The Fed is Starving Economy of Interest Income

By Warren Mosler

He left out the part about needing a fiscal adjustment to compensate but this is part one of a three part presentation of something I wrote.

The Fed is Starving Economy of Interest Income

By Warren Mosler

He left out the part about needing a fiscal adjustment to compensate but this is part one of a three part presentation of something I wrote.

I may have mentioned that for the size govt we have we are grossly over taxed?

;)

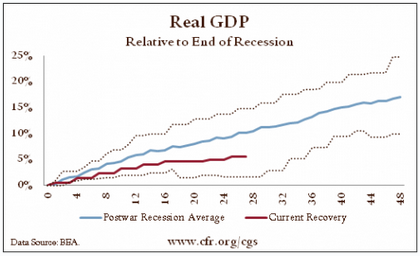

Real GDP is growing, but weakly compared with the postwar average recovery.

The recovery from the 1980 recession was even weaker at this stage, but that reflected a double-dip recession in 1981.

The economy would have to grow at a 7.6 percent annualized rate in order to catch up with the average postwar recovery by the end of 2012.

The consensus forecast for 2012 growth as reported by Bloomberg is 2.1 percent, up just slightly from a forecast of 2.0 percent as of last October.

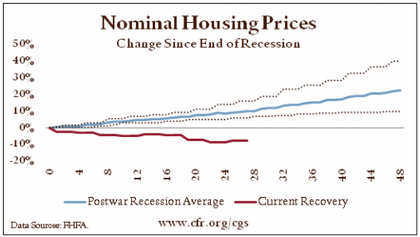

Soft home prices have been central to the weakness of the recovery.

The continued weakness of nominal home prices is a postwar anomaly.

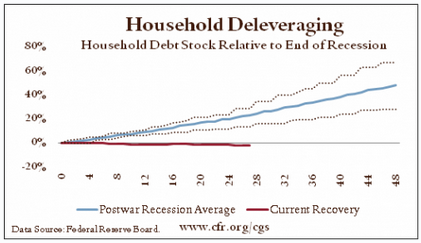

In every previous postwar recovery, the stock of household debt has risen as the recovery has begun.

In the current recovery, the collapse in home prices has severely damaged household balance sheets. As a result, consumers have avoided taking on new debt.

The result is weak consumer demand and, hence, a slow recovery.

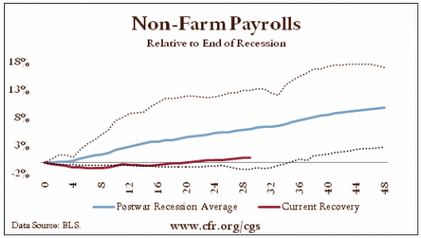

The slow recovery is obvious in the labor market, where job growth remains painfully sluggish compared to the average recovery.

The recent uptick at the end of the Current Recovery linev(red) is the result of encouraging payroll data announced on January 6th 2012.

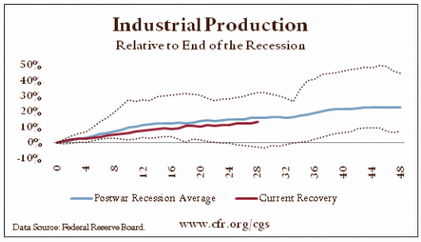

Because of the depth of the recent recession, one might expect stronger-than-average improvement in industrial production.

Despite the predicted snapback, the increase in industrial production during this recovery is actually slightly slower than in the average postwar case.

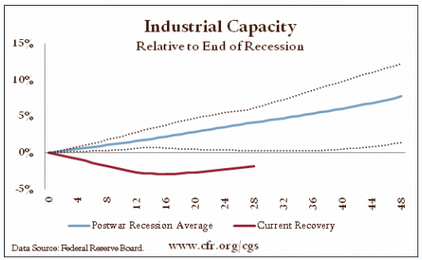

Capacity in manufacturing, mining, and electric and gas utilities usually grows steadily from the start of a recovery.

However, during the current recovery, investment has been so low that capacity is actually declining. Plants and machinery are depreciating faster than they are being installed.

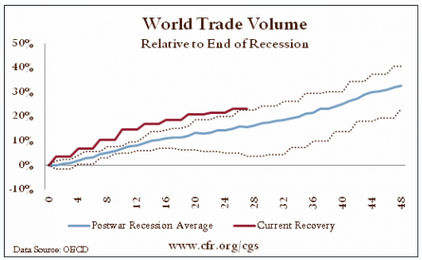

The growth in world trade exceeds even the best postwar experiences.

However, this reflects the depth of the fall during the recession.

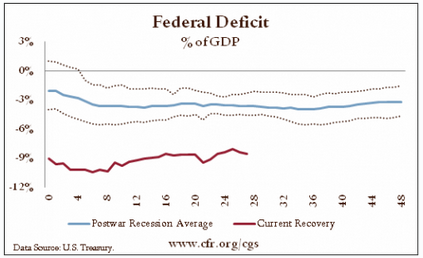

The federal deficit since the start of the recovery has been much higher than in previous postwar cases.

Although the deficit has shrunk slightly, its level creates significant challenges for policymakers and the economy.

The traditional American enthusiasm for the road has been dulled by a combination of weak recovery and high fuel prices.

When compared to other postwar recessions, total vehicle miles traveled in this current recovery has not only lagged the average, but has registered no growth whatever.

It wouldn’t be taking this long if there was a way to get’er done?

Not to mention that once haircuts are finalized the obvious political response from the opposition in Italy, for example, is “if Greece doesn’t have to pay why do we?’

Europe Shares Retreat From Highs as Greece Talks Stall

Jan 24 (Reuters) — European shares retreated from near six-month highs as concerns deepened that Greece might head towards a disorderly default and technical analysts said the recent rally could be coming to a close.

They don’t need to ‘create jobs’ as there is already more to do than there are people to do it.

They need to remove fiscal drag with tax cuts and/or spending increases to allow the needs to be funded:

Sustained Global Unemployment: Interesting stats from the International Labor Organization noting that there are nearly 200million unemployed globally and that another 40million jobs need to be created each year for the next decade. To generate sustainable growth while maintaining social cohesion the world must create 600million production jobs over the next decade which would still leave 900million workers and their families below the $2 a day poverty line, largely in developing countries. These numbers are fairly sobering when you consider that the world’s largest economy only managed to net create around 1.9million jobs in the recent ‘recovery’ and only around 7 million jobs even during the ‘boom’ years between 2002-2007.

Good luck to them:

Prime minister Yoshihiko Noda told parliament that he will move to double sales tax to 10pc, saying the future of the world’s third-largest economy depends on tackling its massive public debt.

Mr Noda said the country has “no time to spare” in cutting its fiscal burden.

“It’s impossible for young people to believe that things will get better tomorrow in a society where debts resting on future generations continue growing,” he said. “It is not too much to say that the revival of hope of the entire society depends on the success of this combined reform.”

Japan Fiscal Pressure Rises as Tax Increase Not Enough

By Mayumi Otsuma

Jan 24 (Bloomberg) — Japan’s government said it will probably miss its goal of balancing the budget by 2020 even with its proposed doubling of the sales tax, underscoring the scale of the nation’s fiscal challenges.

The primary budget deficit, which excludes the cost of servicing debt, will be the equivalent of 3.1 percent of gross domestic product for the year through March 2021, the Cabinet Office said in Tokyo today. Hours after the release, Prime Minister Yoshihiko Noda reiterated his call for opposition lawmakers to engage in talks on boosting the sales levy.

Addressing the shortfall through faster growth may be a limited option for Japan, where the central bank has already cut the key interest rate near zero and the traditional boost from a trade surplus last year evaporated — for the first time since 1980. Absent structural changes that boost incentives to spend and invest, today’s report signals further fiscal tightening will be needed to rein in the world’s largest public debt.

“To balance the budget, the rate needs to rise further,” said Takuji Okubo, chief Japan economist at Societe Generale SA in Tokyo, referring to the sales-tax level. “We’ve passed the point where we can soft-land the fiscal situation. The question is how hard the landing is going to be.”