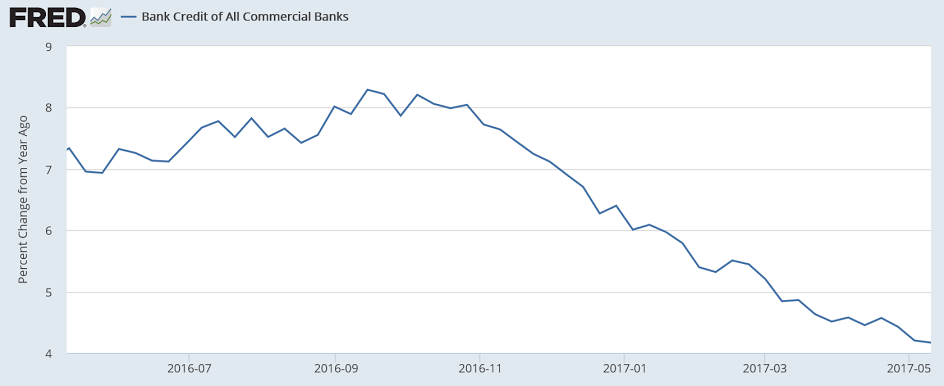

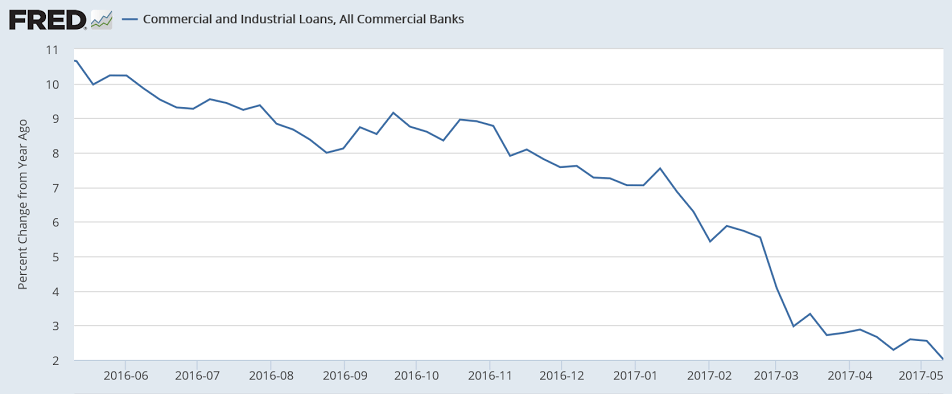

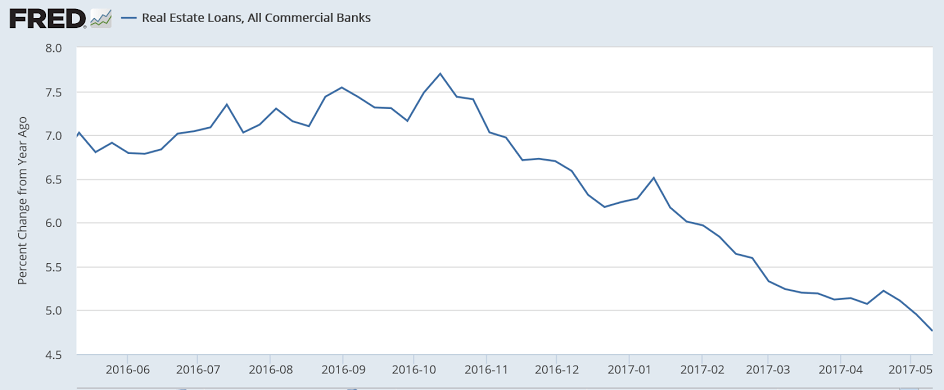

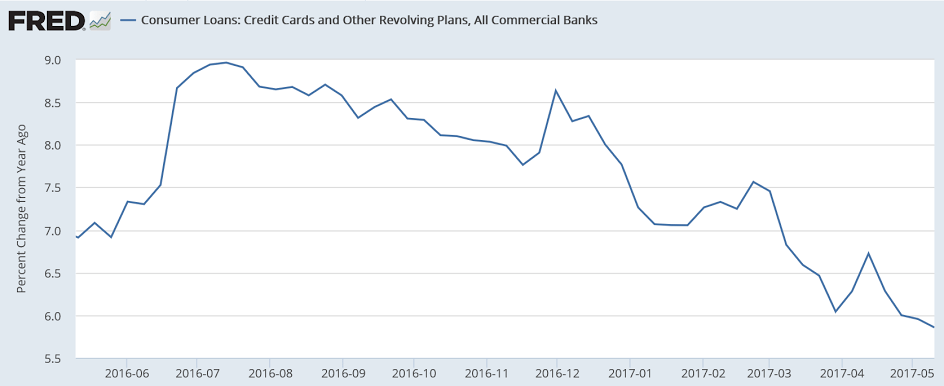

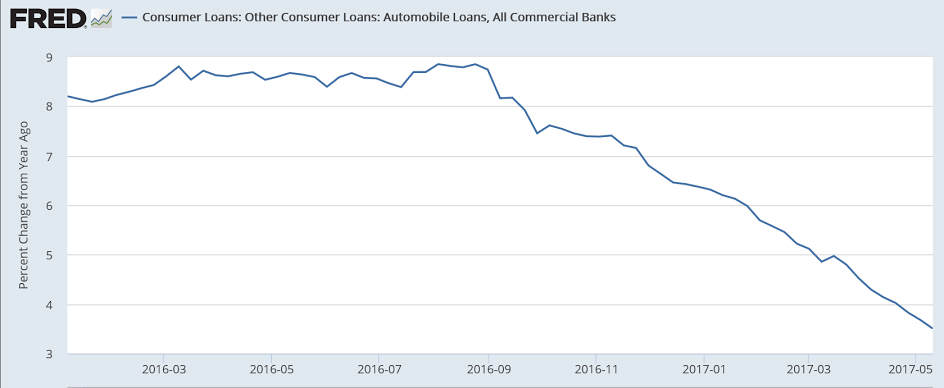

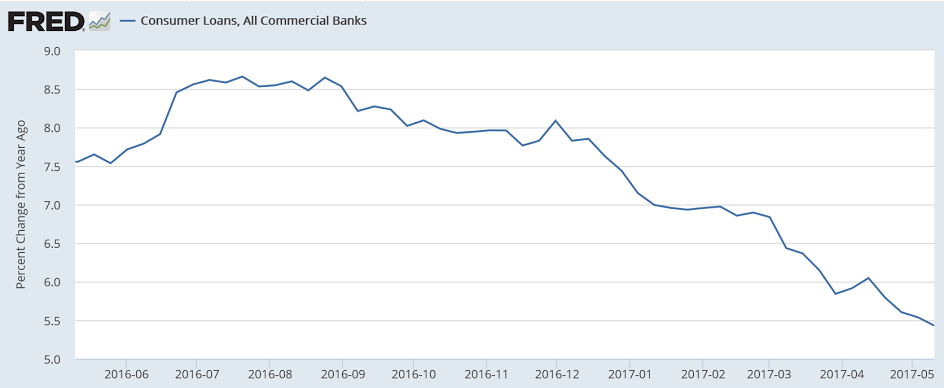

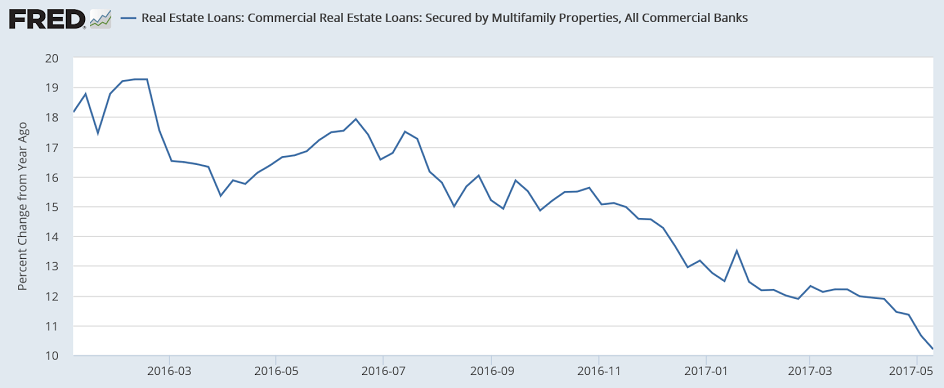

Going from bad to worse, so the way things are going seems the contribution to year over year GDP growth in q2 from credit expansion will be less than it was in q1:

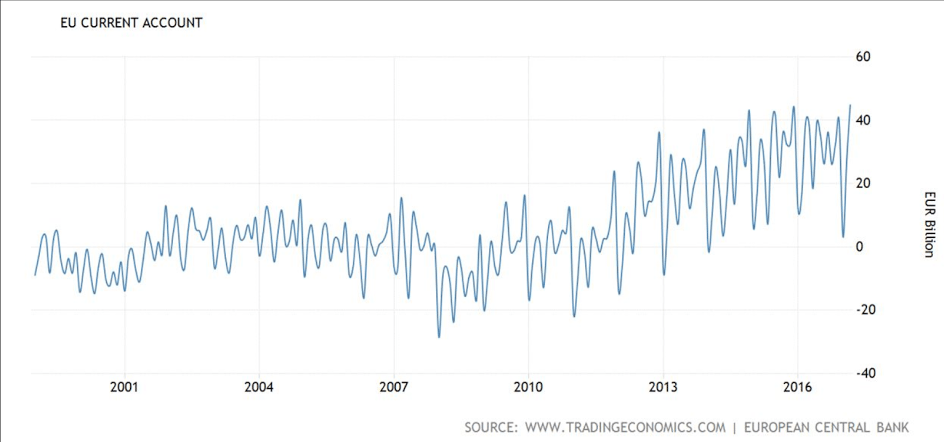

Never yet seen a current account surplus like this and a weak currency? (Euro area surplus = rest of world deficit, etc.) And the pressure has been building for over 3 years now as fear driven

portfolio selling, worked to keep the currency down: