Nothing good happening here either.

Looks like the jobs report was about 100,000 people taking menial jobs out of desperation again.

:(

Consumer Credit

Highlights

Consumer credit rose $11.6 billion in January vs an upwardly revised gain of $17.9 billion in December. Consumers did go to their credit cards in December, when the revolving credit component rose $6.2 billion, but not in January as the component fell $1.1 billion. As always, the data were boosted by the non-revolving component which rose $12.7 billion reflecting strength in auto financing and the government’s acquisition of student loans. Today’s jobs report underscores the strength of the consumer who, boosted also by low gas prices, has less and less reason to turn to credit card debt to fund purchases.

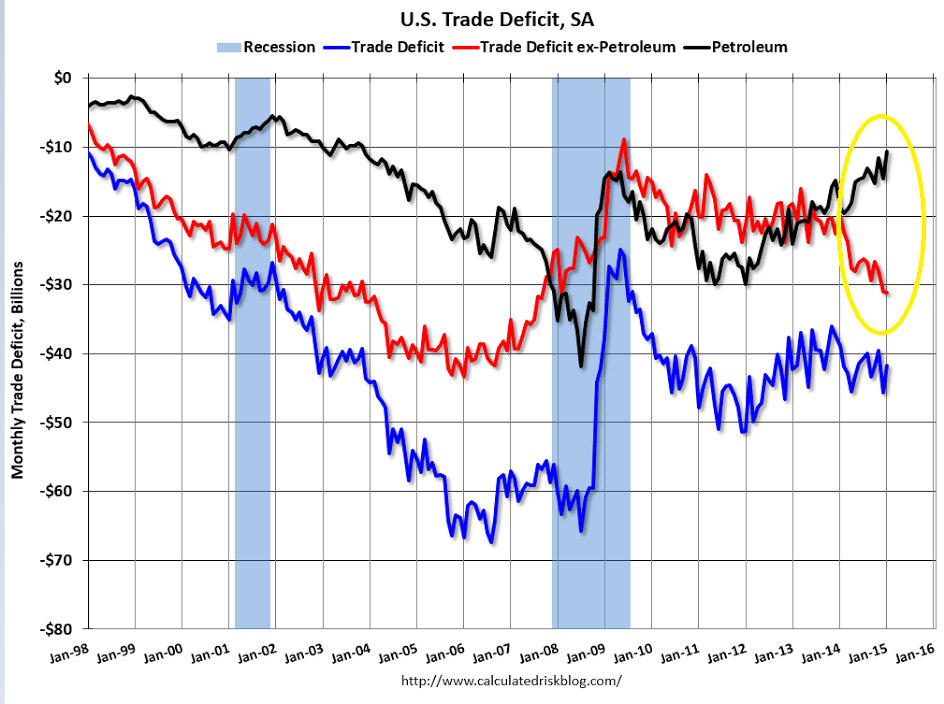

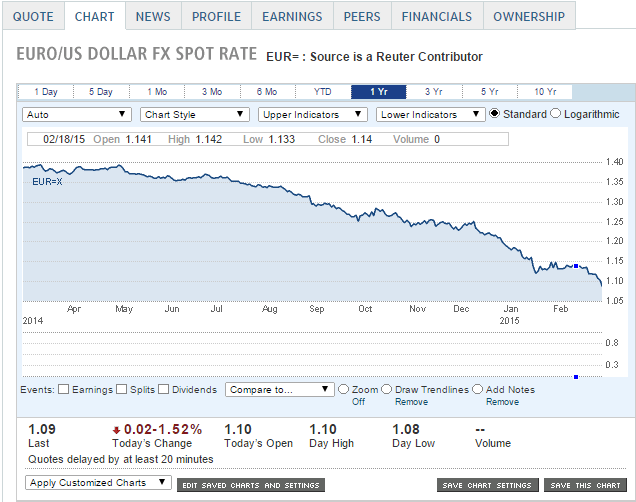

Note the rising trade deficit ex petroleum going up due to the strong dollar from portfolio shifting. And at the same time in the euro zone trade has gone strongly to surplus. This indicate the trade flows remain strongly in favor of the euro even as it declines to new lows due to portfolio managers getting underweight euro and overweight dollars due to misguided notions about QE and interest rates. And this has been happening for quite a while, from back when the dollar/euro was 130. When this shifting is exhausted, and portfolios are left underweight and short with trade removing 20+ billion euro and adding 40+ billion dollars every month to global balances, it all reverses and moves aggressively the other way. But the charts still looking like there’s still more to go as managers react to ECB QE and possible Fed rate hikes: