Today’s zig up in this volatile series doesn’t look like much on the longer term graph.

Monthly Archives: May 2013

JPY

Unfortunately what Japan risks is an exit from headline deflation but no growth in output and employment to show for it. What they’ve done might be to cause the currency to depreciate about 25% via ‘portfolio shifting’, which may not expand real domestic demand. In fact, in real terms, it may go down, leaving them with higher prices and a lower standard of living.

Yes, the currency shift makes imports more expensive, which means there will be some substitution to domestic goods which cost more than imports used to cost, but less than they now cost. But for many imports there are no substitutions, so the price increase simply functions like a tax increase.

And yes, exports, particularly nominal, will go up some, but so does the cost of inputs imported. And yes, some inputs sourced elsewhere will instead be sourced locally, adding to domestic employment and output, but not to real domestic consumption.

At the macro level what counts is what they do with regards to keeping the govt deficit large enough to accommodate the need to pay taxes and net save. Net exports ‘work’ by reducing real terms of trade when the govt purchases fx, which adds net yen to their economy. I call the fx purchases ‘off balance sheet deficit spending’. But so far the govt at least says they aren’t even doing that, and the lifers etc. now deny having done much of that either?

What has changed fundamentally is they are importing more energy since shutting down their nukes. Again, this functions as a tax on their economy (taxonomy for short? really bad pun intended!).

On the other hand, as above, buying fx by either the private or public sector is, functionally, deficit spending, which in this case first supports exports, but could add some to aggregate demand, depending on the details of relevant propensities to consume, etc.

The entire point of all this is Japan can cause some ‘inflation’ as nominal prices are nudged up by the currency depreciation, but with only a modest increase in real output via an increase in net exports that fades if not supported by ongoing fx purchases. And all in the context of declining real terms of trade as the same amount of labor buy fewer imports, etc. which is the engine that makes it ‘work’ on paper.

And for the global economy it’s another deflationary shock in a deflationary race to the bottom as other wanna be exporters compete with Japan’s massive cut in real wages.

So yes, they are trying to cause inflation, but not for inflation’s sake, but as a way to increase output and employment. But I’m afraid what they are missing that the causation doesn’t work in that direction.

In conclusion, this was the thought I was trying to flesh out:

Just because increasing output can cause inflation, it doesn’t mean increasing inflation causes real output and employment to increase.

sorry, this all needs a lot more organizing. Will redo later.

can’t help it, seeing weakness everywhere

Initial claims,GDP, Italy

Karim writes:

-

Q1 Real GDP was revised down just 0.1% to 2.4% but the underlying changes were more volatile:

- Real Consumer Spending up to 3.4% from 3.2%

- Capex up from 3% to 4.6%

- Government consumption down to -4.9% from -4.1%

- Inventory contribution down to 0.6% from 1%

Takeaway is underlying private demand was stronger than initially reported, government was more of a drag and inventories have more room to expand.

Yes, but note this:

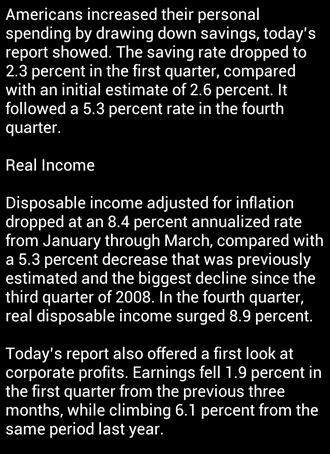

The drag from government and inventories was partially offset by an upward revision to consumer spending, which rose at a 3.4 percent annual rate, up two tenths of a point from the government’s previous estimate. However, a cloud hung over that category, as most of the upward revision was due to higher sales of gasoline. Higher prices at the pump are a burden on consumers, leaving them less money to spend on other things.

And:

After-tax corporate profits fell at a 1.9 percent annual rate in the quarter, the first decline in a year.

Optimism on late 2013 and 2014 growth (Rosengren speech yesterday) stems from government consumption turning from being a drag to neutral sometime in Q3 or Q4, leaving in place the underlying pace of private demand growth of about 3%.

Yes, the question being ‘leaving in place’, as govt spending feeds private sector sales, etc.

So the assumption is the private sector spending that’s been taking place will continue at that pace post tax hikes and sequesters. And note that growth in the credit driven spending (cars, appliances, housing) is showing at least hints of slowing.

Department of Labor reported 5 states didn’t complete their claims count last week due to the holiday, so the rise in claims to 354k to be taken with a grain of salt.

Yes, but here too are at least hints that claims bottomed a few weeks ago and have edged a bit higher since then, and that Non Farm Payrolls peaked in Feb, and if next weeks number prints at 150,000 the three month average is back down to around that level.

And, again, it’s the year end tax hikes and subsequent sequesters that are causing me to look for evidence of subsequent slowing.

This is notable for Italian (and European) growth. Eur10bn (mid-point of estimates below) is worth about a 0.5% add to GDP growth:

EU Recommends Removing Italy From Excessive-Deficit Procedure (Bloomberg) The European Commission recommended today lifting an excessive-deficit procedure against Italy after the government brought its budget shortfall within the European Union limit. “Our task is to respect our commitments with Europe and implement the program the parliament has given its vote of confidence on,” Italian Prime Minister Enrico Letta said. Ending the strict EU monitoring of Italian public spending may free up resources of as much as 12 billion euros, Regional Affairs Minister Graziano Delrio said in an interview with daily La Stampa May 27. “The closing of the procedure alone allows us to boost spending by between 7 and 10 billion euros, 12 billion euros in the most optimistic forecast,” Delrio said in the La Stampa interview.

Yes, this would be helpful, but a deceleration in expected US growth hurts Europe as well.

Initial Claims YTD:

Full size image

Nonfarm Payroll Change YTD:

Full size image

Larry Fink talking position

Americans are not saving enough for retirement, which is a bigger issue than tax policy, Fink said.

Noyer Says Not Convinced About Merit of Negative Rates

No mention that it’s a tax

Noyer Says Not Convinced About Merit of Negative Rates

By: Hans Nichols and Mike Dorning

May 29 (Bloomberg) — European Central Bank Governing Council member Christian Noyer said he’s not convinced about the merits of a negative deposit rate as policy makers debate how to revive a moribund euro-area economy.

“We have prepared so that in case of a need we could implement it,” Noyer said in an interview with Bloomberg Television in Paris yesterday. “This is technically very delicate. I’m personally not convinced there’s an interest in doing that.”

The ECB cut its benchmark rate to a record low of 0.5 percent on May 2 and President Mario Draghi signaled the central bank is ready to reduce borrowing costs further if needed. Noyer said a negative deposit rate — which would mean lenders would pay to park excess cash with the ECB — might prompt institutions to raise their lending rates to offset that cost.

“There have been experiences in the past,” he said. “Not all are convincing. In some cases it even tended to trigger an increase in the rates of credit because the banks were compensating for a loss they were getting on their deposits with the central bank.”

Such an outcome would undermine one of the ECB’s main goals, which is to revive lending by banks ravaged by a debt crisis now in its fourth year. The euro-area economy shrank 0.2 percent in the three months through March, a sixth straight contraction. Lending to households and companies fell for a 12th month in April on an annual basis, the ECB said today.

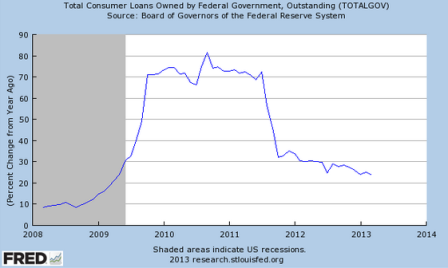

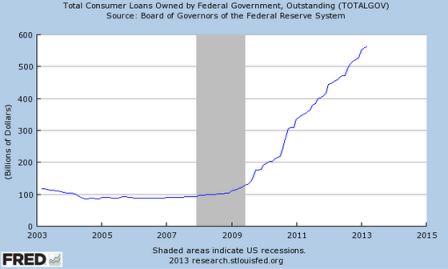

Student Loan FRED Graph

The growth rate of student loans is still high, but decelerating.

It’s still a bit over .5% of GDP each year, but that % is falling as well.

(still searching for the source of credit expansion that’s going to drive GDP in Q2)

Full size image

Full size image