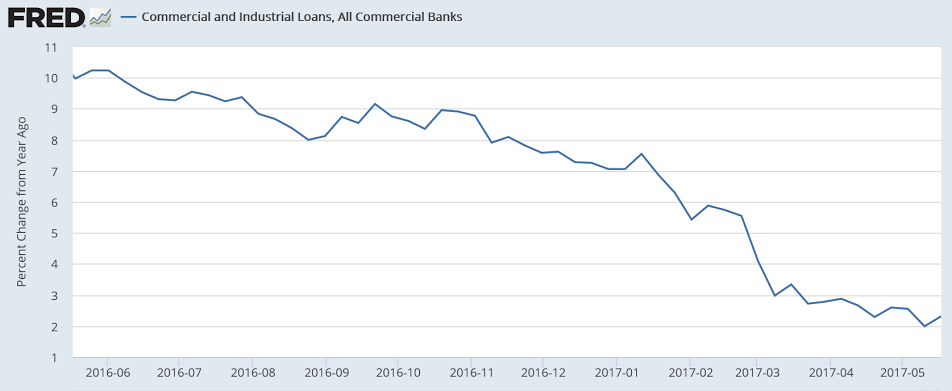

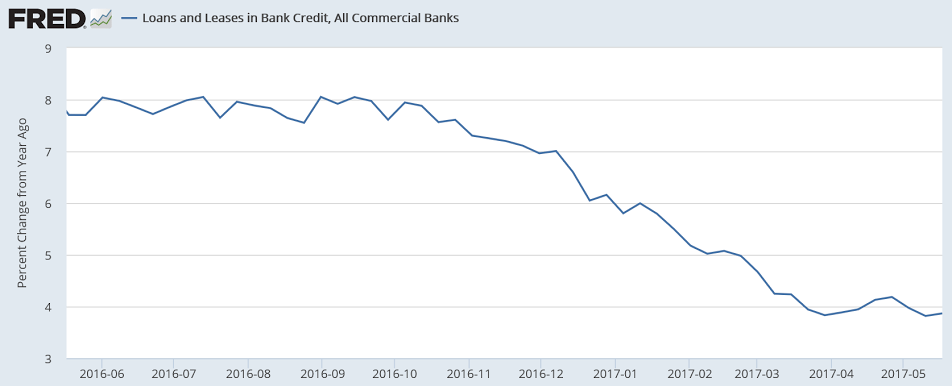

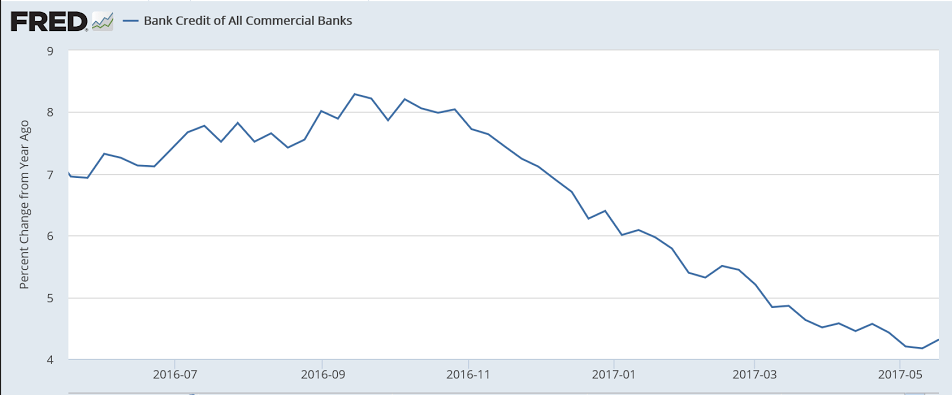

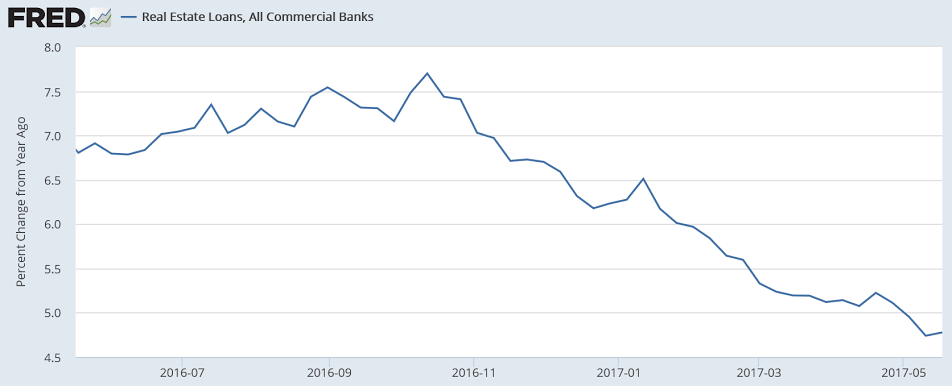

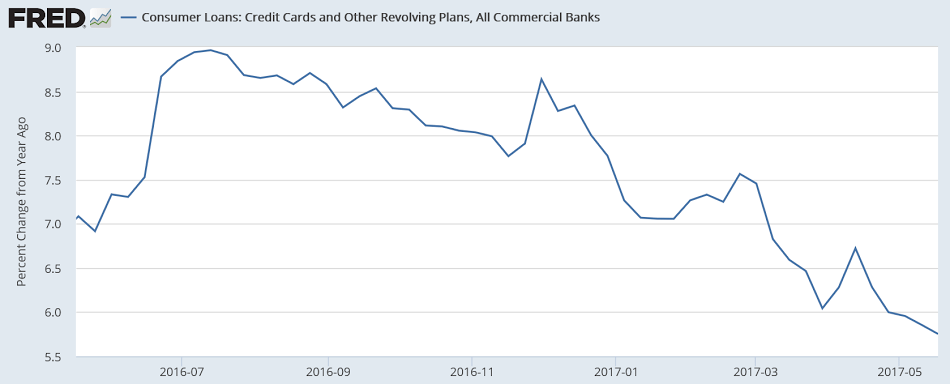

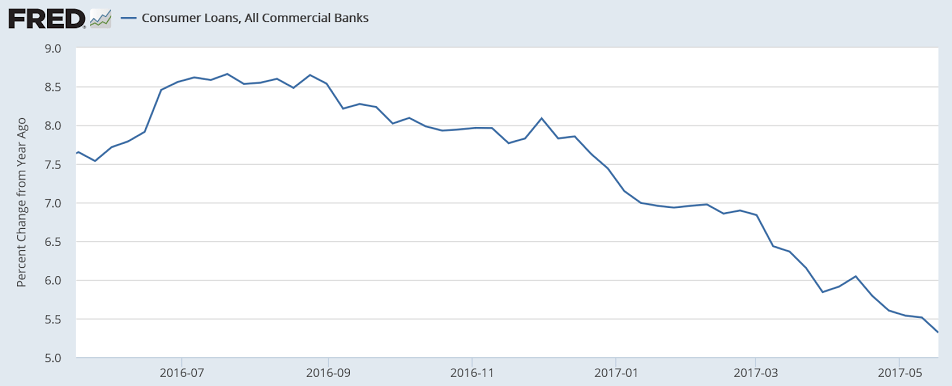

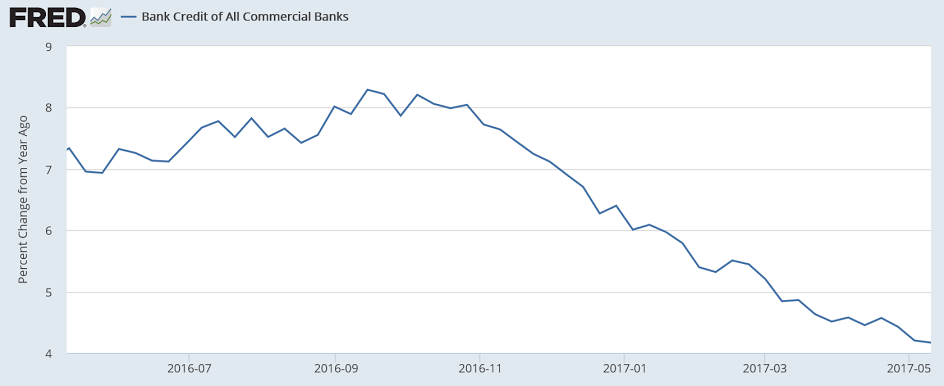

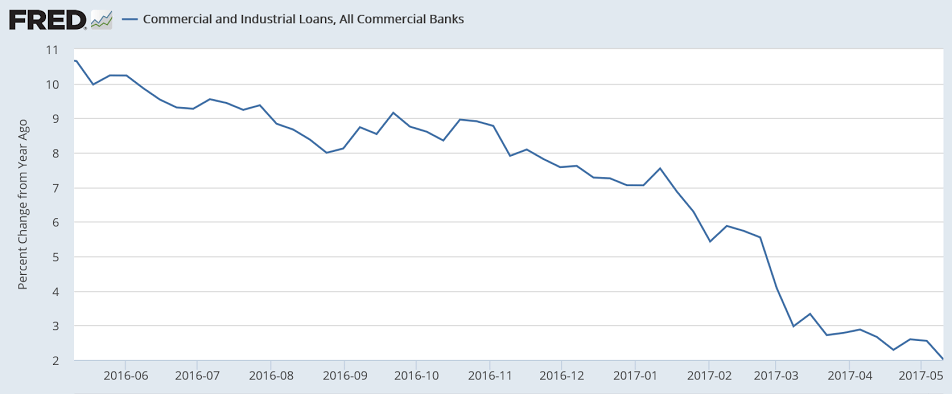

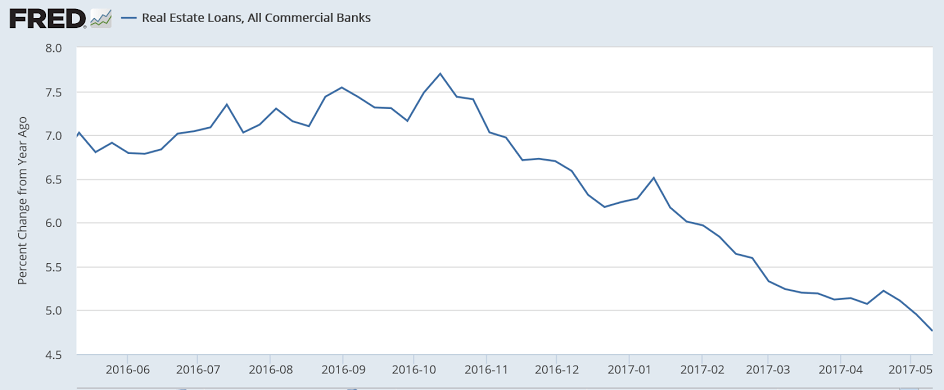

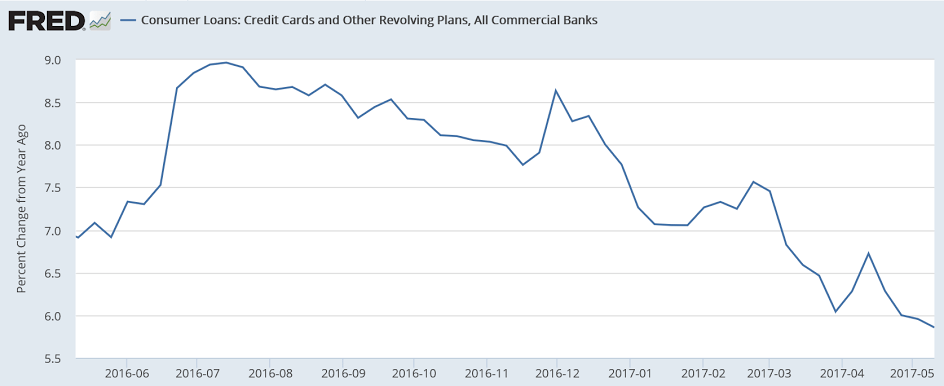

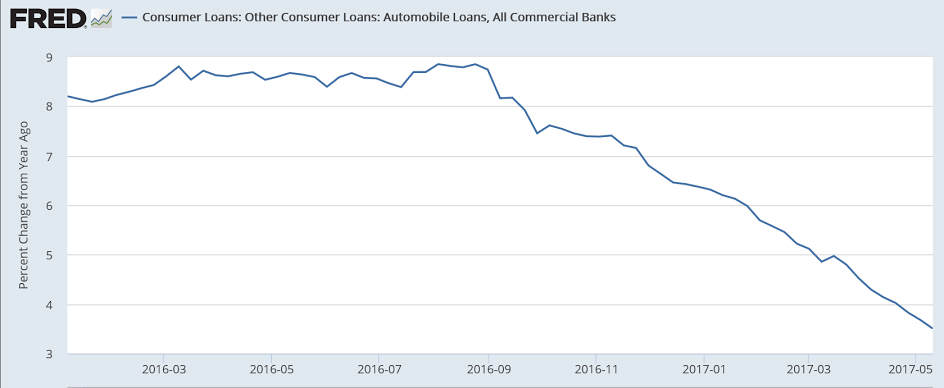

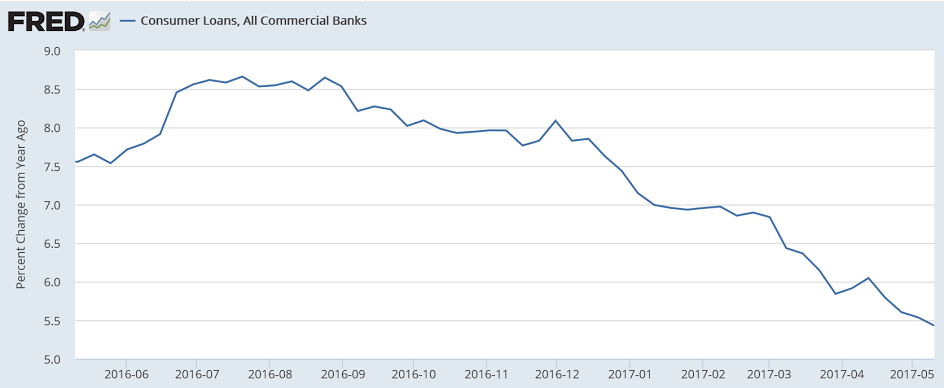

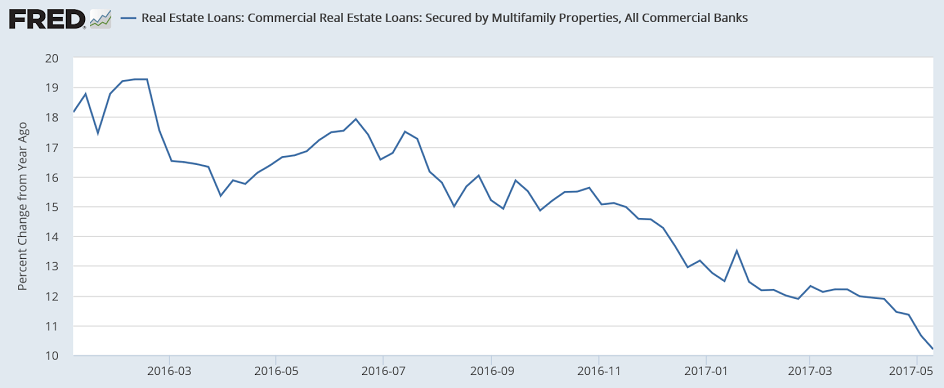

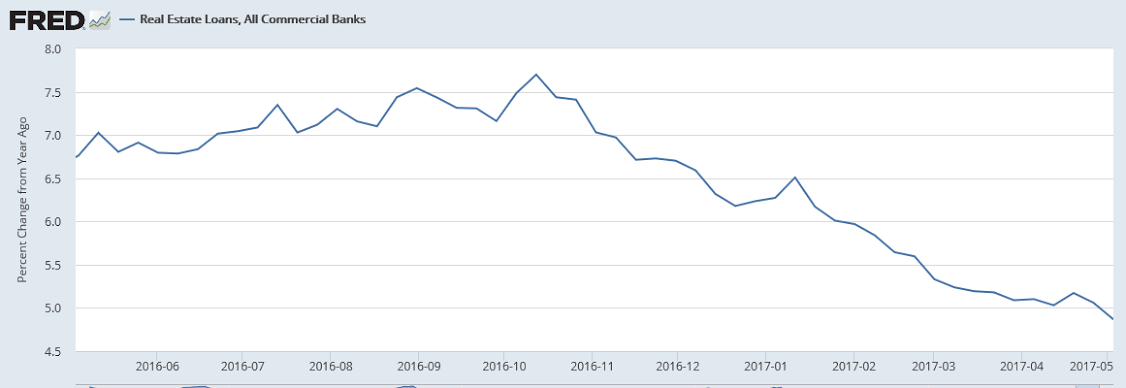

And this, all confirming the sharp deceleration in mortgage loans as previously discussed:

If the outcome is anywhere near revenue neutral, seems the tax cuts have far lower multiples than the spending cuts, so it looks to be contractionary overall. Nor do I think ‘mitigating risk for would-be entrepreneurs’ has any chance of overcoming the fiscal drag:

Trump releases budget that slashes government programs (The Hill) The Trump administration on Tuesday unveiled a budget seeking $1.5 trillion in nondefense discretionary cuts and $1.4 trillion in Medicaid cuts over the course of a decade, while adding nearly half a trillion dollars to defense spending. In 2018, Trump’s budget would shift $54 billion from nondefense discretionary spending to defense by enacting major cuts to government agencies. “We believe in the social safety net. We absolutely do,” Mulvaney said. A well-administered safety net, he continued, could boost economic activity by mitigating risk for would-be entrepreneurs.

At best a drop in the bucket and even then unlikely to ramp up for at least a year:

Trump lays out $1T infrastructure vision in budget request (The Hill) The rebuilding plan would inject $200 billion into transportation projects over 10 years, with the goal of creating $1 trillion worth of overall investment. The spending document says the administration would meet its $1 trillion target through a mix of new federal funding, incentives for private sector investment and expedited projects. The proposal will rely on four key approaches: leveraging private sector investment, ensuring federal dollars are targeted toward transformative projects, shifting more services and underused capital assets to the private sector and giving states and localities more flexibility.

Reads to me like they haven’t made any progress yet and don’t expect to any time soon:

Senate GOP focused on killing Medicaid expansion (The Hill) “There’s an interest among many of our members having a longer phaseout, a smoother glide path” after repealing the expansion, Sen. John Thune said Tuesday. Thune said the Senate is still likely to change the bill to provide more tax credits to better help low-income people afford health insurance, but acknowledged it’s still a “work in progress.” Thune expressed support for a last-minute provision in the House bill that would allow states to opt out of certain ObamaCare essential coverage requirements. Thune said senators want to have some sort of reinsurance program or high-risk pool to protect people with pre-existing conditions, but haven’t narrowed down their options.

Seems to be slowing in line with the deceleration in mortgage lending previously discussed:

Highlights

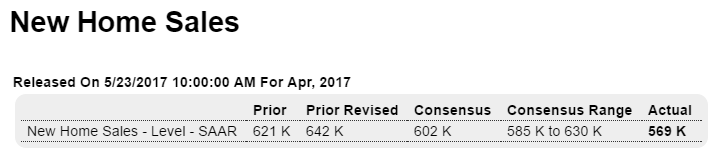

In a mixed report that confirms a reputation for unusual volatility, new home sales swung 11.4 percent lower in April to a much lower-than-expected annualized rate of 569,000. The offset is a 40,000 upward revision to March and February, now at 642,000 and 607,000. Averages are essential to evaluate this report and here the news is clearly good, at a 3-month average of 606,000 and just down from March’s expansion high at 611,000.

But the most recent news for April isn’t so good. Sales slowed even as builders cut prices where the median fell 3.0 percent in the month to $309,200. Year-on-year, the median is down 3.8 percent and is roughly in line with sales which are up only 0.5 percent on the year.

New supply came into the market but not very much, at 268,000 units for a 4,000 increase. On a monthly sales basis, supply jumped to 5.7 months from 4.9 months to reflect April’s sharp sales decline.

April was a bad month for all regions especially the West which at a 126,000 sales rate fell 26 percent in the month. Year-on-year, the Midwest is at 73,000 and is far out in front with a 20 percent gain followed by the South at 4.1 percent. The Northeast is down 5.1 percent on the year with the West, in an ominous reading perhaps given the region’s importance to builders, down 13.7 percent.

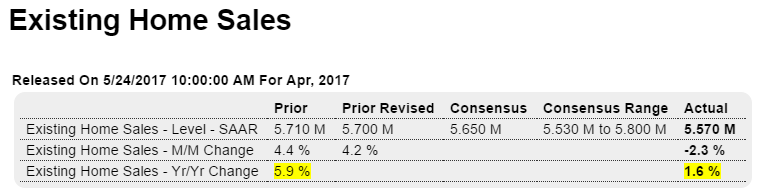

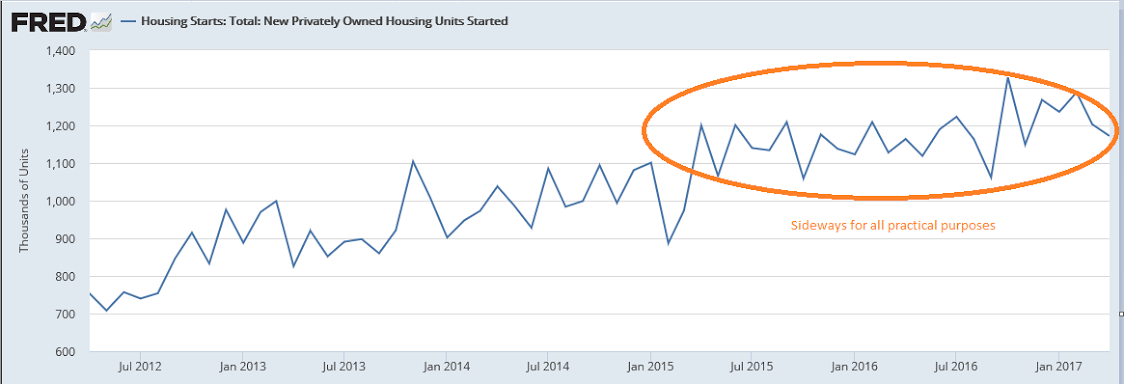

One month is never enough to judge new home sales which eases the negative signals from April. But the report does follow last week’s housing starts which also showed significant April weakness. Watch for existing home sales on tomorrow’s calendar for an additional and very important indication on April for a housing sector that opened the year strongly but may be seeing unwanted slowing during the Spring selling season.

Gets stupider by the day, as the confusion over how the currency works continues to undermine

underlying public purpose, including national security:

U.S. plan to sell oil reserve shows declining import needs

By Henning Gloystein and Dmitry Zhdannikov

May 23 (Reuters) — U.S. President Donald Trump’s proposal to sell half of the United States’ strategic oil reserve surprised energy markets on Tuesday since it counters OPEC’s efforts to control supply in order to boost prices.

The White House requested in its budget released late on Monday gradually selling off the nation’s Strategic Petroleum Reserve (SPR) starting in October 2018 to raise $16.5 billion. The U.S. SPR SPR-STK-T-EIA holds 688 million barrels, making it the world’s largest reserve, and a release of half over 10 years averages about 95,000 barrels per day (bpd), or 1 percent of current U.S. output.

Others taking notice now:

Tells me how seriously you can take some of these surveys:

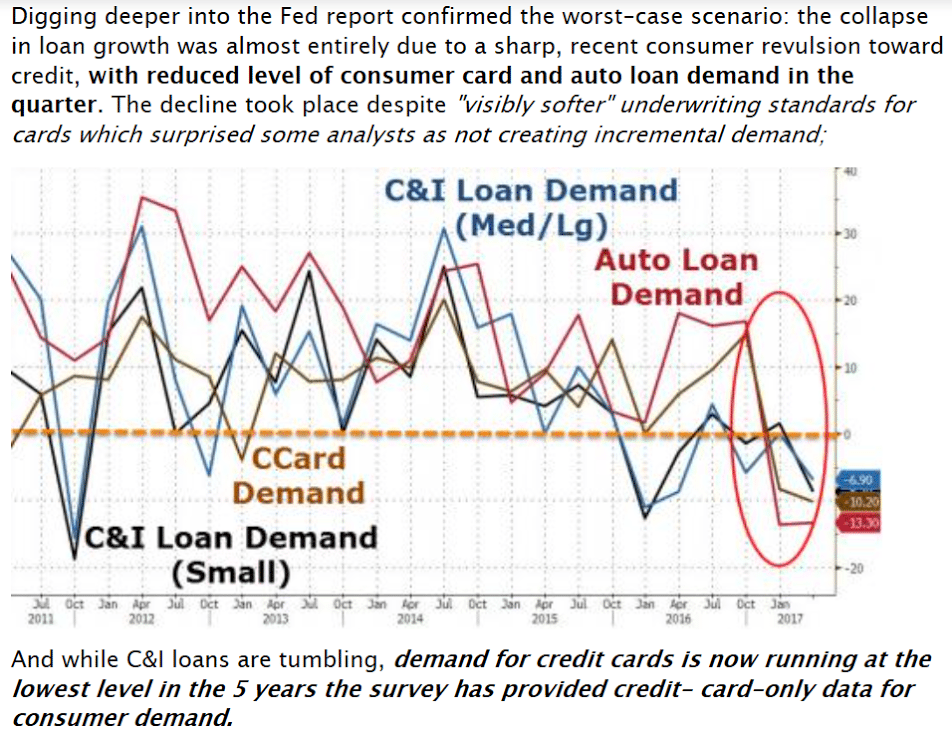

Going from bad to worse, so the way things are going seems the contribution to year over year GDP growth in q2 from credit expansion will be less than it was in q1:

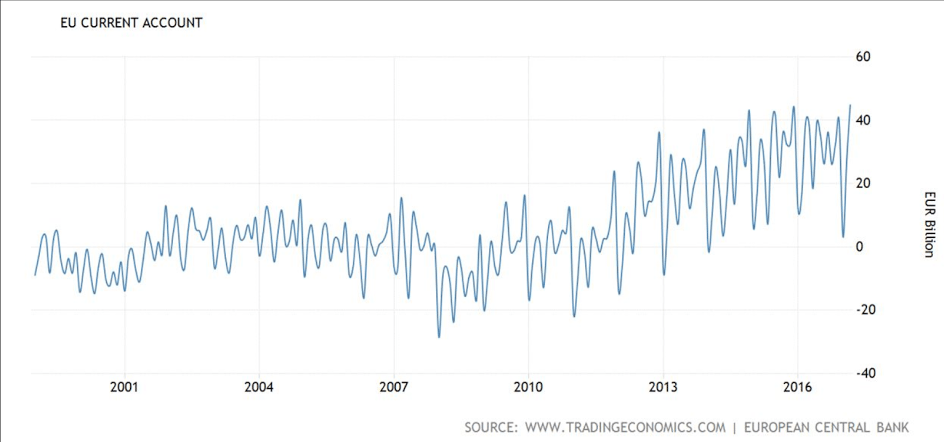

Never yet seen a current account surplus like this and a weak currency? (Euro area surplus = rest of world deficit, etc.) And the pressure has been building for over 3 years now as fear driven

portfolio selling, worked to keep the currency down:

New applications seem to be modestly increasing even as bank lending for real estate has been flat and decelerating:

Hard to say which is worse for markets- if Trump remains as President or if he is removed:

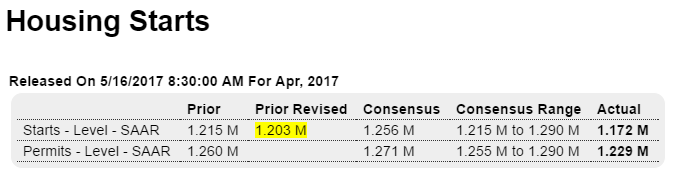

No surprise here, after seeing what mortgage lending has been doing:

Highlights

A topping out from lower-than-indicated expansion highs is the news from the April housing starts report where levels, though still healthy, are disappointing. Starts fell 2.6 percent to a 1.172 million annualized rate that is well below Econoday’s low estimate for 1.215 million. Downward revisions are a factor in the report, totaling 27,000 in the prior two months.

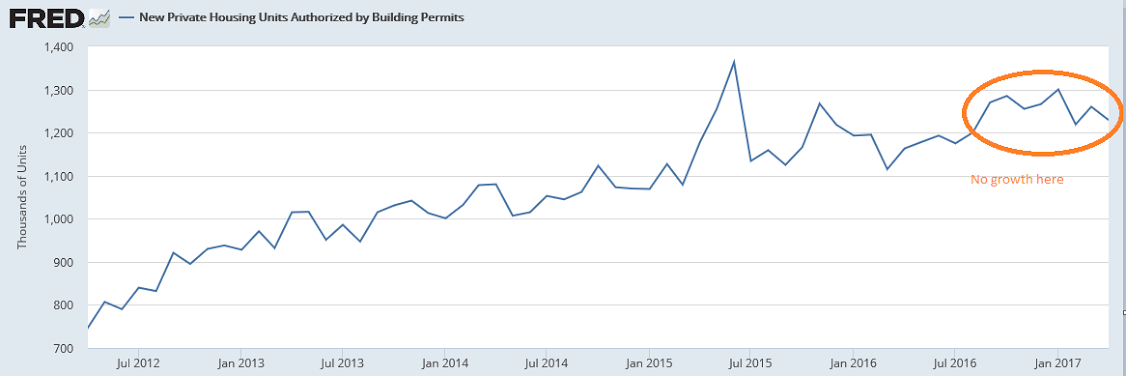

The strength in the report is in the key single-family component with starts up 0.4 percent to a rate of 835,000. Otherwise, however, the report is filled with minus signs. Permits for single-family homes fell 4.5 percent to a 789,000 rate with completions also down 4.5 percent, to 784,000.

The sharpest weakness comes from multi-family homes where starts fell 9.2 percent to a 337,000 rate. Permits did rise 1.4 percent to 440,000 but completions dropped 17.2 percent to a 322,000 rate.

April was supposed to be a rebound month for the economy. It was for the jobs report but bounces in last week’s retail sales and consumer price reports were minimal with today’s report an outright negative for the second quarter. Still most housing data, especially sales, have been showing significant strength going into the spring sales season.

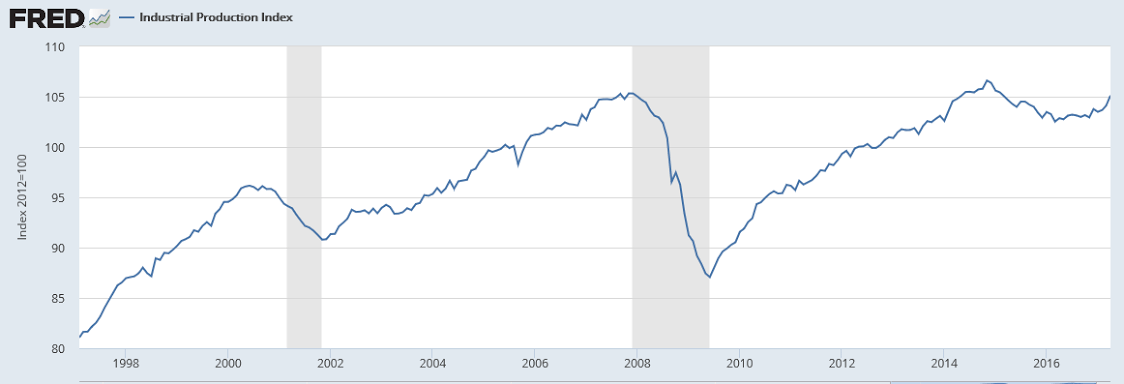

As previously discussed, industrial production is muddling through at modest levels with weakness spreading to the service sector. These numbers are not inflation adjusted, which means industrial production hasn’t even gotten back to the highs of the prior cycle:

Stalled at lows of prior cycle:

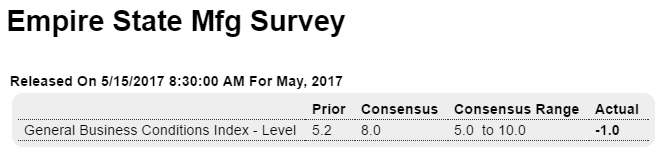

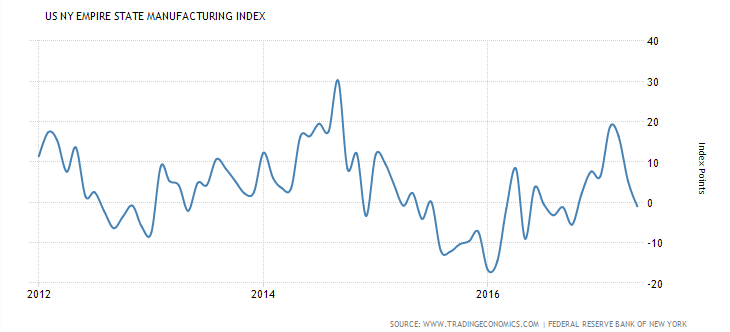

Trumped up expectations reversing?

Highlights

Activity in the New York manufacturing region is flattening out this month following a run of unusually strong growth. May’s Empire State index came in at a lower-than-expected minus 1.0 with new orders also moving into the negative column to minus 4.4. Unfilled orders, which were very strong in April and March, also moved below zero to minus 3.7.

But the strength in prior orders is keeping production up, at a very solid plus 10.6 this month, and is also keeping hiring up, at 11.9 and only 2 points slower than April’s 2-year high. Delivery times continue to slow though to much a lesser degree than prior months which points to easing congestion in the supply chain. Inventories are flat and price pressures still increasing though, once again, less than before.

The slowing in this report is actually welcome news, giving time for supply constraints to ease and reducing risks of over heating. This report points to easing for Thursday’s Philly Fed where another month of enormous strength is currently the expectation. Yet despite the strength of anecdotal reports like Empire State and Philly, definitive factory data out of Washington have yet to show outsized acceleration. Watch for the manufacturing component of tomorrow’s industrial production, definitive data where only a moderate rise is expected.

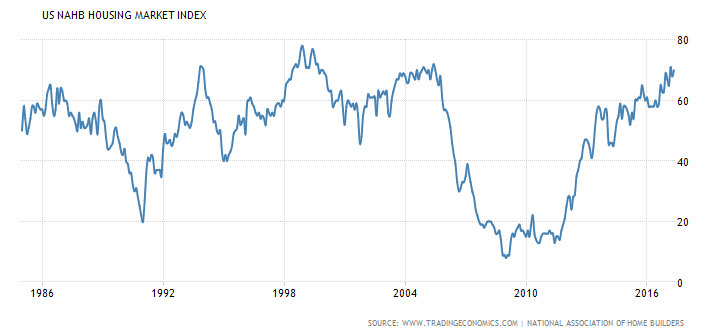

To me buyer traffic is most relevant:

The NAHB Housing Market Index in the United States rose to 70 in May of 2017 from 68 in April, beating market expectations of 68. The index is 1 point shy of 71 reached in March, which was the strongest reading since June 2005. The index of current single-family home sales went up 2 points to 76; sales expectations over the next six months increased 4 points to 79 while buyer traffic edged down 1 point to 51.

Not good:

The worst news for the economy might be coming from banks, not retail

Loan issuance declined in the first quarter from the previous three-month period, the first time that has happened in four years, according to a SNL Financial. Commercial and industrial lending, which usually pops this time of year, posted just a small increase. The business climate, at least measured by the willingness to take on debt, remains cautious.