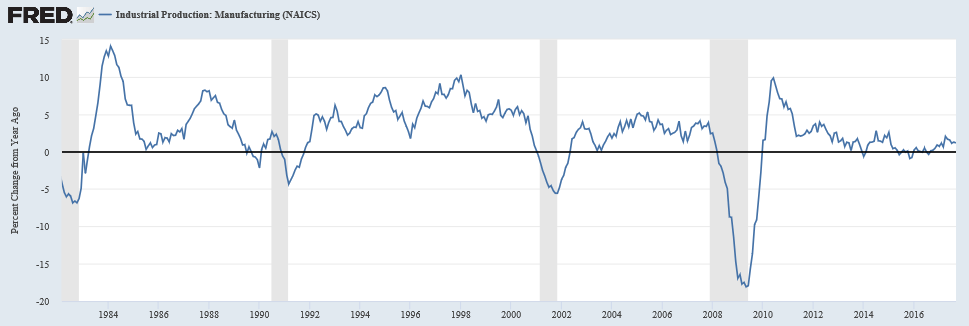

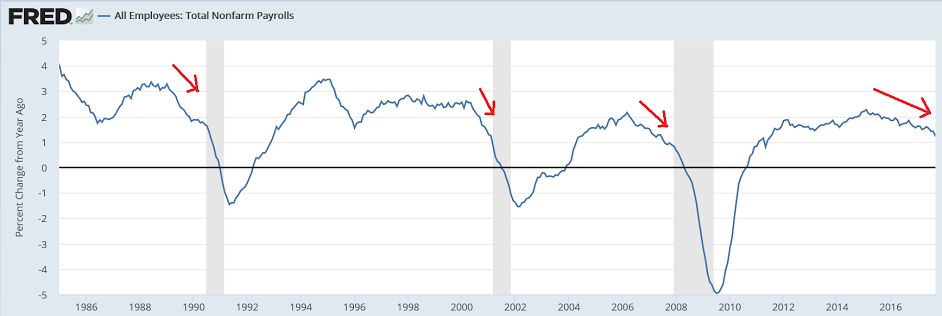

Yet another chart that looks like we might already be in recession:

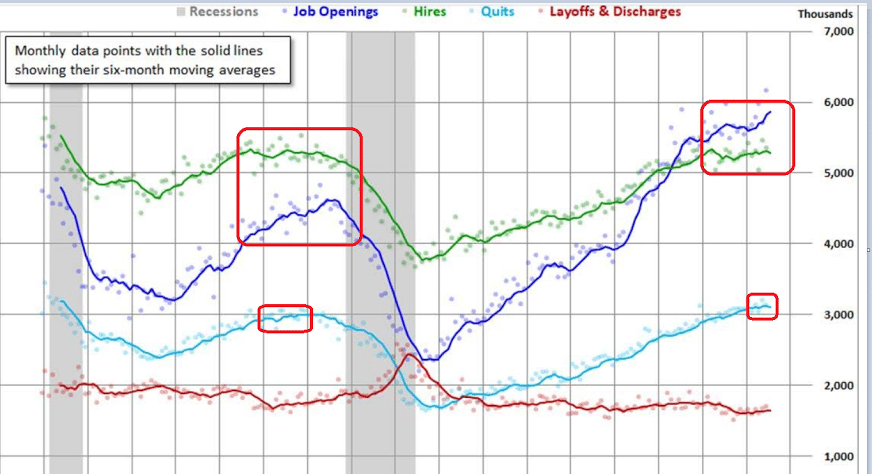

Hires quits were the leading indicators in the last cycle:

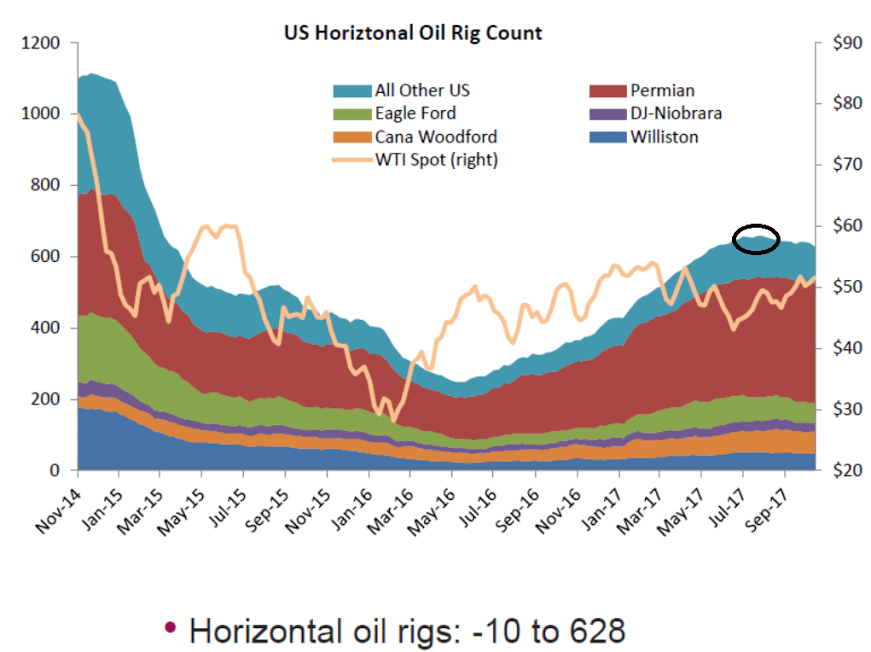

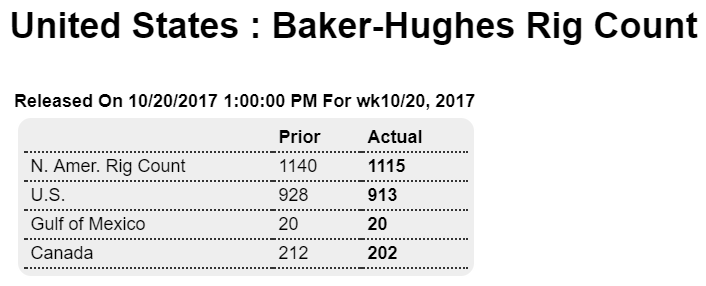

Rig count peaked a few months ago:

Yet another chart that looks like we might already be in recession:

Hires quits were the leading indicators in the last cycle:

Rig count peaked a few months ago:

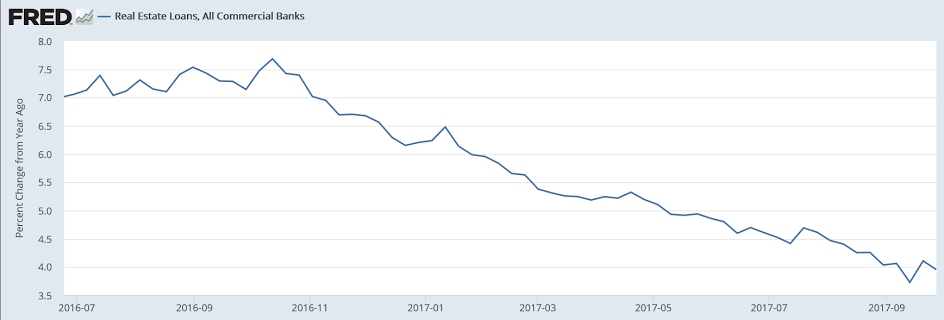

Now down year over year, and in line with the deceleration in bank mortgage lending:

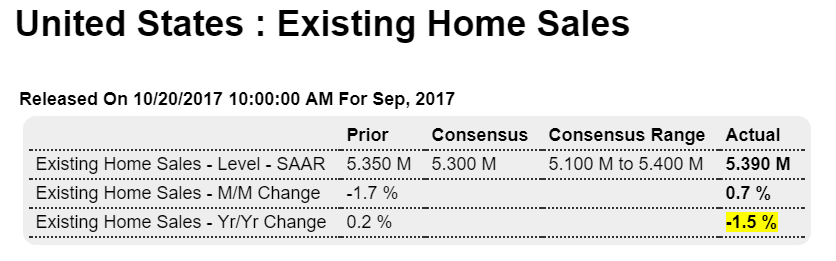

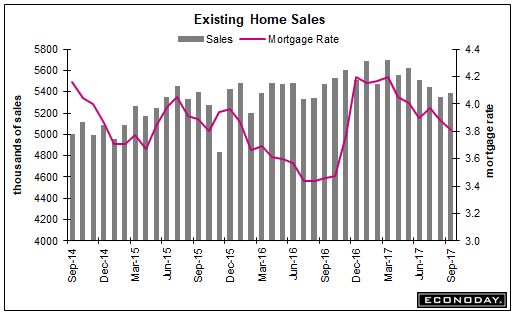

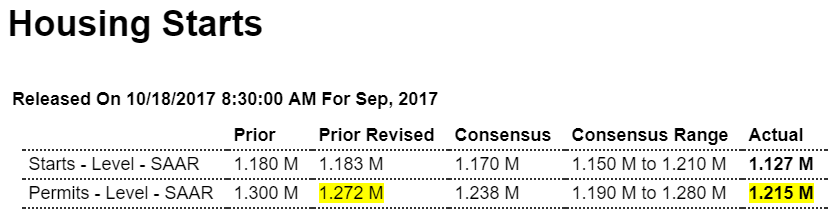

Highlights

Existing home sales posted their first gain in four months, rising 0.7 percent in September to a 5.390 million annualized rate that is near Econoday’s top forecast. Hurricane effects are hard to gauge with the National Association of Realtors reporting that sales in Florida were down substantially though sales in Houston have already recovered.

The sales gain came at a price discount as the median fell 3.2 percent to $245,100 for what is still, however, a respectable 4.2 percent year-on-year gain. Supply is still very tight, at 1.900 million resales on the market which makes for a useful 1.6 percent gain though the yearly rate is down 6.4 percent. On a sales basis, supply is unchanged at only 4.2 months.

Sales in the South fell 0.9 percent in September and follow August’s 5.7 percent decline. These may be hurricane effects but they’re not overly substantial given mixed readings in other regions. All regions are either slightly lower to flat year-on-year.

And overall sales are flat, down 1.5 percent compared to September last year. Yet this report is positive for what is a lukewarm housing sector. Watch for sales of new homes and pending sales of existing homes on next week’s calendar.

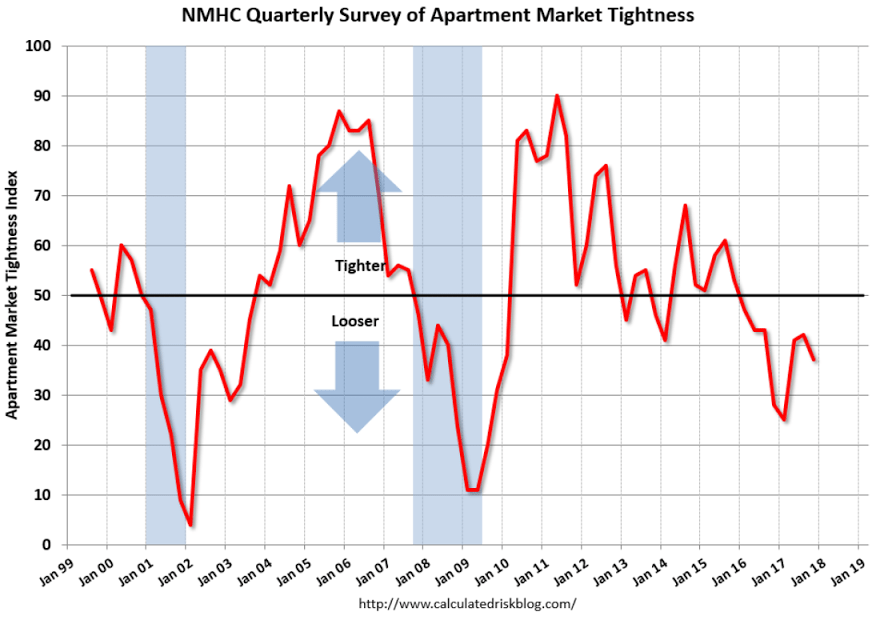

This peaked a while back and continues to fade:

Highlights

The Baker Hughes North American rig count is down 25 rigs in the October 20 week to 1,115. The U.S. rig count is down 15 rigs at 913 but is up 360 rigs from last year at this time. The Canadian count is down 10 rigs from last week at 202 but compared to last year is up 59 rigs.

For the U.S. count, rigs classified as drilling for oil are down 7 rigs at 736 while gas rigs are down 8 at 177. For the Canadian count, oil rigs are down 5 at 107 and gas rigs are also down 5, at 95 rigs.

The week’s large drop is the fourth consecutive weekly decline in the count, and is partly caused by seasonality as cold weather begins to curtail operations in northern regions, and partly probably by lingering hurricane damages, with Texas down 8 rigs to 436.

Schlumberger, Baker Hughes Warn Of N. America Slowdown

Oct 20 (Reuters) — Schlumberger Ltd and Baker Hughes, the world’s top two oilfield services firms, warned on Friday of a slowdown in North America and a challenging year ahead as crude oil prices stay volatile.

Schlumberger said investments in North America were moderating as energy companies increasingly shied away from chasing higher production at the cost of financial returns.

“Oil prices remain volatile and, as a result, our customers remain cautious,” Baker Hughes Chief Executive Lorenzo Simonelli said.

The company, in its first report to include GE Co’s oil and gas business since their merger, reported a quarterly profit that missed analysts estimates by a wide margin.

Schlumberger reported a 53 percent jump in revenue from North America, its biggest market, in the latest quarter, but cautioned that activity had been slowing.

“In the U.S. Gulf of Mexico, activity continued to weaken in the third quarter, and the outlook remains bleak for this region based on current customer plans,” Schlumberger said.

The company’s results and warnings come amid slowing drilling activity in North America.

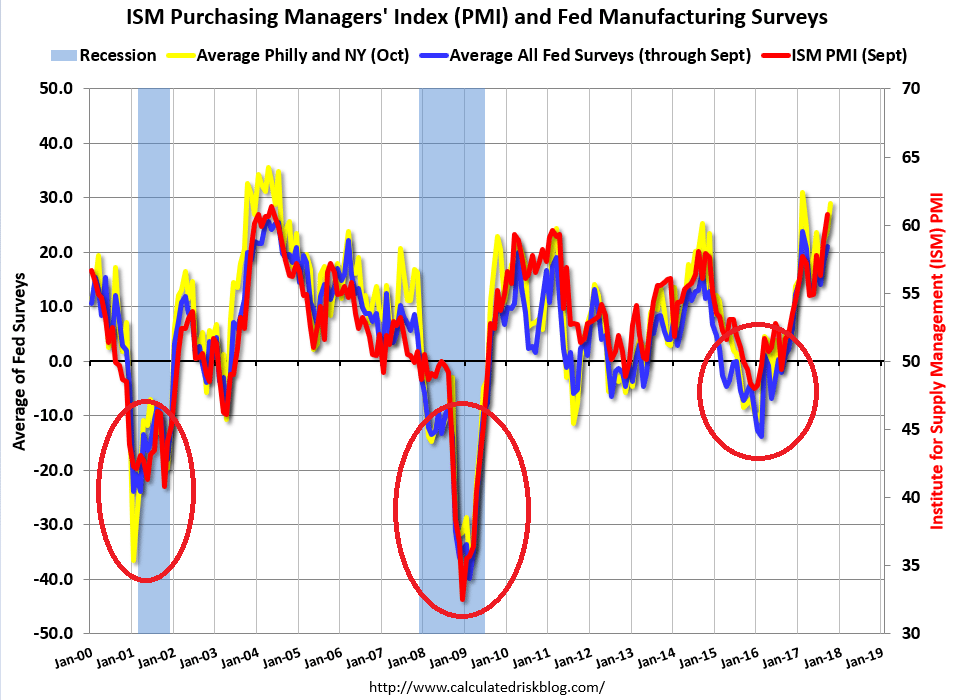

These surveys are the ‘soft data’ that’s looking good. They all gapped higher around election time and have remained elevated. In fact it looks like there’s already been a recession followed by a recovery:

Unfortunately the ‘hard data’ isn’t looking so good:

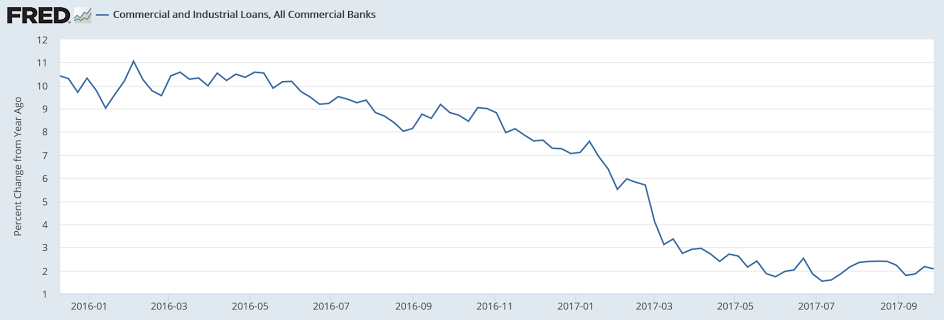

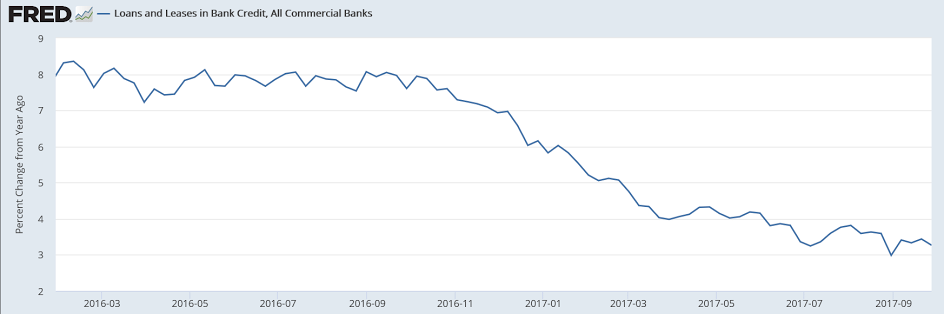

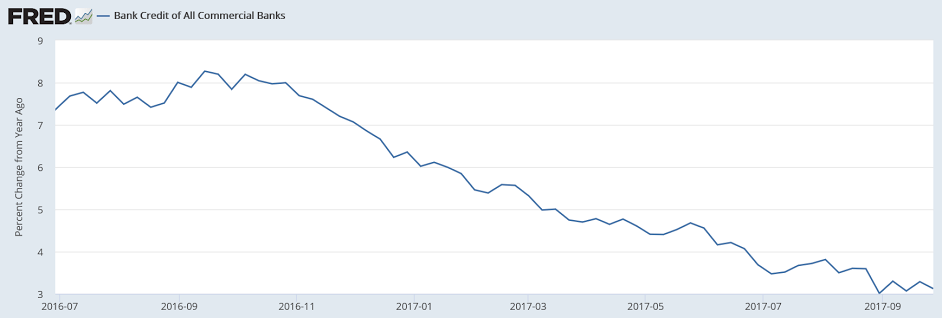

Continuing evidence that the slowdown in bank lending is reflecting slowdowns in the macro economy:

Highlights

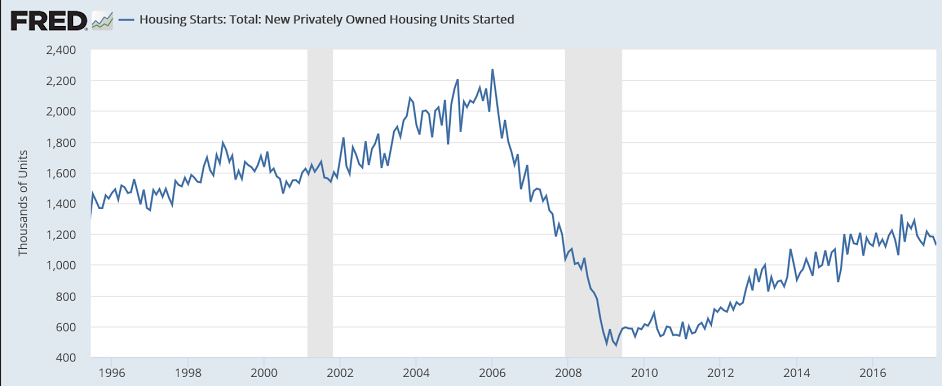

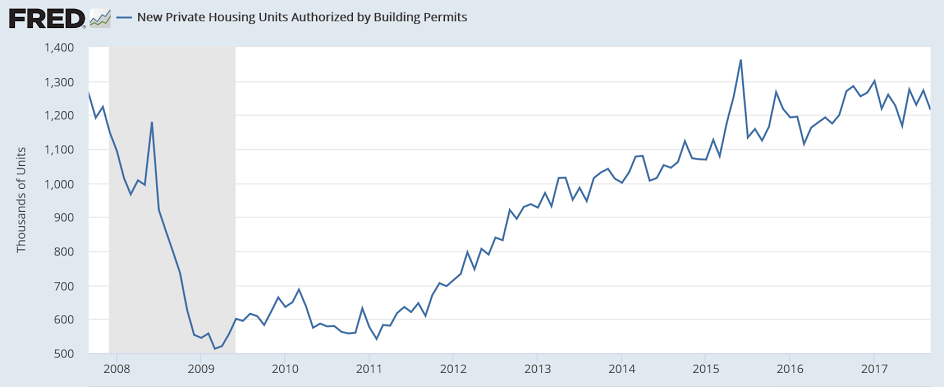

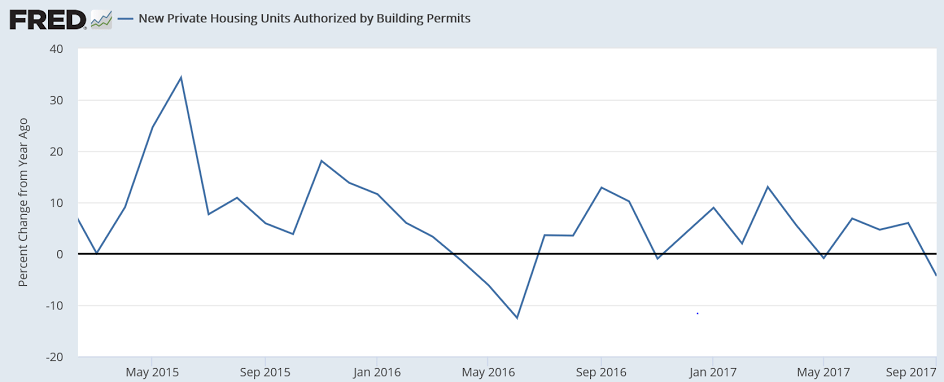

Single-family permits continue to rise in what, however, is the main positive in an otherwise weaker-than-expected housing starts and permits report. Looking first at headline totals, starts fell 4.7 percent in September to a 1.127 million annualized rate which is well under Econoday’s low estimate. Permits fell 4.5 percent to a 1.215 million rate that is above the low estimate but below the consensus for 1.238 million. Hurricane effects aren’t striking despite affected areas accounting for more than 1/4 of the total.

First the good news as permits for single-family homes rose 2.4 percent to an 819,000 rate and a year-on-year gain of 9.3 percent. Single-family homes are the backbone of the housing sector and strength here not only points to greater supply in the new home sales market but also to gains ahead for residential investment in the GDP report.

Not good news are permits for multi-family units which fell 16.1 percent to a 396,000 rate with this yearly rate at minus 24.0 percent. Multi-family units had shown strength earlier in the year but have since tailed off.

Starts for multi-family units fell 5.1 percent to a 298,000 rate with single-family starts down 4.6 percent to 829,000. Single-family completions offer some good news, up 4.6 percent to a 781,000 rate and adding immediate supply to the market.

Regional data do show what is likely hurricane-related weakness in the South, where starts fell 9.3 percent to 527,000 following August’s 4.9 percent decline. Yet also weak were starts in the Midwest, down 20.2 percent to 154,000, and also the Northeast, down 9.2 percent at 119,000.

Housing has been generally slowing and looks to end 2017 no better than flat. Still, permits and completions for single-family homes are solid pluses.

President Trump admits he’s trying to kill Obamacare. That’s illegal.

The president has a right not to like the ACA. But so long as it is the law of the land, he does not have the right undermine it through the use of executive power.

“Faithful” execution of a law that is validly on the books is what the words of the Constitution require of Trump — until Congress decides otherwise.

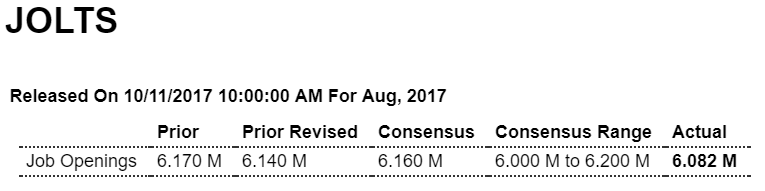

I read this as weakening demand and employers unwilling to pay up to hire, and maybe even posting openings to replace existing workers at lower wages:

Highlights

Job openings held steady at a very abundant 6.082 million in August while hirings remained far behind, at 5.430 million. In an early indication of full employment, the gap between openings and hiring first opened up about 2-1/2 years ago signaling that employers are either not willing to offer high enough pay to fill empty positions and/or are having a hard time finding people with the right skills. At 652,000, the current spread between openings and hirings is one of the very widest on record.

For comparison, the number of job seekers who are out actively pounding the pavement is 6.911 million which is very near the total number of available openings. Today’s results offer further evidence that the economy is at full employment and will likely add urgency for further Federal Reserve rate hikes.

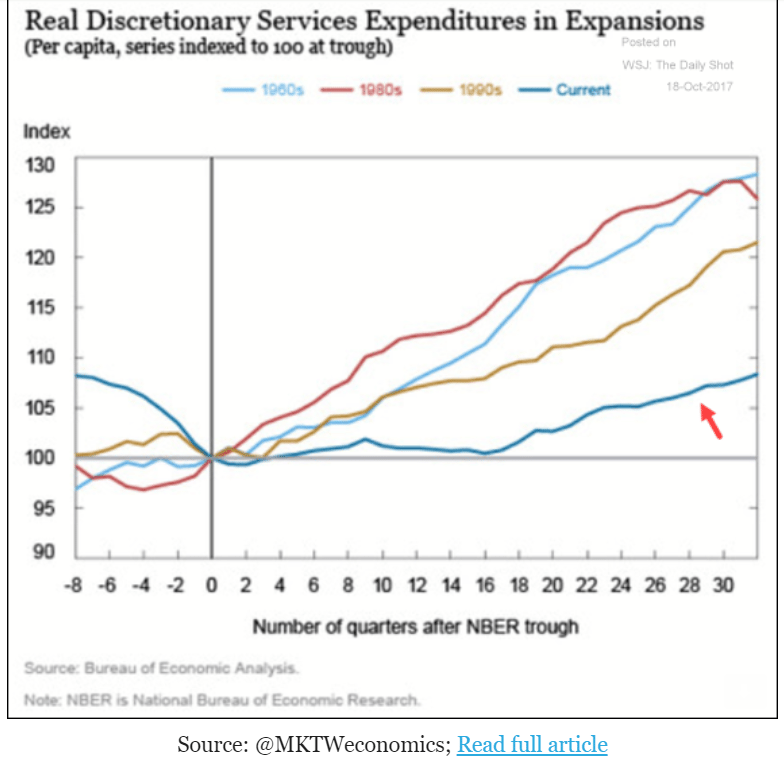

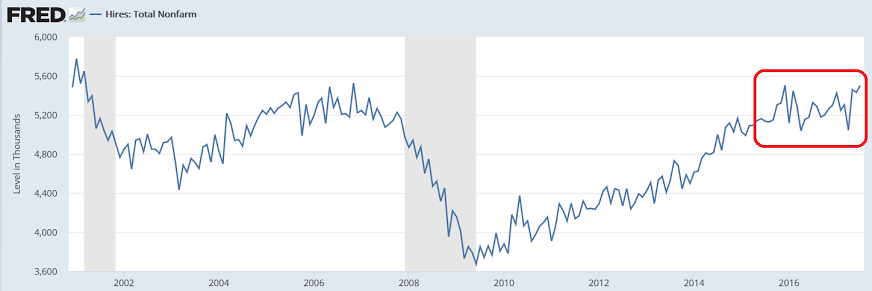

Hires have gone flat and on a per capita basis are far lower than the prior cycle:

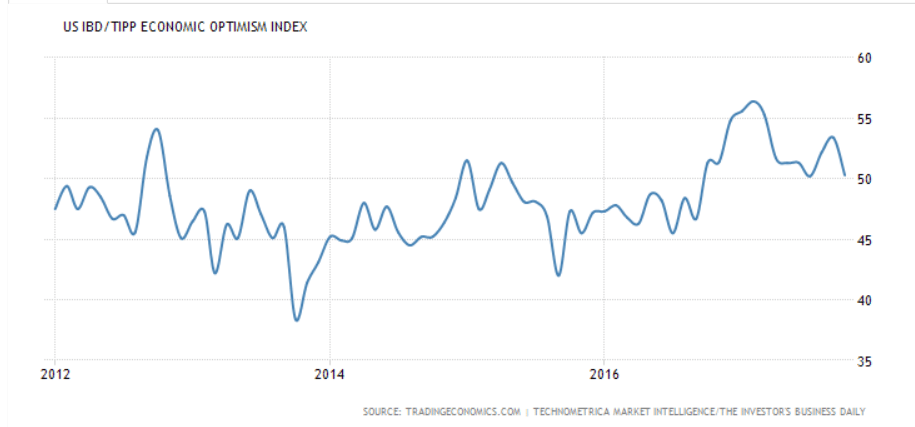

More evidence Trumped up expectations are fading:

United States IBD/TIPP Economic Optimism Index

The IBD/TIPP Economic Optimism Index in the United States fell 5.8 percent from the previous month to 50.3 in October 2017, below market expectations of 54.2. The gauge of the six-month economic outlook declined 4.7 percent to 48.7; and the personal financial outlook index dropped 4 percent to 59.5. Also, the measure of confidence in federal economic policies decreased 9.1 percent to 42.8.

President Donald Trump suggested he’s smarter than Secretary of State Rex Tillerson, saying in an interview published Tuesday that if Tillerson did call him a moron, as reported, the two should ‘‘compare IQ tests.’’

“And I can tell you who is going to win,” Trump said to Forbes magazine.

Trump reportedly wanted nearly 10 times more nuclear weapons

President Donald Trump discussed increasing the number of U.S. nuclear weapons by nearly 10 times at a July meeting with top national security officials, according to NBC News. After the meeting, Secretary of State Rex Tillerson was heard calling Trump a “moron,” NBC reported.

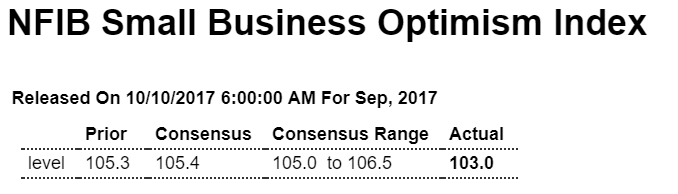

Trumped up expectations continue to unwind, though still above pre election levels, and note the details:

Highlights

The small business optimism fell 2.3 points in September to 103.0, led by a sharp drop in sales expectations, not only in states affected by hurricanes in Texas and Florida, but across the country. The surprising drop put the index at the lowest level of the year after hovering just below the 12 year high set in January, and came in not only below the consensus forecast of 105.4 but below the range of analysts’ forecasts.

Of the ten components making up the index, 6 declined, 3 rose and 1 was unchanged. The most severe declines were registered in sales expectations, which fell 12 points to 15, and now is a good time to expand, falling 10 points to 17. But planned increases in capital outlays by small business owners also fell significantly, with the component shedding 5 points to 27.

Despite the sharp drop in sales expectations, the one bright spot of the report was the net percentage of small business owners planning to increase inventories, which rose by 5 points to 7, as more owners expected a strong quarter.

The employment front also remained very strong, with the net percentage of business owners planning to increase employment rising by 1 point to 19 while current job opening slipped by just a point to a still exceptionally strong 30.

Though the level of optimism remains very high by historical standards and despite the month’s decline still surpasses any month in previous years going back to 2006, the September survey indicates the frothy expectations of business-friendly health reform and lower corporate taxes have cooled noticeably in September. Moreover, NFIB noted that optimism may have actually declined more than its survey indicates, since it was likely that reporting members in Florida and Texas were underrepresented because of disruptions.

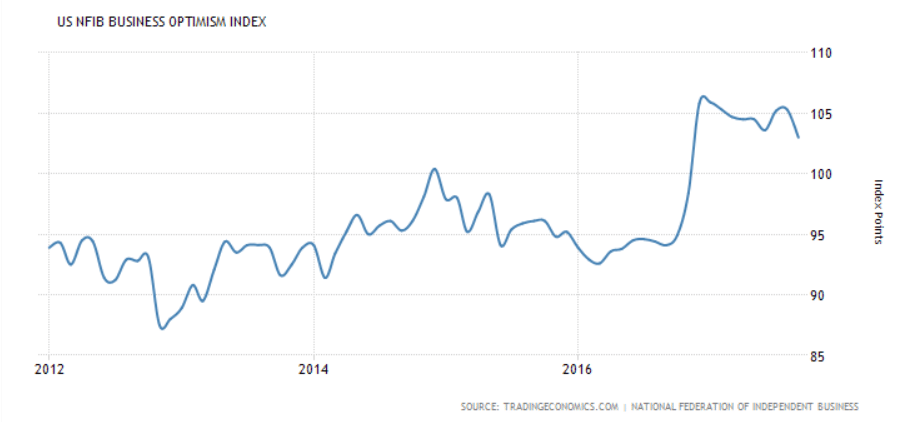

Optimism Among US Small Businesses at 10-Month Low

The NFIB’s Index of Small Business Optimism in the US fell to 103 in September 2017 from a six-month high of 105.3 in August, and below market expectations of 105.1. It was the lowest reading since November last year, as 6 of 10 index components declined: Higher sales expectations (-12 pp to net 15 percent); good time to expand (-10 pp to 17 percent); plans to make capital outlays (-5 pp to 27 percent); expectations the economy will improve (-1 pp to 30 percent); current job openings (-1 pp to 30 percent); and expected credit conditions (-1 pp to -3 percent). On the other hand, earnings trends were flat (at -11 percent) and improvement was observed for: Plans to increase inventories (+5 pp to 7 percent); current inventory (+2 pp to -3 percent); and plans to raise employment (+1 pp to 19 percent).

This index is down in line with decelerating commercial real estate bank borrowings:

A few comments on share buybacks:

Once a company decides it has ‘excess cash’ the options are dividend payments or share buybacks.

After a dividend payment the company has that much less cash and shares outstanding remain the same.

After a share buyback the company has that much less cash and shares outstanding are reduced.

Now consider that after a reverse split the company has the same cash and there are fewer shares outstanding.

Therefore, for the company, share buybacks are functionally equivalent to a dividend payment combined with a reverse split, as in either case the company has less cash and there are fewer shares outstanding.

But for executive compensation related calculations, a reverse split reduces share count or increases option strike prices, while buybacks do no alter executive share count and option strikes.

Seems the accounting process should disclose any increases in executive compensation due to share buybacks?

Seems the accounting process should disclose any increases in executive compensation due to share buybacks?

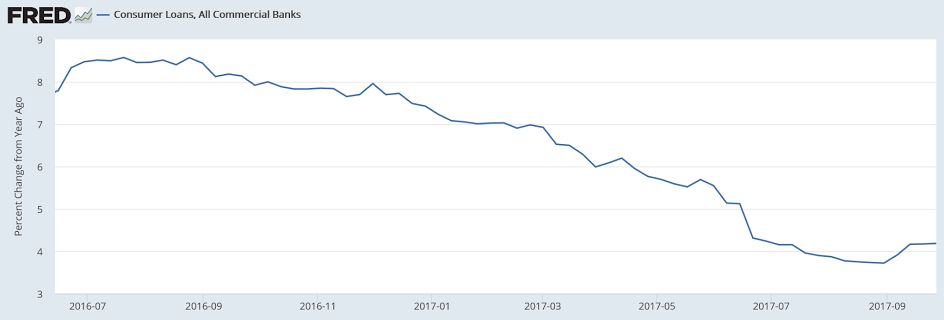

Appears to be leveling off at much lower rates of growth than last year, as reflected by weaker than expected data releases and revisions:

Year over year growth has been decelerating for all practical purposes in a straight line, as per the chart. And the downward revisions in prior months are further evidence of the weakness which began with the collapse in oil capex at the end of 2014. And wage growth increased at least partially because the jobs lost were largely those of lower income workers.

Also, at this point with low levels of deficit spending, both public and private, the economy is more likely to be path dependent. In other words, a drop in employment and sales for any reason is also a drop in income which probably means less subsequent spending, less income, etc. etc. but it take another month or so of data to see if that’s what’s happening:

Highlights

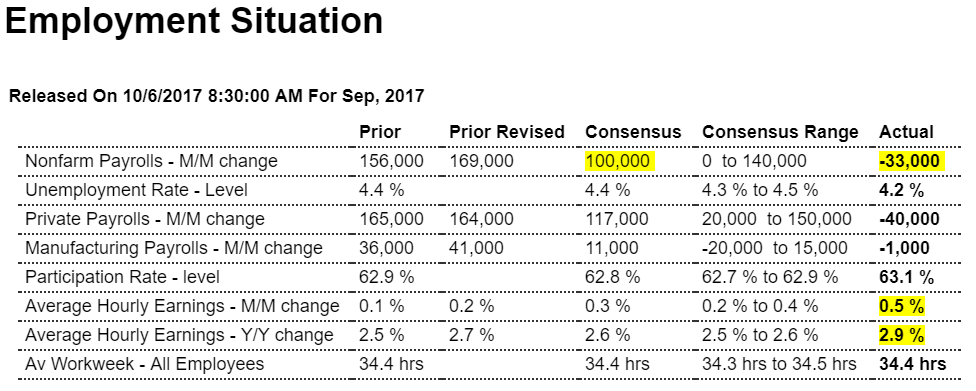

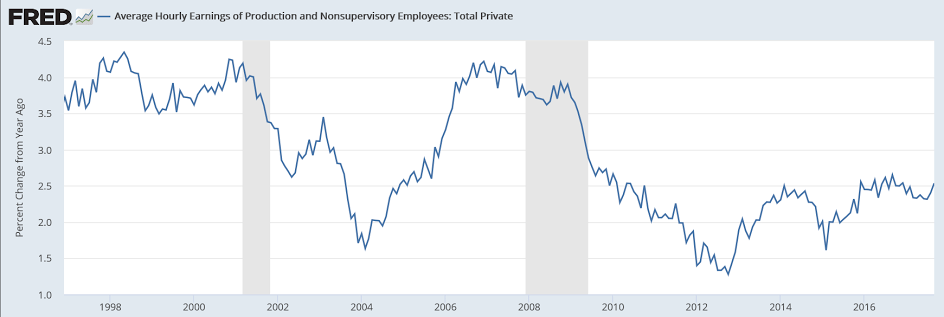

The Department of Labor can’t quantify September’s hurricane effects on payrolls or the unemployment rate but they appear to be very dramatic nonetheless. Nonfarm payrolls were negative in September and, at minus 33,000, were well below Econoday’s low estimate. But the big surprise in today’s report are sudden indications of excessive labor market tightness as the unemployment rate fell 2 tenths to 4.2 percent and average hourly earnings spiked 0.5 percent with the year-on-year rate jumping 4 tenths to 2.9 percent. This report on the surface — and needing confirmation from the October employment report to follow next month — appears to change the dynamics for the labor market and suggests that the Federal Reserve, the decline in September payrolls aside, has fallen behind the inflation curve.

The 0.5 percent spike in earnings now matches July, which has been revised 2 tenths higher, as the strongest monthly surge of the expansion. The 2.9 percent yearly rate matches December last year as the expansion high. Revisions here are important and very sharp with August’s monthly change revised 2 tenths higher to a 0.3 percent increase with the yearly rate revised 2 tenths higher to 2.7 percent.

The 4.2 percent unemployment rate, derived from a separate set of data that also include the self-employed who are not on payrolls, is not only lowest of the expansion but of the prior expansion as well, going all the way back to January 2001. Here employment, likely reflecting a jump in those now actively looking for work, rose 906,000 at the same time that the number of unemployed fell 331,000. The pool of available workers which includes those who can work but aren’t pounding the pavement fell a very sizable 547,000 to 12.429 million. This reading is a sleeper in this report and points squarely at the risk of a wage flash point. The labor participation rate, reflecting the move toward employment, rose 0.2 percent to 63.1 percent to exceed Econoday’s high estimate by 2 tenths.

Turning now to payrolls, they were pulled lower by a 104,700 drop at restaurants. Again, the Labor Department says it can’t pin this on hurricanes but it does seem likely. Both August and July nonfarm payrolls were revised lower by a net 38,000. Manufacturing payrolls fell 1,000 in September following an upward revised 41,000 surge in August but also following a sharply downward revised 11,000 decline in July. But averaged together and including a 21,000 rise in June, manufacturing is definitely improving and is a further risk to wage inflation.

Other data include, in what perhaps is a surprise given the hurricane disruptions in the South, no change in the workweek, at 34.4 hours in a measure that tracks all private sector employees. Government payrolls are a positive in the report, up 7,000 and making for a 40,000 decline in private payrolls in what, in an aside, is yet another miss for ADP which called here for respectable growth.

The hurricanes are one factor that may or may not have skewed payrolls sharply lower, and probably did, but it’s the wage pressures that will make everyone on the FOMC, even the most dovish, suddenly concerned that wage-push inflation has arisen from the dead. The Department of Labor hasn’t offered adequate explanations of these results which puts the focus on individual Fedspeak with the chances of a rate hike at the month-end meeting, let alone the December meeting, now likely in play.

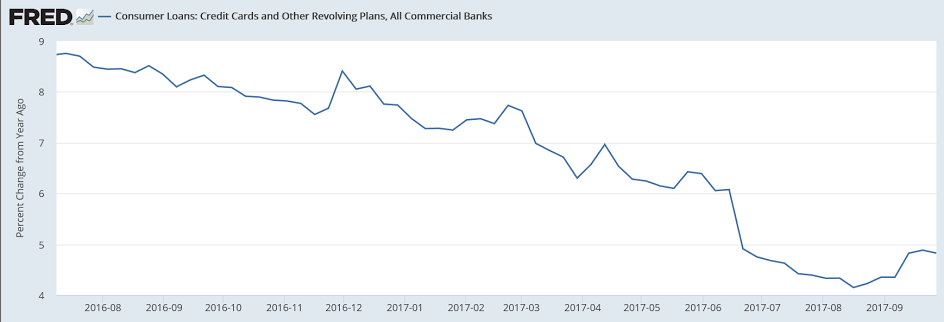

Even with this recent ‘spike’ it’s still very low by historically:

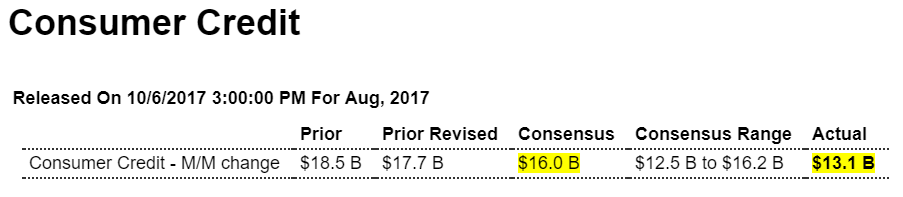

The deceleration continues, in line with recent data showing a deceleration in consumer spending. The jump in credit card borrowing could be due to falling incomes, aka ‘dipping into savings’, and also an unsustainable process:

Highlights

Consumer credit rose a lower-than-expected $13.1 billion in August which masks, however, a sharp gain for revolving credit. This component, which is where credit-card debt is tracked, rose a sizable $5.8 billion in a gain that will renew talk of slackening credit standards among lenders. The gain for the nonrevolving component, where auto financing and also student loans are tracked, is an undersized $7.3 billion and explains the weakness in the headline. But this report is not about weakness but about strength, at least strength for consumer spending.

This is social security at work vs a low demand economy where support for labor has been removed. Game theory tells you ‘the labor market’ isn’t a ‘fair game’ as people need to work to eat, while business only hires if it likes the returns on investment:

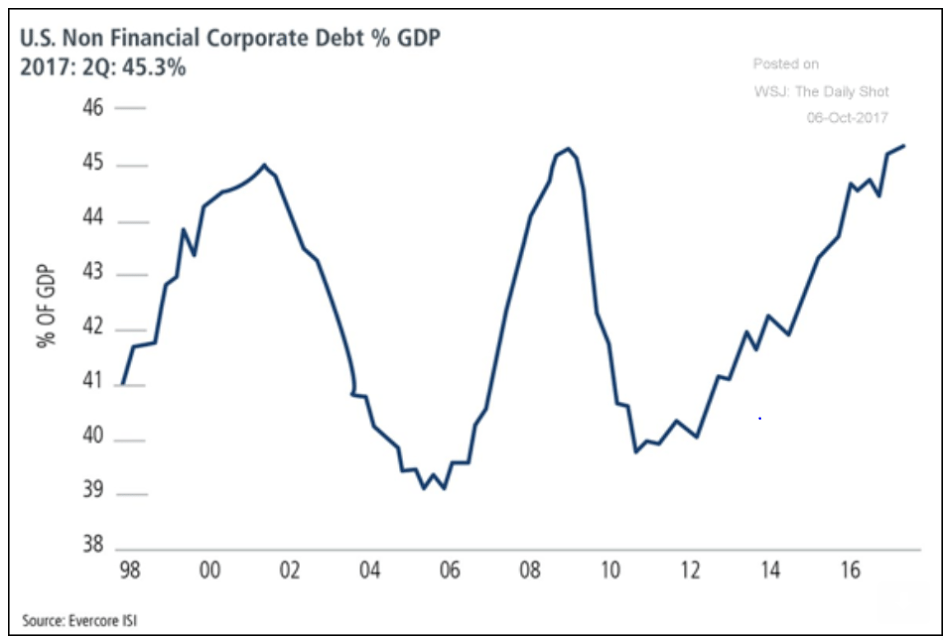

Another way to look at corporate debt. Note that it grew slower this cycle, which is in line with slower gdp growth. Second, this is about as high as it’s gotten in past cycles and when it’s no longer contributing to growth GDP tends to slow. Third, looks like it flattened with the collapse of oil capex, then had a move up, and has most recently turned sideways:

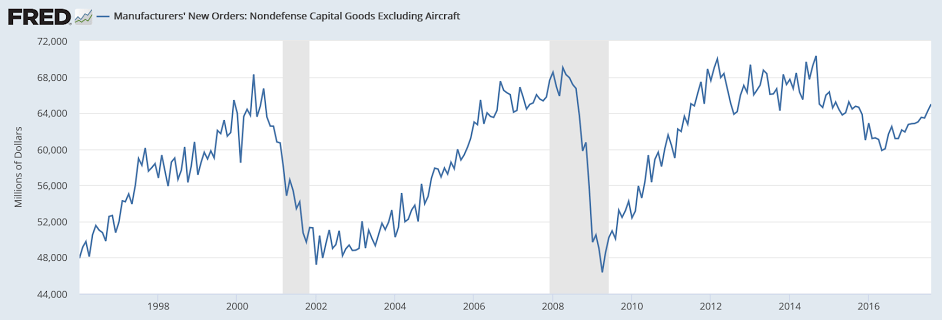

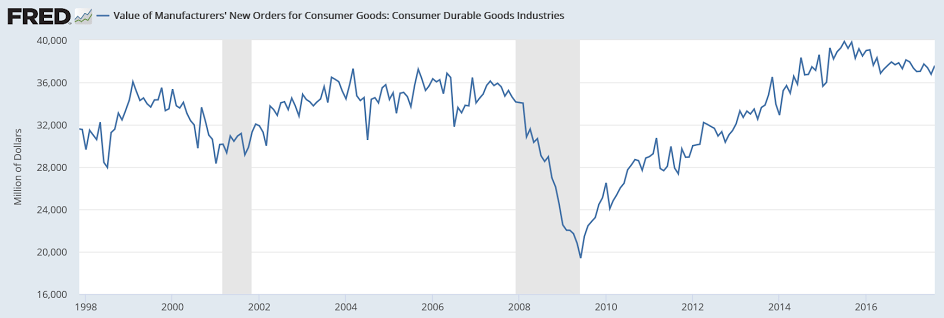

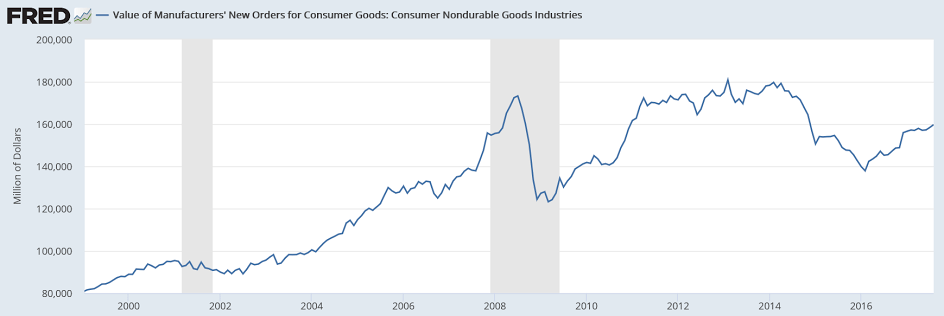

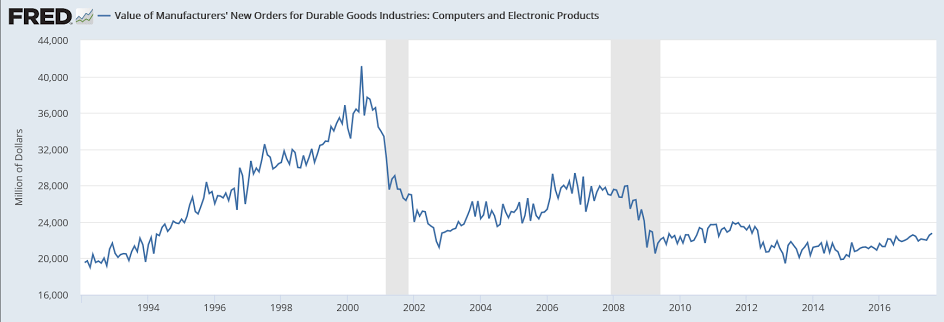

You can see from the longer term charts not much to write home about here:

Highlights

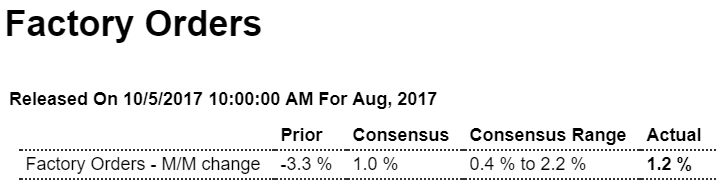

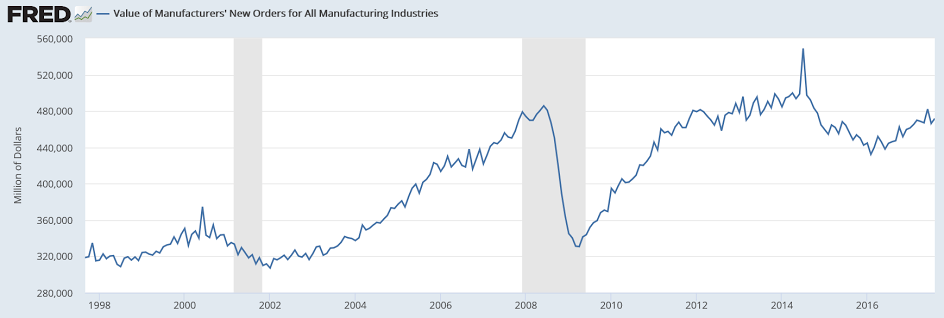

Increasing strength in capital goods is the good news in today’s factory orders report where a headline 1.2 percent gain is 2 tenths above Econoday’s consensus. The split between the report’s two main components shows a 2.0 percent gain for durable goods, which is a 3 tenths upgrade from last week’s advance report, and a 0.4 percent gain for non-durable goods which is the fresh data in today’s report and reflects gains for petroleum and coal. Hurricane Harvey’s late month impact was not able to be quantified by the Commerce Department though its effects appear to be marginal.

Sticking to durables, today’s report upgrades core capital goods orders (nondefense ex-aircraft) to monthly gains of 1.1 percent in August and 1.3 percent in July versus prior readings of 0.9 and 1.1 percent. Shipments for core capital goods, which are inputs into GDP business investment, are revised a very sharp 4 tenths higher in August to 1.1 percent offset only in part by a 1 tenth downward revision to July to what is a still very sharp gain of 1.0 percent.

Commercial aircraft is always volatile in this report with orders up 72 percent following a drop of 83 percent in August-to-July swings that are behind the monthly swings in the headline. Vehicles are another positive in today’s report, up 0.7 percent for orders following a 2.2 percent drop in July. Excluding transportation equipment, which is considered a smoother barometer for underlying change, orders are up 0.4 and 0.5 percent the last two months.

Unfilled factory orders were unchanged in the month following the July’s 0.3 percent decline. Weakness here is not a positive indication for factory labor demand. But shipments, up 0.5 percent, are very favorable as are inventories which are keeping pace with a 0.4 percent rise that keeps the inventory-to-shipments ratio unchanged at 1.38.

The strength in ex-transportation and especially capital goods are outstanding positives and help offset what has been a very disappointing run in the manufacturing component of industrial production, a separate report released by the Federal Reserve, where August fell 0.3 percent and July was unchanged. Today’s factory orders report closes the book on what was, despite Hurricane Harvey, a mostly strong August for manufacturing.

This is not adjusted for inflation:

Note the .com/y2k boom:

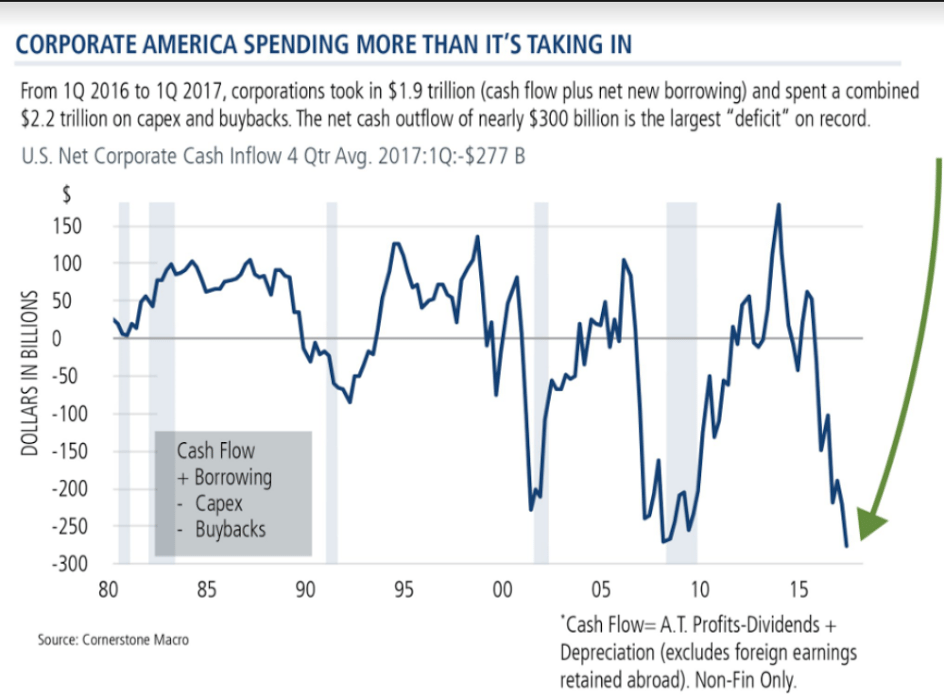

Looks like we’ve been getting a bit of help from corporate ‘deficit spending’ which works to support gdp growth,-to the extent it’s ultimately spent on goods or services- while it lasts. And while this may have further to go, it is not, as Wynne Godley used to say, a sustainable process:

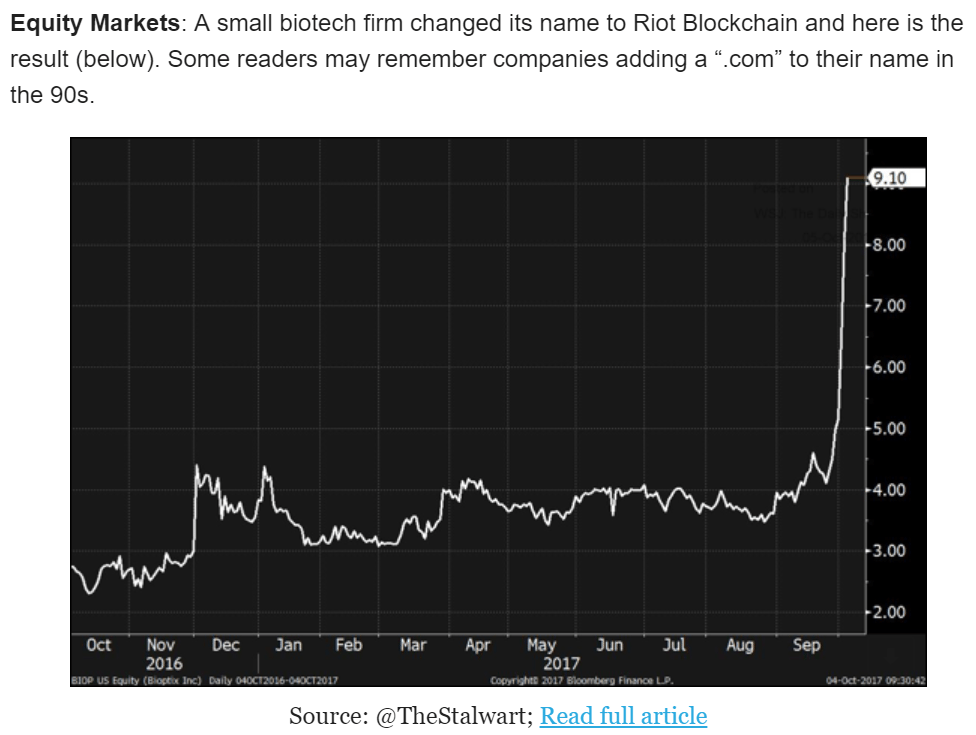

Call a tulip a blockchain…

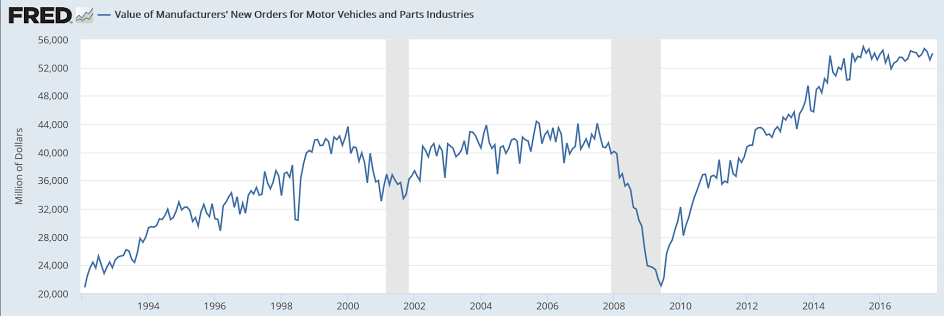

Nice spike after the hurricane lull:

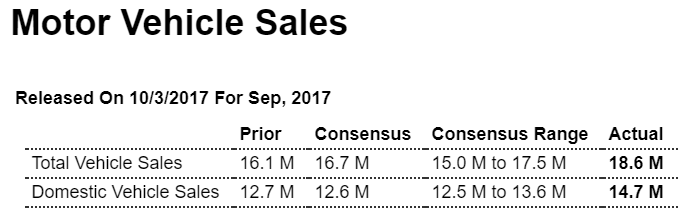

Highlights

In the strongest monthly sales performance in 12 years, unit vehicle sales shot up to a hurricane-fueled 18.6 million annualized rate in September vs a hurricane-depressed 16.1 million rate in August. September’s rate points squarely at replacement demand following Hurricane Harvey’s flooding of Houston just as the weak August rate pointed to the initial negative effects of the hurricane. Today’s results point to a substantial surge for the motor vehicle component of the retail sales report and a major boost for what was a weak overall report in August. Sales of domestic-made vehicles rose to 14.7 from August’s 12.7 million.

President Trump just set a new standard in his search for flattery, this time in hurricane-ravaged Puerto Rico

He thanked Puerto Rico’s non-voting representative in Congress, Jenniffer Gonzales Colon, for “saying such nice things” about the administration’s response. He repeated his appreciation for Puerto Rico’s governor, Ricardo Rosselló, as someone who “did not play politics.”

The evidence? “He was giving us the highest grades,” the president said.

I got a mention here: