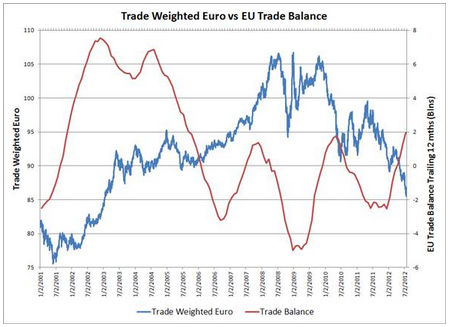

Trade differentials have been blamed for the euro crisis, implying that that if trade had some how been balanced there wouldn’t have been the kind of liquidity crisis we’ve been witnessing.

While I do recognize the trade differentials, it remains my deduction that the source of the ongoing liquidity crisis is the absence of the ECB (the only entity not revenue constrained) in critical functions, including bank deposit insurance and member nation deficit spending. And I continue to assert that the euro zone liquidity crisis is ultimately obviated only by the ECB ‘writing the check’, as has recently indeed been the case, however reluctantly.

Trade issues within the euro zone, however, will remain a point of economic and political stress even with a full resolution of the liquidity issues, which leads to discussions of fiscal transfers.

Fiscal transfers can take two forms. One is direct payments to individuals, such as unemployment compensation. Another is the placement of enterprises in a region.

The US does both. For example, it funds unemployment compensation and also spends to directly support all federal agencies, including contracting private sector agents for goods and services to provision the federal govt and its agencies.

And here’s where mainstream economics has left out a critical understanding. In real terms, the allocation of the production of goods and services to a region is a real cost to that region.

This is because that region has to supply its labor to the production of output that is directed to the public sector for the mutual benefit of all the regions.

Note that this is not the case with the likes of unemployment compensation, where the payment is made without any ‘real output’ transmitted to the public sector.

For the euro zone, this means that if Germany, for example, located a military production facility in Greece, where Germany got the benefit of the output, in ‘real terms’ Greece would be ‘paying’ for Germany’s military.

This type of thing could work to readily ‘balance’ euro zone trade, at the real expenses of the ‘deficit’ nations.

Which is exactly what happens in the US, for example, when a military procurement expenditure is located in a region of high unemployment.

And yes, I fully appreciate the obstacles to this actually happening, including deficit myths that prevent full employment and politics that need no further discussion, so thanks in advance for not telling me about them!

But the point remains- the trade differentials in the euro zone are not in the least an insurmountable problem, at least not in theory…