Looks like no repeal and replace pending:

I think Paul Ryan is trying to pull a fast one on repealing Obamacare

On the surface, it looked like a GOP news conference touting a possible compromise with conservatives to help get the health-care reform bill passed. But House Speaker Paul Ryan and his fellow Republicans really just tipped their hand and admitted their top concern isn’t really repealing and replacing Obamacare, it’s keeping what’s left of the Obamacare exchanges up and running.

Don’t take my word for it. House Energy and Commerce Committee Chairman Greg Walden said it himself when he cheered on the compromise:

“So this is another step in the right direction and I know we’ll keep working forward in this process in the next couple of weeks as we work to refine our product, improve our product, and get to the goal of saving Americans on their premiums, making sure that the Affordable Care Act exchanges don’t fully collapse, we see examples again of more insurers contemplating pulling out of the market, and our job is to try and reform this process in a timely manner.”

Sometimes public purpose demands regulation, regardless of ideology.

One classic example is a football game, where if any one person stands he can see better, but if everyone stands no one can see better and no one can see at all if they are seated. The answer is collective action, where you might have a policy of no one being allowed to stand for more than a few seconds, or something like that.

Likewise, if there are no federal pollution laws, states then compete with each other where whoever allows companies to pollute has the highest inflow of new companies and the lowest personal tax rates. Again, public purpose is served by having national minimums.

That is, there is public purpose in preventing what otherwise would be what’s called a ‘race to the bottom.’

So when dismantling regulation, public purpose is best served by not reinstituting any such races to the bottom, which I have yet to here even discussed.

Somewhat related are moral hazard issues.

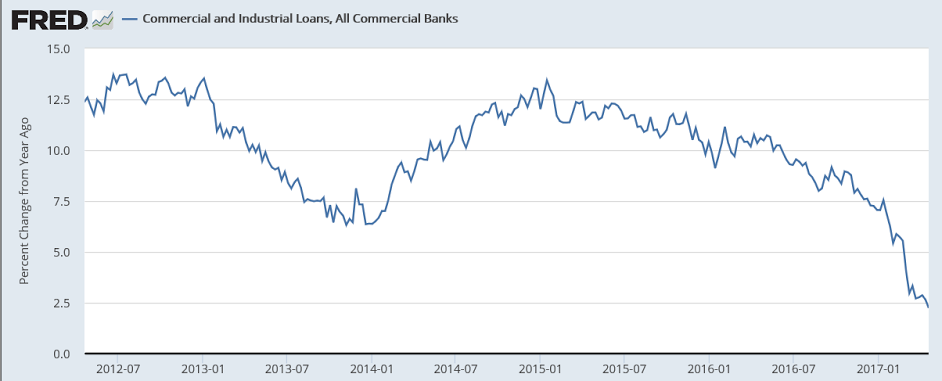

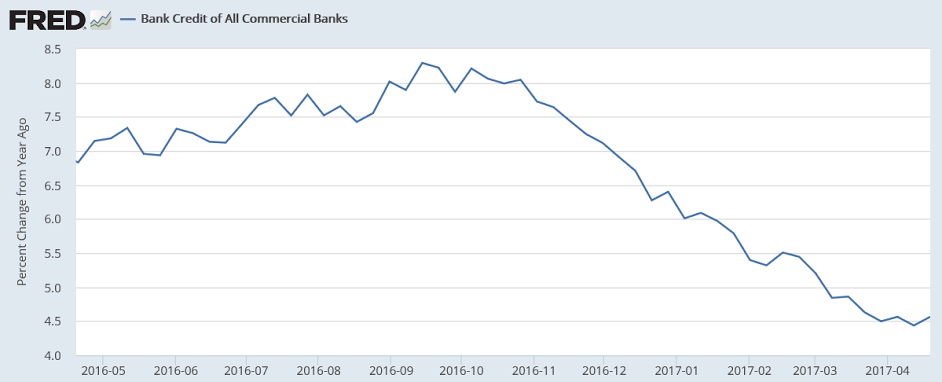

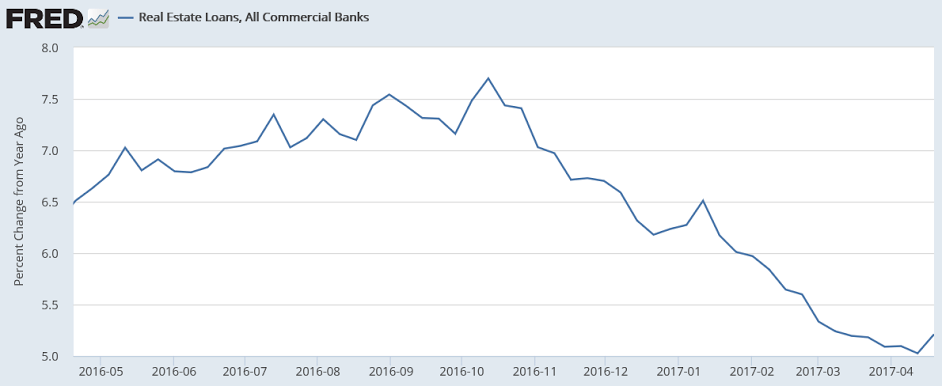

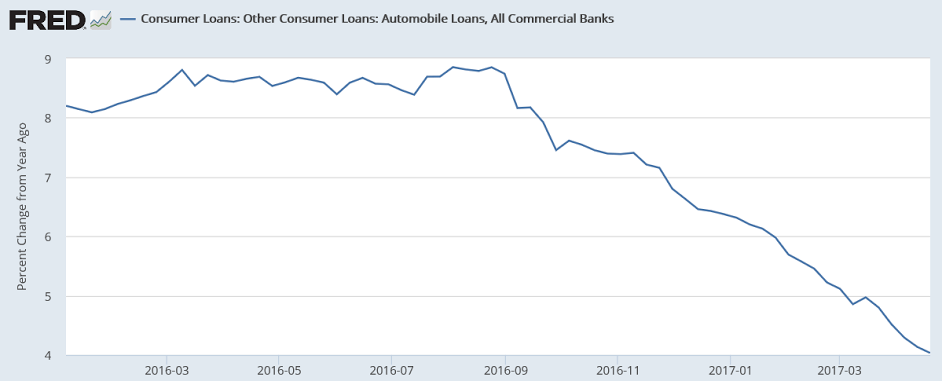

For example, since bank deposits are federally insured, which has been shown beyond dispute over time to itself serve public purpose, there is no ‘market discipline’ on the liability side of banking, and therefore the asset side begs full regulation and supervision as the savings and loan debacle of the 1980’s and other periods of lax supervision have repeatedly demonstrated.

Unilaterally announcing we are now the new ‘global police’ raises a few questions?

Seems to me there are at least dozens of serious infractions daily?

‘Holding to account’ and ‘crimes against the innocents’ etc. begs further definition?

Is launching a few missiles to announce displeasure the President’s precedent?

Does this policy require legislative initiative?

And many more.

Looks to me like drawing a line in the sand with your head in the sand?

“The U.S. will stand up against anyone who commits crimes against humanity, Secretary of State Rex Tillerson said on Monday, less than a week after Washington launched missile strikes in response to an alleged Syrian chemical attack.

“We rededicate ourselves to holding to account any and all who commit crimes against the innocents anywhere in the world,” Tillerson told reporters while commemorating a German Nazi massacre committed in Italy in 1944.”