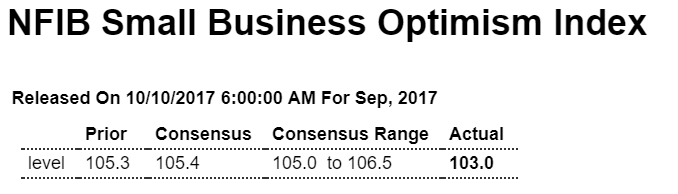

Trumped up expectations continue to unwind, though still above pre election levels, and note the details:

Highlights

The small business optimism fell 2.3 points in September to 103.0, led by a sharp drop in sales expectations, not only in states affected by hurricanes in Texas and Florida, but across the country. The surprising drop put the index at the lowest level of the year after hovering just below the 12 year high set in January, and came in not only below the consensus forecast of 105.4 but below the range of analysts’ forecasts.

Of the ten components making up the index, 6 declined, 3 rose and 1 was unchanged. The most severe declines were registered in sales expectations, which fell 12 points to 15, and now is a good time to expand, falling 10 points to 17. But planned increases in capital outlays by small business owners also fell significantly, with the component shedding 5 points to 27.

Despite the sharp drop in sales expectations, the one bright spot of the report was the net percentage of small business owners planning to increase inventories, which rose by 5 points to 7, as more owners expected a strong quarter.

The employment front also remained very strong, with the net percentage of business owners planning to increase employment rising by 1 point to 19 while current job opening slipped by just a point to a still exceptionally strong 30.

Though the level of optimism remains very high by historical standards and despite the month’s decline still surpasses any month in previous years going back to 2006, the September survey indicates the frothy expectations of business-friendly health reform and lower corporate taxes have cooled noticeably in September. Moreover, NFIB noted that optimism may have actually declined more than its survey indicates, since it was likely that reporting members in Florida and Texas were underrepresented because of disruptions.

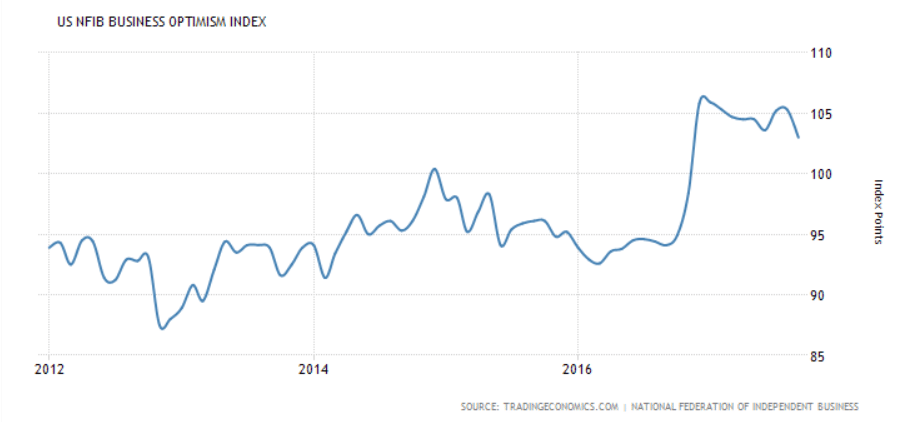

Optimism Among US Small Businesses at 10-Month Low

The NFIB’s Index of Small Business Optimism in the US fell to 103 in September 2017 from a six-month high of 105.3 in August, and below market expectations of 105.1. It was the lowest reading since November last year, as 6 of 10 index components declined: Higher sales expectations (-12 pp to net 15 percent); good time to expand (-10 pp to 17 percent); plans to make capital outlays (-5 pp to 27 percent); expectations the economy will improve (-1 pp to 30 percent); current job openings (-1 pp to 30 percent); and expected credit conditions (-1 pp to -3 percent). On the other hand, earnings trends were flat (at -11 percent) and improvement was observed for: Plans to increase inventories (+5 pp to 7 percent); current inventory (+2 pp to -3 percent); and plans to raise employment (+1 pp to 19 percent).

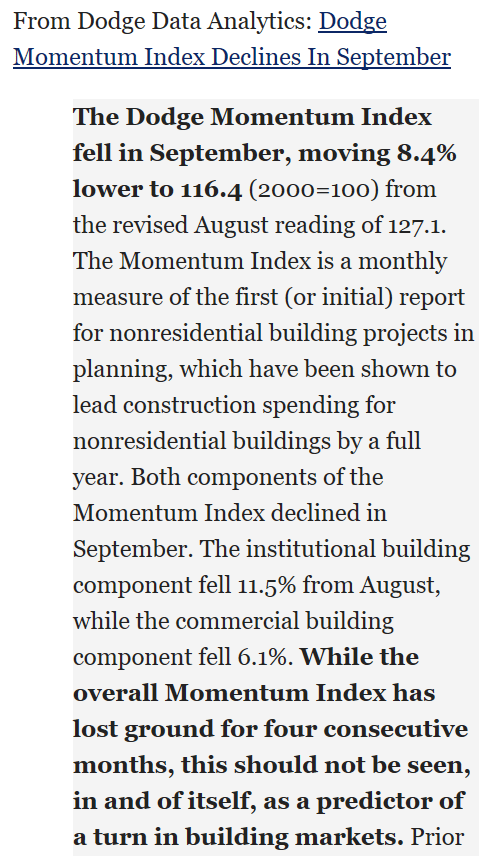

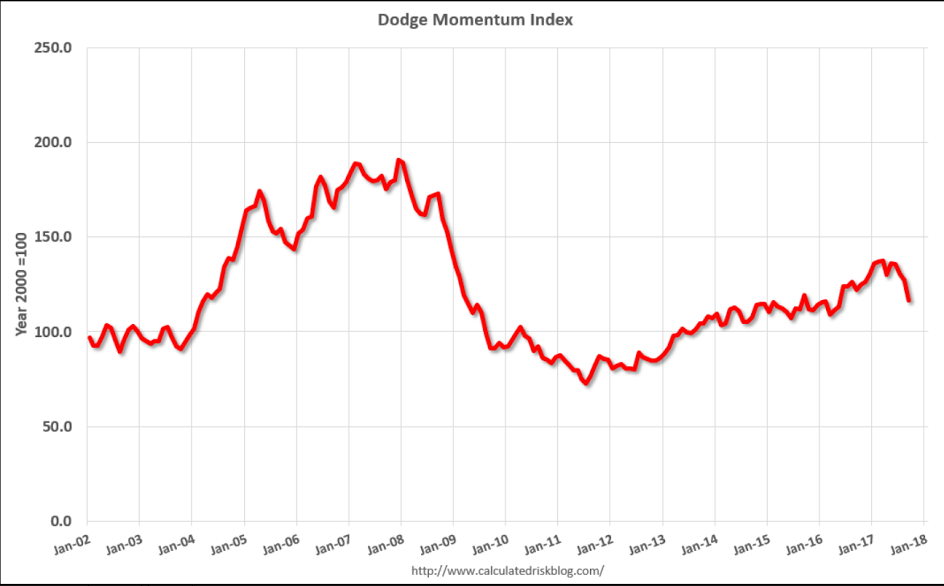

This index is down in line with decelerating commercial real estate bank borrowings:

A few comments on share buybacks:

Once a company decides it has ‘excess cash’ the options are dividend payments or share buybacks.

After a dividend payment the company has that much less cash and shares outstanding remain the same.

After a share buyback the company has that much less cash and shares outstanding are reduced.

Now consider that after a reverse split the company has the same cash and there are fewer shares outstanding.

Therefore, for the company, share buybacks are functionally equivalent to a dividend payment combined with a reverse split, as in either case the company has less cash and there are fewer shares outstanding.

But for executive compensation related calculations, a reverse split reduces share count or increases option strike prices, while buybacks do no alter executive share count and option strikes.

Seems the accounting process should disclose any increases in executive compensation due to share buybacks?

Seems the accounting process should disclose any increases in executive compensation due to share buybacks?