The low jobless claims number seem to have sent markets into full taper mode. Stocks down due to fears of what happens without the presumed Fed support, and bonds higher in yield due to fears of what happens when the Fed slows down purchases.

And so while the ‘better jobs’ outlook that’s driving tapering is arguably good for stocks, markets are saying it’s not good enough to outweigh the higher bond yields and therefore the higher ‘discount rate’ for asset valuations.

Point here is, as previously discussed, the Fed will be cutting back it’s QE unless stocks fall hard enough to change their minds.

Which could very well happen.

While desperate circumstances that drive a large number of people to take on extra jobs at any pay to survive show ‘improvement’ in claims and payrolls, that’s not necessarily good enough for stocks, which look to earnings growth through top line growth, which is looking highly suspect.

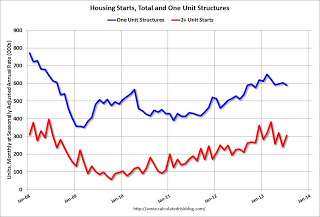

And the higher mortgage rates have already pulled the rug out from under mortgage purchase applications and homebuilder stocks, etc. the one green shoot beginning to drive credit expansion.

And Walmart again pointing to the year end tax hikes slowing things down and low income growth keeping them from improving, and nothing in the rest of today’s numbers cause me to think top line is shifting gears, as least not for the better. And more ‘fiscal responsibility’ may be coming soon as both sides agree there is a long term deficit problem, and score political points for doing something about it.

All in the context of the macro issue where for gdp sales = income and a cut in net income from proactive deficit reduction means credit expansion elsewhere has to rise to the occasion to offset ever growing demand leakages.

Egypt and higher oil prices isn’t helping either. It wouldn’t be the first time oil price spikes toppled a suspect economy.

Walmart:

“The retail environment remains challenging in the U.S. and our international markets, as customers are cautious in their spending. Net sales in the first six months were below our expectations, so we are updating our forecast for net sales to grow between 2 and 3 percent for the full year versus our previous range of 5 to 6 percent,” said Holley. “This revision reflects our view of current global business trends, and significant ongoing headwinds from anticipated currency exchange rate fluctuations.”

“Across our International markets, growth in consumer spending is under pressure,” said Doug McMillon, Walmart International president and CEO. “Consumers in both mature and emerging markets curbed their spending during the second quarter, and this led to softer than expected sales. While this creates a challenging sales environment, we are the best equipped retailer to address the needs of our customers and help them save money.

During the 13-week period, the Walmart U.S. comp was negatively impacted by lower consumer spending due to the payroll tax increase and lower inflation than expected. Comp traffic decreased 0.5 percent, while average ticket increased 0.2 percent.

“While I’m disappointed in our comp sales decline, I’m encouraged by the improvement in traffic and comp sales as we progressed through the quarter. The 2 percent payroll tax increase continues to impact our customer,” said Bill Simon, Walmart U.S. president and CEO. “Furthermore, we also expected an increase in the level of grocery inflation, which did not materialize in a meaningful way. We were pleased that both home and apparel had positive comps.

Egypt Spirals Out Of Control

The violence that has plagued Egypt since the ouster of President Mohamed Morsi on July 3 has finally spiraled out of control. Clashes broke out across Egypt on Wednesday when police tried to break up two protests in support of Morsi. The Healthy Ministry says at least 525 were killed in the violence, and 3,717 were injured. The interim government declared a month-long state of emergency, a tool Egyptian rulers have frequently used to crack down on perceived threats. Cairo was quiet Thursday morning, but Morsis Muslim Brotherhood party has called for protests later today.