Just heard 10 year US credit default swaps are at 35 basis points.

The Fed needs to sell this in unlimited quantities and drive the price to near 0 to help restore and normalize liquidity.

[top]

Just heard 10 year US credit default swaps are at 35 basis points.

The Fed needs to sell this in unlimited quantities and drive the price to near 0 to help restore and normalize liquidity.

[top]

[Skip to the end]

As this goes down, the value of AIG (and probably Lehman) goes up.

[top]

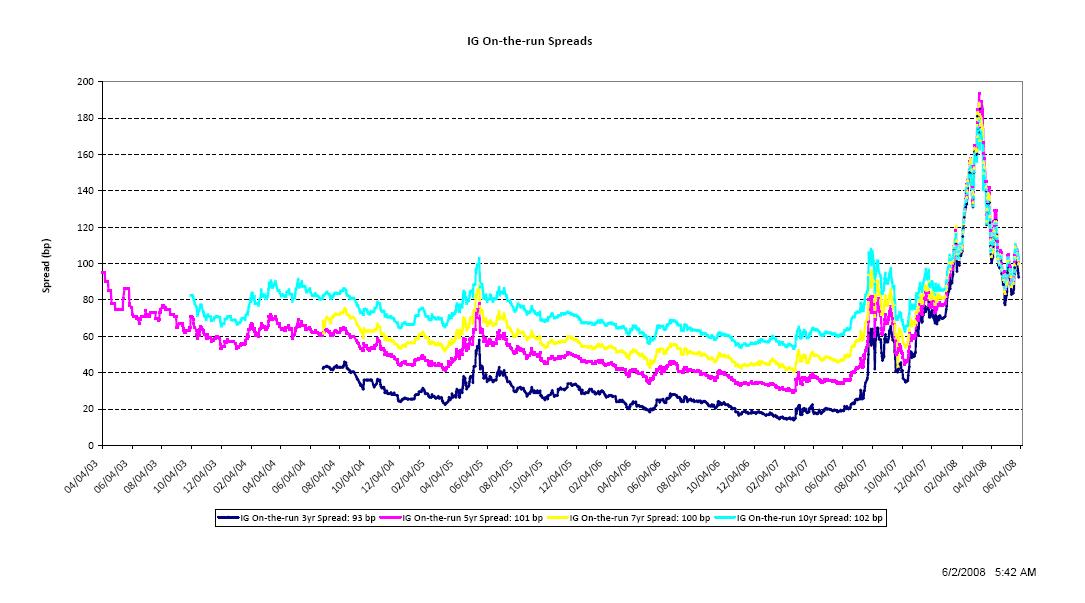

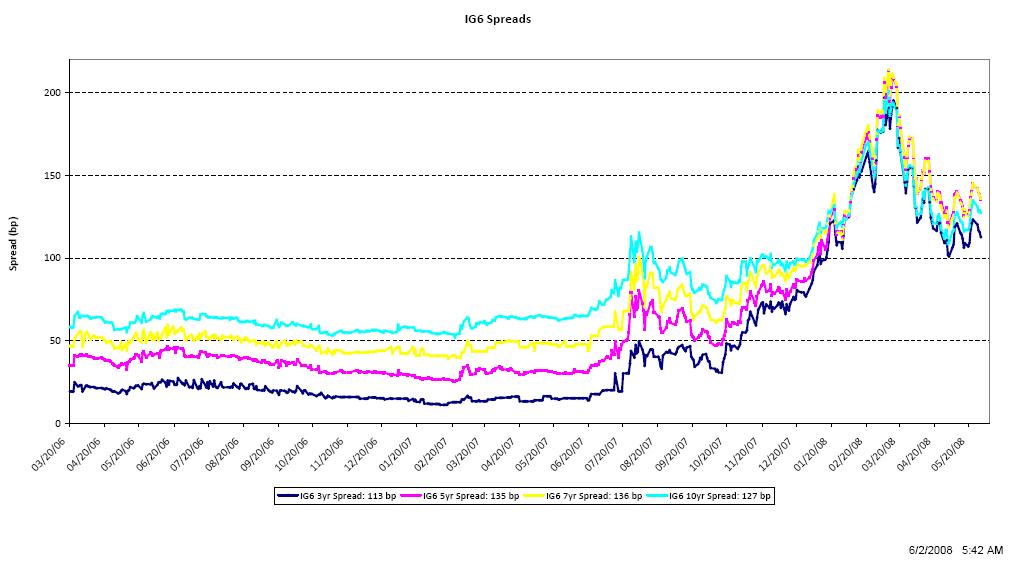

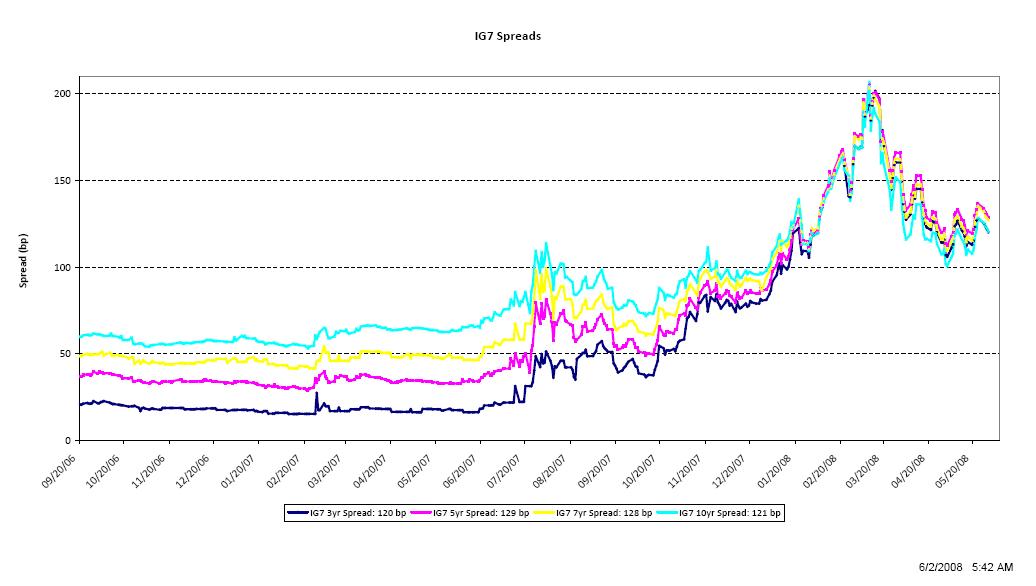

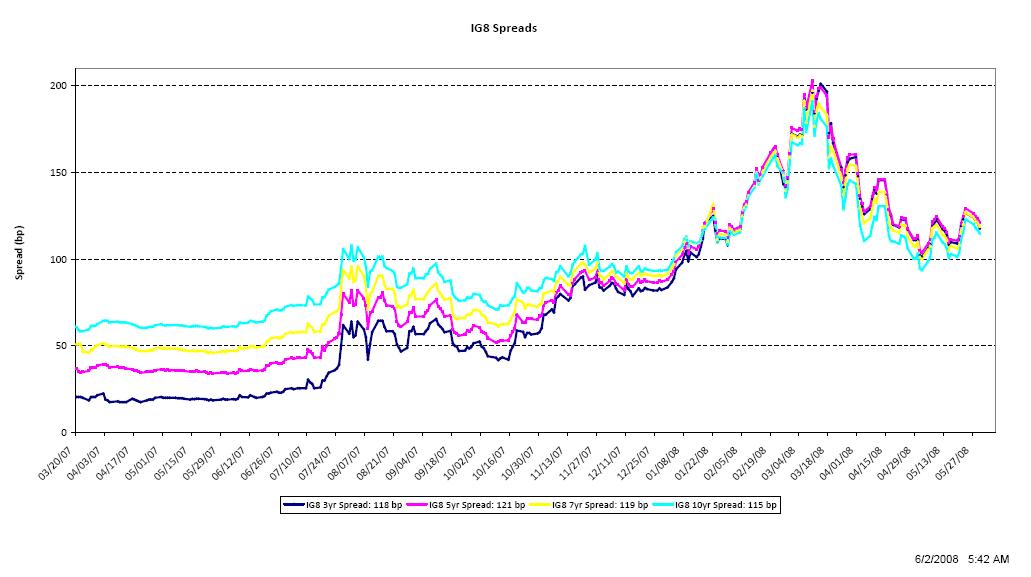

Should resume narrowing from here.

[top]

Seems these spreads relate directly to the equity markets, which are simply that last step down in the capitalization.

I’ll be looking to see if the equity markets can rally much without these spreads tightening as well.

[top]

[top]

Combined commercial and industrial loans and commercial paper show a leveling off after the initial drop.

Back in mid 2006, I remember commenting that I thought the government deficit was no longer high enough (given everything else that was going on) to support the credit structure.

The last push up was largely a product of fraudulently obtained sub prime and Alt-A loans.

[top]

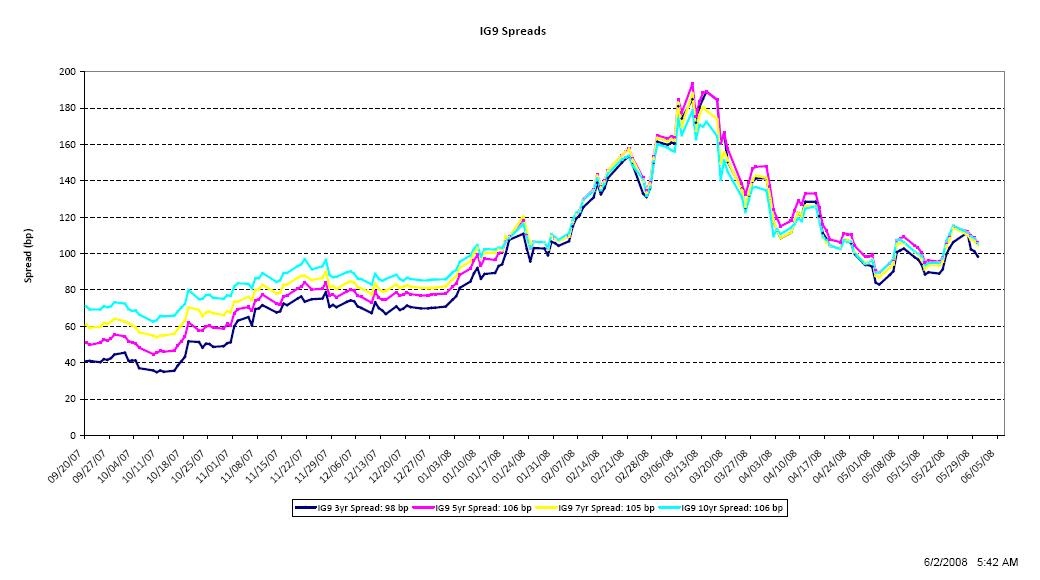

Looks and feels like spreads will be generally narrowing for a considerable period of time.

Bank earnings are better than expected with revenues growing nicely.

GDP, income, and spending being sustained by a growing government budget deficit, exports, and housing leveling off and no longer subtracting from growth.

‘Inflation’ continues with Saudi’s supporting prices and pass-throughs intensifying.

[top]

[top]

Still working its way higher.

[top]

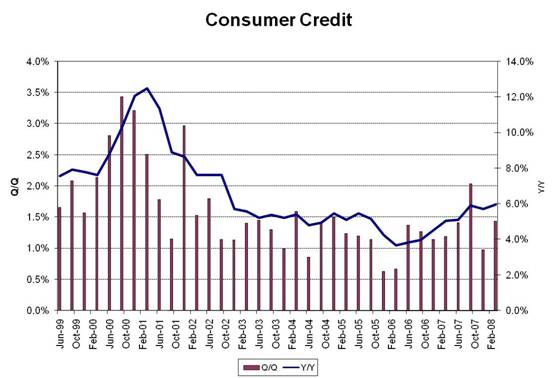

Moving up some, supporting spending at muddle through ‘better than recession’ levels, but not a bubble yet, as happened at the turn of the century.

[top]

Pricing of risk looking more like it’s settling into a range.

[top]