You’re the best!!

Still laughing!!!

Bill on top of his game here:

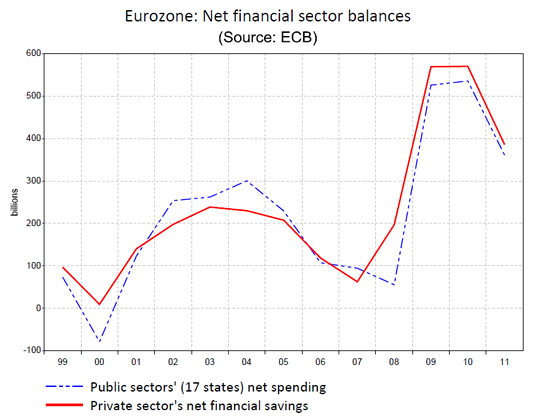

There’s a reason the hardcore budget balancer/deficit hawk does not last long under the microscope. Their numbers can’t add up, which leaves them with contradictory statements.

Why can’t they add up? The dollar is a ‘closed system’, what’s called a case of ‘inside money’ due to the fact that they all come from govt and/or its designated agents (apart from counterfeits).

This means the dollars in our pension funds, IRA’s, corporate reserves, cash in circulation, foreign central bank reserves, etc. all come from someone else spending more than his income.

Yes, the rest of the private sector can and does often spend a bit more than it’s income to supply those ‘saver’s dollars’ but most of it comes from the $15 trillion or so the US govt has spent in excess of its tax collections. That’s called federal deficit spending.

In fact, the US govt debt is equal to the net dollar denominated ‘savings’ of all the other sectors combined. To the penny. It can’t come from anywhere else.

That means any plan to balance the federal budget is also a plan that doesn’t allow global dollar savings to grow. This means the ‘automatic savings’ like dollars going into and compounding in pension funds, IRA’s, corporate reserves, cash in circulation, and foreign central bank reserves, etc. either can’t happen or are ‘supplied’ by equal private sector debt increases.

So a plan to reduce the deficit $10 trillion from current forecasts is also a plan that either causes private sector debt to increase by that much and/or causes pensions, IRA’s, corporate reserves, cash in circulation, and foreign central bank reserves to decrease by that much.

None of which is consistent with a growing economy, to say the least.

This means, any plan for long term deficit reduction that includes relatively high rates of growth is what can be called a financial optical illusion, that doesn’t hold up on close examination.

And that’s why all the budget balancers ultimately fail. Yes, their headline rhetoric can be casually convincing and even win local elections. But under serious scrutiny, it all falls apart.

But maybe this time it’s different.

:(

This Could Change Everything

By Dick Wagner

Romney and Ryan’s Disastrous Economic Plan

By John T. Harvey

>

> (email exchange)

>

> On Sat, Aug 11, 2012 at 1:32 PM, Paul wrote:

>

> In an op-ed ”Thirty Years Later, a Return to Stagflation” (Op-Ed, Feb. 14), Representative

> Paul D. Ryan, Republican of Wisconsin, argued that the stimulus plan will bring the

> combination of high inflation and high unemployment known as stagflation.

>

> Here is a copy of my February 22, 2009 published letter to the Editor of the New York

> Times evaluating Paul Ryan’s economics.

>

LETTERS; Can We Spend Our Way to Recovery?

February 22, 2009 (NYT)

To the Editor:

Paul D. Ryan repeats the tired idea that when the Federal Reserve prints money for the government to spend on economic recovery, the result will be inflation because ”it is a situation in which too few goods are being chased by too much money.” This is based on a false assumption that the output of the country will not increase when government lets contracts to businesses to produce more goods and services that will improve the productivity and health of our country.

If there is significant unemployment and idle capacity in the private sector (and who can deny that there is?), then this deficit spending will not cause inflation. Rather, the ”printed” money spent on a recovery plan creates profit opportunities that induce private enterprise to hire and produce more goods. Then there will be many more goods available for this money to chase and no inflation need occur.

Paul Davidson

Boynton Beach, Fla., Feb. 14, 2009

The writer is editor of The Journal of Post Keynesian Economics.

A few more modest ‘green shoots’ including US personal income up .5, a few more jobs, houses and cars looking reasonable firm, etc. and markets starting to ‘undiscount’ a US recession.

Govt deficits remain plenty high to support income/sales/employment at current (depressed) levels and promote modest growth. Just as in the prior two double dip panics of the last several years, markets and the mainstream tend to give little if any weight to the notion that large deficits support aggregate demand. (Interesting how ideology seems to be adversely influencing their forecasting.)

So right now I see no fundamental reason for a meaningful drop in aggregate demand, apart from a politically driven external shock of some sort from Europe or maybe Iran, where there have been a few too many very recent noises regarding an Israeli attack for comfort.

Swiss Manufacturing Slump Unexpectedly Eases on Output Gain

By Simone Meier and Klaus Wille

August 2 (Bloomberg) — Swiss manufacturing contracted at a slower pace in July than in the previous month as companies stepped up production, suggesting that the economy is weathering Europe’s deepening slump.

The procure.ch Purchasing Managers’ Index rose to 48.6 from 48.1 in June, when adjusted for seasonal swings, Credit Suisse Group AG said in an e-mailed statement today. That’s the highest since March. A reading below 50 indicates contraction.

Marginal rise in construction output, but new orders continue to decline during July

August 2 (Markit) — At 50.9 in July, up from 48.2, the Markit/CIPS Construction PMI rebounded slightly from June’s two-and-a-half year low. However, the latest reading was well below the long-run series average (54.2). Growth was largely confined to the commercial sub-sector in July, as house building and civil engineering activity continued to decline. July data indicated a further reduction in new work received by construction companies. Although the rate of decline eased over the month, it was still the second-fastest since January 2010. Survey respondents widely cited a lack of new opportunities to tender and a general weakness in underlying market demand.

Sweden Krona Jumps as Rate Cut Calls Fade on Accelerating Growth

By Stephen Treloar and Johan Carlstrom

August 1 (Bloomberg) — Sweden’s krona surged, posting the biggest gains of all major currencies, after a report showed manufacturing unexpectedly expanded, damping speculation the Riksbank will cut interest rates at its meeting next month.

The krona rose as much as 0.8 percent to 8.2979 per euro, the highest since Sept. 11, 2000, and was up 0.5 percent at 8.3217 as of 1:15 p.m. in Stockholm. It surged almost 0.9 percent against the dollar to 6.7411, a three-month high. It gained against all 16 major currencies tracked by Bloomberg.

An index based on responses from purchasing managers rose to a seasonally adjusted 50.6 in July from 48.4 the previous month, Stockholm-based Swedbank AB said today. A reading above 50 signals an expansion. It was estimated to drop to 47.7, according to the median estimate in a Bloomberg survey.

“Following the surprisingly strong GDP number Monday this gives further ammunition for unchanged Riksbank rates at the September meeting and lends additional support to krona appreciation,” said Claes Maahlen, head of trading strategy at Svenska Handelsbanken AB in Stockholm, in a note today.

Sweden has been able to avoid a recession this year as companies such as retailer Hennes & Mauritz AB and Sandvik AB have benefitted from demand outside Europe and as the central bank cut interest rates. The economy expanded 1.4 percent in the second quarter as increased exports of services offset a decline in the export of goods. Consumer spending also rose.

The yield on Sweden’s two-year notes increased three basis points to 0.9 percent.

It’s getting to be downright embarrassing to be an American…

Treasury Plans Floating Rate Notes, Looks at Negative Rate Bids

By Meera Louis and Cheyenne Hopkins

August 1 (Bloomberg) — The U.S. Treasury Department said today it is developing a floating rate note program that could be operational at least a year away, while it is also looking at capabilities for negative rate bidding.

The U.S. Treasury Department said it plans to sell $72 billion in notes and bonds in next week’s refunding. The Treasury intends to auction $32 billion in 3-year notes on Aug. 7, $24 billion in 10-year notes on Aug. 8 and $16 billion in 30-year bonds on Aug. 9.

“Treasury plans to develop a floating rate note program to complement the existing suite of securities issued and to support our broader debt management objectives,” the department said in a statement today. “The first FRN auction is estimated to be at least one year away.”

The Treasury also said it is “in the process of building the operational capabilities to allow for negative rate bidding in Treasury bill auctions, should we make the determination to allow such bidding in the future.”

The Treasury said that the U.S. debt limit is expected to be reached at the end of this year, and it expects to use “extraordinary measures” to fund the government into early 2013.

The Obama administration said July 27 it is forecasting the federal budget deficit will be $1.21 trillion this year, down from $1.33 trillion projected in February. The U.S. faces a so- called fiscal cliff of higher taxes and reductions in spending on defense and other government programs that will take effect at year-end unless Congress acts.

“I think it’s pretty clear that the Treasury has to tread lightly,” William O’Donnell, head U.S. government bond strategist at the Stamford, Connecticut-based RBS Securities primary dealer unit of Royal Bank of Scotland Group Plc., said by e-mail before the report. “There is a lot of uncertainty in the near-future path(s) of outlays and receipts and the fog may not lift until the fiscal issues are addressed.”