Bill Mitchell to lead a discussion on the Job Guarantee at the European Commission’s conference this week.

Jobs 4 Europe: The Employment Policy Conference

Job guarantee: Concept and implementation

Bill Mitchell to lead a discussion on the Job Guarantee at the European Commission’s conference this week.

Jobs 4 Europe: The Employment Policy Conference

Job guarantee: Concept and implementation

Exchange Rate Policy and Full Employment

By Warren Mosler

>

> Posted By Warren Mosler on January 15, 2003 at 13:04:00:

>

> Here’s what’s being set up.

>

> 1. Bush tax stuff is way too small to turn the economy.

>

> 2. Over the next 24 months the economy weakens as the deficit grinds its way to the usual

> 5% of gdp or more – $500 billion + – mainly through falling revenue as unemployment

> rises, corporate earnings wither, etc.

>

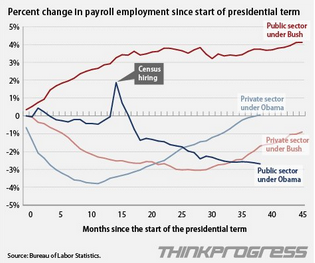

A month or so after this was written I met with Andy Card, Bush’s chief of staff, and told him much the same. He got it and they took immediate action to increase spending and cut taxes. It was shortly after that meeting that Bush was asked about the deficit and said he doesn’t look at numbers on pieces of paper, he looks at jobs, and did all he could to make the deficit as large as possible. It got up to 200 billion for Q3 or about 800 billion annually; enough to turn the economy enough to not lose the election.

>

> 3. Hillary Clinton wins the Presidency by a landslide promising to increase taxes on the

> rich to assist the poor and balance the budget.

>

I forget why she didn’t run and/or lost to Kerry?

>

> 4. After the innaguration the program gets passed while the federal deficit remains around

> $600 billion.

>

> 5. The economy recovers as it always does after a couple of years of 5%+ deficits restore

> non govt net financial assets/savings/aggregate demand.

>

This is pretty much what happened under Bush.

>

> 6. Once again the Clintons ‘prove’ balancing the budget is good for the economy and win

> two terms.

>

> 7. Half way into her 2nd term the strong economy drives the budget into surplus further

> proving Clintonomics.

>

This happened under Bush as the strong economy driving by private credit expansion took the deficit down to 1% of GDP by mid 2006. Unfortunately the expansion included the sub prime fraud which was seriously unsustainable.

>

> 8. The next president is Hillary’s VP who gets the votes counted in his favor this time.

>

> 9. This next president gets clobbered with another economic downturn caused by the

> previous surplus, and the federal budget goes into deficit.

>

It happened during the last few months of the Bush administration. And Obama did get clobbered by it.

>

> This time they aren’t ‘fooled’ by Bush style tax cuts anymore, and try instead to again raise

> taxes on the rich to assist the poor and balance the budget, but they do it too soon, before

> the deficit is large enough to turn the economy, and it gets much worse.

>

My timing was far from perfect, but not terrible for a 10 year forecast?

Any other 10 year forecasts from back then on record?

Bill on top of his game here:

This Could Change Everything

By Dick Wagner

Romney and Ryan’s Disastrous Economic Plan

By John T. Harvey

Actually down a tick this month, but looks to me like it’s bottomed, though after getting back to levels not seen since women started entering the labor force.

As previously discussed, looking good for stocks, the euro, wti crude, and not so good for bonds which may have touched cyclical lows in yields.

A few more modest ‘green shoots’ including US personal income up .5, a few more jobs, houses and cars looking reasonable firm, etc. and markets starting to ‘undiscount’ a US recession.

Govt deficits remain plenty high to support income/sales/employment at current (depressed) levels and promote modest growth. Just as in the prior two double dip panics of the last several years, markets and the mainstream tend to give little if any weight to the notion that large deficits support aggregate demand. (Interesting how ideology seems to be adversely influencing their forecasting.)

So right now I see no fundamental reason for a meaningful drop in aggregate demand, apart from a politically driven external shock of some sort from Europe or maybe Iran, where there have been a few too many very recent noises regarding an Israeli attack for comfort.

Swiss Manufacturing Slump Unexpectedly Eases on Output Gain

By Simone Meier and Klaus Wille

August 2 (Bloomberg) — Swiss manufacturing contracted at a slower pace in July than in the previous month as companies stepped up production, suggesting that the economy is weathering Europe’s deepening slump.

The procure.ch Purchasing Managers’ Index rose to 48.6 from 48.1 in June, when adjusted for seasonal swings, Credit Suisse Group AG said in an e-mailed statement today. That’s the highest since March. A reading below 50 indicates contraction.

Marginal rise in construction output, but new orders continue to decline during July

August 2 (Markit) — At 50.9 in July, up from 48.2, the Markit/CIPS Construction PMI rebounded slightly from June’s two-and-a-half year low. However, the latest reading was well below the long-run series average (54.2). Growth was largely confined to the commercial sub-sector in July, as house building and civil engineering activity continued to decline. July data indicated a further reduction in new work received by construction companies. Although the rate of decline eased over the month, it was still the second-fastest since January 2010. Survey respondents widely cited a lack of new opportunities to tender and a general weakness in underlying market demand.

Sweden Krona Jumps as Rate Cut Calls Fade on Accelerating Growth

By Stephen Treloar and Johan Carlstrom

August 1 (Bloomberg) — Sweden’s krona surged, posting the biggest gains of all major currencies, after a report showed manufacturing unexpectedly expanded, damping speculation the Riksbank will cut interest rates at its meeting next month.

The krona rose as much as 0.8 percent to 8.2979 per euro, the highest since Sept. 11, 2000, and was up 0.5 percent at 8.3217 as of 1:15 p.m. in Stockholm. It surged almost 0.9 percent against the dollar to 6.7411, a three-month high. It gained against all 16 major currencies tracked by Bloomberg.

An index based on responses from purchasing managers rose to a seasonally adjusted 50.6 in July from 48.4 the previous month, Stockholm-based Swedbank AB said today. A reading above 50 signals an expansion. It was estimated to drop to 47.7, according to the median estimate in a Bloomberg survey.

“Following the surprisingly strong GDP number Monday this gives further ammunition for unchanged Riksbank rates at the September meeting and lends additional support to krona appreciation,” said Claes Maahlen, head of trading strategy at Svenska Handelsbanken AB in Stockholm, in a note today.

Sweden has been able to avoid a recession this year as companies such as retailer Hennes & Mauritz AB and Sandvik AB have benefitted from demand outside Europe and as the central bank cut interest rates. The economy expanded 1.4 percent in the second quarter as increased exports of services offset a decline in the export of goods. Consumer spending also rose.

The yield on Sweden’s two-year notes increased three basis points to 0.9 percent.

Karim writes:

June DGOs/July 20 Claims-Weaker CapEx; Jumpy Claims