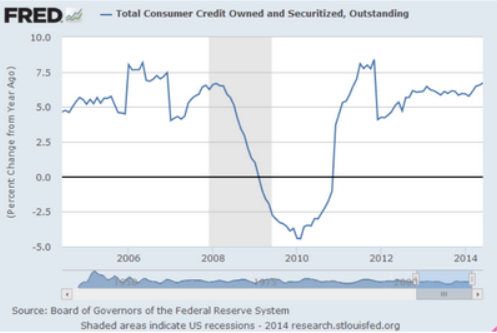

This has been going the wrong way since the post winter April ‘surge’:

Highlights

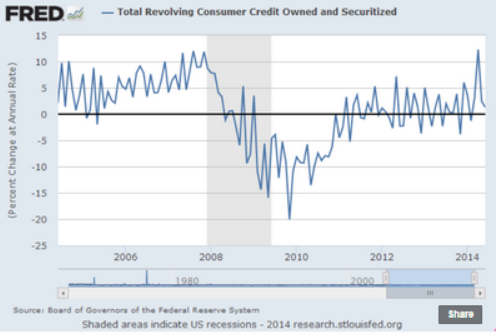

Consumer credit rose $17.3 billion in June and was driven once again by the nonrevolving component, which rose $16.3 billion on vehicle financing and also the government’s continued acquisition of student loans from private lenders. The revolving component, which is key for retailers, did rise but not very much, up $0.9 billion following a revised $1.7 billion rise in May that followed a rare surge in this category of $8.8 billion April. Aside from vehicles, consumers remain reluctant to take on new debt.

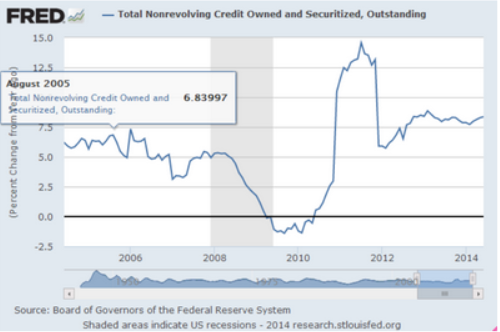

Growth rate of student loans continues to slow:

Trade numbers resulted in upward Q2 GDP revisions, while today’s inventory report means downward revisions:

Wholesale Trade

Highlights

Wholesale inventories rose 0.3 percent in June, a modest rise in line with a modest 0.2 percent gain in wholesale sales that leaves the stock-to-sales ratio unchanged at a lean 1.17. Activity has been strong in the auto sector with wholesale sales of autos jumping 2.1 percent, following gains of 1.4 percent and 3.1 percent in the prior two months. The gain in sales made for a 0.3 percent draw in wholesale inventories of autos, one that will have to replenished which is a plus for auto production.

Outside of autos, inventory draws are scarce but do include a major 5.3 percent draw in farm products which follows prior consecutive monthly draws of 4.4 percent and 0.4 percent. How much the draws in farm products will be replenished is uncertain given an 8.1 percent drop in wholesale sales for farm products during the month, not to mention current concern over the Russian embargo of US food products.

Turning back to sales, paper products, professional equipment (including computers), lumber, and metals show strong gains, all matched by what are likely desired builds on the inventory side. Weakness in sales, outside of farm products, includes chemicals, hardware, groceries, and apparel, groups all showing on the inventory side what are likely to be unwanted builds.

Outside of autos, this report on net points to soft growth in the wholesale sector during June. Next inventory data will be the business inventories report next Wednesday.

“Inventories are a key component of gross domestic product changes. The component that goes into the calculation of GDP—wholesale stocks excluding autos—increased 0.4 percent.

A report this week showed stocks of nondurable goods at manufacturers rose far less than the government had assumed in its advance second-quarter gross domestic product estimate published last week.

In that report, the government said inventories contributed 1.66 percentage points to GDP growth, which expanded at a 4.0 percent annual pace.

Wholesale inventories in June were held back by a decline in automobiles and nondurable goods.

Sales at wholesalers rose 0.2 percent after increasing 0.7 percent in May. There were declines in sales of nondurable goods, hardware and apparel.”

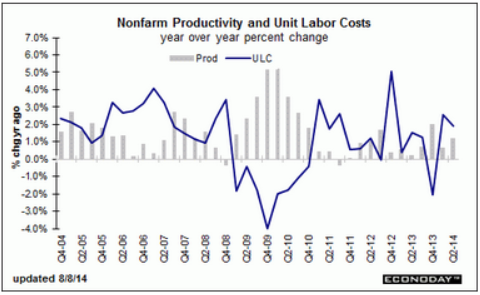

Unit labor costs below expectations: