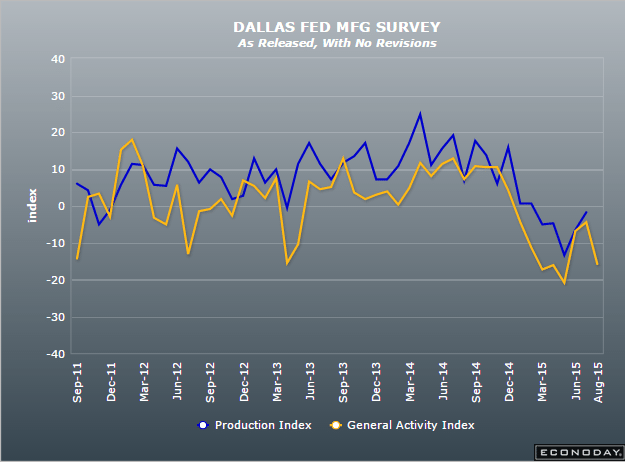

Shockingly negative:

Dallas Fed Mfg Survey

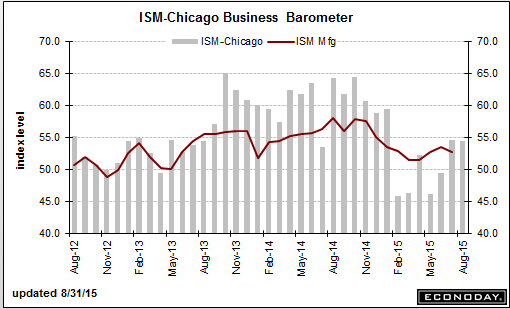

Not so good:

Chicago PMI

Highlights

The headline for August looks solid, at 54.4 for the Chicago PMI, but the details look weak. New orders and production both slowed and order backlogs fell into deeper contraction. Employment contracted for a fourth straight month while prices paid fell back into contraction. Lifting the composite index are delays in shipments which point to tight conditions in the supply chain. Inventories rose sharply in the month and the report hints that the build, despite the weakness in orders, was likely intentional. But strength is less than convincing and this report suggests that activity for the Chicago-area economy may be flat going into year end.

Japan : Industrial Production

Italy : Retail Sales

Highlights

Retailers had another poor month in June as nominal sales fell 0.3 percent versus May when they declined a slightly steeper revised 0.2 percent. Unadjusted annual growth actually accelerated from 0.1 percent to 1.7 percent but this was due to extra shopping days in this year’s report. Volume purchases were also 0.3 percent lower on the month.

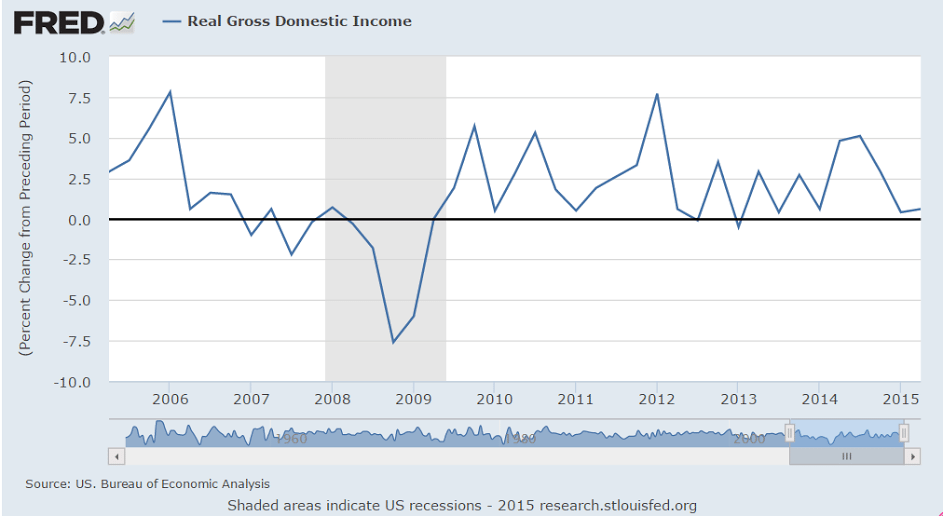

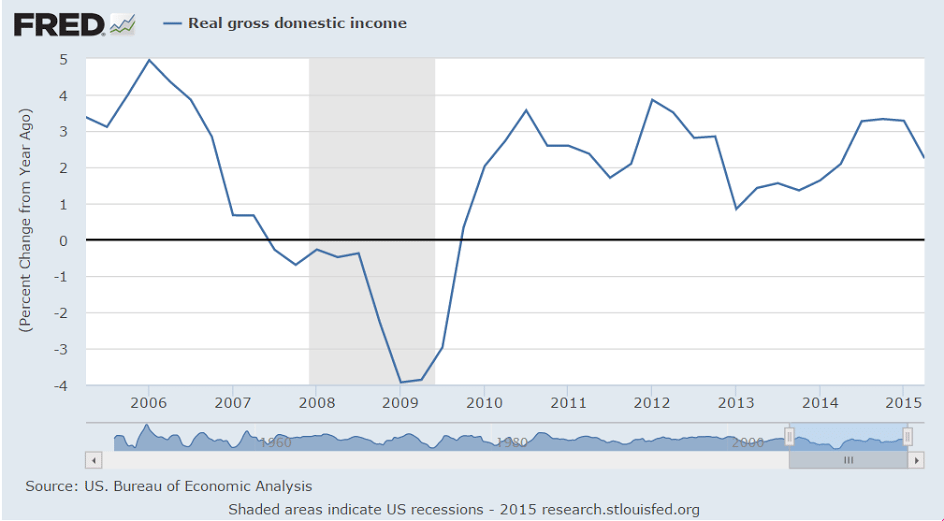

Real gross domestic income (GDI) was up at only a .6% annual rate, only a bit higher than Q1, and in contrast to GDP being up 3.7% for the same quarter. This time looks to me like it’s GDP that’s out of line, as per my narrative where I don’t see any signs of any other sector stepping up and replacing the GDP supported by the now lost oil capital expenditures:

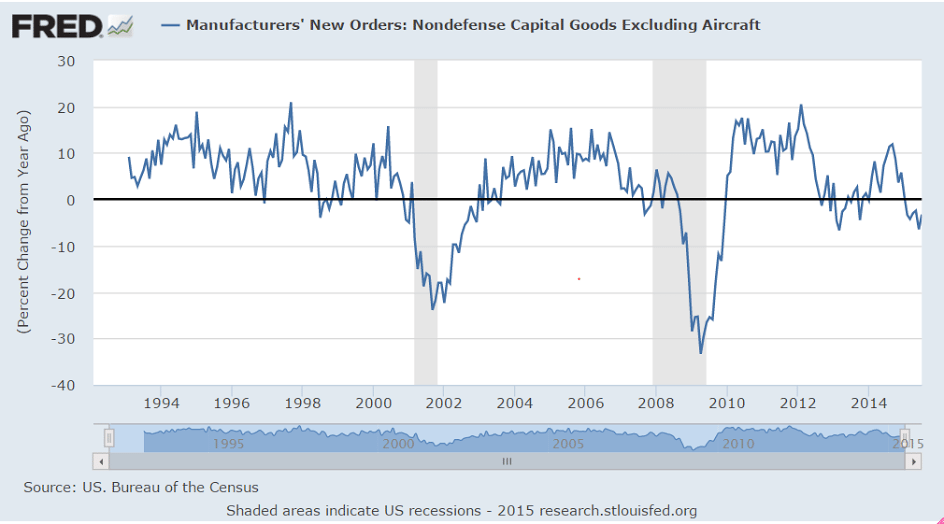

The capital goods sector remains in retreat:

Lots of anecdotals don’t jibe with 3.7% growth:

21 August 2015: ECRI’s WLI Growth Index Sinks Slightly More Into Contraction

(Econintersect) — ECRI’s WLI Growth Index which forecasts economic growth six months forward – remains in negative territory. This index had spent 28 weeks in negative territory then 15 weeks in positive territory – and now is in its second week in negative territory.

Rail Week Ending 22 August 2015: Some Improvement But Continued Deterioration Of Year-over-Year Rolling Averages

(Econintersect) — Week 33 of 2015 shows same week total rail traffic (from same week one year ago) marginally expanded according to the Association of American Railroads (AAR) traffic data. Intermodal traffic expanded year-over-year, which accounts for approximately half of movements. but weekly railcar counts continued in contraction.

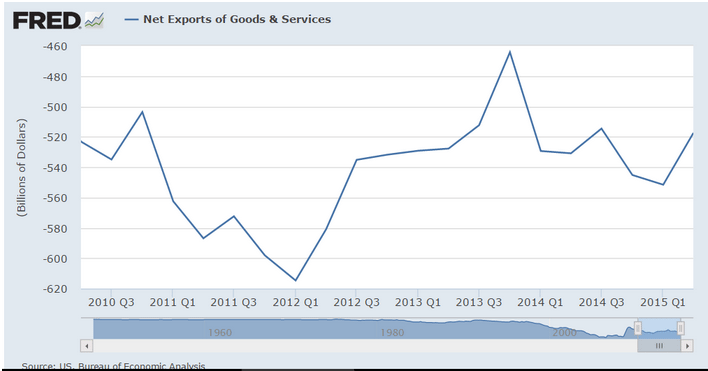

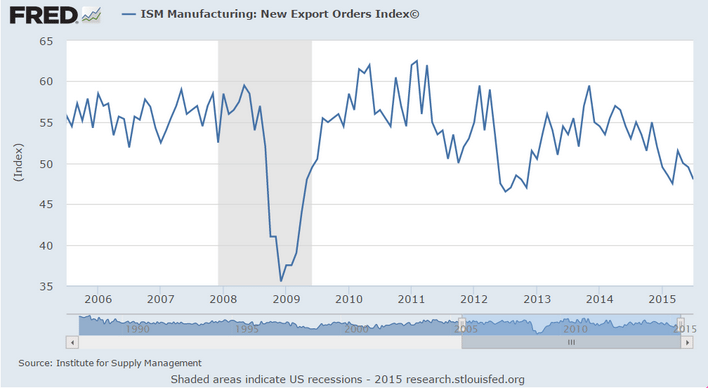

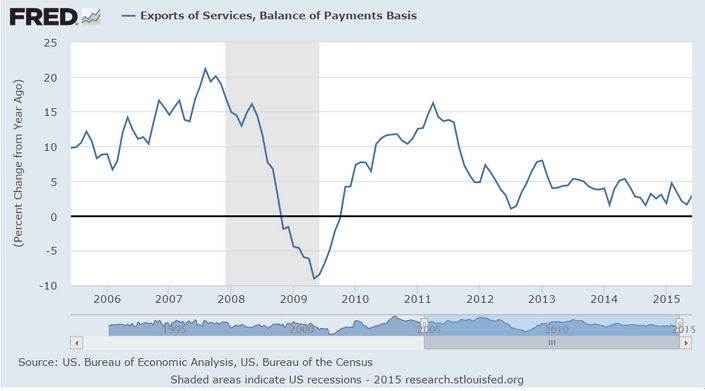

Lots of reasons to suspect net exports will revert in Q3, or be revised down for Q2 as blips up like this latest one tend to quickly reverse, especially with all the surveys showing exports in retreat:

The goods component is looking in full retreat:

And the service component of exports isn’t offering any material support either:

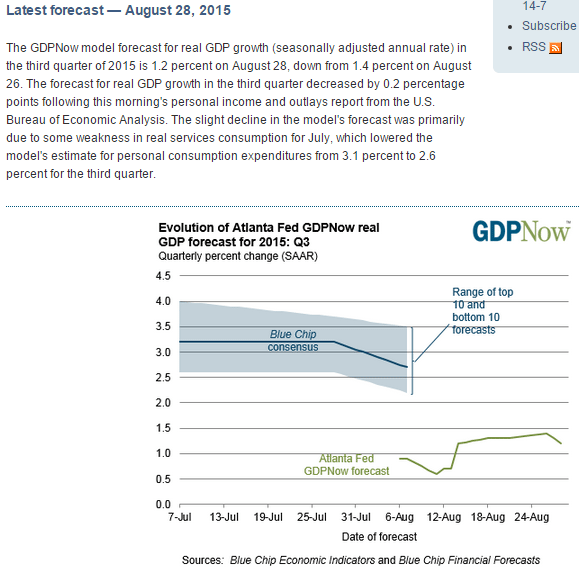

And the Atlanta Fed’s Q3 GDP forecast of only 1.2% remains well below mainstream forecasts: