Author Archives: WARREN MOSLER

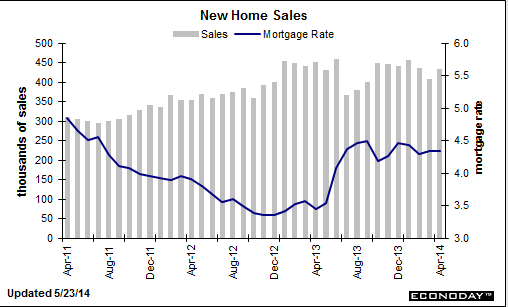

New home sales

Another uninspiring chart, as sales dipped with the cold weather and only partially recovered, down vs same month last year, and, at best, looking very flat as we enter the ‘prime selling season’

Not to mention inventories are up and the composition of sales was towards condos, last I read:

Highlights

April did provide a spring lift to the housing sector at least compared to March, evident in yesterday’s report on existing home sales and especially evident in today’s 6.4 percent jump in new home sales to a higher-than-expected 433,000 annual rate. Also positive is an upward net revision of 11,000 to the two prior months.

A dip in prices contributed to April’s sales strength with the median price down 2.1 percent to $275,800. Year-on-year, the median price is at minus 1.3 percent for only the second negative reading since July 2012. Prices are now in line with sales where the year-on-year rate is minus 4.2 percent.

But, unlike the existing home sales report that shows a sudden swelling in supply, supply on the new home side remains scarce and will remain a negative for sales. Supply was hardly changed on the month, at 192,000 units for sale, while supply at the current sales rate fell to 5.3 months from March’s 5.6 months.

The new home market got an April bounce but against a very weak March. In context, April’s 433,000 is the second weakest rate of the last seven months. Still, the gain is welcome and should give a slight boost to the housing outlook. The Dow is holding at opening highs following today’s report.

Just landed Portland and still somewhat out of close touch.

My concerns remain that the too small federal deficit is keeping a lid on aggregate demand as the demand leakages continue, and the automatic fiscal stabilizers keep tightening the noose even with modest levels of growth.

It’s also possible the monthly employment numbers have been supported by the 1.2 million who lost benefits at year end taking ‘menial’ jobs, which would ‘front load’ jobs to the first several months of 2014, followed by lower than otherwise increases subsequently.

Early car sales forecasts are coming in just over 16 million, so that chart would continue it’s flattish appearance as well.

I’m thinking June numbers will show whether this economy can keep it’s head up with credit expansion sufficient to replace the reduction in govt deficit spending, or head south.

“Contraction in Architecture Billings Index Continues”

Federal budget process: What did Leon Panetta mean?

Federal budget process: What did Leon Panetta mean?

By Duane Catlett and Dan Metzger

May 19 (IR) — Leon Panetta was recently the guest lecturer at the University of Montana’s annual Jones-Tamm Judicial Lecture. Mr. Panetta is a true patriot, having served with distinction for more than 20 years under two presidents. Under President Clinton he directed the Office of Management and Budget and later served as Clinton’s chief of staff. Under President Obama he served as secretary of defense and later as director of the CIA.

Mr. Panetta stated in his lecture that “the nation’s biggest security issue was its inability to deal with the budget.” Although many will interpret his statement as a call to cut the deficit, what he was really criticizing was the Congress’ inability to produce and pass a spending budget that would put some certainty into the ability of the nation to do strategic long term planning.

Like most Washington public servants, Mr. Panetta holds the old-fashioned view that federal budgets should be balanced and the magnitude of deficits is an important metric for the economy. This view is appropriate for households and businesses that have limited financial resources. However, the federal government issues the nation’s currency and is not constrained by financial resources. It has all the financial resources it needs and is constrained only by the nation’s productive resources.

Both political parties are dominated by the false view that the federal budget must be balanced. The only difference is that conservatives think the government has a spending problem and liberals think it is a revenue problem. Both are wrong and it is hurting America’s competitive global advantages.

In the modern world of fiat currency the federal government must focus on real resources (available materials, factories, infrastructure, labor, knowledge) instead of financial resources (money and bonds) in managing the economy. Money is the vehicle that allows the smooth movement of goods and services from sellers to buyers in the economy. The federal government as the sole issuer of the U.S. dollar can issue all the money it needs to move any resources of the nation.

The U.S. and most other nations of the world have used a fiat monetary system since President Nixon defaulted on the gold standard in 1971. Under a gold standard the quantity of money available to the nation is determined by its store of gold, which limits economic growth. Under a fiat system the available money varies with the growth of the economy, and depends on bank loans and federal spending. In the absence of adequate bank loans to make investments in our main-street economy, Congressional budget decisions are responsible for reviving a depressed economy.

The Congressional budget exercise should not be about achieving a balanced federal budget. The budget should be developed to assure that all available resources of the nation are put to good use. There is plenty of work to be done, and we can avoid high unemployment. The federal government can employ all the resources not employed by private industry. If unemployment is high, as it is now, federal deficits are too small.

Many will denounce deficits as causing inflation or adding to a gigantic national debt. They forget to mention that inflation is the result of demand greater than our productive capacity. But, government purchases of either goods or services from labor, which are readily available because of high unemployment, increase total production along with demand, and that benefits businesses. Such purchases are not inflationary.

They also fail to mention that the huge national debt is in reality a huge private asset. The national debt is nothing more than government bonds that individuals, banks, and pension funds hold in their accounts as secure savings instruments.

Mr. Panetta is correct that the nation is weakened when it fails to deal with the budget. But, forcing the federal budget to be balanced either by reducing spending or increasing taxes only hurts our main-street economy by preventing it from growing. Such austerity measures are appropriate only on the rare occasion when the economy is overheated and threatening inflation. A depressed economy, which is what we have today, requires higher spending and lower taxes.

The threat to our future generations is not from a gigantic national debt, which is in reality a gigantic collection of safe and secure savings instruments that will be held by our future generations. The real threat results from the U.S. Congress’ failure to responsibly spend money into circulation to fix our failing bridges, highways, waterways, sanitation systems, public schools, state universities and other public services that we citizens rely on in our daily lives.

Duane Catlett lives in Clancy. He is a retired career Ph.D chemist and materials technology manager. He is a student of Modern Money Theory and the role of government in our economy. Dan Metzger lives in Santa Fe, N.M. He is a retired Ph.D physicist and engineering manager. He is a serious student of Modern Money Theory.

Honorary Degree commencement this Sunday

Warsaw conference

>

> (email exchange)

>

> On May 13, 2014 12:31 PM, Mariusz wrote:

>

> Mr. Mosler,

>

> It’s official, your conference will take place on May 20th starting at 13:00 hrs in REGENT > WARSAW HOTEL (formerly Hyatt) Belwederska 23, 00-761 Warsaw, Poland.

>

> We are still working on some promotional stuff and we’ll be keeping you posted .

>

> Regards

>

> Mariusz

>

That Confounding Mr. Market

That Confounding Mr. Market

By Gary Carmell

Professor Andrea Terzi quoted on CNBC

Well done!!!!

You’d think he’d turn to Brits like Charles Goodhart who wrote volumes on it for the last 50 years!

;)

How QE may be doing more harm than good

By Paul Gambles

May 7 (CNBC) — I’ve spent the last few weeks talking almost entirely about the Bank of England’s (BoE) latest research findings – and that we’re headed toward what could be the most almighty economic and market meltdown ever seen unless we embark on drastic changes in economic policy.

The default reaction to this has tended to be a mixture of incredulity and confusion, with most people wondering “What’s Gambles going on about now?” This piece is an attempt at proclaiming a pivotal moment in economic understanding at a key time for the global economy.

The findings in question are contained in the BoE’s Quarterly Bulletin. The paper’s introduction states that a “common misconception is that the central bank determines the quantity of loans and deposits in the economy by controlling the quantity of central bank money — the so-called ‘money multiplier’ approach.”

This “misconception” is obviously shared by the world’s policymakers, including the U.S. Federal Reserve, the Bank of Japan and the People’s Bank of China, not to mention the Bank of England itself, who have persisted with a policy of quantitative easing (QE).

QE is seen by its adherents, such as former U.S. Federal Reserve Chairman Ben Bernanke, as both the panacea to heal the post-global financial crisis world and also the factor whose absence was the main cause of the Great Depression. This is in line with their view that central banks create currency for commercial banks to then lend on to borrowers and that this stimulates both asset values and also consumption, which then underpin and fuel the various stages of the expected recovery, encouraging banks to create even more money by lending to both businesses and individuals as a virtuous cycle of expansion unfolds.

The theory sounds great.

However it has one tiny flaw. It’s nonsense.

Back in June 2011, when CNBC’s Karen Tso asked me why I was so critical of Ben Bernanke, an acknowledged academic expert on The Great Depression, I explained that I couldn’t justify the leap of blind faith demanded by Bernanke’s neo-classical monetarist theories.

Professor Hyman Minsky was one of the first to recognize the flaw in those theories. He realized that in practise, in a credit-driven economy, the process is the other way round. The credit which underpins economic activity isn’t created by a supply of large deposits which then enables banks to lend; instead it is the demand for credit by borrowers that creates loans from banks which are then paid to recipients who then deposit them into banks. Loans create deposits, not the other way round.

In the BoE’s latest quarterly bulletin, they conceded this point, recognizing that QE is indeed tantamount to pushing on a piece of string. The article tries to salvage some central banker dignity by claiming somewhat hopefully that the artificially lower interest rates caused by QE might have stimulated some loan demand.

However the elasticity or price sensitivity of demand for credit has long been understood to vary at different points in the economic cycle or, as Minsky recognized, people and businesses are not inclined to borrow money during a downturn purely because it is made cheaper to do so. Consumers also need a feeling of job security and confidence in the economy before taking on additional borrowing commitments.

It may even be that QE has actually had a negative effect on employment, recovery and economic activity.

This is because the only notable effect QE is having is to raise asset prices. If the so-called wealth effect — of higher stock indices and property markets combined with lower interest rates — has failed to generate a sustained rebound in demand for private borrowing, then the higher asset values can start to depress economic activity. Just think of a property market where unclear job or income prospects make consumers nervous about borrowing but house prices keep going up. The higher prices may act as either a deterrent or a bar to market entry, such as when first time buyers are unable to afford to step onto the property ladder.

Dr Andrea Terzi, Professor of Economics at Franklin University, also suggests that many in the banking and finance industry, who often have trouble with the way academics teach and discuss monetary policy, will find the new view much closer to their operational experience. “The few economists who have long rejected the ‘state-of-the-art’ in their models, and refused to teach it in their classrooms, will feel vindicated,” he adds.

Foremost among those economists is Prof Steve Keen: a long-time proponent of the alternative view, endogenous money. Having co-presented with Prof. Keen, I’ve been taken with the way that his endogenous money beliefs stand up to ‘the common sense test.’ The proverbial ‘man on the Clapham omnibus’ knows that borrowing your way out of debt while your returns are dwindling makes no sense. Friedman and Bernanke couldn’t see that.

Ben Bernanke positioned himself as a student of history who had learned from the mistakes of the past. Dr. Terzi questions this, “This view that interest rates trigger an effective ‘transmission mechanism’ is one of the Great Faults in monetary management committed during the Great Recession.”

“The reality is that the level of interest rates affects the economy mildly and in an ambiguous way. To state that monetary policy is powerful is an unsubstantiated claim.”

For a central bank to recognize that its economic understanding is flawed is a major admission. However, unless it takes the opportunity to correct its policy in line with this new understanding then it will repeat the same old mistakes.

The world’s central banks are steering a course unwittingly directly towards a repeat of the 1930s but on a far greater scale. It’s not yet clear that there is any commitment to change this course or indeed whether there is still time to do so. Either way, it will be very interesting to see what future economic historians make of Ben Bernanke’s contribution to economic policy.

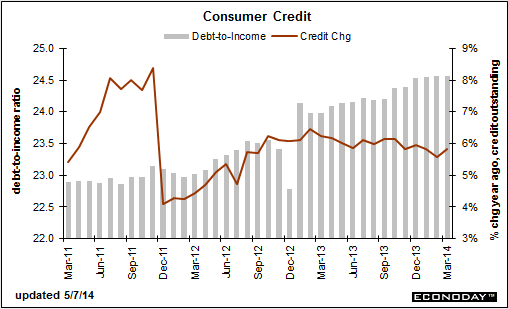

Consumer credit

Keeps coming back to fiscal for me.

I see the year over year change going from up nicely to flattening/decelerating as the tax hikes, followed shortly after by the sequesters, took their toll. And with the federal deficit way down, that ‘spending more than income’ isn’t there to help offset the ever growing ‘demand leakages’, meaning we need that much more ‘borrowing to spend’ to grow, etc.

So far, with GDP tracking at about -.5 for q1 and +4.5 for q2, that’s about a +2% first half, down a lot from H2 2013, which I saw as higher than otherwise due to inventory building and ‘mysterious’ year end surges that had the appearance of spending ahead of expiring tax credits, etc.

So I see what’s happened (and worse) as consistent with my narrative, with the evidence looking more and more like the demand leakages may now be ‘winning the race.’

Which also explains the long bond coming down in yield??? ;)

Consumer Credit

Highlights

Credit card debt is not building, a plus for consumer wealth perhaps but a definite minus for store sales. Consumer credit did expand by a sharp $17.5 billion in March but, as has been the case since the 2008 financial meltdown, the gain is centered almost entirely in non-revolving credit which continues to get a boost from strong vehicle sales and the government’s acquisition of school loans from private lenders. Revolving credit is barely showing any life, up $1.1 billion following a decline of $2.7 billion in February.